Who is eligible for the child tax credit?

By law, if you have children under the age of eighteen, children with disabilities, or children receiving full-time education at any educational institution (under the age of 24), you are entitled to a standard tax deduction. In addition, the monthly tax deduction applies not only to parents, but also to the child’s guardians, trustees, adoptive parents, as well as their spouses who support the children.

Both parents at work and one parent, who in this case can claim a double deduction, can receive a monthly tax deduction. But in order to receive the double standard child tax credit in 2013 at the place of work of one of the parents, the other parent must refuse the deduction by writing a corresponding application.

Standard child tax credit in 2013: how much was it raised to?

In 2012, there was an increase in the child tax deduction and today the amount of the deduction depends on the code and on whether it is the first, second, third or disabled child.

So, for example, the deduction for the first child under code 114 will be 1,400 rubles, for the second – under code 115 – 1,400 rubles, for the third under code 116 – 3,000 rubles, for a disabled child under code 117 – 3,000 rubles.

Currently, the amount within which a child tax deduction is made is 280,000 rubles. This means that the deduction is made until the income of the child’s parent in a particular calendar year reaches this amount.

Amount of deduction for 1 child 2013

Standard deductions for personal income tax in 2013 did not change compared to the size and composition of deductions in force in 2012.

We remind you that since 2012 the standard deduction in the amount of 400 rubles per employee has not been applied.

The changes also affected children's deductions; for example, since 2012, deductions for children have been significantly increased.

Changes in the composition and size of standard deductions for personal income tax occurred in connection with the entry into force of Federal Law No. 330-FZ of November 21, 2011. All changes can be seen in the table; for clarity, the table shows the standard deductions in force in 2011, and the standard deductions in force in 2012 and 2013.

| Deduction | 2011 | 2012 2013 | Limit for deduction | |||

| Per employee | 400 rub. | — | 40,000 rub. | |||

| Per employee for the categories of citizens specified in paragraph 2, paragraph 1 of Art. 218 Tax Code of the Russian Federation | 500 rub. | 500 rub. | No limit | |||

| Per employee for the categories of citizens specified in paragraph 1, paragraph 1 of Art. 218 Tax Code of the Russian Federation | 3000 rub. | 3000 rub. | No limit | |||

| For the first and second child | 1000 rub. | 1400 rub. | 280,000 rub. | |||

| For the third and each subsequent child | 3000 rub. | 3000 rub. | 280,000 rub. | |||

| For each disabled child under 18 years old (disabled student of groups I and II up to 24 years old) | 3000 rub. | 3000 rub. | 280,000 rub. | |||

The standard employee deduction has been cancelled.

Until the end of 2011, the deduction provided for in paragraph 3 of clause 1 of Article 218 of the Tax Code of the Russian Federation was provided to each employee for income up to 40,000 rubles.

Since 2012, the standard deduction per employee for personal income tax in the amount of 400 rubles has been abolished, and in 2013 standard deductions are also not provided to employees.

As for other standard deductions provided for by the Tax Code, certain categories of employees can still count on them in 2012 and 2013.

Thus, a standard deduction in the amount of 3,000 rubles is provided to employees specified in paragraph 1 of paragraph 1 of Article 218 of the Code, these include:

- Persons who have received various types of diseases, disabilities as a result of the disaster at the Chernobyl nuclear power plant;

- Participated in testing nuclear weapons and radioactive substances;

- Disabled people of the Great Patriotic War;

- Military personnel who received disabilities due to wounds and other injuries received while defending the USSR and the Russian Federation.

The second subparagraph of the first paragraph of the same article lists persons who are provided with a monthly standard personal income tax deduction in the amount of 500 rubles, these include:

- Heroes of the Soviet Union, Heroes of the Russian Federation, persons awarded the Order of Glory of three degrees;

- Civilian employees of the SA, Navy of the USSR, Department of Internal Affairs and State Security of the USSR;

- Participants of the Second World War, participants in military operations to defend the USSR;

- Those who were in besieged Leningrad;

- Former prisoners of concentration camps, ghettos and other similar places of forced detention during the Second World War;

- Disabled people of groups I and II, and people with disabilities since childhood;

- Persons who have received various diseases as a result of radiation accidents;

- Persons who donated bone marrow to save people's lives;

- To the parents and spouses of military personnel who died defending the USSR and the Russian Federation;

- Persons who served in Afghanistan, in other countries where military operations took place and who participated in hostilities on the territory of the Russian Federation.

In 2012 and 2013, these categories of employees are provided with deductions in the amount of 3,000 rubles or 500 rubles monthly during the year.

There is no salary limit beyond which deductions are not provided. Employees are not required to submit annual applications for standard deductions; it is enough to receive such an application once.

Children's personal income tax deductions increased

With the entry into force of Law 330-FZ, the amount of children's deductions has increased since 2012. The following categories of employees receive deductions for children:

- Parents, siblings and adoptive parents;

- Spouses of parents, spouses of adoptive parents;

- Adoptive parents, guardians, trustees (spouses of this category are not given a deduction).

In connection with the adopted amendments, which also apply to 2011, the amount of the deduction provided is directly related to the number of children.

Thus, the base for calculating personal income tax is reduced by 1,400 rubles - this is the amount that is deducted for the first and second child. Parents with many children receive a deduction of three thousand rubles for the third and all subsequent children.

How to get the standard child deduction?

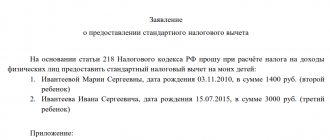

To receive a standard tax deduction for a child in 2013, documents confirming the right to deduction, age and status of the child must be provided to the employer. What documents exactly are we talking about? This:

- application of the established form for the provision of a tax deduction;

- certificate 2-NDFL for the current year;

- a copy of the child's birth certificate;

- a certificate from the child’s place of study (if the children are between 18 and 24 years old and are studying in various educational institutions);

- certificate of disability for disabled children of the first and second groups.

Sometimes there are situations when the employer, for some reason, does not provide tax deductions to employees. In this case, the employee can receive the deduction due to him next year. To do this, he must contact the tax authority with the same documents, and also provide his tax return for the previous year in form 3-NDFL.

How is the deduction distributed between spouses when purchasing a home in common shared ownership?

If, when purchasing a home, the spouses chose the “common shared ownership” form, then the shares are determined in advance and are indicated in the Certificate of Registration of Property Rights.

Therefore, the tax deduction is strictly tied to the established share and cannot be redistributed to the second spouse.

Even if the first spouse has no income or has a small salary, if he has already exercised the right to a property benefit or has decided for some reason not to receive the deduction right now, he cannot transfer his share to his partner.

Reason: Letters of the Federal Tax Service of the Russian Federation dated July 11, 2013 No. ED-4-3/ [email protected] , Ministry of Finance of the Russian Federation dated February 27, 2013 No. 03-04-05/9-148.

For housing purchased before 01/01/2014, there is a rule: the tax deduction is tied to the housing object, and not to the owners, and its maximum total amount is 2 million rubles.

It is this amount that is distributed in shares between the spouses, even if the apartment cost more.

This is stated in the old version of the Tax Code of the Russian Federation (paragraph 25, paragraph 2, paragraph 1, article 220), Letter of the Ministry of Finance of the Russian Federation dated June 21, 2012 N 03-04-05/5-756, June 08, 2012 N 03-04-05/ 9-706, March 15, 2012 N 03-04-05/7-307, Letter of the Federal Tax Service of the Russian Federation dated September 19, 2012 N ED-3-3/ [email protected]

Super deduction: payment for our services only after receiving the deduction!

Order service

Example:

In 2012, a married couple bought a house as common property. When purchasing, the spouses distributed shares in equal parts, that is, 50% to the wife and 50% to the husband.

Despite the fact that the house cost 5 million rubles, the total tax deduction for the owners will be 2 million rubles. As a result, both husband and wife will receive a property deduction of 1 million. Each person will receive 130 thousand rubles of overpaid income tax back into their account.

Example:

In 2011, a married couple bought a room as shared ownership for 1.2 million rubles. When purchasing, the spouses distributed shares in equal parts, that is, 50% to the wife and 50% to the husband.

Since the husband is temporarily unemployed and does not pay income tax, the couple decided to distribute the entire deduction to the wife.

Unfortunately, they were unable to do this, since the property benefit is distributed according to the shares indicated in the Certificate and cannot be transferred to the second spouse. As a result, the wife received a deduction only for her share and returned 78 thousand rubles of overpaid personal income tax (13% x 600 thousand rubles).

Example:

In 2013, a married couple bought an apartment in common shared ownership for 4.5 million rubles. When purchasing, the spouses distributed shares in equal parts, that is, 50% to the wife and 50% to the husband.

Since the wife has already received a property deduction for other housing in the past, only the husband can claim a deduction for this apartment.

Despite the fact that the apartment costs 4.5 million, the husband will receive 50% of the maximum allowable deduction, that is, half of 2 million rubles. As a result, 130 thousand rubles (13% x 1 million) will be credited to his account.

Quick deduction service: personal income tax refund in 7 days, not 4 months!

Order service

Double tax deduction: documents and rules for provision

If one parent refuses a tax deduction in favor of the other parent, then the second has the right to a double tax deduction. The refusal of the deduction is formalized by a corresponding application, which, together with the application for a double tax deduction, the employee who wishes to receive it must submit to his employer.

In addition, you will have to provide the employer providing the tax deduction with a monthly 2-NDFL certificate from the place of work of the parent who refused the deduction (since otherwise it is impossible to determine when the salary of the other parent will reach the limit of 280,000 rubles established for the child tax deduction), and also documents confirming the child’s status - birth certificate, certificate from the place of study, certificate of disability (for disabled children).

Also, the only parent of the child (single mother, widows, widowers, adoptive parents, etc.) has the right to double deduction. But when entering into a remarriage or when a child is adopted by another person, the parent ceases to be considered the only one.

But we should not forget that only those taxpayers who support a child and those who have official income taxed at a rate of 13% (for personal taxes) have the right to a tax deduction.

Therefore, if one of the child’s parents does not work and, accordingly, does not have income that is taxed at a rate of 13%, he cannot legally transfer his right to a tax deduction to a working parent.

When is it more profitable to receive a property deduction when buying an apartment: in 2013 or 2014?

Almost every third and even second person in the country plans to buy an apartment. It's time to think about this seriously. The rules according to which the state provides a property deduction when purchasing an apartment since 2014 may push you to such a decision.

In order, as they say, not to get into trouble with a possible profit, it is necessary, first of all, to do the calculations, and not just give up and choose to buy an apartment in the outgoing 2013 or the coming 2014.

Your decision will affect the amount of money you can get from the tax deduction when buying an apartment.

What changes to the personal income tax deduction are coming?

So, on January 1, 2014, changes to the Tax Code will come into force, or more precisely in Article 220, which will allow you to receive a property deduction several times when buying an apartment, however, it will reduce its size if we consider, for example, mortgage interest.

Somehow it turns out to be unprofitable, given that the vast majority of buyers purchase apartments using a mortgage loan. That’s why you need to decide whether you are buying an apartment now or next year in 2014!

What to consider regarding deadlines

By the way, a small formality that must be taken into account - the right to a property deduction when purchasing an apartment will arise only at the moment when the apartment is registered as ownership.

For example, you entered into a deal in December 2013, but Rosreestr registered the transfer of ownership only in January 2014. In this case, you will receive a tax deduction when purchasing an apartment according to the new rules.

When is it more profitable to buy an apartment, depending on the following situations:

- for the first time you will receive a tax deduction when purchasing an apartment;

- you decide to take out a mortgage;

- you purchase an apartment, registering it in the name of your children;

- you are employed in several organizations.

I suggest looking at them in order :)

You receive a tax deduction for the first time when buying an apartment

What now: You probably already remember that in 2013, the property deduction for personal income tax when buying an apartment can be no more than 260 rubles if the cost of the purchased apartment is 2 million rubles. The formula is simple: (2 million rubles × 13%) = 260 thousand rubles.

If the apartment is cheaper than 2 million rubles, then you will receive less and the rest of the tax deduction will be wasted, which is not very pleasant. For example, the cost of an apartment is 1,700 thousand rubles, then (1.7 million rubles x 13%) = 221 thousand rubles. The shortfall is almost 40 thousand rubles, which would not have been superfluous.

What will happen in 2014: In the coming year, you will be able to get your 40 thousand rubles when buying your next apartment, until the established purchase amount of 2 million rubles is exhausted.

Will it be possible to get the missing property deduction for personal income tax if you bought an apartment in 2013 or earlier?

Answer: No. The rules for obtaining a tax deduction when purchasing an apartment, which will come into force in 2014, apply only to transactions completed in 2014 and beyond. They even issued a separate letter about this dated September 6, 2013 No. 03-04-05/36876, dated September 20, 2013 No. 03-04-05/39121, for those who are interested, read it :) That is. I repeat once again that if you received a property deduction when purchasing an apartment from 2001 to 2013, but not in full, then you will not be able to get it in 2014 when purchasing a new apartment. Therefore, if you have postponed your purchase, hoping to take advantage of the innovations in Art. 220 of the Tax Code, then don’t wait any longer - buy now - in 2013.

Have you decided to take out a mortgage?

It is profitable for you to buy an apartment in 2013!

Yes, right now those whose mortgage is already at the approval stage will be able to hurry up with the transaction. Just keep in mind that this mortgage should, in this case, be issued to you, and not to the children (we’ll look at an example with registration for children below).

What now: In 2013, it is profitable to purchase an expensive apartment with a mortgage. Although, you will have to overpay for it, but along with a tax deduction when buying an apartment from the amount of 2 million rubles, you can also claim a deduction from interest on a mortgage loan (according to subparagraph 2, paragraph 1, article 220 of the Tax Code). At the moment, such property deduction for personal income tax is not limited.

What will happen in 2014: There will be a restriction on tax deductions when purchasing an apartment using a bank loan. The cost limit for an apartment is 3 million rubles. Plus, this deduction can be taken only once and when purchasing only one apartment. Those. either you take an apartment for 3 million rubles or more in order to get the full deduction, or you take it cheaper, but don’t get the whole thing.

How to calculate property deduction for personal income tax when buying an apartment with a mortgage

For example, you took out a loan of 3.5 million rubles for 10 years and received a payment schedule, from which you learned that your final payment is 4.5 million rubles. You found and purchased an apartment in 2013. As a result, you can return, thanks to a tax deduction when purchasing an apartment in 2013: ((2 million rubles + 4.5 million rubles) × 13%) = 845 thousand rubles. And if you buy an apartment in 2014, you will receive: ((2 million rubles + 3 million rubles) × 13%) = 650 thousand rubles. The difference will be 195 thousand rubles! As they say, they don’t lie on the road :)

How the property deduction for personal income tax is paid: Few buyers manage to receive the entire amount of the property deduction when buying an apartment in a year, but maybe, if only deputies :) In this connection, first they receive a property deduction for personal income tax for the general deduction (2 million rubles), if they do not have time in the current year, then the balance is transferred to the next one.

Then a deduction from the mortgage interest is paid. But even with all these transfers, you will not be affected by the innovations of 2014 if you completed the transaction (became the owner) in 2013 (registered the transfer of ownership).

The only exception to the case considered when purchasing an apartment with a mortgage would be a situation where your mortgage loan does not exceed 3 million rubles, then you don’t have to rush into purchasing in 2013.

You purchase an apartment, registering it for your children

Earlier, I already mentioned that the purchase of an apartment, with registration for children and the features of property deduction for personal income tax in this case, we will consider later - this moment has come.

It is more profitable to buy an apartment in 2014!

If you buy an apartment and register it for your children because you already have an apartment or for other reasons, then in 2013 you will not be able to get a tax deduction when buying an apartment, but in 2014 you can!

True, for this you need to provide the following list of documents to the tax service:

- in form 3-NDFL, completed declaration;

- write an application for a personal income tax refund and money transfer, indicating your bank details;

- bring a 2-NDFL certificate for the year for which you want to receive a tax deduction;

- real estate purchase and sale agreement or equity participation agreement;

- Certificate of ownership or deed of transfer of shared construction object;

- fiscal documents (bank statement on the transfer of money from the buyer to the seller, receipt from the seller on receipt of money);

- agreement with the bank on a mortgage loan (if you buy an apartment with a mortgage);

- Birth certificate of children or a child if you are registering for one (for children under 18 years of age).

You are employed in several organizations

It is more profitable to buy an apartment in 2014!

From January 2014, when receiving a tax deduction when purchasing an apartment, you will be able to choose one or more tax agents (employers). In this case, at your choice, one or more of your employers will not withhold personal income tax from you.

This plus also has a minus, which concerns the procedure for obtaining a property deduction for personal income tax from the employer, as opposed to the inspection.

Before the employer begins not to withhold personal income tax from you, your documents will be reviewed by the tax authorities within 3 months. And only after you provide your employer with a notification from the tax office about the deduction provided, will he stop withholding personal income tax from you.

Plus, you will have to return the tax for the period from January to March through the tax office. In other words, it turns out somehow in parts:(

You found out when it is more profitable to get a tax deduction when buying an apartment - now it’s up to you!

Future changes to the child deduction amount

The issue of increasing the tax deduction for children in 2013 is currently being discussed. So in the near future, the amount of deduction for the first child may be 1,400 rubles, for the second – 2,000 rubles, for the third, fourth, and so on – 4,000 rubles. For disabled children under 18 years of age, as well as for full-time students, interns, graduate students, and residents under 24 years of age who are disabled in the first or second group - 12,000 rubles. And the amount within which tax deductions for children are made will be raised from 280,000 to 350,000 rubles

Before you recalculate

Before recalculating personal income tax, the accountant needs to check whether the employee is entitled to a deduction. The fact is that there are certain restrictions for providing a “children’s” deduction.

Child's age

A tax deduction is made for each child under the age of 18, as well as for each full-time student, graduate student, resident, intern, student, cadet under the age of 24.

Parent's income amount

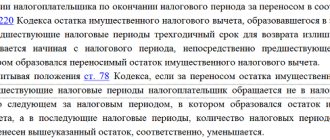

The accountant provides a tax deduction for children up to the month in which the employee’s income, taxed at a rate of 13%, exceeds RUB 280,000. (Subclause 4 of Article 218 of the Tax Code of the Russian Federation). Starting from the month in which the specified income exceeded the limit of 280,000 rubles, the tax deduction is not applied. Income that is exempt from taxation or taxed at other personal income tax rates does not participate in the calculation of the limit (letter of the Federal Tax Service of Russia dated June 5, 2006 No. 04-1-04/300). If an employee has not been working for a company since the beginning of the year, to determine the amount of the limit, the accountant takes into account the amount of income received at the previous place of work. Information about it is contained in the certificate in form 2-NDFL, submitted by the employee when hiring.

The amount of the deduction

The amount of the deduction depends on the age, status and order of birth of the children. The dependence of the size of the deduction on these circumstances is presented in table. 1.

How to calculate the child tax deduction in 2013?

Calculating the child tax deduction is quite simple, since the amount of the deduction depends on the number of children and is fixed. To make a deduction, the deduction rate of a specific employee is taken and subtracted from the amount of accrued wages, and income tax is already taken from the remainder. Thus, the tax base is reduced by the amount of the deduction.

For example, the accrued salary is 30,000 rubles. If the employee has a third child, the deduction is 3,000 rubles. This means that out of 30,000 - 3,000 = 27,000, then we take an income tax of 13% from this amount - 3,510 rubles, and the employee receives 30,000 - 3,510 = 26,490 rubles.

Child tax deduction in 2013: single mothers

Today, single mothers in our country have the right to a double tax deduction for the costs of maintaining each of their children until they reach the age of 18, as well as for children under 24 years of age who are students, cadets, graduate students, and residents.

To receive a double tax deduction, a single mother must provide documents confirming that the child has only one parent. This may be a birth certificate, where only one parent is indicated - the mother, a certificate of form 25 from the registry office, which will confirm that the child’s father is entered on the birth certificate according to the mother’s words (if both parents are recorded on the certificate), a death certificate of the father a child entered on the birth certificate, a court decision declaring the child’s father dead or missing.

Many people are interested in the question: is it possible to receive a double deduction for the child of the mother with whom the child lives if the parents of this child have divorced their marriage or are not married at all? If the father who recognized the child and is now alive is included in the birth certificate, then the mother is not considered a single parent or the only parent of the child. So she can receive a double deduction only if the child’s father refuses the deduction in her favor.

Tax lawyer Alexander Chochiev answers:

No, in this case you do not have the right to take advantage of the deduction for an apartment purchased with a mortgage. The fact is that you have already taken advantage of the tax deduction once in connection with the purchase of housing. And the law directly states that this deduction is not provided again (clause 11, article 220 of the Tax Code of the Russian Federation).

Currently, a deduction claimed for several residential real estate properties is not considered a repeated deduction, provided that the total amount of the deduction does not exceed the maximum amount of 2 million rubles (clause 1, clause 3, article 220 of the Tax Code of the Russian Federation). In other words, it is now possible to receive a property deduction until its maximum amount is fully used, without limiting the number of real estate properties for which such a deduction is claimed. However, it should be borne in mind that this rule applies to relations for providing deductions for objects acquired in ownership only starting from January 1, 2014 (this follows from paragraph 2 of Article 2 of the Federal Law of July 23, 2013 N 212-FZ).

Can I get a tax deduction for two properties?

Can I get a tax deduction again?

In your case, this rule does not apply, since you bought your first apartment before January 1, 2014. Consequently, you have already exercised your right to a deduction, so the tax authority will refuse to provide a deduction in connection with the purchase of a second apartment.

I emphasize that everything said above applies to the deduction in the form of the cost of the apartment itself. Let us recall that a separate tax deduction is provided for interest on a loan received for the purchase of housing (clause 4, clause 1, article 220 of the Tax Code of the Russian Federation). Therefore, if, when purchasing the first apartment, bank interest was not deductible (for example, if this apartment was purchased without borrowing funds), you have the right to receive a tax deduction in the amount of interest that you paid to the bank on a mortgage loan for the purchase of a second apartment . This point of view is confirmed in the letter of the Ministry of Finance of the Russian Federation dated 06/08/2018 No. 03-04-05/39409.