The ESM-7 certificate is used in organizations that specialize in providing services for the provision of special construction machines. The unified form ESM-7 was approved by Decree of the State Statistics Committee of Russia dated November 28, 1997 No. 78. The document is used to confirm the work performed by construction machines or mechanisms and for the organization’s settlements with customers.

How to fill out the ESM-7 form? What information needs to be included in the certificate, on what basis to fill out the document, and who should participate in filling it out, we will consider in detail below.

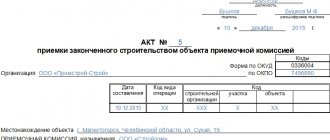

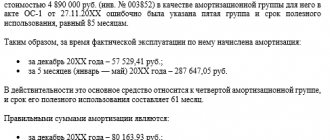

ESM-7 (filling sample)

In the header of the document, you must fill in the date the certificate was completed, information about the organization (name, company address, contact phone number, OKPO code). In the process of filling out ESM-7, detailed information about the customer is also indicated: name of the company that is the customer, address, contact phone number, OKPO code.

The ESM-7 certificate contains data about the object (name of the object and address of its location), name and make of the car, state license plate. In addition, it is necessary to indicate the driver’s details (last name, first name, patronymic).

Filling out the ESM-7 certificate should not cause any difficulties. The form consists of one sheet. The main part of the help contains a table of five columns in which the following information must be reflected:

- Name and code of the type of work;

The number of machine hours worked by construction equipment;

The cost of one machine hour and the work performed (all machine hours worked).

Below the table you need to summarize the data. In addition, ESM-7 (certificate of work performed, services) contains data on downtime due to the fault of the customer - they must be displayed under the table with the data. Next, you need to reflect the total data, the amount of tax (VAT) and the total amount including VAT. In the completed ESM-7 (sample presented below) you can see how this needs to be done. Under the table, you must write down the number of machine hours in words, by hand. The cost of work (or services) is indicated in the contract prices at which settlements between the customer and the contractor are made.

The ESM-7 certificate (a sample form is provided at the end of the article) must be signed by the customer and the contractor, indicating the position and a transcript of the signature. The ESM-7 certificate is drawn up in one copy by representatives of the customer and the organization performing the work or services. To fill out the ESM-7 certificate, you must use the data from the waybill (the waybill is filled out using the ESM-2 form) or data from reports.

A report on the operation of the tower crane is filled out using Form ESM-1. This document is used to account for the operation of various types of cranes (tower, stationary, self-propelled, etc.). The report is the basis for obtaining initial data when calculating wages for drivers.

A report is filled out using the ESM-3 form to record the work of construction equipment at an hourly rate, which is the basis for obtaining initial data when calculating wages for service personnel.

Thus, when filling out the certificate, you must use the information specified in the listed documents. It must be remembered that for each waybill for the operation of a machine or other mechanism, a separate ESM-7 certificate must be issued (you can find the certificate at the end of the article).

For example, the equipment worked for several days for one customer. A separate vehicle waybill has been compiled for each day (form ESM-2). In this case, the number of issued certificates will be equal to the number of vehicle waybills. For example, five waybills have been issued. This means there should also be five certificates.

The ESM-7 certificate (a sample and certificate form can be found at the end of the article) must be certified by the customer’s seal. The completed certificate is sent to the accounting department of the organization, which uses it as an attachment to the document that will be issued to the customer for payment. Thus, the only copy of the certificate is transferred to the accounting department and the other party does not have a copy in hand.

We rent out special equipment. For each trip we fill out ESM-2 (waybill). At the moment, the equipment worked on 02/17, 02/20, 02/25, 03/03, 03/06 (the total number of hours for these days is 40) for one customer. We have five ESM-2.

For each waybill in the ESM-2 form, a separate ESM-7 certificate is issued (Resolution of the State Statistics Committee of Russia dated November 28, 1997 No. 78). You cannot issue one certificate. For each ESM-7 certificate you need to create an invoice.

The lessor must issue an invoice within five calendar days from the moment the services for leasing special equipment were provided (clause 3 of Article 168 of the Tax Code of the Russian Federation). The date of provision of services under the equipment rental agreement is determined by the ESM-7 certificate. Indeed, according to the Decree of the State Statistics Committee of Russia dated November 28, 1997 No. 78, the certificate is used to make settlements between the organization and customers and to confirm the work (services) performed by construction machines (mechanisms).

Oleg the Good,

Head of the Corporate Income Tax Department of the Department of Tax and Customs Policy of the Ministry of Finance of Russia

How often should the landlord invoice the tenant? The lease agreement is concluded for a long term. According to the agreement, monthly acts on the provision of rental services are not drawn up

The procedure for issuing invoices does not depend on the preparation of acts on the provision of rental services. The lessor must issue an invoice within five calendar days from the moment the services for leasing the property were provided (clause 3 of Article 168 of the Tax Code of the Russian Federation). This is explained by the fact that services are sold (consumed) in the process of their provision (Clause 5, Article 38 of the Tax Code of the Russian Federation). Documents confirming the provision of rental services are:

- lease contract;

- act of acceptance and transfer of property to the tenant.

Thus, unless otherwise provided by the lease agreement, monthly preparation of acts on the provision of services for the provision of property is not necessary.

With regard to lease agreements, the validity of which covers more than one tax period for VAT, the financial department provides the following explanations (letter of the Ministry of Finance of Russia dated April 4, 2007 No. 03-07-15/47). If the terms of the lease agreements do not provide for advance payment for services, then the lessor must determine the VAT tax base on the last day of the quarter in which the services were provided (March 31, June 30, October 31 and December 31). Accordingly, within five calendar days after the end of each quarter, the lessor must issue an invoice to the lessee for services provided in the expired period. It is explained this way. For tax purposes, a service is recognized as an activity whose results do not have material expression (clause 5 of Article 38 of the Tax Code of the Russian Federation). As part of the lease agreement, the lessor provides rental services to the tenant continuously (daily) during the entire term of the agreement. Therefore, the lessor is obliged to determine the tax base for VAT based on the results of each quarter (clause 1 of article 54, clause 4 of article 166 and the Tax Code of the Russian Federation). It is impossible to issue invoices ahead of schedule (until the period in which rental services are provided is completed) (letters from the Ministry of Finance of Russia dated February 8, 2005 No. 03-04-11/21 and dated July 2, 2008 No. 03-07- 09/20

From the legal framework

RESOLUTION OF THE GOSCOMSTAT OF RUSSIA DATED 28.11.1997 No. 78 “On approval of unified forms of primary accounting documentation for recording the work of construction machinery and mechanisms, work in road transport”

Certificate for settlements for work (services) performed

(Form N ESM-7)

“Used for making settlements between the organization and customers and for confirming work (services) performed by construction machines (mechanisms).* For each report (waybill) for the work of a construction machine ( mechanism) a separate certificate is issued. Drawed up in one copy by representatives of the customer and the organization performing the work (services) based on the data of the waybill (form N ESM-2) or reports (forms NN ESM-1, ESM-3).* The certificate is certified by the customer’s seal and transferred to the organization’s accounting department , which uses it as an attachment to a document issued to the customer for payment. The cost of work (services) is indicated in contract prices at which settlements between the customer and the contractor (mechanization department) are made.”

Question answer

Fill out form No. ESM-7

A construction organization rents an excavator. He worked 200 hours in a month. Is it possible in

Form No. ESM-7

indicate the total number of hours or do you need to schedule the work by day?

You can enter the total number of hours for the month.

The fact is that form No. ESM-7 is a derivative document, since it is drawn up on the basis of contractual documents and forms

Which subject is it used by?

It is used in organizations specializing in the provision of services for the provision of construction machines (mechanisms).

How many copies are compiled?

Compiled in one copy.

Which employee compiles

Compiled by representatives of the customer and the organization performing the work (services).

4.

Help for payments for work (services) performed. Form ESM-7

Which confirms

The certificate confirms the volume and cost of work performed (services provided).

It is necessary to take into account that the certificate is a derivative document, since it is drawn up on the basis of contractual documents and forms ESM-1, ESM-2, ESM-3.

Application procedure

The certificate is used to make settlements between the organization and customers and to confirm the work (services) performed by construction machines (mechanisms).

It is compiled in one copy by representatives of the customer and the organization performing the work (services) based on the data from the waybill (form N ESM-2) or reports (forms NN ESM-1, ESM-3).

The certificate is certified by the customer's seal and submitted to the accounting department of the executing organization, which uses it as an attachment to the document issued to the customer for payment (for example, an attachment to an invoice, etc.).

Thus, a single copy of the certificate is transferred along with the invoice from the accounting department of the executing organization to the accounting department of the customer organization.

A separate certificate is issued for each report (waybill) for the work of a construction machine (mechanism).

The cost of work (services) is indicated in contract prices at which settlements between the customer and the contractor (mechanization department) are made.

Storage

The certificate is stored in the accounting department of the customer organization along with the payment document (as an attachment to the invoice, invoice, etc.).

Scheme for compiling a certificate

Arbitration practice

Arbitration practice in tax disputes

1. An organization carrying out activities for the reception and disposal of solid waste has the right to take into account the costs of paying for environmental protection works, regardless of the availability of standard forms ESM-1, ESM-2, ESM-3 and ESM-7, since it is not a specialized construction organization (Resolution of the Federal Antimonopoly Service NWZ dated 06/04/2007 N A56-11660/2006).

Comments on this case are set out in the “Arbitration Practice” for the report on the operation of a tower crane in Form N ESM-1.

2. The decision of the court of first instance was overturned, the case was sent for a new trial, since the court did not evaluate the arguments of the tax authority about the absence of standard forms ESM-6 and ESM-7 when documenting expenses (Resolution of the Federal Antimonopoly Service of the Central District of May 31, 2005 N A64-5332 /04-17).

A construction vehicle waybill (form ESM-2) is an important document that serves as the basis for transferring wages to employees: those who work on tractors, graders, bulldozers, excavators, pipe layers and other construction machines.

FILES

Let's sum it up

- A waybill is a corporate accounting document that confirms the fact of expenses. There is no unified form of the document, but there is a list of required details.

- The company independently develops the travel document form. It must be approved by order of the manager, otherwise the tax office will not accept the expenses and will charge additional taxes.

- The order is drawn up in any form and notified to the responsible employees against signature. A sample of the completed waybill must be attached to the document.

If you find an error, please select a piece of text and press Ctrl+Enter.

Description of the parties

The document must be completed on both sides. This design is convenient when signing. On the one hand, the contractor (persons who provide services related to the work of the construction machine itself) signs, and on the other, the customers. Also on the second side there is a special column for an accountant who calculates the salary of a specific employee.

First side

The first one contains:

- OKUD form (0340002);

- reference to Resolution No. 78 of the State Statistics Committee of November 28, 1997, according to which the paper forms were adopted (this particular one received the number ESM-2);

- the name of the logistics company that provides transportation services, or the name of another company that fulfills the order (with address and telephone number);

- Full name or company name of the customer who hires a construction machine for any of his needs (also with written contact details);

- make and name of the car, its state number, as well as inventory and service records (below);

- Full name of the driver;

- transaction type code;

- period of work (indication of duration of activity);

- information about the column or work area (if available).

After this informative part comes the tabular part. If we are talking about one day, then only one line is filled in. If several days (shifts) are required to complete the work, then each new line should contain information about a separate day.

The tabular section states:

- the date and month in which the service was provided;

- name and address of the object;

- dispatcher signature (separate for each line);

- when the car left, speedometer readings when leaving (in km);

- the driver’s signature stating that the car was in good working order upon departure; the mechanic’s signature will also be required to express his agreement with this fact;

- the time when the equipment arrived at its permanent location, which was visible on the speedometer;

- signatures of the driver - in the delivery of the car and mechanic - that he accepted it upon arrival at the garage (in one column).

A special place in the document is given to fuel consumption. And this is not an accident. Lack of control over the consumption of fuels and lubricants usually leads to their shortage. Thus, the penultimate column of the table is dedicated to fuel and is divided into several sub-items, filled out separately:

- how much fuel was in the tank (or cylinder, if it is gas) when leaving;

- how much was issued to complete the work;

- how much is left upon arrival at the garage.

Also (at the very end of this column of the table) it is necessary to indicate what the actual consumption was and what it should be according to the standards.

Completes the tabular part of the column “Signature of the driver (refueler)”. At its level there are also the names of those who have taken responsibility for performing this type of work. Moreover, there is a place for both parties (on the part of the customer and the contractor). The riggers are not forgotten either. When filling out, it is advisable to write down their full name and service ID numbers.

Order for waybill in 2021

A waybill is a primary accounting document that confirms the fact of economic activity. It must include all the required fields that are required by Art. 9 of the Federal Law of 06.12.11 No. 402-FZ “On Accounting” and clause 1 of Order No. 368. The head of the garage, doctor, drivers, mechanics, dispatchers - everyone who works with the company’s transport must understand the procedure and responsibility for errors in documents.