The birth of children is a joyful event for a family, but it affects not only the parents, but also the organization in which the young mother works. By law, a woman has the right to receive maternity benefits, and can also receive payments while on maternity leave after childbirth. Considering the fact that employee income is generally subject to taxation, the question arises whether these payments are included in their number - are benefits up to 1.5 years subject to personal income tax? It is important to know exactly in what form such payments need to be displayed and whether this needs to be done in order to avoid mistakes in preparing the relevant documentation.

Features of taxation

All income is shown in the 2-NDFL certificate. Child care benefits are a kind of exception in this case. They are subject to other rules, which also affect the preparation of reporting documentation.

Thus, sick leave for temporary disability is usually taxed, but this rule does not apply to maternity benefits. This is prescribed by law, so you can be sure that such payments are not required to be indicated in the 2-NDFL certificate.

If a woman is on maternity leave to care for a child who is not yet 1.5 years old, she also receives a corresponding benefit, which is not taxed and is not reflected in 2-NDFL.

If an employee simultaneously works part-time, she will receive a salary, which, in turn, is already subject to taxation.

Also see “Benefits from May 1, 2021 after increasing the minimum wage: new sizes.”

It is worth noting that parental leave is not reflected in 2-NDFL. But if this is sick leave, then the same rules apply to it as sick leave for temporary disability. Therefore, if the child gets sick and the mother receives sick leave due to this, then tax payments must be deducted.

In some cases, maternity leave may be less than average earnings. Then the employer can pay some additional amount, giving out even more than is required for established benefits. Since this money will no longer be considered part of the benefit, it is taxable and classified as “other income.”

Also see “What are the minimum maternity payments in 2021.”

Income tax on maternity payments.

In addition to payments for sick leave, pregnant women have the right to the following financial assistance:

- allowance for early registration;

- a lump sum payment upon the birth of a minor.

In the first case, financial assistance is 300 rubles, but is subject to annual indexation. In 2021, women will be able to receive 675.15 rubles.

The one-time payment was initially set at 8,000 rubles.

Since February 2021, it has been just over 18,000 rubles. No personal income tax is taken from these amounts. Therefore, and after taxes

Despite the fact that the payments are made by the Social Insurance Fund, they are calculated by the employer. If a woman is an individual entrepreneur, then she is entitled to benefits only if she has a voluntary insurance agreement with the Social Insurance Fund.

It concludes independently. A woman will need to pay 2.9% of her income monthly to the government. Payment under the BiR will be assigned if the duration of the voluntary insurance contract is more than 1 year.

The law establishes minimum and maximum amounts of maternity payments. They depend on the minimum wage, which is 12,130 rubles.

During the normal course of pregnancy, a woman should not receive a payment of less than 55,830.60 rubles. The maximum benefit amount will be 322,191.80 rubles.

Tax amount.

If a woman has taken maternity leave, income tax is not charged on all payments. The legislation defines that this is the time when a pregnant woman is on sick leave according to the BiR.

After its completion, the employee can take parental leave for up to 1.5 or 3 years. In the first case, a woman is entitled to a monthly payment of 40% of average earnings. Personal income tax is not calculated from it.

Thus, information about the benefit for a pregnant woman is not included in the 2-NDFL certificate. It is believed that during this period the woman did not receive any income.

The exception is when the employee continues to work. She cannot receive both wages and B&R benefits.

A 2-NDFL certificate for an employee who is on maternity leave or maternity leave is not issued, since it will be blank, and the accounting department does not issue such forms.

If a woman continues to do her work and receives remuneration for it, then she can receive a certificate of income.

The legislation provides for the possibility of a woman to perform her labor functions while on maternity leave. However, she must work part-time. Otherwise, the payment for caring for a minor is terminated.

Tax deduction for children in 2020-2021.

Tax deduction for children.

Tax on premiums.

Employers often congratulate an employee on the birth of a child and want to reward her with a bonus. Amount up to 4000 rub. not subject to personal income tax.

If a higher payment is assigned, then you will need to calculate the tax only on the part that is above 4,000 rubles.

If a pregnant woman is employed in several jobs, she can receive B&R benefits from all employers. In this case, you will need to take several certificates of incapacity for work with the name of the enterprise.

The employer where the woman works part-time pays payments in the same manner as at her main place of work.

Eligibility for benefits

The legislation specifies the circle of those who can receive maternity benefits:

- Women who work officially and under an employment contract, as well as those who work as civilian personnel in military formations in other countries, can count on it;

- if a woman does not work, but was fired due to the liquidation of the enterprise, then she can also apply for benefits; the same applies to women who have ceased activities as individual entrepreneurs;

- full-time students in any educational institution.

It is important that only the woman herself is entitled to maternity benefits. It cannot be issued by other relatives, as is possible in the situation with some other child benefits.

A woman can also receive benefits when adopting a child under 3 months old, which will be accrued only to the mother. If in the family that adopted the baby, the father works and the mother does not, then the benefit will not be transferred.

If a woman officially works in two places at once and has worked in these organizations for the last 2 years, then she can count on accruing two benefits at once - from each employer.

Everything you need to know about applying for child care benefits for children up to 1.5 years old

I often see questions from young mothers (and dads too) about how to usually apply for benefits due to being on maternity leave for a child up to 1.5 years old, because according to the current legislation of the Russian Federation, only until the child reaches the age of 1.5 years, the employer is responsible for the corresponding payments.

Who is eligible to receive benefits?

In accordance with Federal Law No. 81-FZ of May 19, 1995 “On state benefits for citizens with children,” child care benefits for children under 1.5 years of age are paid to persons who care for a child during the leave of the same name, namely:

- mothers or fathers, other relatives, guardians actually caring for the child, subject to compulsory social insurance in case of temporary disability and in connection with maternity, including mothers or fathers, other relatives, guardians actually caring for the child, from among civilian personnel of military formations of the Russian Federation located on the territories of foreign states in cases provided for by international treaties of the Russian Federation and on parental leave;

-mothers undergoing military service under contract, mothers or fathers serving as privates and commanding officers of internal affairs bodies, national guard troops, the State Fire Service, employees of institutions and bodies of the penal system, compulsory enforcement bodies of the Russian Federation, customs authorities and those on parental leave;

-mothers or fathers, other relatives, guardians actually caring for the child, dismissed during the period of maternity leave, mothers dismissed during maternity leave due to the liquidation of organizations, termination of activities by individuals as individual entrepreneurs, termination of powers by notaries engaged in private practice and termination of the status of a lawyer, as well as in connection with the termination of activities by other individuals whose professional activities in accordance with federal laws are subject to state registration and (or) licensing, including those dismissed from organizations or military units located outside the Russian Federation, dismissed due to the expiration of their employment contract in military units located outside the Russian Federation, as well as mothers dismissed during parental leave, maternity leave in connection with the transfer of their husband from such units to the Russian Federation;

-mothers dismissed during pregnancy due to the liquidation of organizations, termination of activities by individuals as individual entrepreneurs, termination of powers by notaries engaged in private practice, and termination of the status of a lawyer, as well as in connection with the termination of activities by other individuals whose professional activities are in accordance with federal laws, is subject to state registration and (or) licensing, including those dismissed from organizations or military units located outside the Russian Federation, dismissed due to the expiration of their employment contract in military units located outside the Russian Federation, or in connection with the transfer of the husband from such units to the Russian Federation;

-mothers or fathers, guardians who actually care for the child and are not subject to compulsory social insurance in case of temporary disability and in connection with maternity (including full-time students in professional educational organizations, educational organizations of higher education, educational organizations of additional professional education and scientific organizations);

- other relatives who actually care for the child and are not subject to compulsory social insurance in case of temporary disability and in connection with maternity, if the mother and (or) father died, were declared dead, were deprived of parental rights, had limited parental rights, were recognized missing, incompetent (partially incompetent), for health reasons cannot personally raise and support a child, are serving a sentence in institutions executing a prison sentence, are in places of detention of suspects and accused of committing crimes, are evading raising children or from protecting their rights and interests or refused to take their child from educational organizations, medical organizations, social service organizations and other similar organizations.

It should be noted that the right to a monthly child care allowance is retained if the person on parental leave works part-time or at home, as well as in the case of continuing education.

Persons entitled to both monthly child care benefits and unemployment benefits are given the right to choose to receive benefits on one of the grounds.

If maternity leave occurs while the mother is on maternity leave, she is given the right to choose one of two types of benefits paid during the periods of the corresponding leave.

Mothers entitled to maternity benefits, during the period after childbirth, have the right, from the day of birth of the child, to receive either a maternity benefit or a monthly child care benefit with credit for the previously paid maternity benefit if the amount of the benefit is for child care is higher than the amount of maternity benefits.

Persons entitled to receive a monthly child care benefit on several grounds are given the right to choose to receive benefits on one of the grounds.

If a child is cared for by several persons at the same time, the right to receive a monthly child care benefit is granted to one of these persons.

To terminate the payment of the monthly child care allowance for the period when the mother of the child does not actually care for the child due to her illness, the mother’s application for termination of the payment of the allowance must be submitted to the place where the monthly child care allowance is assigned to her, and in the event , if the woman is on maternity leave, also a statement that she is interrupting her maternity leave.

If, for health reasons or for other reasons, the child’s mother cannot submit this application in person, it can be accepted from another family member upon presentation of a document proving his identity and relationship.

To assign and pay a monthly child care allowance, the specified persons shall submit the documents provided for in paragraph 56 of this Procedure, as well as a certificate from the place of work (study, service) of the child’s mother stating that she does not use the specified leave and does not receive child care benefits a child, and if the child’s mother belongs to the category of persons not subject to compulsory social insurance in case of temporary disability and in connection with maternity, including full-time students in educational organizations - a certificate from the social protection authorities at the place residence of the mother about non-receipt of monthly child care benefits. If at the time of applying for the appointment and payment of a monthly child care allowance, the specified certificate is not available, before its submission it can be replaced with a copy of the mother’s application specified in paragraph four of this paragraph, certified at the place of its submission (at the place of work, study, mother's service or the social protection authority).

Unmarried minor parents, in the event of the birth of a child and when their maternity and (or) paternity are established, have the right to independently exercise parental rights upon reaching the age of sixteen.

The assignment and payment of a monthly child care allowance to a minor unmarried parent of a child who has reached the age of sixteen and is actually caring for the child is carried out according to the rules established by this Procedure.

Until the child's unmarried minor parent reaches the age of sixteen, the child may be appointed a guardian who will raise him or her together with the child's minor parents.

In the event that the care of a child for whom a guardian has been appointed is carried out by a guardian, a monthly child care allowance is assigned to the guardian according to the rules established by this Procedure.

In the event that the care of a child for whom a guardian has been appointed is carried out by the child’s minor parent, who is unmarried and under the age of sixteen, the child care allowance is assigned to the guardian who is raising him or her together with the child’s minor parent, regardless of the fact that This guardian is on parental leave.

If it is not possible to appoint a guardian for the child, a monthly child care allowance is assigned to one of the capable relatives of the child’s minor parent, who has not reached the age of sixteen and is not married, living together with the child and his minor parent.

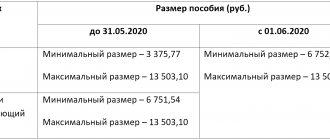

What is the amount of the benefit in cash equivalent?

- 6,752 rubles - to persons whose circle is defined by law,

-40 percent of average earnings on which insurance contributions for compulsory social insurance in case of temporary disability and in connection with maternity are calculated: mothers or fathers, other relatives, guardians who actually care for the child, subject to compulsory social insurance in case of temporary disability and in connections with motherhood, including mothers or fathers, other relatives, guardians actually caring for the child, from among the civilian personnel of military formations of the Russian Federation located on the territories of foreign states in cases provided for by international treaties of the Russian Federation, and who are on leave for child care, while the minimum monthly child care benefit cannot be less than 6,752 rubles.

-40 percent of the average earnings (income, salary) at the place of work (service) for the last 12 calendar months preceding the month of parental leave (month of dismissal during maternity leave) - to persons specified in the Law, the minimum benefit amount is 6,752 rubles. The maximum amount of child care benefits cannot exceed 13,504 rubles for a full calendar month.

In districts and localities in which regional coefficients are applied to wages in accordance with the established procedure, the minimum and maximum amounts of the specified benefit are determined taking into account these coefficients.

In the case of caring for two or more children before they reach the age of one and a half years, the amount of the benefit calculated in accordance with parts one and two of this article is summed up. In this case, the summed amount of the benefit, calculated on the basis of average earnings (income, cash allowance), cannot exceed 100 percent of the amount of the specified earnings (income, cash allowance), but cannot be less than the summed minimum amount of the benefit (Art. 11.2 of the Federal Law of 29.12 .2006 N 255-FZ “On compulsory social insurance in case of temporary disability and in connection with maternity”).

From January 1, 2021, the maximum amount of care allowance is 29,600 rubles 48 kopecks. The following are entitled to benefits in the specified amount:

mothers dismissed during pregnancy due to the liquidation of the organization

mothers, fathers, guardians, full-time students

relatives caring for a child in the event of deprivation of parental rights to the mother and (or) father

Benefit calculator:

average earnings for the two previous calendar years / per number of calendar days in the same period (excluding periods of temporary disability, maternity and child care leave, period of release from work with retention of salary) = average daily earnings * 30.4 * by 40%.

You must apply for child care benefits no later than six months from the date the child reaches 1.5 years of age.

The benefit is assigned within ten calendar days from the date of provision of the necessary documents.

Let's look at the step-by-step algorithm for processing this payment:

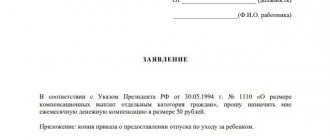

1. Application from a person entitled to receive benefits.

2. Child’s birth certificate with a copy.

3. Certificate from the second parent’s place of work confirming that the specified benefit has not been accrued.

4. Certificate 2 of personal income tax for the two previous years prior to the date of filing the application for benefits.

5. If the employee works part-time, then it is necessary to provide a certificate

Direct payments

In some regions, the Social Insurance Fund project “Direct Payments” operates. It provides that the woman will receive benefits directly through the Social Insurance Fund. In this case, the documents are submitted to the appropriate department by the employer himself, or in some situations the woman can do this herself.

The presence of such a project makes life easier for accountants of organizations and the employees of the Social Insurance Fund themselves, and a woman receives a guaranteed opportunity to receive payments in the required quantity and on time - regardless of how the financial affairs are in the organization where she works. This procedure protects against unscrupulous employers who use crisis conditions as an excuse not to pay employees or delay due payments.

Also see “FSS Pilot Project in 2021.”

Certificate of incapacity for work when caring for a patient

The amount of the benefit depends on the insurance period of the person receiving sick leave and his average earnings . Only persons who have had insurance coverage for more than 8 years can apply for full compensation of average earnings. With an insurance period of 5 to 8 years, the benefit is calculated based on 80% of average earnings, less than 5 - 60%.

However, some employers provide the possibility of paying additional benefits from their own funds.

Are taxes withheld?

In accordance with the Tax Code of the Russian Federation, the income of an individual is subject to taxation, unless otherwise provided by law. Payments of sick leave benefits are not exempt from personal income tax .

The tax is levied at a rate of 13%. Individuals who are not tax residents in Russia pay a tax of 30%.

Are there any insurance premiums?

The Tax Code of the Russian Federation provides that state benefits are not subject to insurance contributions . Since, as a general rule, incapacity for work to care for a sick child is compensated from the Social Insurance Fund from the first day of his illness, the benefit received by the employee may not be subject to insurance contributions (you can find out who pays for sick leave for child care - the Social Insurance Fund or the employer here ).

In this case, additional payments, the amount of which is established by the employer, are subject to insurance contributions in full.

Other deductions

When calculating personal income tax for child care disability benefits, the same standard tax deductions apply as when calculating income tax.

Standard “child” tax deductions apply for children under 18 years of age, as well as for each full-time student under the age of 24 years. The amount of tax deductions is :

- 1,400 rubles each for the first and second child;

- 3,000 rubles for the third and each subsequent child.

For disabled children under the age of 18, as well as disabled people of group I or II under the age of 24, studying full-time, the tax deduction is:

- 12,000 rubles - for parents and adoptive parents;

- 6,000 rubles - for guardians, trustees or adoptive parents.

Receiving benefits

Payments are made for the time that the woman remains on maternity leave. You can go into it at the 30th week of pregnancy - 7 months after its onset. If a mother is expecting not one baby, but several, then she can go on vacation earlier.

To receive payments, you need an appropriate basis, which will be attached to the documentation. This may be a certificate from the antenatal clinic, as well as a birth certificate when the child is born. These documents are attached to the application, and are also included in the order for the calculation of benefits, which the employer draws up after receiving the application.

Also see “Order for payment of benefits for registration in the early stages of pregnancy.”

Read also

19.05.2018

What is maternity leave

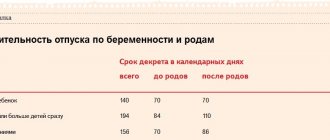

According to labor law, a pregnant employee has the right not to go to work seventy days before giving birth and another seventy days after it.

During her stay at home, she will receive an allowance, and this period of time is called maternity leave or maternity leave, in official terms. It goes without saying that when making calculations, enterprise managers are interested in whether personal income tax is withheld from maternity leave, as well as other taxes and contributions. The same question, of course, worries employees who are going on vacation - after all, it is much more pleasant to receive the entire accrued amount in your hands in full, without any deductions.

Pilot project for direct payments from the Social Insurance Fund

Since 2012, a pilot project for direct payments from the Social Insurance Fund has been launched in two constituent entities of the Russian Federation. Since 2021, the number of participants has increased to 50. By July 2021, it is planned to transfer all regions of the Russian Federation to the new system.

The essence of the project is that the employer acts as an intermediary between the employee applying for maternity leave and the fund. The project helps a woman draw up an application for benefits using a special form and creates a package of documentation.

Then the employer contacts the Social Insurance Fund on behalf of the employee. The fund assigns benefits and independently transfers funds to the woman’s bank account. At the same time, the transactions are not reflected in the employer’s records, and the question of withholding personal income tax and insurance contributions does not arise.