Income tax

Taking into account the provisions of sub. 12 clause 1 art. 264 of the Tax Code of the Russian Federation, travel expenses are classified as other expenses. And the list of other expenses is not clearly defined (subclause 49, clause 1, article 264 of the Tax Code of the Russian Federation). other economically justified expenses can be added to it

Tax legislation does not regulate the acceptance of taxi expenses on a business trip.

The employer independently determines the procedure and amount of reimbursement for travel allowances in accordance with Art. 168 Labor Code of the Russian Federation. According to the position of the Ministry of Finance, set out in letter No. 03-03-07/23568 dated March 25, 2020, expenses for taxi travel on a business trip can be taken into account when calculating income tax if you have correctly executed supporting documents.

An employer may prescribe in its local regulations the procedure for accepting taxi expenses. For example, in case of departure or return from a business trip, when public transport is no longer available. Or when the airport is in a remote area. In addition, the company may decide that an employee who goes on a business trip to the airport or train station during working hours takes a taxi to save time.

Taxi expenses for business purposes at the location

The next set of situations when an organization faces the question of accounting for taxi costs is the use of this type of transport for employees’ business trips. Here the explanations of the Ministry of Finance of Russia, given in letter dated October 20, 2017 No. 03-03-06/1/68839, will come to the rescue. It states that organizations can use taxis as official transport. In this case, the costs associated with transporting employees for corporate purposes by taxi services can be taken into account on the basis of subparagraph 11 of paragraph 1 of Article 264 of the Tax Code of the Russian Federation as the cost of maintaining official transport (of course, subject to the requirements of Article 252 of the Tax Code of the Russian Federation).

Single tax payers under the simplified tax system can also write off the costs of transporting employees by taxi, since the costs of maintaining official vehicles are included in the list provided for in paragraph 1 of Article 346.16 of the Tax Code of the Russian Federation. These costs will “pass” on the basis of subclause 12 of clause 1 of Article 346.16 of the Tax Code of the Russian Federation.

Regardless of what tax regime the organization applies, we recommend documenting the fact that a taxi is used as official transport. This can be done by the relevant administrative document of the organization (order or directive of the manager). It should also specify the procedure for employees who need to travel (application, approval, visa, etc.).

There is a second option for accounting for these costs. According to paragraph 25 of Article 255 of the Tax Code of the Russian Federation, labor costs include any types of expenses incurred in favor of the employee, which are provided for by the labor and (or) collective agreement. At the same time, paragraph 26 of Article 270 of the Tax Code of the Russian Federation states that when determining the tax base, expenses for travel to and from work by public transport, special routes, and departmental transport are not taken into account. However, this rule does not apply to amounts that are included in the costs of production and sale of goods (work, services) due to the technological features of production, as well as cases where the cost of travel to and from work is provided for in employment agreements (contracts) and/or collective agreements.

As follows from the explanations contained in the letter of the Ministry of Finance of Russia dated November 27, 2015 No. 03-03-06/1/69181, when calculating income tax, organizations have the right to take into account expenses associated with the transportation of employees by taxi services. But subject to the following conditions: these expenses are due to the technological features of production or are provided for by employment agreements (contracts) and (or) collective agreements as a remuneration system, and are also incurred to carry out activities aimed at generating income. (See “The Ministry of Finance announced in which case taxi costs for employees reduce taxable income”).

Thus, the organization has the right to take into account the costs of taxi services as part of labor costs (subclause 25 of Article 255 of the Tax Code of the Russian Federation) if the above conditions are met. In particular, if the organization is located far from public transport stops or there are other technological features of production, due to which employees use taxi services for business trips, and payment of these expenses is provided for in employment contracts. Since the rules of Article 255 of the Tax Code of the Russian Federation also apply when determining the object of taxation according to the simplified tax system, all of the above is also relevant for taxpayers using this special regime (subclause 6, clause 1 and clause 2, article 346.16 of the Tax Code of the Russian Federation)

But with this approach to accounting for the costs under consideration, one must be prepared for possible claims from tax authorities regarding the calculation of personal income tax and insurance premiums. Therefore, we recommend taking into account the cost of a taxi for business trips according to the first option, that is, as the cost of maintaining official transport. With this method of accounting, the focus of costs on the interests of the organization, and not individuals, is obvious, which eliminates questions regarding both personal income tax and insurance premiums.

Calculate your salary, contributions and personal income tax for free in the web service

Personal income tax

- If an employee uses a taxi for production purposes - traveling by taxi to the destination on a business trip or back - such amounts are not subject to personal income tax.

In this case, the employer must have documents confirming payment for a taxi on a business trip. This opinion was voiced in the letter of the Federal Tax Service of Russia for Moscow dated January 28, 2019 No. 13-11/011687. Otherwise, in the absence of documents justifying production necessity or payment for a taxi, will be imposed .

BSO for taxis from July 1, 2021

Astral

October 16, 2021 6375

OFD

A business traveler often has to travel around the city by taxi. In order not to pay for such business trips out of his own pocket, he needs to confirm his expenses. A strict reporting form will help with this. We talk about all the intricacies associated with BSO for taxis in 2021 in the article.

July 2021 brought with it not only legislative changes in the scope of online cash registers, but also the abolition of printed strict reporting forms. Now the BSO should be printed using a cash register in fiscal mode. In terms of details, it is not much different from a regular cash receipt; it should even have a QR code. In fact, the only important difference between a BSO and a check is their name.

This means that from July 1, 2019, a passenger taxi driver is required to use an online cash register and, after completing an order, issue the passenger with a strict reporting form printed using it.

Procedure for issuing BSO:

- in paper form ─ issuance of an electronic form printed using an online cash register;

- in electronic form ─ sending the BSO to the email address specified by the passenger.

For issuing old-style forms and not using an online cash register, the law provides for a fine of 30,000 rubles (Part 2 of Article 14.5 of the Code of Administrative Offenses of the Russian Federation).

Exceptions to the rules

But there is one “but”. On June 6, 2021, Vladimir Putin signed amendments to Federal Law No. 54-FZ, according to which individual entrepreneurs without employees have the right to a deferment from using online cash registers until July 1, 2021.

A logical question arises: what should a passenger taxi driver, registered as an individual entrepreneur and without employees, be given to a passenger?

According to Law No. 129-FZ dated 06/06/2019 and Letter of the Ministry of Finance No. 03-01-15/28134 dated 04/18/2019, in this case, the individual entrepreneur can issue any paper document confirming payment. This could be a receipt or receipt. The law does not stipulate the form of such a receipt, but it is better if it contains the details of the primary document:

- name, date;

- seller's name;

- name of service, price;

- Full name and signature.

In addition, drivers who work for online aggregators, such as Yandex.Taxi, are not required to use an online cash register. All responsibility for issuing documents confirming expenses falls on the shoulders of the aggregator itself.

Astral

October 16, 2021 6375

Was the article helpful?

75% of readers find the article useful

Thanks for your feedback!

Comments for the site

Cackl e

Products by direction

Astral.OFD

—> Online service for transmitting fiscal data in accordance with the requirements of 54-FZ

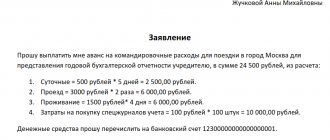

Documents for a taxi on a business trip

Confirmation of taxi expenses - an advance report for a business trip with supporting documents attached to it. Supporting documents for taxi services can be:

- act (in case of payment for a taxi by bank transfer by the employer under an agreement with the carrier);

- receipt (BSO);

- cash receipt (issued by the driver to the passenger).

Additional mandatory receipt details (BSO) for taxis are determined by Decree of the Government of the Russian Federation dated February 14, 2009 No. 112 in the Rules for the transportation of passengers and luggage by road and urban ground electric transport. Such documents must indicate:

- FULL NAME. employee (passenger);

- place of destination and departure;

- boarding and disembarking times.

Taxi expenses for tax purposes, income minus can be taken in

The mandatory details on documents confirming the use of a taxi service have already been discussed. You need to choose some of these options yourself during the transition to the “simplified” version.

Note: The effective rate will be set at the start of the tax period. The organization also bears expenses for third parties (guests), where it pays for a taxi from the airport to the office, or for moving around the city.

Should our organization withhold personal income tax from employees of the organization if this is not a business trip?

2. Do such expenses reduce income tax if the employee attaches a memo with justification? Should an organization take data from third parties in order to submit information on them to the Federal Tax Service in Form 2-NDFL (as receiving income in kind). Does he have the right to take into account in expenses under the simplified tax system the costs of the employee’s travel, including by taxi, to the place of business trip and back to the place of permanent work?

What documents confirm taxi costs? Yes, the “simplifier” has the right to include in expenses the cost of a passenger taxi incurred by an employee who is sent on a business trip.

These expenses must be documented with established documents. 13 clause 1 art. 346.16 of the Tax Code of the Russian Federation, when determining the object of taxation, a taxpayer applying the simplified tax system with the object of taxation in the form of income reduced by the amount of expenses, reduces the received income by business trip expenses.

Based on paragraph 1 of Art. 252 of the Tax Code of the Russian Federation recognizes justified and documented expenses incurred by the taxpayer. — name, series and number of the receipt; — cost of using a passenger taxi; - last name, first name, patronymic and signature of the person authorized to carry out settlements.

Let's sum it up

Taxi expenses incurred on a business trip can be taken into account for profit tax purposes, provided that the expenses are justified and documented.

If such expenses of a business traveler are included in income expenses, then they are not subject to personal income tax. If the employer compensates the employee for taxi expenses that are not sufficiently justified economically or are not supported by documents, then personal income tax should be withheld from such amounts.

Read also

15.05.2020

Personal income tax on travel expenses

If the need to use a taxi on a business trip is completely justified and caused by the current need, then the employee does not have an economic benefit. This means that personal income tax does not need to be calculated and withheld. These types of trips are driven by the interests of the organization, not the employee.

You might be interested in:

Daily allowances for business trips abroad: expense norms and accounting procedures

The organization must have supporting documents. They indicate the fact that the taxi was used by the employee for official purposes. In addition, it is advisable to specify the validity of such costs in internal documents, for example, in the regulations on business trips.

Also, the employee’s expenses for hiring a taxi do not need to be taken into account as part of the base for calculating insurance premiums. The object of their taxation is payments to employees in bilateral labor relations or under a contract. The subject of the latter is usually the provision by a citizen of certain services or the performance of work for a customer.

Attention! When paying for services for hiring a taxi or a car without a driver, the benefit accrues to the organization, not the employees. Therefore, there is no need to impose insurance premiums on these costs.

However, if an organization pays for taxi expenses that are not documented or found to be unreasonable, then these amounts must be subject to personal income tax and insurance premiums. Indeed, in such a situation, this will be considered as the employee receiving a benefit.

How to register an online cash register for a taxi according to the law

When collaborating with partners of aggregators, private traders who are not registered with the Federal Tax Service act outside the legal framework, since they receive money for the trip, give a commission, but do not pay taxes. In this situation, there are 4 legal options:

Newjer Atol 91F

- Get a job in a taxi company under an employment contract. The organization hiring drivers is required to equip all vehicles with terminals.

- Open an individual entrepreneur (using a simplified, imputed or patent system) and work on your own car (in a taxi company or independently). Individual entrepreneurs will have to set up an online cash register for taxis at their own expense.

- Open an individual entrepreneur and drive clients in a rented car. The CCT is set by the owner of the car who rented it out.

- Become self-employed.

When the car arrives, ask the driver again if he is ready to give you a document. If the taxi driver refuses, then you should remind him of the provisions of federal legislation. And specifically about Law No. 54 of May 22, 2003, as well as on the rules for the transportation of passengers No. 112 of February 14, 2009.

There is no need to despair. Typically, in any city or other locality there is more than one taxi ordering service. The employee should independently find out which service is ready to provide checks and receipts. That is, you need to find out in advance which taxi - with a receipt. Moscow, for example, is ready to offer dozens of different options. Each of the companies operates officially and is ready to document payment for the trip.

What is the problem

- Full name of the company or individual entrepreneur carrying out transportation. And also all the details of the individual entrepreneur or company, that is, tax identification number, checkpoint, location address, contact numbers.

- The date of provision of services, that is, the date of travel, as well as the date and time of issue of the form.

- The unit price of the service provided, for example, the price per kilometer, as well as the total cost of the trip.

- FULL NAME. driver or other responsible person who made the payment.