Home / Taxes / What is VAT and when does it increase to 20 percent? / Declaration

Back

Published: 08/09/2017

Reading time: 5 min

0

281

It is very important for an accountant, before submitting a VAT return, to double-check its completion, and in particular, the correct calculation of VAT payable to the state budget. This will help the company avoid penalties for possible errors and legal costs.

- Procedure 1: Checking VAT accrual

- Procedure 2: Checking the balance sheet and accounting

Procedure 1: Checking VAT accrual

Step-by-step algorithm:

- First of all, check the data from the general ledger. It is necessary to check the correspondence of the numbers and dates of the primary accompanying documentation that you use when filling out accounting records, check the amounts of payments and taxes on them. Correct all discrepancies and contradictions before the declaration falls into the hands of the tax inspector, otherwise you risk paying a penalty after a desk audit.

- Analyze the balance sheet. Now it is important to divide the data from accounts 60 and 62 into subaccounts, where 60.2 and 62.1 are always exclusively in debit, and 60.1 and 62.2 are in credit, respectively. If there is a contradiction, reconcile the balance at the end of the tax period using accounts and amounts from the books of purchases and sales.

- Next, you need to create a statement for account 41 “Goods”. The remaining goods must be in debit and not highlighted in red in accounting. Otherwise, if an error was made, check all issued and received invoices for mis-grading.

- In this order, you need to create a statement of account 19 “VAT on acquired values”, where the debit balance should be zero.

- If there were advances during the reporting period of the declaration, the balance sheet of subaccount 76 “Advances” should be opened. Multiply the credit of subaccount 62.2 by the VAT rate - the value should coincide with the credit at the end of the period.

- In the 1C program, you need to create a subaccount for counterparties, check all invoices, accompanying documents, amounts paid and received - they should not freeze. If you have signed multiple agreements with the same supplier or customer, break them down separately in your accounting. This will help you avoid getting lost in payments and advances, as well as VAT calculations.

- Be sure to check the data on the purchase and sales books for issued and received invoices: their numbers, dates, product names, amounts and costs - do not allow continuous numbering. The manager or chief accountant of the enterprise must approve the signatures and seals in the documentation if corrections have been made to them.

- Check the invoice journal: data on numbers and dates, VAT amounts, total cost, name of the buyer, TIN number and final amounts using the balance sheet. If the transfer of products was free of charge, invoices are not recorded in the journal. The invoice for the advance payment, if there was one, is also not registered.

- Next, it would be advisable to number the sales book, sew it together, certify the information with the seal and signature of the head of the organization, and indicate the number of pages on the last page on the reverse side.

- After checking the details of the purchase book, check the data with the specified statements. Tax documents must be registered in the period when the right to VAT deduction arose.

- If you missed an invoice for the last tax period, or made a mistake in it, cancel it. In this case, you need to fill out an additional sheet, draw up and submit an updated VAT return.

Certain categories of citizens are eligible to lease a plot of land on preferential terms.

How to properly register ownership of a land plot? The step-by-step algorithm is described.

Ownership of land can arise for several reasons. You can read about this in our article.

If you want to find out how to solve your particular problem in 2021, please contact us through the online consultant form or call:

- Moscow.

- Saint Petersburg.

How to check the VAT return using the balance sheet?

It is very important for an accountant, before submitting a VAT return, to double-check its completion, and in particular, the correct calculation of VAT payable to the state budget. This will help the company avoid penalties for possible errors and legal costs.

Procedure 1: Checking VAT accrual

Step-by-step algorithm:

- First of all, check the data from the general ledger. It is necessary to check the correspondence of the numbers and dates of the primary accompanying documentation that you use when filling out accounting records, check the amounts of payments and taxes on them. Correct all discrepancies and contradictions before the declaration falls into the hands of the tax inspector, otherwise you risk paying a penalty after a desk audit.

- Analyze the balance sheet. Now it is important to divide the data from accounts 60 and 62 into subaccounts, where 60.2 and 62.1 are always exclusively in debit, and 60.1 and 62.2 are in credit, respectively. If there is a contradiction, reconcile the balance at the end of the tax period using accounts and amounts from the books of purchases and sales.

- Next, you need to create a statement for account 41 “Goods”. The remaining goods must be in debit and not highlighted in red in accounting. Otherwise, if an error was made, check all issued and received invoices for mis-grading.

- In this order, you need to create a statement of account 19 “VAT on acquired values”, where the debit balance should be zero.

- If there were advances during the reporting period of the declaration, the balance sheet of subaccount 76 “Advances” should be opened. Multiply the credit of subaccount 62.2 by the VAT rate - the value should coincide with the credit at the end of the period.

- In the 1C program, you need to create a subaccount for counterparties, check all invoices, accompanying documents, amounts paid and received - they should not freeze. If you have signed multiple agreements with the same supplier or customer, break them down separately in your accounting. This will help you avoid getting lost in payments and advances, as well as VAT calculations.

- Be sure to check the data on the purchase and sales books for issued and received invoices: their numbers, dates, product names, amounts and costs - do not allow continuous numbering. The manager or chief accountant of the enterprise must approve the signatures and seals in the documentation if corrections have been made to them.

- Check the invoice journal: data on numbers and dates, VAT amounts, total cost, name of the buyer, TIN number and final amounts using the balance sheet. If the transfer of products was free of charge, invoices are not recorded in the journal. The invoice for the advance payment, if there was one, is also not registered.

- Next, it would be advisable to number the sales book, sew it together, certify the information with the seal and signature of the head of the organization, and indicate the number of pages on the last page on the reverse side.

- After checking the details of the purchase book, check the data with the specified statements. Tax documents must be registered in the period when the right to VAT deduction arose.

- If you missed an invoice for the last tax period, or made a mistake in it, cancel it. In this case, you need to fill out an additional sheet, draw up and submit an updated VAT return.

Procedure 2: Checking the balance sheet and accounting

To do this, use accounts 46, 47, 48, reconcile the data from the order journal 11, 13, statements 16 and 16a.

List of documentation to check the total turnover of product sales for tax purposes:

- statements of current bank accounts of the enterprise.

- bank and cash documents.

- statements of product sales and settlements.

- paid customer invoice, etc.

From the statement, determine:

- when the amount from the advance payment will be in the buyer's settlement account, and not in the sales account;

- Are there any errors in tax calculations?

All tax return data must match the data on the accounting forms.

Within the specified period, the taxpayer can correct errors in the prepared annual report. Failure to do so on time may result in a fine.

All of the above measures are necessary to prevent improper and unacceptable reduction in turnover and understatement of tax.

Dear readers, the information in the article may be out of date, please take advantage of a free consultation by calling: Moscow +7 , St. Petersburg +7 or using the feedback form below.

Source:

Procedure 2: Checking the balance sheet and accounting

Check all taxable turnovers. The amounts in the calculation of turnover must correspond to the accounting information.

To do this, use accounts 46, 47, 48, reconcile the data from the order journal 11, 13, statements 16 and 16a.

List of documentation to check the total turnover of product sales for tax purposes:

- statements of current bank accounts of the enterprise.

- bank and cash documents.

- statements of product sales and settlements.

- paid customer invoice, etc.

From the statement, determine:

- when the amount from the advance payment will be in the buyer's settlement account, and not in the sales account;

- Are there any errors in tax calculations?

All tax return data must match the data on the accounting forms.

Within the specified period, the taxpayer can correct errors in the prepared annual report. Failure to do so on time may result in a fine.

If you want to find out how to solve your particular problem, please contact us through the online consultant form or call:

- Moscow.

- Saint Petersburg.

The inspector will review all records of sales of goods when reconciling the readings in VAT calculations for taxable turnover.

All of the above measures are necessary to prevent improper and unacceptable reduction in turnover and understatement of tax.

Author's rating Author of the article Andrey Chernov Lawyer. Practice in real estate, labor law, family law, consumer protection. 3159 articles written

What is the object of interest of inspectors in the declaration

In full accordance with internal instructions, each employee of the desk audit department must recalculate the 44 control ratios available in letter No. GD-4-3/ [email protected] , and it is always crystal clear to him how to check the VAT return . After changes made to the form in 2015, the number of calculations required for a scrupulous verification has increased. This is due to the need for additional analysis of new sections 8–12, in which new tax reporting indicators have appeared.

In order to link VAT values in the fields of sections 1–7 and 8–12, the following new algorithms were introduced:

- Field 060 section 2 + field 110 section. 3 + fields 050 and 080 section. 4 + fields 050 and 130 section. 6 = fields 260 and 270 sections. 9.

If the result in section 9 turns out to be higher than the first part of the ratio, you will probably have to explain to the tax authorities why this happened.

- Field 190 sec. 3 + fields 030 and 040 section. 4 + fields 080 and 090 section. 5 + fields 060, 090 and 150 section. 6 = field 190 section 8.

If the second part of the equation is less than the first, you will also need to defend your case before the inspectors, preferably backing it up with weighty arguments.

- Sec. 8: field 180 = field 190.

The total at the end of the section should be equal to the total VAT deduction in the declaration.

- Sec. 9: field 200 = field 260, field 210 = field 270.

The total amount of VAT to be transferred must be equal to the total reflected on the last page of the section

- When field 050 section. 1 > 0, then field 190 section. 8 – (field 260 + field 270 section 9) > 0.

In a situation where the amount of VAT to be reduced turned out to be greater than the tax payable, the amount to be refunded from the budget is recorded in field 050 of section 1. In this case, it must be equal to the difference between the tax subject to deduction and the tax accrued for payment, in accordance with the payments made. calculations.

Tax agents should be sure to recalculate the following ratios:

- VAT payable: field 060 section. 2 = fields 200 and 210 sections. 9 with index 06 in field 010.

- VAT for deduction: field 180 section. 3 = field 180 div. 8 with index 06 in field 010.

The legality of applying the deduction is established in accordance with the letter of the Ministry of Finance of Russia dated October 23, 2013 No. 03-07-11/44418.

Organizations from which, in accordance with the Tax Code of the Russian Federation, the obligation to calculate and pay VAT has been removed, must necessarily clarify the following ratio: field 030 section. 1 = field 070 section 12.

The program will show an error if:

- VAT will be reflected in field 040 section. 1 or 9;

- section 1 is filled, and sec. 12 no;

- deductions are included in Sec. 8.

Organizations importing anything from abroad must also recalculate declaration data using the formulas:

- field 150 section 3 = field 180 div. 8 marked 20 in field 010;

- field 160 section 3 = field 180 div. 8 with index 19 in field 010.

First of all, the correct use of ciphers that reflect where the goods are imported from is clarified.

***

To protect themselves from excessive attention from fiscal authorities, companies should be extremely careful in checking the control ratios in the VAT tax return. The addition of new sheets to the declaration form since last year has made this issue even more relevant for most companies.

The growing volume of information that needs to be calculated and entered into VAT reporting documents leads to an increased risk of errors. In this regard, the tax department persistently asks payers to approach audit issues responsibly and, in order to simplify the procedure, invites everyone to familiarize themselves with the list of control ratios that are mandatory for use by inspectors.

A simple recalculation according to the algorithms given in letter No. GD-4-3/ [email protected] will most likely save the company from unjustified tax risks and claims from the Federal Tax Service. Moreover, there is nothing complicated in these formulas. They are understandable even for a beginner and inexperienced specialist.

Similar articles

- How can a tax agent fill out a VAT return?

- Filling out section 4 of the VAT return

- The updated form of the UTII declaration has been approved

- How to correctly fill out field 109 in a payment order?

- Sample of filling out a land tax return

How to check a VAT return in 1C

Published 10/18/2016 11:28

In this article I want to tell you a little about checking your VAT return. Of course, this is a complex and multifaceted process, which largely depends on the specifics of the organization’s activities and the composition of the operations performed. But, nevertheless, there are some basic techniques, without knowledge of which it will not be possible to understand the logic of filling out and checking this report. Now we will talk about one of these techniques, namely, reconciling the VAT return with information on account 68.02. We will consider an example based on 1C: Enterprise Accounting 8 edition 3.0, but the information provided is also relevant for other 1C version 8 programs.

So, in order to start checking, we need to open the completed VAT return and generate an “Account Analysis” report for account 68.02 for the tax period.

The “Credit” column of this report reflects the amount of calculated VAT, and the “Debit” column shows the amount of VAT claimed for deduction and transferred to the budget. We will check the “account analysis” with section 3 of the VAT return. Line 010 of Section 3 of the VAT return reflects the amounts of the tax base and the tax calculated on the sale of goods, works, and services at a rate of 18%. In our case, the organization carried out sales only at this rate, so the amount in line 010, in general, should coincide with the turnover of account 68.02 and account 90.03.

Also in the “Credit” column of the “Account Analysis” report we see the turnover on account 76.AB, i.e. VAT calculated on the amounts of advances received from buyers. Accordingly, we should see the same amount in the declaration on line 070. Now we check the tax deductions. The amount of VAT charged to our organization when purchasing goods, works, services is reflected in account 68.02 in correspondence with account 19, and in the declaration it falls on line 120.

The amount of VAT on offset advances from customers is displayed in the “Debit” column in correspondence with account 76.AB and in line 170 of section 3 of the VAT return.

I would like to draw your attention to several important points: - if during the tax period there were refunds of advances to buyers, then you must remember that the amounts of such refunds will be reflected on line 120 of section 3 of the VAT return, i.e. together with VAT on purchased values. Accordingly, when reconciling the declaration and analyzing account 68.02, there will be discrepancies by the same amount in turnover with accounts 19 and 76.AB (refund amounts will be reflected in correspondence with account 76.AB, but in the declaration they will appear in the line that we check with count 19). - if you want to check the total turnover in the debit and credit of account 68.02 with the total amounts of calculated VAT and VAT deductible on the declaration, then you need to remember that in the account analysis in the “Debit” column also reflects the amounts of paid VAT, which are not reflected in the declaration (turnover with a score of 51). — the final balance in account 68.02 will coincide with the amount of tax payable according to the declaration if there is no debt or overpayment for previous tax periods. Of course, the situation that we have considered is quite simple and illustrates only the basic principles of VAT verification. If VAT recovery operations, accounting at different tax rates or various returns are added, then the reconciliation becomes more complex and interesting. But I highly recommend checking the declaration with an analysis of account 68.02 for one simple reason: the declaration is filled out using information from the VAT tax registers, and the account analysis is performed according to the accounting entries. Unfortunately, in practice, I very often encounter discrepancies in these amounts, which are caused by errors in accounting, manual entries and adjustments. In this case, a simple reconciliation will help you find shortcomings, understand their causes and submit a correct VAT report. If you want more useful information about working with VAT, about filling out and checking the declaration in the 1C: Enterprise Accounting 8 program, and you would also like our written consultations on this topic, then we highly recommend our video course “VAT: from concept to declaration” , which has already helped a large number of accountants understand the calculation of this confusing tax. I wish you an easy reporting period and successful work in 1C programs!

Did you like the article? Subscribe to the newsletter for new materials

Our training courses and webinars

Reviews from our clients

>

Reconciliation of “Account Analysis” with the VAT return

Next, we will proceed to reconcile the “Account Analysis” with section 3 of the VAT return. Let us remind you that the “Credit” column displays the amount of calculated VAT, and the “Debit” column displays the amount of VAT that is subject to deduction and transfer to the budget.

In section 3 of the declaration, line 010, you can see the amount of the tax base and the tax that was calculated on the sale of goods and services at a rate of 18%. In the above example, the organization carried out sales only at this rate, therefore the amount in line 010, as a rule, coincides with the turnover of account 68.02 and account 90.03.

Please note that the “Credit” column in “Account Analysis” will show the turnover on account 76.AB - VAT, which was calculated from the amounts of advances from customers. You will see the same amount in the declaration on line 070.

VAT check

Current as of: February 20, 2021

The current form of the VAT return, as well as the fact that it is submitted to the Federal Tax Service in electronic form, allows tax authorities to conduct more in-depth desk audits of VAT reporting submitted by payers (clause 5 of Article 174 of the Tax Code of the Russian Federation, Letter of the Federal Tax Service of Russia dated August 20. 2015 No. PA-3-17/ [email protected] ).

After all, now inspectors can not only use control ratios to check the declaration for any inconsistencies in it (Letter of the Federal Tax Service of Russia dated March 23, 2015 No. GD-4-3 / [email protected] ), but also cross-check the data specified in your declaration and declarations of your counterparties.

For example, if the tax authorities discover that in section 8 of the declaration (information from the purchase book) you reflected the invoice data from the supplier, but the supplier himself did not reflect the data of the same invoice in section 9 of the declaration (information from the sales book), then this fact will raise questions among the inspectors, and you will be asked:

- or provide explanations;

- or submit an updated declaration.

Therefore, independently checking the declaration before submitting it to the Federal Tax Service will not be superfluous. After all, a correctly completed VAT return is a guarantee that the amount of tax to be paid/reimbursed is calculated accurately, and, therefore, the tax authorities will not have any complaints about either the declaration itself or the amount received into the budget.

How to check VAT yourself

You can conditionally check the calculation of VAT in two ways: independently and during a tax audit. Regulatory authorities have their own methods. Internal accounting uses several methods.

You need to independently check the correctness of the calculation of value added tax in the following ways:

- For advance payments

- Sales check

- According to the balance sheet

- Analysis of calculations from purchase books.

Timely monitoring of the correctness of calculations allows you to avoid many problems. This is the right approach, but it does not promise to be simple and fast.

This video will tell you how to check a VAT payer:

With this method of verification, it is easy to identify errors in VAT calculations. The process itself is not complicated, but it requires a lot of time, care and perseverance. It is required to analyze all records of the following operations:

- documentation of advance payments

- return of registered goods

- information on the fulfillment of their obligations by tax agents

- documents confirming receipt of any funds increasing the tax base

- data on receipt of funds during the sale, provision of services or performance of work, including for one’s own needs, during the transfer of property rights.

Transactions that are not subject to tax deductions are not taken into account. All other data must be carefully calculated. Analysis of sales ledger data should always be performed in conjunction with purchase documentation.

When calculating VAT using a purchase ledger, you can determine the amount of funds to be deducted. For VAT payers, this document is required, and when checking independently, the accountant needs to take into account the following items:

- Advance documentation

- Travel expenses

- Invoices from sellers

- Adjustment invoices

- Expenses for construction and installation works for own needs

- Customs declaration and related documents

- Application for import of goods and payment of indirect taxes.

It is necessary to calculate the volume of VAT amounts to be paid to the budget and determine the amount of funds to be reimbursed (for example, for construction, in case of overpayment from the budget, etc.). It is also necessary to take into account the paid amounts from advances received and sent to counterparties.

For correct calculation, you need to compare the debit data on subaccounts 60.2 and 62.1, take into account credit calculations (60.1 and 62.2). Determine the balance of the listed accounts at the end of the tax period, check with the books of purchases and sales. Additionally, you need to check the VAT on advances and purchased valuables. If calculated correctly, the data on the debit and credit subaccounts will coincide with sales and purchases. Otherwise, you need to check the correctness of the information entered in sales, purchases and advance payments.

Let's find out how to check VAT on advances received.

Advance payments subject to VAT require special attention. Accounting departments often have questions regarding calculations. This happens especially often if the advance payment and shipment of the goods occurred in the same tax period.

A number of orders of the Ministry of Finance imply separate calculations for the advance payment and the remaining amount to be paid. In some cases, it is acceptable not to issue an invoice for the advance payment. This occurs in the case of advance payment and shipment of goods on the same day. It is also sometimes practiced to refuse to calculate VAT on an advance payment if the difference with shipment is no more than 5 days.

The Federal Tax Service of Russia recommends avoiding this practice in order to eliminate unnecessary questions during the inspection. The tax base does not increase from the timely calculation of VAT, so its correct documentation prevents controversial situations with regulatory authorities. In this case, it is necessary to take into account not only advances paid, but also received.

We will tell you below how tax authorities (tax authorities) check the VAT return.

This video will tell you how to get a VAT deduction and then check its accrual:

VAT reconciliation with the tax office

In addition to checking the VAT return, it is also important to reconcile calculations with the budget for this tax.

To check whether all your VAT payments have been received by the budget and whether you have tax debts, submit an application to the Federal Tax Service indicating your desire to conduct a reconciliation. You can submit such an application:

- or on paper;

- or in electronic form (via TKS or through the Personal Account of a legal entity / individual entrepreneur on the Federal Tax Service website).

To generate a reconciliation report, tax authorities have 5 working days from the date of receipt of your application (clause 3.4.3 of the Regulations, approved by Order of the Federal Tax Service of Russia dated 09.09.2005 No. SAE-3-01 / [email protected] ), after which the report is transferred to you for reference.

If your data on calculations with the budget for VAT coincides with the data of the Federal Tax Service, then the act is signed without disagreement. If the data does not match, then you must indicate your indicators in the act and return this act to the inspectors in order to then understand the reasons for the discrepancies.

> How to check the VAT return (control ratios)?

Why do you need to check your VAT return?

What inspectors check

Results

VAT reconciliation by tax authorities

The Tax Service has an effective tool used as a system for checking VAT returns. This complex has been used since 2015 and is called ASK VAT 2. Using the system, the tax service can find out the transparency of the collection and track the chain from the manufacturer to the buyer.

There have already been changes in filing the declaration. All VAT returns are submitted electronically, calculations in the book of purchases and sales are included as an appendix to the audited declaration, and the reports are subsequently carefully processed. It is checked automatically; if payers made mistakes when specifying payments, they receive requests to provide explanations.

With the help of ASK VAT 2, it is possible to compare information from the invoices of the buyer and seller, it is possible to build a chain of counterparties, form a database in accordance with legal norms, and identify those who benefit from the tax gap. All submitted declarations for each period are analyzed.

If the payer has received requests for clarification, he needs to send a receipt for receipt of the document and analyze the errors and submit an updated document.

Why do you need to check your VAT return?

It is imperative to check the VAT return before submitting it to the Federal Tax Service in order to exclude errors in it and avoid submitting clarifications due to inconsistencies in the data.

How to check your VAT return? The Tax Service has established control ratios (hereinafter referred to as CS), according to which inspectors carry out their verification, to facilitate this procedure in the Federal Tax Service. However, taxpayers can also use the CC. They can be found in the Federal Tax Service letter dated March 23, 2015 No. GD-4-3/ [email protected] For reporting for the 1st quarter of 2021, you need to use the updated KS, which are intended for the current tax return form (see Federal Tax Service letter dated March 19. 2019 No. SD-4-3/ [email protected] ).

The formulas contained in the CS allow you to compare the indicators entered in sections 1–7, both within these sections and between them, and in conjunction with data from sections 8–12. For the convenience of users, all KS are presented in the letter of the Federal Tax Service in question in the form of a table.

In addition to the formulas, the tabular part also contains information about how the inspector will qualify the detected violation and what his actions will be.

However, checking the VAT return according to the Tax Code is the final stage of the verification. Therefore, before applying the CS, the taxpayer should check the accounting records. How to check a VAT return based on turnover or other accounting registers? Data from these registers should give the figures that will appear in the declaration:

- for accounts 90, 91 - in terms of sales volume for each tax rate;

- accounts 60, 62, 76 - in relation to the correspondence of the amounts of advances and VAT related to them;

- for account 19 - according to the amounts of deductions;

- account 68 - in terms of accounting for all VAT amounts involved in the calculation and forming the final result of the declaration.

Let's look at how to check a VAT return on turnover using an example.

Example.

The accountant of Smiley LLC filled out a VAT return and, before sending it to the Federal Tax Service, decided to reconcile the data with accounting (the rate of incoming and outgoing VAT is 20%).

To do this, he generated an analysis of account 68 VAT subaccount.

He also checked the speed by:

- Dt 62.1 x 20: 120 = Dt 90.3 = line 010 section 3;

- Kt 62.2 x 20: 120 = Dt 76 AB = line 070 section 3;

- Dt 62.2 x 20: 120 = Kt 76 AB = page 170 section 3;

- Kt 60 x 20: 120 = Dt 19.03 = page 120 section 3.

The accountant also verified the sales adjustment reflected in the VAT return, because an adjustment invoice was issued for the increase. The accountant recorded this information in pp. 040-090 section 9.

Checking the correctness of filling out the VAT return when maintaining complex VAT accounting

The pressing question is how to check the correctness of filling out the VAT return and avoid mistakes. It is especially popular among accountants. To reconcile the value added tax return, you need to study the control ratios of the indicators.

The check must be carried out without fail before submitting it to the tax service - according to VAT indicators, turnover and other parameters. The tax authorities have established control ratios, according to which inspectors carry out analysis to increase the speed of this procedure in the Federal Tax Service.

Taxpayers can use these indicators. KS formulas allow you to check the indicators reflected in sections 1-7, as well as in conjunction with sections 8-12.

Checking against benchmarks is the final stage of study. Therefore, it is recommended to reconcile accounting information before using this system. According to accounts 90, 91, the sales volume is checked for each rate, according to accounts 60, 62,76 the compliance of the amounts of advances and VAT is determined, and according to account 19 the amount of deductions is determined.

Thus, before submitting documentation, payers and agents must conduct a preliminary check so that they do not receive questions from fiscal authorities.

Often there are technical errors in declarations, which can be avoided by using the control ratios used by the Federal Tax Service.

What inspectors check

How to check the correctness of filling out the VAT return under the KS? When analyzing declarations, the necessary indicators are calculated using the formulas available in the methodology (depending on the status of the taxpayer and the nature of the transactions).

These also include formulas for reconciling values between sections 1–7 and 8–12:

- Page 060 section 2 + page 118 sec. 3 + pages 050 and 080 sec. 4 + page 050 and 130 sec. 6 = page 260 + page 270 sec. 9 (clause 1.27 KS) - if the amount of VAT in section. 9 will be greater than in Sect. 2–6, then the tax office will require clarification.

- Page 190 section 3 + pages 030 and 040 sec. 4 + pages 080 and 090 sec. 5 + pages 060, 090 and 150 sec. 6 = page 190 sec. 8 (clause 1.28 KS) - explanations from the taxpayer will be required if the deductions in section. 8 will be less than in section. 3–6.

- Sec. 8: page 180 = page 190 (clause 1.32 KS) - the amount of VAT to be deducted must coincide with the total value on the last page of the section.

- Sec. 9: page 200 = page 260; page 210 = page 270 (clauses 1.37, 1.38 KS) - the amount of VAT payable must coincide with the total value on the last page of the section.

- If page 050 sec. 1 > 0, then page 190 sec. 8 - (page 260 + page 270 section 9) > 0 (clause 1.25 KS) - if deductions exceed the amount of VAT payable, then the amount to be reimbursed must be indicated in page 050 of section 1, in this case the amount of compensation must be equal to the difference between all deductions and the calculated VAT.

When checking returns submitted by tax agents:

- VAT payable: page 060 section. 2 = page 200 and 210 sec. 9 indicating “06” on page 010 (clause 1.26 KS); VAT (right to deduction): page 180 section. 3 = page 180 sec. 8 indicating “06” in page 010 (clause 1.31 KS) - the tax agent’s right to deduction is checked in accordance with the recommendations set out in the letter of the Ministry of Finance dated October 23, 2013 No. 03-07-11/44418.

When checking the declarations of taxpayers exempt from VAT:

- Page 030 section 1 = page 070 sec. 12 (clause 1.24 KS) - the program will show an error if the company indicates VAT on page 040 of section. 1 or in section. 9; It would also be a mistake to fill out section. 1 without filling out section. 12; there will also be an error when filling out deductions in section. 8.

Read about the VAT exemption procedure in the article “How to properly exempt from VAT.”

When checking declarations of importing companies:

- Page 150 section 3 = page 180 sec. 8 with the indication “20” on page 010 (clause 1.29 KS).

- Page 160 section 3 = page 180 sec. 8 indicating “19” in page 010 (clause 1.30 of the Constitutional Code) - here it is important to correctly indicate the codes: imports from the EAEU countries - 19, from other countries - 20.

Filling out a VAT return

Until 2014, the main condition for choosing a declaration format was the current number of employees. If an employer employed more than 100 people, reporting must be provided electronically. For other subjects, regular paper forms were also accepted.

Starting from the 1st quarter of 2014, VAT returns are provided only in electronic format. An exception is made only for a small category of subjects:

- tax agents who are not VAT payers;

- tax agents are VAT payers, but exempt from the obligation to charge it.

If this group of persons issues invoices with an allocated tax amount in favor of third parties, then it loses the right to report using paper media.

Taxpayer online

A new tax return 6-NDFL has been implemented, format version 5.02 for quarterly reporting, starting from the fourth quarter of 2017; The water tax calculation has been updated.

11.01.2019

In Taxpayer Online, the 2021 reporting year is open for working with the Declarations and 2-NDFL section.

29.12.2018

A new form and format of 2-NDFL version 5.06 has been implemented for reporting for 2021.

30.10.2018

A new feature in the “Sending reports via the Internet” section, which allows you to download a ZIP archive of the necessary reports sent to the Federal Tax Service for submission to the Bank to confirm that you are submitting reports correctly. To do this, select the report you need, then in the “Details” tab you will find the item “Get a ZIP archive of the report for the bank”; by clicking on the floppy disk, the archive will be downloaded to your computer.

06.08.2018

A new opportunity in the “Sending reports via the Internet” section is to generate special requests to the Federal Tax Service (Section “Letters”). The following types of requests are available:

- certificate on the status of settlements for taxes, fees, insurance premiums, penalties, fines, interest

- statement of transactions for settlements with the budget

- list of tax returns (calculations) and financial statements

- act of joint reconciliation of calculations for taxes, fees, insurance premiums, penalties, fines, interest

- a certificate confirming the fulfillment by the taxman (fee payer, insurance premium payer, tax agent) of the obligation to pay taxes, fees, penalties, fines

12.06.2018

Added support for format 5.05 of section 2-NDFL.

25.04.2018

The information collection sections “Information about the organization” and “Wizard for connecting to sending reports” have been combined. Now the first section is the minimum set of information required to work with reporting sections, and the second section “Additional information” includes the information necessary to connect to sending reports and takes into account the rest of the data you previously entered.

09.02.2018

In section 2-NDFL, Certificate 2-NDFL is generated according to the old format 5.04. Employers have the right to submit certificates of income of individuals in form 2-NDFL for 2021 in the new and old forms. To generate according to the new format 5.05, please use “Taxpayer PRO” () Information message:

- By Order of the Federal Tax Service of Russia dated January 17, 2018 N ММВ-7-11/ [email protected] changes were made to the certificate form, in particular, allowing the successor organization to submit certificates in Form 2-NDFL for the reorganized organization to the tax authority at the place of its registration. In addition, the new form does not contain the “Residence address in the Russian Federation” field.

- Tax authorities are instructed to ensure the acceptance of these certificates for 2021 in the previously approved form, as well as in the new form, taking into account the changes made.

08.02.2018

Added auto-fill feature in the "Organization Information" section. Now you can enter your organization details in one click!

29.12.2017

Major update to the “Organization Information” section.

04.03.2017

A new SZV-M report has been implemented. The report must be submitted monthly no later than the 10th day of the following month. The service includes: a form and a list of insured persons for printing, as well as preparation and uploading of a report in electronic form.

22.02.2017

2-NDFL: new directories of income and deductions have been connected, import of 2-NDFL files has been updated.

05.12.2016

Major update to the Reporting Manager (section Sending reports via the Internet)

- automatic receipt of incoming documents;

- notification by mail about important events in the Reporting Manager (incoming Federal Tax Service Requirements, replies about sent reports, etc.);

- improved capabilities for working with separate document flow;

- added statuses of sent reports;

- The informal correspondence section has been improved.

How to check a VAT return: indicators that the tax office checks

- the ratio of total sales and total revenue (this indicator is reflected in the Company’s statements of profit and loss). For example: combining UTII with the general tax regime, the amount of revenue according to the VAT return will be less than that reflected in the profit and loss statements.

- comparison of indicators from the VAT return with indicators from the income tax return (for example, the amount of sales revenue according to these documents). Deviations in amounts are acceptable if part of the profit came from non-operating income. When comparing these documents, it is necessary to take into account the differences by period: a VAT return is prepared for each quarter, and profit reports are generated incrementally towards the end of the year.

- the ratio of previously received advances and the amount of VAT on sales . First of all, attention will be drawn to the excess of the advance over the specified amount. Although this is possible if not all implementation was completed during the reporting period.

What verification formulas are used to compare data from sections 1 to 7 with data from sections 8 to 12

The following abbreviations are used in the given formulas for checking the KS: page - s, section - r.

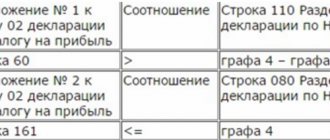

- According to paragraph 1.27: p.060 r.2 + p.110 r.3 + p.050 and p.080 r.4 + p.050 and p.130 r.6 = p.260 + p.270 r.9 (when the VAT amount in section 9 is greater than in sections 1 to 6, the Federal Tax Service will request clarification on this fact).

- According to paragraph 1.28: p.190 r.3 + p.030 and p.040 r.4 + p.080 and p.090 r.5 + p.060, p.090, p.150 r.6 = p. 190 rub. 8 (will attract the attention of the Federal Tax Service when deductions in section 8 are less than in sections 3 to 6).

- According to clause 1.32: p.8 / p.180 = p.190 (the amount of VAT to be deducted must match the total on the last page of the section).

- According to paragraph 1.37: p.9 / p.200 = p.260; p.210 is equal to p.270 (the amount of VAT payable must match the total on the last page of the section).

- According to clause 1.25: if p.050 r.1 > 0, then p.190 r.8 – (p.260 + p.270 r.9) > 0 (when deductions exceed the total VAT payable, the amount must be paid for reimbursement in p.050 r.1; the amount of reimbursement is equal to the difference of all deductions and calculated VAT).