Standard composition

The law does not contain a list of characteristics by which an object is determined. Traditionally, household supplies mean the following objects:

- Office furniture: sofas, tables.

- Communication equipment: telephones.

- Electronic equipment: cameras, tablets, computers.

- Tools for cleaning the internal and adjacent areas of the enterprise: vacuum cleaners, rakes, mops.

- Fire safety tools: fire extinguishers.

- Lighting tools: lamps, lanterns.

- Toilet supplies: towels, hand drying equipment, air fresheners, toilet paper, soap.

- Stationery: pens, pencils, notepads.

- Household appliances for equipping kitchen premises: microwaves, refrigerators, electric kettles.

The list of accessories will depend on the size of the enterprise and the type of its activity. However, the main list is standard.

Separation of household goods by purpose

- Kitchen. In general, they are represented by devices for cooking. There are products that are indispensable for every housewife: a frying pan, a saucepan, a knife, and forks. But much more coverage is given to products that make the process of cooking and eating easier: garlic jugs, sauté pans, skimmers, graters.

- Cleaning. They can be divided into everyday and special. The first group includes sponges, napkins, rags, floor rags, buckets and mops. But during general cleaning, to simplify the task, the range can be significantly expanded by adding: melamine sponges and microfiber cloths, carpet brushes and glass scrapers.

- For washing. Baskets for clothes, basins for soaking and boiling clothes, ironing boards, clothes dryers and clothespins, brushes and absorbent sponges for washing.

- Country houses. The lion's share of this category of household goods is occupied by gardening tools: rakes, shovels, hoes, hillers of various configurations and purposes, utility carts and storage containers. An integral part is watering equipment: hoses and fittings for them, sprayers, dispensers, pumps and automatic watering systems. At the end of the season, you cannot do without household goods for canning: jars, metal and nylon lids, seaming machines, packaging bags and bags.

- For minor repairs. There is equipment for home craftsmen, which allows them to eliminate emergency situations on their own: sets of keys, pliers, a hacksaw, a hammer, a building level, a stationery knife, taps, drills, etc.

Note! In addition to the listed categories, the hardware store always has related products. It is not included in the main range, but perfectly expands it. Represented by household chemicals, textiles, hygiene and cosmetic products.

Inventory accounting

Accessories will be included in fixed assets only if their use period exceeds a year. This rule is contained in subparagraph “b” of paragraph 4 of the Accounting Rules (PBU). Inventory may be recorded as part of the materials. However, this is permissible only within a certain limit. This limit may be set by the policy of the enterprise itself. However, it cannot be more than 40 thousand rubles. The maximum volume of the limit is established by paragraph 4 of clause 5 of the PBU.

If the useful life does not exceed a year, records are kept in the list of materials. For this purpose, according to paragraphs 2 and 4 of the PBU, the score is 10-9. The introduction of objects is reflected in accounting in a standard manner.

Question: An enterprise purchased inventory and household supplies for its new division, but due to the fact that the division did not start operations, it was forced to sell them. How to reflect this transaction in accounting? View answer

Documentary support

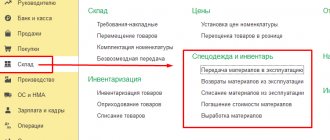

When releasing tools from warehouses, it is necessary to issue a demand invoice. The document is executed according to form No. M-11. The requirement was established by the State Statistics Committee of the Russian Federation in 1997 (resolution No. 71a). The document indicates, in accordance with Order of the Ministry of Finance of the Russian Federation No. 119n, the following information:

- The name of the department that requested the inventory.

- Account number for accounting costs for supporting the activities of the unit.

Accessories can be transferred to an intermediate unit (this concept refers to accounting departments and purchasing departments). In such a situation, it is difficult to determine the exact amount of inventory that will be used by the departments. The way out is to draw up reports as supplies are used up. The acts are drawn up in free form, but they must contain the following information:

- department name;

- number of supplied accessories;

- price;

- the purposes for which the object is requested.

Based on the drawn up acts, objects are written off as expenses. The procedure was approved by MU No. 119n.

How to fill out line 6330 “Acquisition of fixed assets, inventory and other property” in the Report on the intended use of funds?

Accounting in a simplified form

Companies classified as small businesses can conduct accounting in a simplified form. The release of objects involves a connection with the account “Production expenses” or account 44 “Expenses for sales”. The accountant must issue a demand invoice. It is performed according to form No. M-11. At the same time, posting is carried out: DT 25, 26, 44 KT 10-9 (release of objects).

Writing off accessories involves setting a price at which they will be written off. The operation is performed from a count of 10-9. The cost is determined based on the following methods:

- At the cost of one piece.

- FIFO.

- Average cost.

The methods are approved by paragraph 16 of the PBU. The method used must be reflected in the accounting policy. This is needed for accounting purposes. This provision was introduced by paragraph 73 of MU No. 119n.

When reflecting, security control is used. This is due to the fact that when a facility is put into operation, costs are transferred into costs.

Only objects whose service life exceeds a year and are registered in the list of materials are controlled.

The law does not stipulate the procedure for accounting for objects transferred to use. Therefore, it is installed by the enterprise itself. To track the movement of objects across departments, the following documents are used:

- Statement.

- Off-balance sheet accounting.

The chosen option for maintaining papers is fixed in the company policy. Documentation is maintained by an employee with financial responsibility. The Plan does not have an individual off-balance sheet account, and therefore it is created independently. For example, an enterprise opens account 013 “Households. accessories".

When transferring inventory to use, the following transactions are made:

- DT 25, 26, 44 KT 10-9 (release of objects from warehouse).

- DT 013 (accounting of objects).

- KT 013 (inventory write-off).

When objects are disposed of, it is necessary to create a write-off report. Its form is not established by law. Its independent approval is allowed. The procedure for recording related expenses is determined depending on the taxation system adopted by the enterprise.

Classification of household goods by material

Current market trends require not only high strength and reliability of products, but also compliance with environmental requirements. In some categories this area is addressed indirectly. Even if household products are completely safe for humans, their production can release huge amounts of hazardous emissions. Modern technologies allow us to avoid this or minimize damage to the environment. Based on material, household goods are classified into the following groups:

- Wooden. The simplest and most environmentally friendly to manufacture. They can perform a decorative function. When using wooden cutting boards, masher, rolling pins, and choppers, keep in mind that wood absorbs moisture, odors, and pathogenic microorganisms well.

- Steel. For non-food purposes, ferrous metal is actively used, followed by painting. Stainless steel has proven itself well in cooking. It is strong, durable and safe for health. It is used as a coating or base material. Protects other metals from corrosion and the formation of dangerous compounds when interacting with food.

- Enameled. Serve as a continuation of steel products. Enamels are applied mainly to dishes, extending their service life and allowing the use of ferrous metal for food purposes.

- Aluminum. The main advantages are lightness and high thermal conductivity. Thanks to this, the metal is actively used in complex dimensional products. Using it in dishes allows you to speed up the process of heating and cooking.

- Glass. Presented with decorative elements and tableware. The products are very durable, but quite fragile. Modern alloys are characterized by impact resistance, heat resistance and wear resistance. They can be used in ovens, microwaves and dishwashers.

- Plastic. The widest group of household goods. Thanks to the development of production technologies, products made from this material can have a variety of properties: strength, impact resistance, heat resistance, elasticity, etc. This allows plastic to be substituted for products made from other materials. The result is not very environmentally friendly, but the cheapest product to produce.

Note! Not always one type of raw material is used. Most household goods combine different materials to achieve the desired physical and consumer characteristics.

How is tax calculated?

Objects with a service life of more than a year and costing more than 100 thousand rubles must be included in fixed assets.

This is depreciable property, which is stipulated by paragraph 1 of Article 256 of the Tax Code of the Russian Federation. Expenses on accessories that are not included in depreciable items are taken into account as part of material expenses. The write-off procedure is determined by the enterprise itself. For example, this operation can occur at once or in parts. If the enterprise uses the cash method, the tax base is reduced after the facilities are put into operation.

All costs must be justified by the economic policy of the enterprise. For example, the advisability of their acquisition may be stipulated by an internal agreement. The document indicates the need to maintain sanitary and hygienic standards. In connection with this rule, the purchase of toilet accessories is carried out. Other expense items may be justified by other internal documentation.

Example

The company purchased the following toilet accessories:

- Toilet paper for 1180 rubles (VAT will be 180 rubles).

- Towels worth 11,800 rubles (tax is 1,800 rubles).

- Soap for 3,540 rubles (VAT – 540 rubles).

- Air freshener for 2,950 rubles (tax – 450 rubles).

The total cost was 19,470 rubles. VAT – 2,970 rubles). Accessories worth 1,650 rubles were released from the warehouse. The following wiring is required:

- DT 10-9 CT 60 (16,500 rubles).

- DT 19 CT 60 (2,970 rubles).

- DT 68 subaccount “Calculations for VAT” KT 19 (tax deductible in the amount of 2,970 rubles).

- DT 60 CT 51 (19,470 rubles).

- DT 26 CT 10-9 (1,650 rubles).

All expenses must be recorded in accordance with the reporting period and month. Before accounting, all relevant calculations are made. In particular, you need to determine the total costs and subtract VAT from the resulting amount. Then the accounting itself is carried out on the basis of primary documentation.

Algorithm of actions when exchanging or returning goods

According to the current regulations of the Russian Federation, it is possible to exchange or return non-food products. However, the same rules establish a fourteen-day period for carrying out such a procedure.

It is important to know that not every product item can be returned. So, the following items can be returned: shoes, accessories and clothing. The reason for return for the listed product categories may be unsuitable size, or even color. Please note that in order to return your purchase, the item must be in an undamaged packaging box and not show any signs of wear. Having a sales receipt confirming the purchase and sale of the item to be returned will help speed up the process.

In cases where a defect is discovered by the consumer already in the process of using the item, the return of the goods is also provided for by the Russian legislative framework, but for this it is necessary to carry out an examination, which in turn must confirm that the defect was not formed during operation.