How to process salary payment

In order to calculate salaries, the accountant uses the T-51 or T-49 statement. A separate statement is drawn up for issuance. The T-53 statement is not intended for issuing wages other than cash, so it will be difficult to use it for this type of payment. To simplify the work, you can use the statement form intended for agricultural complexes No. 415-APK, but in order to use it, this should be specified in the accounting policy of the organization (unless, of course, the company is engaged in non-agricultural activities).

What is provided in natural form

Payment in kind can be made with any property that can be useful or suitable for use by the employee for personal purposes. The following may be issued in kind:

- Finished products;

- Product;

- OS;

- Materials;

- Raw materials, etc.

If the goods that are issued in the form of wages exceed their market value, then such a payment may be considered unreasonable. At the same time, market means the cost of goods, which is established in the employer’s region at the time of payment of wages (

Payment in kind - what is it?

Payment in kind is the payment to subordinates of a part or full salary in kind in the form of products produced by the enterprise, employees or purchased by the company for the purpose of sale.

According to generally established requirements, salaries to subordinates in non-monetary form are given in the form of consumer goods. These often include food products.

More specific cases are often noted when temporary housing is transferred or provided for workers.

Amount of payment in kind

Important! Only part of the salary can be paid in kind. This part should not exceed 20% of the total accrued salary.

There are also situations when an employee asks to give him more than 20% of his salary in kind. In this case, you need to formalize the sale of the property. That is, so that the documents show that the employee received the full amount of the salary, and then bought property in his organization for cash. If the payment amount exceeds the 20% limit, this will lead to claims from the inspection authorities (

Accounting for salaries in kind

Depending on what property the organization plans to give to the employee as salary, accounting operations depend.

| Business transaction | Postings | |

| Debit | Credit | |

| Payment in finished products, goods | ||

| Finished products were issued to the employee as payment for his salary | 70 | 90 subaccount “Revenue” |

| Write-off of the cost of finished products issued in the salary invoice | 90 subaccount “Cost of sales” | 43(41) |

| Payment in materials, OS | ||

| Materials (OS) were issued to the employee as payment for his salary | 70 | 91 subaccount “Other income” |

| Write-off of the cost of materials (OS) transferred on account of salary | 91 subaccount “Other expenses” | 01(08, 10, 21) |

| Write-off of depreciation on retired fixed assets | 02 | 01 |

Tax accounting

The following is calculated from payment of wages in non-monetary form:

- personal income tax;

- Insurance premiums.

The procedure for calculating contributions and personal income tax is the same as in the case of paying salaries in cash equivalent. Personal income tax is calculated at a rate of 13%, so the amount of goods issued is included in the employee’s total income, reduced by standard deductions. To calculate the tax, you need to determine the value of the property transferred to the employee. It is determined based on the price agreed upon between the employee and the employer. In this case, the price is set based on market prices, and it includes VAT, and if excisable goods are transferred, then also the amount of excise tax.

The calculation of other taxes depends on the tax system used by the employer. If an organization pays income tax, then when calculating it, the entire amount of accrued wages is included in expenses, and the form in which it is paid (cash or in kind) does not matter.

If an organization paid out more than 20% of its salary in kind, then it should not be taken into account when calculating income tax. You can only take into account that part of the salary paid in kind that does not exceed 20%. This follows from the following conclusion: as a rule, organizations pay their employees wages in rubles, but part of it (not exceeding 20%) can be paid in kind. At the same time, the company has the right to take into account the accrued salary amount when calculating income tax. It is included in labor costs. Based on this, it is impossible to write off as expenses wages paid in kind in excess of the 20% limit (letter of the Ministry of Finance No. 03-03-05/59). However, such a limit of 20% is provided only by labor legislation. As for the tax authorities, there are no restrictions on accounting for wages as part of labor costs. You can take into account absolutely the entire salary, regardless of the form in which it was issued. But in this case, the organization may have to defend its position in court, since there is still a violation of the law.

How to reflect income in kind in 1C

In this article we will look at how to reflect employee income in kind in 1C programs (ZUP, UPP) and how to withhold personal income tax on such income.

Wages can be paid to employees in cash and non-monetary forms - when instead of money the employee is provided with some goods, work or services. An employee’s income in non-monetary form is called income in kind; it can include payment by an organization for goods, work and services for an employee, for example, payment for food, utilities, training - partially or fully. If an employee receives income in kind, then the tax base of this income is determined as the market value of the relevant goods, works and services.

Additional income of employees in kind, received in addition to the “regular” salary, is registered in the program using an appropriately described additional accrual and the document “Registration of one-time accruals for employees of organizations.”

The first thing that needs to be reflected in the program is an additional type of accrual. It should be described in terms of the types of calculation “Additional accruals of organizations”. You can open it through the “Payroll calculation for organizations” interface in the submenu “Enterprise” - “Salary calculation settings” - “Additional charges”.

In the list of additional charges, create a new element using the “Create” button. On the accrual card we indicate its name, which will reflect the essence of the accrual, and the code. The accrual code must be unique.

On the “Calculations” tab, we set the calculation sequence to “Primary accrual” - that is, the calculation of this accrual will not depend on the calculations of other accruals. We also set the calculation method to “Fixed amount” or “Custom calculation formula”. If a custom calculation formula is selected, it must be configured. Some one-time income in kind may be reflected in a fixed amount.

On the “Usage” tab we do not change anything, we leave all the parameters as default.

On the “Accounting and UTII” tab, set the attribute “Is income in kind.” Setting this attribute ensures that the accrual amount does not increase the “amount payable” to the employee, and accounting entries are not generated for such accruals from the Kt 70 account, but entries can be generated for personal income tax and insurance contributions if the accrual is subject to them.

It is also necessary to indicate the method of reflecting the accrual in regulated accounting. In our example, the method of reflecting accruals is determined based on data about the employee and his planned accruals.

On the “Taxes” tab in the personal income tax group, select and set “Taxed, income code” - you can specify 4800 as the income code - other income.

On the “Contributions” tab, it is necessary to describe the procedure for assessing accrual contributions. The switch in the area “FSS, accident insurance (before 2011)” does not affect accruals after 2011, so it does not matter what position it is set to.

The type of income in the area of “Unified Social Tax (until 2010)” has been used since 2011 to set up the assessment of contributions for insurance against accidents and occupational diseases.

On the “Management Accounting” tab, set up the order in which accruals are reflected in management accounting. There is no need to fill out the “Other” tab.

To save the accrual, click the “Ok” button.

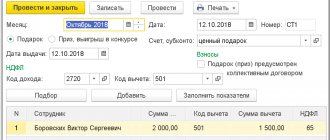

Once the accrual for income in kind has been described, the income must be recorded. It is recommended to register the fact that an employee receives additional income using the document “Registration of one-time accruals for employees of organizations.” You can open the document through the “Salary calculation of organizations” interface, submenu “Salary calculation” - “Primary documents” - “One-time charges”.

Let's create a new document. Income in kind is reflected in this document on the “Additional” tab. accruals." Let's add a new row to the tabular section, indicate the employee who received the income, and the previously created accrual type, which corresponds to income in kind. In the row of the tabular section in the column “Indicators for calculating accrual” we indicate the amount of accrual. We indicate the accrual period. After this, click the “Calculate” button to calculate the accrual result and personal income tax amounts.

The “Personal Income Tax” tab displays the calculated personal income tax amounts for the income registered in the document. Here you can recalculate personal income tax by clicking the “Recalculate” button.

After calculating personal income tax, you should post a document.

Example

LLC "Continent" to employee Petrova O.P. part of the salary for November 2021 was given in kind. The conditions for such payment are specified in the employment contract with Petrova. Petrova’s salary for November was calculated in the amount of 35,000 rubles. Petrova wrote a statement according to which she was given a microwave electric kettle as part of her salary, worth 3,000 rubles, including VAT 458 rubles.

The cost of the kettle at which the organization purchased it was 1,500 rubles, including VAT of 229 rubles. The amount of the teapot does not exceed 20% of the salary. The postings will be as follows:

D44 K70 – Petrova was accrued a salary in the amount of 35,000 rubles;

D70 K68 – personal income tax in the amount of 4,550 rubles was withheld from Petrova’s salary;

D44 K69 – insurance premiums in the amount of 7,700 rubles were accrued on Petrova’s salary;

D70 K90 subaccount “Revenue” - Petrova was given goods worth 3,000 rubles as salary;

D90 subaccount “VAT” K68 – VAT in the amount of 458 rubles was charged;

D90 subaccount “Cost of sales” K41 – the kettle is written off at cost, the amount is 1,271 rubles (1,500 – 229);

D70 K50 – Petrova was given the remaining salary of 27,450 rubles (35,000 – 4,550 – 3,000).

When calculating income tax, income includes the proceeds received from the sale of the kettle, 2,542 rubles (3,000 - 458), expenses include the cost of the kettle, 1,271 rubles (1,500 - 229).

Payment to employees for housing and travel

Sometimes, for employees living in another city, the employment contract provides for payment for both housing and travel home on weekends and to work. Such a payment is not recognized as salary in kind, since it is not payment for the employee’s labor functions. However, such compensation should not exceed 20% of the total accrued salary.

This is due to the fact that the amounts of payments for housing or travel provided for in the employment contract are recognized as wages in kind, which should not exceed 20%.

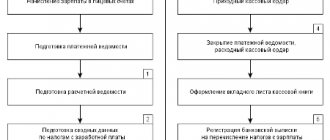

Registration process

The company may give the employee part of the salary in kind if such conditions are specified in the employment contract. If such a decision was made by the organization after the employee was registered, an agreement or a separate document is attached to the employment contract, supplementing the local regulatory act on the employee remuneration system. The employee must be notified of the timing of the introduction of such conditions, since payment in kind can be either temporary (one-time) or systematic.

By agreement with the employer, the employee may refuse payment in this form earlier than the prescribed period. However, if the manager does not give his consent, the payment will be made until the end of the period specified in the contract. Amounts of payments in monetary and non-monetary forms are included in the wage fund.

Before paying wages, the accounting department makes calculations and determines the market value of goods formed as part of the salaries of employees (Article 40 of the Tax Code of the Russian Federation). This amount is reflected in the invoice, according to which workers receive the agreed quantity of the company's products. If an employee takes part of the required salary for services or certain works, their cost is determined based on the provided payment documents, checks, and receipts.

Salaries, regardless of the form of receipt in hand, are subject to taxes and are subject to allocation to mandatory contributions. Therefore, from “payment in kind” the amounts of contributions to the pension fund, accident insurance premiums are necessarily withheld and personal income tax is deducted.

The legislative framework

| Legislative act | Content |

| Article 131 of the Labor Code of the Russian Federation | "Forms of remuneration" |

| International Labor Organization Convention No. 95 of July 1, 1949 | "Regarding wage protection" |

| Letter of the Ministry of Finance of the Russian Federation No. 03-03-05/59 dated March 24, 2010 | “On the procedure for accounting for income tax purposes for wages in kind in excess of 20%” |

| Letter of the Ministry of Finance No. 03-03-06/2/109 dated 08/27/2008 | “On compensation to employees for rent” |

Payment of wages in kind

If the employer, on the one hand, does not have enough available funds to pay wages, and on the other hand, has sufficiently large balances of goods or finished products in the warehouse, he can use one option that is beneficial to him. Give part of the salary not in money, but in goods or products. In what cases is this option possible, what documents need to be drawn up and how this will be reflected in accounting, we suggest you figure it out.

Labor legislation provides for the possibility of paying wages not only in cash, but also in kind.

As a rule, the non-monetary part of wages is paid in so-called consumer goods (food, clothing, household appliances, etc.).

At the same time, in practice, it is common to pay wages not only with one’s own products or purchased goods, but even by providing housing for rent for employees.

It is worth noting that the legislation of the Russian Federation establishes a list of goods that cannot be transferred to employees as wages in kind.

Thus, it is not allowed to pay wages in bonds, coupons, in the form of promissory notes, receipts, as well as in the form of alcoholic beverages, narcotic, poisonous, harmful and other toxic substances, weapons, ammunition and other items in respect of which prohibitions or restrictions have been established for their free circulation (Article 131 of the Labor Code of the Russian Federation).