What applies to business travel expenses?

Most of the employee's duties must be performed directly at his main place of work.

However, there are often situations in which it is necessary to send an employee to another location. For example, to submit reports to a higher authority, to undergo retraining, or to conclude an agreement. Regardless of the purpose of the trip, travel expenses must be paid by the employer and then reflected in the organization's accounting records. What is required by law (Article 168 of the Labor Code of the Russian Federation):

- The employee’s workplace, as well as the position, will be retained for the entire period of absence - being on a business trip.

- Average salary for all days of stay on a business trip. Let us remind you that days of downtime, days of departure and arrival, as well as days of travel are subject to payment.

- Travel and accommodation expenses. The employer is obliged to pay at his own expense for rented housing, as well as the employee’s transportation costs.

- Costs that compensate for the inconveniences associated with a specialist living outside his home, that is, outside his main place of residence. Such costs are also called per diem.

- Other expenses. For example, purchasing teaching aids or additional supplies. However, such expenses must be agreed upon separately with management. Otherwise, the employee will not be reimbursed.

Principles for choosing KVR and KOSGU

First of all, we note that when sending an employee on a business trip, ensuring the guarantees enshrined in Articles 167, 168 of the Labor Code of the Russian Federation can be carried out in two ways:

- The employee is given an advance to purchase travel documents and pay for the hotel, and is paid a daily allowance. Expenses actually incurred for the business trip are also reimbursed upon return.

- The institution independently purchases travel (flight) tickets for the posted employee, pays for the hotel, purchases fuel, lubricants, etc.

The procedure for allocating expenses to CWR and KOSGU in both cases will differ.

Limit on travel expenses in 2021

For a long time, Russian legislation had limited norms for expenses on business trips. That is, the employee was calculated an advance for expenses during the trip, based on the current limits. It was not possible to obtain a refund for the overdrawn funds.

Currently, such limits have been abolished. They were preserved only for certain federal government employees. Consequently, organizations now determine their own limits.

IMPORTANT!

For public sector employees, different rules are established. The maximum permissible amounts for them are established by the local government body or the founder. Such norms can be circumvented; for example, autonomous institutions can set their own limit based on the economic situation of the state institution, or pay extra from business funds. This exception is not provided for government and budgetary types of organizations.

Let us remind you that such restrictions are established not only on daily costs. That is, during the financial crisis, most organizations introduced limits on both accommodation and travel, which does not allow employees to make unreasonable expenses.

At the same time, the Tax Code of the Russian Federation establishes a limit on the taxation of daily allowances. Thus, for travel expenses abroad there is a limit of 2,500 rubles per day, for trips within our country - 700 rubles per day. That is, amounts exceeding the specified limits must be included in the base for calculating personal income tax and insurance premiums.

Daily allowance in 2021

The monetary amount of daily allowance is determined by the company independently on the basis of a concluded collective agreement and can be recorded in the company’s accounting policies and employment contracts. For accounting purposes, there are no limits on these compensation amounts.

For tax accounting, daily allowance rates are determined in the following amount:

- When traveling around Russia - no more than 700 rubles per day per person;

- For business trips to the territory of a foreign state - no more than 2,500 rubles per person.

The organization has the right to set daily allowances in amounts greater than these standards. Then it will not be able to reduce the tax base for income tax by these excess amounts. Also, these funds must be included in the employee’s income, and personal income tax must be withheld from them.

The start of a business trip is the date the employee leaves work for his destination. At the same time, if the time is indicated in the supporting documents, then the period of the official trip begins to be calculated on that day until 0-00 hours.

Otherwise, the next day is considered the start day of the business trip. When determining the period of a business trip, it is necessary to remember that it includes not only working days, but holidays and weekends, days of travel, forced stops, periods of temporary disability that occurred during a business trip.

Example: An employee went on a business trip by plane on Monday at 10.00 from Moscow to St. Petersburg, returned on Tuesday at 0.10, it turns out that this is the next day and per diem must be paid for 2 days - for Monday and Tuesday .

A business trip can be interrupted on the basis of an order to recall an employee from a business trip, which is drawn up in any form and must necessarily contain information about its reason.

In this case, daily allowances should be accrued only for the time you are actually on a business trip. The employee must return the remaining funds to the company. If there is a need to send him on a business trip again, then all documents must be filled out again.

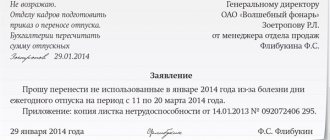

Example: claim for travel expenses

If an employee wishes to receive an advance in cash for travel expenses, an invoice does not need to be specified.

Please note that the application must be checked by the responsible accountant before being submitted to the manager. The accounting employee must verify the correctness of calculations for the number of days, according to the limits established by the institution and other conditions.

Then the manager endorses the application. Based on the document, you can immediately issue funds or draw up an order.

Optimization and improvement of provision for business travelers

Since business trips cannot be removed from the current activities of organizations, the legislator constantly monitors the standards for payment of employee overhead expenses. Thus, among the changes for 2021, design optimization should be noted. Forms of travel certificates, official assignments and reports on their execution have been eliminated from the list of mandatory documents. At the same time, the Law does not oblige them to be excluded from the document flow.

In addition, the legislator leaves organizations with an arsenal to optimize the tax burden, while not limiting enterprises in the amount of daily allowance. A business trip, as an integral part of the working regime, should be paid, if not generously, then at least take on the motivational component of the employee. It should also be noted that there have been changes in the structure of travel expenses due to the addition of a new type of cost - resort tax. Currently, entry regimes are being studied in pilot projects, but will soon become mandatory in a number of regions - summer holiday centers.

Similar articles

- Standard daily travel expenses in 2021

- Business trip 2018

- Payment of daily travel expenses in 2021

- How are travel days paid?

- Amount of travel expenses in 2021 per diem

Option No. 1. Limits approved

If the institution has limits on business travel expenses in separate local regulations, then ask to provide this information. Calculate the amount of the requested advance using the formula:

Cost rate = number of days × limit per day.

Transport costs are rarely limited, since tickets (travel) are paid upon delivery. However, it should be borne in mind that the employer has the right to refuse reimbursement of expenses for travel on certain types of transport. For example, a taxi ride when there are regular flights (train, bus). They may also refuse to pay for a premium seat (business or first class ticket).

Example.

The employee is sent to Tver for 11 days. The institution has the following limits:

- daily allowance - 200 rubles per day;

- accommodation - 700 rubles per day;

- actual travel.

Therefore, a specialist has the right to claim:

Daily allowance - 2200 (11 × 200 rubles), accommodation - 7000 (10 × 700) and 2000 for tickets at actual cost (1000 one way).

Option number 2. No limits

If the institution does not provide restrictions on who. expenses, estimates can be drawn up for a larger amount. However, you should not escape reality. All the same, the costs will have to be documented. In addition, a luxury hotel room and a business class flight are unlikely to be paid for using budget money.

How to plan costs correctly:

- Check the cost of tickets (train, bus, plane, etc.). Include the best travel option to your destination in your travel cost estimate.

- Book your hotel room. When making a reservation, immediately check the cost per day. Take this price into account in your calculations.

- Daily allowance. The amount of such costs should be agreed with management. Let us remind you that there are no restrictions in the legislation. However, if the amount exceeds 700 rubles per day when traveling within Russia and 2,500 rubles per day for foreign business trips, then the difference is subject to taxation (personal income tax and insurance contributions).

IMPORTANT!

To eliminate problems with supervisors, develop and approve a travel policy in the institution. And also establish in a separate local order the norms of expenses for business trips.

If this is not done, then some of the institution’s costs may be considered inappropriate. As a result, the manager will be fined and forced to return the money to the budget. When approving standards, follow the recommendations and orders of higher ministries and departments.

What nuances do you need to know about?

Any issue related to material payments has its own nuances that you need to know about, and this is no exception to the rule. For example, the head of an enterprise usually checks all the receipts provided by his employee, and if he believes that the latter spent too much money on lunch at a restaurant, then he may quite rightly be indignant and consider these expenses unreasonable. It must be said right away that travel expenses abroad will also not be changed in 2021, but everyone understands that 2,500 rubles per day may not be enough to pay for travel, food and accommodation, therefore, when monitoring the flow of funds for those employees who went on business trips abroad , employers are more loyal to spending.

Will the rumors about the cancellation of travel allowances be confirmed?

It’s also worth saying a few words about the fact that no one plans to cancel compensation for travel expenses, although rumors about this have been agitating the public for quite some time. During the crisis, this measure seemed simply necessary, because many enterprises suffered from a lack of funding, but it was impossible to accept it, because then company employees would have the full right to refuse business trips at their own expense. Today it is known for sure that the rate for reimbursement of travel expenses in 2021 will remain the same, therefore, there is definitely no need to worry about the cancellation of financial assistance. Moreover, there are no prerequisites for this, so we can say for sure that the country’s economy is gradually recovering, and at the same time its financial problems are decreasing, which means that financial support for citizens should gradually increase.

What documents are needed for a business trip?

Let's say the application for an advance payment is approved. What to do next?

First of all, draw up an order to send a specialist on a business trip. In the administrative act it is necessary to indicate not only the full name. and the position of the employee, but also the period of business trip, destination, purpose of the trip. It is acceptable to provide additional information about the job assignment. For example, write in the order “sent for submission of annual financial statements to the Ministry of Education.”

Use the unified order form No. T-9 (OKUD 0301022), approved by Resolution of the State Statistics Committee of the Russian Federation dated January 5, 2004 No. 1.

The use of a unified order form is not necessary. The institution has the right to use a form developed independently. However, regardless of the chosen form of the document, it must be fixed in the accounting policy.

Example of filling out a unified document

In addition to the order to send on a business trip and pay an advance for travel expenses, the employer must issue a work assignment. This document contains a list of duties that the employee must perform while traveling. However, the formation of a job assignment is not mandatory. It is quite enough to list the duties and purposes of the trip in the order.

Just a couple of years ago, it was possible to confirm travel expenses only with a special document - a travel certificate. Other checks and receipts were considered secondary documents. Currently, legal norms have changed. Now you do not need to issue a special certificate. But many institutions continue to issue the canceled form. Why?

Firstly, the validity of the form was preserved. Officials only determined that the document has now become optional. However, it can be issued at the discretion of the company management. Secondly, the ID allows you to confirm your daily expenses. Thirdly, the form allows you to mark the receiving party. That is, confirm that the employee has arrived at his destination.

You can develop your own certificate form or use the unified form No. T-10 (OKUD 0301024), approved by Resolution of the State Statistics Committee of the Russian Federation No. 1 of 01/05/2004.

KOSGU

As noted above, travel expenses are considered in the context of the Labor Code of the Russian Federation as reimbursements (compensations) related to the employee’s performance of work duties. In international statistical practice, such payments are not considered as payments in the interests of employees, but belong to the category of expenses made by the employee for the purpose of performing work duties. In this regard, reimbursement of expenses related to business trips (travel, accommodation, other expenses related to the performance of official assignments on a business trip), starting in 2021, were transferred to subarticle 226 “Other work, Other payments” * (3) KOSGU ( clause 7, clause 10.2.6 clause 10 of Procedure No. 209n, clause 2.1.4 of the Methodological recommendations for the procedure for applying KOSGU, communicated by letter of the Ministry of Finance of Russia dated June 29, 2018 No. 02-05-10/45153).

More on the topic: Budget reporting 2021: innovations and changes

If we are not talking about reimbursement of expenses, but about providing the employee with everything necessary before a business trip (when the institution independently purchases tickets, pays for a hotel, etc.), then the institution’s expenses will include, in particular:

- to subarticle 222 “Transport Other work, Payment for work, services” of KOSGU, articles and subarticles of group 300 “Receipt of non-financial assets” of KOSGU, based on the economic sense.

Note! Expenses regarding daily allowances are still included in subarticle 212 “Other non-social payments to staff in cash” of KOSGU (clause 10.1.2 clause 10 of Procedure No. 209n).

How to report travel expenses

Expenses incurred on a business trip must be reimbursed by the employer. Of course, within the established norm, in compliance with expediency and validity, as well as in the presence of supporting documents. So, how to confirm a specific type of cost:

- Transport. For this category of expenses, supporting documents are tickets, checks and taxi receipts, electronic receipts (for example, when issuing an electronic ticket).

- Housing. A receipt from a hotel or a rental agreement can confirm the rental of housing. Please note that when renting a home from third parties, it is necessary to check the correctness of the lease agreement. You should also be given a check, receipt or receipt indicating that you have received money to pay for the rent. Incorrectly completed documents cannot be accepted for registration.

- Daily allowance. It will not be possible to confirm this category of travel expenses with a special document. Previously, an identity card was used for this; now it is not necessary to use this form. You can confirm the number of days using your tickets.

- Other expenses. To receive reimbursement for other types of expenses while traveling, please attach receipts, sales receipts, receipts, invoices and other documents. Please note that such costs should be agreed upon with management in advance. Otherwise, you may be denied payment.

If you received money from someone. expenses in advance, that is, a report, then upon return you must fill out an advance report. Attach all supporting checks, tickets and receipts to it and submit it to the accounting department.

IMPORTANT!

The advance report must be submitted within three days of returning from a business trip. Exception: the employee fell ill immediately after completing the trip. In this case, you should report for the advance on travel expenses no later than 3 days from the date of closing the certificate of incapacity for work.

The accountant will check the advance report, check the authenticity and correctness of filling out the supporting documents. Based on the results of the inspection, final calculations will be made. The excess will have to be returned, and the overexpenditure will have to be paid extra.

What is considered a business trip?

The law contains a clear definition of what exactly can be considered a business trip. This is a trip during which you perform a work assignment for another company. In this case, the receiving party can be located either in the region where the subject is located or in another locality or country.

Trips to advanced training courses, as well as the temporary transfer of an employee to another structural unit located in the same area cannot be business trips, but such a transfer should not entail changes in the terms of the employment agreement.

However, an employee’s trip on instructions from management from the head office to the regional office and back will be considered a business trip.

The duration of the trip is determined by the management of the business entity and is specified in the business trip order or official assignment.

Attention: within 3 days from the date of return from a business trip, the employee must provide a report on the work done and documents confirming expenses.

Features of accounting

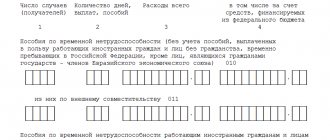

In the accounting of a budgetary institution, travel expenses should be reflected in the appropriate account:

- to reflect daily allowances - 0 208 12 000 “Settlements with accountable persons for other payments”, according to KVR 112 and KOSGU 212;

- to reflect other costs - according to subaccount 0 208 26 000, according to KVR 112 and KOSGU 226.

The new provisions have been in effect since 2021 (Orders of the Ministry of Finance No. 132n and No. 209n).

However, if the payment for housing is carried out by the organization itself, for example, an agreement for the provision of services has been concluded between the institution and the hotel, then such costs are reflected in account 0 302 26 000. And if payment for the hotel is carried out under an agreement between the organization and the hotel, but with accountable money through an employee, such costs We reflect on the account 0 208 26 000.

A similar procedure is provided for purchasing tickets. So, for example, if an employee himself bought a ticket for a train (bus, plane), then travel expenses for transport are reflected in account 0 208 26 000, according to CVR 112. If the institution entered into an agreement with a transport company and transferred money for the ticket from the current account , reflect the costs at 0 302 22 000, use KVR 244. But if the employee paid under such an agreement with accountable money, then reflect the transaction at 0 208 22 000, KVR 244, KOSGU 222.

KVR

One of the essential requirements of the approved structure of types of expenses, enshrined in clause 46.5 of Procedure No. 85n, is the reflection of travel expenses * (4), as follows:

- issuance of cash to seconded workers (employees) (or transfer to a bank card) on account of the guaranteed expenses listed above - according to CVR 112 “Other payments to personnel of institutions, with the exception of the wage fund”, 122 “Other payments to personnel of state (municipal) authorities, with the exception of the wage fund", 134 "Other payments to military personnel and employees with special ranks" and 142 "Other payments to personnel, with the exception of the wage fund" (see also clause 48.1.1.2, clause 48.1.2.2, clause 48.1.4.2 clause 48 of Order No. 85n);

- payment for the purchase of tickets for travel to and from the place of business trip and (or) rental of residential premises for seconded workers under agreements (contracts) - according to KVR 244 “Other procurement of goods, works and services”.

Thus, Procedure No. 85n clearly establishes the use of various CVRs when reimbursing an employee’s expenses and when an institution purchases services for him under a contract.

More on the topic: Operations with subsidies received from the founder: the procedure for reporting by budgetary institutions in 2021

Note! According to clause 46.5 of Procedure No. 85n, the list of other expenses incurred by a posted employee with the permission or knowledge of the employer, attributable to CVR 112, 122, 134 or 142, is determined by the employer in a collective agreement or local regulation (due to the specifics of the activities of individual main managers of budget funds - in a normative legal act). That is, if the relevant act does not indicate certain expenses incurred by an employee on a business trip with the knowledge of the employer, they cannot be attributed to CVR 112, 122, 134 or 142. In this case, the expenses will be attributed to CVR 244 * (5) .

As we can see, the attribution of travel expenses can be carried out according to various CVR and KOSGU, depending on whether funds are issued (compensated) to the employee or whether the institution purchases services for him. And the procedure for attributing other expenses incurred by an employee on a business trip depends on the availability of a list of such expenses, enshrined in the relevant act, and the presence of specific expenses in such an act.

Along with the above, it is interesting that if the purpose of the business trip is the purchase of material supplies, for example, fuels and lubricants, then the purchase costs should be reflected according to KVR 244 and subarticle 343 of KOSGU (letter of the Ministry of Finance of Russia dated March 15, 2019 No. 02-05-10/17872 ).

Let us remind you that the CWR and KOSGU expenditure subitems are used in mutual coordination. In this regard, we advise you to always check the CVR for coordination with the articles (sub-articles) of the KOSGU according to what is posted by the Ministry of Finance of Russia on its official website (www.minfin.ru). Please note: the table of correspondence between the CWR and the articles (subarticles) of the KOSGU related to expenses often undergoes changes. At the time of preparation of the material, the correspondence table posted on the website of the Ministry of Finance of Russia on 04/09/2020 is valid (Budget - Budget classification of the Russian Federation - Methodological office).