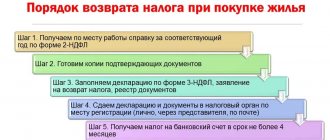

When is it necessary to apply for a refund of overpaid tax?

There are different situations where tax overpayment occurs.

For example, a taxpayer mistakenly transferred a tax amount greater than what he showed in the declaration. Or he filed an updated declaration with a lower tax charge than was initially shown and, accordingly, has already been transferred. In addition, it is possible that more advance payments were transferred at the end of the reporting periods than the amount of tax accrued for the tax period.

In such cases, the taxpayer should contact the tax office at the place of registration with an application for a refund of the amount of overpaid tax. The tax can be refunded within 3 years from the date of overpayment (Clause 7, Article 78 of the Tax Code of the Russian Federation).

Learn more about tax refunds in this article.

Do not forget that the tax office is obliged to independently calculate and pay interest for late repayment of the overpayment. You do not need to submit an application for this. You can learn about how interest should be calculated and what to do if the tax authorities refuse a refund from the Ready-made solution from ConsultantPlus. Trial access to K+ can be obtained for free online.

Procedure and deadlines for filing an application for a refund of personal income tax.

A taxpayer who has overpaid tax within three years has the right to submit a corresponding application. The fact of overpayment is determined by the Federal Tax Service as part of a desk audit submitted by the taxpayer in the form of 3-NDFL. In accordance with Article 88 of the Tax Code of the Russian Federation, the period for its implementation is three months from the date of filing the tax return.

Based on the results of the audit, the tax authority sends a message to the taxpayer about the decision made, confirming his right or denying it (Clause 9 of Article 78 of the Tax Code of the Russian Federation)

Thus, the return of the overpayment is a declarative procedure, due to which the funds must be returned within one month from the moment the taxpayer submits the corresponding application (clauses 6 and 7 of Article 78 of the Tax Code of the Russian Federation).

An application for a personal income tax refund can be submitted by a taxpayer either together with a declaration or based on the results of a desk audit. In any case, the amount of the overpayment must be transferred to the taxpayer within a month from the moment the tax authorities receive the relevant application, and if it is submitted simultaneously with the declaration, then the money is returned no earlier than the expiration of the deadline established by the Tax Code for conducting a desk audit, and no earlier than the tax authority makes a decision on the refund tax (clauses 6, 8, 8.1 of Article 78 of the Tax Code of the Russian Federation; Letter of the Federal Tax Service of Russia dated October 26, 2012 N ED-4-3/ [email protected] ; clause 11 of the information letter of the Presidium of the Supreme Arbitration Court of the Russian Federation dated December 22. 2005 N 98)

In general, it is enough to submit one application for all tax deductions (property, social, standard). The total amount to be refunded on the tax return is indicated in one application.

Multiple applications are required if:

- an error was made and there was a need to submit an updated application;

— it is necessary to return the overpayment for several years (an application is submitted for each year);

— various taxes are subject to refund (personal income tax, personal property tax, transport tax, etc.);

— income is received from several sources with different OKTMO, i.e. if during the tax period (year) income is received from sources located in different municipalities (they have different OKTMO), accordingly, the tax refund is carried out from the budget of each of these municipalities, i.e. from where the tax was previously paid. Hence the need to write several different statements, one for each OKTMO, in accordance with sections 1 of the 3-NDFL declaration, in which several sections will be filled out, one for each OKTMO.

Tax Refund Application Form 2020-2021

The application form for a refund of overpaid tax was approved by Federal Tax Service order dated 02/14/2017 No. ММВ-7-8/ [email protected] From 01/09/2019 it is used as amended by the Federal Tax Service order dated 11/30/2018 No. ММВ-7-8/ [email protected]

In the application form for a refund of overpaid tax, you must indicate:

- TIN, KPP (if any) of the person submitting the application (this information is indicated on all pages);

- application number, code of the tax authority to which it is submitted;

- name of the taxpayer (if it is an organization) or full name (if it is an individual entrepreneur or individual);

- payer status (from 01/09/2019);

- article of the Tax Code on the basis of which the refund is made;

- taxable period;

- OKTMO and KBK codes;

- who confirms the accuracy of the information specified in the application, telephone number.

Also on the first sheet is the signature of the applicant and the date of signing. The second page contains information about the bank account details (from 01/09/2019, the type of account is indicated as a code, and there is no field for specifying a correspondent account), the name of the recipient and information about the identity document. The third page is filled out by individuals who are not individual entrepreneurs. It also provides information about the identity document. From January 9, 2019, the individual’s place of residence is not indicated in the application. Please note that this page may not be filled out if a TIN is provided.

The application must be dated and signed by the applicant. If the application is submitted electronically, it is certified by an enhanced qualified electronic signature.

To find out whether a stamp is needed on the application, read the article “The Tax Office will accept documents without a stamp .

We draw up and submit to the Federal Tax Service an application for a refund of the overpayment

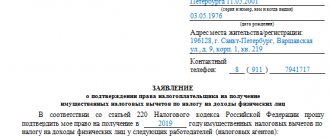

First, fill out the title page of the form.

The top 2 lines of the form indicate the TIN, KPP and page number (001). In the example given, the application is drawn up from an organization, which means we enter 10 digits in the TIN field, and 9 digits in the KPP field: respectively, the data of Vympel LLC.

Then in the line “Application number” we put its number (if it is the first, then it is “1”) for this year. Next to it we write the code of the tax authority to which we are addressing it.

Next are lines to indicate the full name of the organization (full name of the individual), in our example this is the limited liability company “Vympel”.

In the “Taxpayer Status” line, select the appropriate unambiguous code from those proposed in the form. All empty cells in the form fields must be filled in with dashes.

In the line “Based on the article” you should indicate the number of the article in the Tax Code of the Russian Federation, which serves as the basis for the upcoming return of the overpaid payment. When returning overpaid tax or contribution, this is Art. 78 of the Tax Code of the Russian Federation, when returning state duty - Art. 333.40 of the Tax Code of the Russian Federation, the tax office erroneously collected it - Art. 79 of the Tax Code of the Russian Federation, you reimburse VAT - Art. 176 of the Tax Code of the Russian Federation, etc.

In our example, this is Art. 78 of the Tax Code, since a refund of overpaid income tax is required.

Below, in two cells located one below the other, we indicate information about what kind of overpayment and for what type of payment, and select the appropriate unambiguous codes for these fields from those proposed in the form. For example, “1” is overpaid, and “1” is tax.

In the “in amount” line, we write down in numbers the amount of the requested tax overpayment, for example, 5,350 rubles. The line “Tax (settlement) period” is filled in with the following codes for the first two cells:

“MS” - if the payment is monthly;

“KV” - if quarterly;

“PL” - if overpayment for half a year;

"GD" - if annual.

After the point, the selected and specified reporting period is specified, i.e. the serial number of the month, quarter or half-year is entered, and for the annual payment we put “00” here.

The year in which the overpayment occurred is indicated after the next dot in four empty cells.

In our example: “GD.00.2018”.

Next to it you should indicate the OKTMO code, which can be clarified on the official website of the Federal Tax Service.

To fill out an application for a refund of overpaid tax, organizations can take the region code (OKTMO) from the submitted tax return (in the example, this is a profit declaration), and an individual can indicate the region where this tax was paid: if we are talking about property tax, OKTMO is taken according to the location of this property, transport tax - at the place where the owner of the car is registered, personal income tax - from a certificate of income from work.

In the line below - “Budget classification code” - fill in the 20-digit BCC of the overpaid payment. In our example, this is the KBK of income tax to the federal budget.

Next, we write down the number of pages and attachments in the submitted application. Remember that we cross out all empty cells in the fields of the form.

At the bottom left of the title page of the form, a part of the page is provided to reflect information about the applicant (payer/his representative): full name, phone number, signature and date. If the application is submitted by a representative, you must indicate the details of the document confirming his authority and attach a copy of it to the application.

Find out if you are subject to mandatory audit

according to your situation and get advice from an auditor.

Request a call

Request a call

Results

The resulting tax overpayment can be returned from the budget. To do this, you must submit an application in the prescribed form to the Federal Tax Service Inspectorate, indicating in this document the necessary codes, taxpayer data, the period of the overpayment, its amount and details by which the overpayment will be returned.

Sources:

- Tax Code of the Russian Federation

- Order of the Federal Tax Service of Russia dated February 14, 2017 N ММВ-7-8/ [email protected]

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Return procedure

- Before you run to the tax office with an application for a refund, you need to ensure that you have documents confirming the overpayment.

- Once the evidence is in hand, the taxpayer writes a corresponding statement, which he submits to the tax office.

For example, if there was an oversight on the part of the company’s accountant, which was subsequently discovered, an updated declaration must be prepared and submitted to the tax authorities. Or you can simply draw up a reconciliation report with the tax office - if it reveals an overpayment, then you will no longer need to submit a “clarification”.

Sometimes the fact of tax overpayment is revealed as a result of on-site tax audits - in this case, the tax office sends a written notification to the organization.

Sometimes, in search of the truth, taxpayers are forced to go to court, but as a rule, this is a last resort. However, if in court , this will also serve as the basis for a refund.

Tax officials are required to consider the application within 10 days of receipt.

List of documents

To assign a benefit, in addition to the application, other documentation is required, based on the type of compensation.

The general list includes:

- passport (copy);

- declaration (not required when issued through an employer);

- information about income.

The list of additional documentation includes:

- confirmation of family ties - when indemnifying children, brothers, sisters, and so on;

- an agreement with a medical institution, a copy of a license, a payment slip, a prescription in a special form (107/u) with a note for the Federal Tax Service - if deducted for treatment;

- education contract, institution license, confirmation of payment - in case of reimbursement for training;

- property papers, receipts, payment receipts, loan agreement, certificate from the bank on payment of interest - in case of property benefits.

Each taxpayer, under certain conditions, has the right to benefit from compensation for his own expenses in the form of a refund of part of his personal income tax. However, to assign a benefit, you need to go through a registration procedure, which takes about 4 months.

One of the stages is filling out an application form for a personal income tax refund and sending it to the Federal Tax Service. At the same time, it is important to take into account innovations in legislation and the procedure for preparing documentation.

Officially employed citizens pay personal income tax - personal income tax - from their wages at a rate of 13%. Some of them, by law, have the right to return part of the amount paid as tax. To do this, you must apply for a tax deduction through the employer or the Tax Office.

- How to pickle watermelons in jars for the winter

- From August, Russian drivers will begin to use new license plates

- 5 foods you shouldn't eat if you have a cold

Title page

On the title page of the application, the taxpayer fills in all the necessary details, except for the section “To be completed by a tax authority employee”

.

In the "Application number"

The serial number of the application from the applicant for the current year is indicated.

In the field “Submitted to the tax authority (code)”

The code of the tax authority to which the application is submitted is reflected. This code is indicated in the documents on registration with the tax authority (certificate of registration with the tax authority, notice of registration with the tax authority of a legal entity as the largest taxpayer). By default, the field is automatically filled with the code that was specified when the client registered in the system.

In the field “Full name of the organization (responsible participant of the consolidated group of taxpayers) / last name, first name, patronymic of an individual”

the name of the organization is reflected, corresponding to that indicated in the constituent documents or the full name of the individual in accordance with the identity document.

In the “Based on article”

the number of the article of the Tax Code of the Russian Federation is selected, in accordance with which the refund is made.

Next, select the code for the amount that the applicant requests to return:

- “1” – overpaid;

- “2” - overcharged;

- “3” – subject to compensation.

Then select the appropriate payment code: “1” - tax, “2” - fee, etc. and the amount of overpayment that the applicant requests to be returned from the budget is indicated.

In the field “Tax (calculation) period (code)”

The code of the tax (settlement) period is indicated in accordance with the established requirements:

- to fill in the first 2 digits of this indicator, select the appropriate code: “MS” - monthly, “QV” - quarterly, “PL” - semi-annual, “GD” - annual, “Date” - the specific date of tax payment;

- in the 4th and 5th digits of the indicator the following is indicated: month number (from 01 to 12) – for “MS”, quarter number (from 01 to 04) – for “KV”, half-year number (from 01 to 02) – for “PL”, for “GD” - “00”;

- The year is indicated in 7-10 digits.

In the “OKTMO code”

a code is selected for the place where the tax or fee is paid. You can find out your OKTMO code using the electronic services of the Federal Tax Service of Russia “Find out OK” (https://nalog.ru, section “All services”).

In the “Budget classification code”

The KBK of the tax or fee for which the overpayment is recorded is selected.

Attention! Each tax corresponds to one or more budget classification codes (BCC), depending on the payment attribute. So, for example, when selecting the payment code “01”, the BCC of the tax is selected from the corresponding directory, the overpayment for which the applicant requests to be returned from the budget. If in relation to this tax it is necessary to return excessively collected penalties, then when the payment code is changed from “01” to “04”, the BCC automatically changes, in particular, the value of 14-17 digits. The structure of the KBK is a 20-digit code, in which digits 1 to 20 mean the following:

- categories 1-3 – code of the department that controls the payment of the tax or fee (for example, “182” - Federal Tax Service);

- category 4 – income group code (for example, “1” - tax and non-tax income, “2” - gratuitous receipts);

- digits 5-6 – income subgroup code (for example, “01” - income tax, “02” - insurance premiums, etc.);

- categories 7-11 – code of article and sub-item of income;

- digits 12-13 – code of the income element (for example, “01” - federal budget, “06” - Pension Fund budget, etc.);

- digits 14-17 – code of the budget income subtype group (for example, “0000” is the general group of the income tax income subtype, “1000” is the income tax income group, “2100” is the income group for income tax penalties, “3000” - income group for income tax fines, etc.);

- categories 18-20 – code of the analytical group of the subtype of budget revenue (for example, “110” - tax revenue, “120” - property income, etc.).

In the field “The application is drawn up on ____ pages”

The number of pages on which the application is drawn up is automatically indicated.

In the section of the title page “I confirm the accuracy and completeness of the information:”

indicated:

- 1 - if the application is submitted by the taxpayer,

- 2 - if the application is submitted by a representative of the taxpayer.

In this case, the full name of the head of the organization or representative is indicated, as well as the name and details of the document confirming his authority.

In the "Phone"

The telephone number of the taxpayer or his representative is reflected.

The date is also automatically indicated on the title page.

Social

Based on Art. 219 of the Tax Code of the Russian Federation, any citizen of the Russian Federation has the right to receive social benefits when spending on charity, paying for education or treatment, buying medicine, making contributions to the Pension Fund. To receive a refund, the taxpayer applies either directly to the Federal Tax Service or to the employer. Please note: the sample application for a tax deduction in connection with payment for medical services refers to the notification issued by the Federal Tax Service confirming the right to social benefits.

Application form for personal income tax refund through the Federal Tax Service

Filling out the document is allowed both on a computer, typewritten, and manually.

ATTENTION! There is no strictly mandatory form for the application, that is, if desired, a citizen has the right to draw up a paper at will, entering the information required by the tax authority. The Federal Tax Service cannot refuse to accept such a document.

Example of a free-form application

However, the recommended type of document is indicated by the Federal Tax Service: the form consists of 3 pages containing personal information, bank details, information about the amount to be returned, and so on.

To receive the benefit, you must fill out all the data correctly, taking into account the recommendations of the tax service located at the end of the third sheet of the form. It is important to make sure that your bank details are correct, since the funds due for refund will be transferred to the specified account.

Application methods

To assign benefits, they operate in 2 ways: directly through the inspectorate or the employer. In the second case, as described above, 2 applications are required: first to the Federal Tax Service to receive confirmation of the benefit, then to the accounting department in person together with a positive verdict from the inspection.

When contacting the Federal Tax Service Inspectorate directly in person, the application is filled out once; over the Internet, first, a declaration and an application confirming the right to a benefit are filled out, and after a positive response from the tax office, an application to receive a deduction through a bank or employer. Sending documentation directly to the tax authority (to receive a lump sum payment or confirmation for the employer) is possible through mail, the Internet or a personal visit.

Table 2. Options for filing an application with the tax authority

| Way | Description |

| Through the Internet | The action is performed through the taxpayer’s personal account or the State Services service. It is necessary to have an electronic signature to certify documentation |

| By mail | Papers are sent by registered mail with an inventory |

| Personal visit | It is recommended to fill out the declaration (if executed directly through the Federal Tax Service Inspectorate) in advance, before visiting the Federal Tax Service Inspectorate, since the procedure takes a significant amount of time. The application can be completed on the spot with the help of an inspector. |

After checking the documents and a positive decision on granting the benefit, the refund amount will be credited to the account specified by the recipient in the application. Usually the registration procedure takes 3-4 months.