Can a founder lend to his company?

The company and its founder, if necessary, can act as parties to a loan agreement - a mutual agreement on the transfer of funds or other property to the borrower from the lender into ownership.

Find out more about borrowed funds by following the link.

Borrowing relationships with the founder allow the company to urgently receive money or other items at the lowest cost:

- for carrying out current business activities;

- expansion of the material base;

- introduction of new technologies;

- for other purposes (for making a deposit for participation in a tender, paying off debts, etc.).

There are no special regulatory restrictions in relation to the company (borrower) and the founder (lender). Therefore, the founder can lend his company:

- money or any other property that has common generic characteristics (model, color, variety, etc.) - clause 1 of Art. 807 Civil Code of the Russian Federation;

- borrowed funds in any amount and for any period;

- with or without interest.

You can view and download a sample interest-free loan agreement between the founder and the organization in ConsultantPlus. Trial access to the system is provided free of charge.

The borrowing company can borrow from the founder:

- regardless of the size of its share in the authorized capital;

- for specific purposes (targeted loan) or without specifying the purpose of the loan;

- subject to the obligation to return the borrowed funds received and to formalize the loan agreement in writing (Article 808 of the Civil Code of the Russian Federation).

ConsultantPlus has tax specialists’ answers to various questions from taxpayers. For example, Advisor to the State Civil Service of the Russian Federation, 1st class A.A. Batarin explained:

If you don't have access to the system, get a free trial online.

Financial assistance from the founder

The wiring will look like this:

- on the date of registration of the minutes of the meeting of participants (or the decision of the sole founder), it is necessary to enter debit 75, subaccount “Funds of the founders aimed at covering the loss”, credit 84 - a decision was made to pay off the loss at the expense of the shareholder (founder);

- on the date of receipt of funds to the account, debit 50 (51), credit 75, subaccount “Funds of the founders aimed at covering losses” is entered - finances were received from the founder to cover losses at the end of the reporting year.

EXAMPLE. CJSC Stalprokat applies a general taxation system. According to the financial results of 2021, it shows a loss in the amount of 600,000 rubles. The founders of CJSC Stalprokat are R. I. Proskurov (share in the authorized capital 51%), N. S. Probirchenko (share in the authorized capital 28%) and L. D. Samoilova (share 21%). In addition, the period for which money can be issued on account is also not established by law. Another thing is that companies, as a rule, themselves set both the upper limit for the amounts issued for reporting and the period for which they are issued.

Otherwise, it is difficult to control the timely return of money by employees. And in this case, you can already set a specific date for the return of money.

The fact is that the period during which the employee must account for the amounts received is precisely stipulated. It is stated in paragraph 11 of the Procedure for Conducting Cash Transactions (approved by decision of the Board of Directors of the Bank of Russia dated September 22, 1993 No. 40) and is three working days from the moment the employee was supposed to return the money.

Read more: Database of enforcement proceedings of Yaroslavl

However, even if this deadline is missed, nothing bad will happen. The fact is that no liability is provided for such a violation.

Loan agreement with the founder: how to protect yourself from mistakes?

The return of money under the loan agreement is one of the final stages of the borrowing relationship. It is preceded by such important procedures as:

- agreeing on the terms of the loan;

- drawing up a loan agreement;

- transfer of borrowed funds from the founder to the company and preparation of a supporting document (transfer and acceptance certificate, receipt, etc.);

- reflection in accounting of operations to obtain borrowed funds.

If mistakes are made in these steps, problems may arise at the loan repayment stage. Therefore, check in advance:

- whether the property transferred under the loan agreement has individual characteristics (for example, a car with a title and identification number cannot be the subject of a loan);

- currency of the monetary obligation - according to Art. 317 of the Civil Code of the Russian Federation, such an obligation must be expressed in rubles (foreign currency may appear in the loan agreement, but only as an equivalent at the rate of the Central Bank of the Russian Federation);

- whether the loan agreement provides for all its essential (subject of the loan and its repayment) and additional (repayment period, interest-free condition, etc.) conditions.

IMPORTANT! If the loan agreement does not contain provisions on interest or the absence thereof, the loan is considered interest-bearing. Interest is calculated based on the refinancing rate (clause 1 of Article 809 of the Civil Code of the Russian Federation). The contract also cannot stipulate that the loan is irrevocable. According to paragraph 1 of Art. 807 of the Civil Code of the Russian Federation, the lender is a priori obliged to repay the loan to the lender.

Find out what conditions are necessarily included in the purchase and sale agreement for an apartment from the material “Essential terms of the purchase and sale agreement under the Civil Code of the Russian Federation.”

Loan repayment: what to consider first?

Before deciding whether to return the interest-free loan to the founder on the card, you need to check:

- the founder-lender has no debt to contribute a share to the authorized capital - if the founder has not contributed his “authorized” share in a timely manner or has not transferred it to the company in full, the borrowed funds received will be used to pay off such debt, and there will be nothing to return to his card;

- the presence in the loan agreement of a condition allowing the use of a method of returning borrowed money to the founder’s card;

- compare the types of borrowed funds received by the company from the founder and the funds returned by it under the loan agreement.

If you received a batch of building materials under a loan agreement, then there can be no question of any return to the loan card in cash. Borrowing relationships presuppose a single rule: “what you borrow, return it” (Clause 1, Article 807 of the Civil Code of the Russian Federation).

Thus, having ensured against mistakes at the stage of agreeing on the terms of the loan agreement and having made sure that the loan can be repaid in money to the card of the founder-lender, you can proceed directly to the procedure for returning the borrowed funds (see below).

Situations of issuing (returning) a loan in which a cash register is not needed

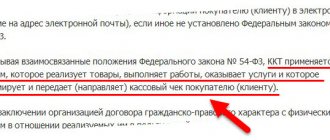

The employer issued a loan to his employee for personal expenses, and not for the purchase of various goods from the same employer. In this case, the online cash register is not involved in the calculations. The basis is Article 1.1 of Law No. 54-FZ, which clearly indicates the narrow purpose of the loan. In this situation, there is no purchase from the lender using the borrowed funds issued by him.

In the event that a loan is issued to an employee or another person for the purpose of purchasing goods, work, or services from another enterprise, cash register equipment is also not used. Reason - Law No. 54-FZ talks about settlements with the creditor company for goods (work, services) sold by it (letter of the Ministry of Finance of Russia No. 03-01-15/71861 dated 10/05/2018).

When an organization issues a loan to its founder or director, its own employee or a third-party individual, but there is no reference anywhere to the purpose of these funds, then an online cash register is also not required. The reason is the lack of a purpose for borrowing. Article 1.1 of Law No. 54-FZ clearly states “for payment for goods, work, services.” Therefore, if it is not clear from the agreement where the borrowed funds are directed, the cashier’s check when issuing and returning such a loan is not punched. Reason: in the understanding of Law No. 54-FZ, no “calculation” arises with such an operation.

As for closing loans, if they were not used to pay for the benefits sold by the lender, then the online cash register is not used at the time of repayment of the loan debt.

[adsp-pro-6]

A special place in settlement transactions is given to a loan received by an enterprise from its founder. Even if these funds are provided by the organization for the purchase of goods, works, services, an online cash register is not needed either at the time of receiving such a loan or when repaying it to the founder. The reason is that Law No. 54-FZ itself does not classify this operation as “settlements”.

CCT does not apply even when a loan is issued in a non-cash format and without presentation of an ESP by an enterprise of another organization or an entrepreneur for the purpose of purchasing goods, works, services from the lender (clause 9 of Article 2 of Law No. 54-FZ). The same applies to non-cash return of these funds.

A loan comes in more than just a monetary form. This could be, for example, a deferment or installment payment. Therefore, all of the above applies to any loan options.

Returning an interest-free loan to the founder: which method to choose?

A company can only have 2 legal “cash pockets”, from which it can transfer to the founder the funds borrowed from him:

- from a current account;

- from the cash register.

To transfer to the founder's card from a current account you will need:

- a description in the loan agreement (or in an additional agreement to it) of a similar method of debt repayment;

- indicating in it detailed bank details for transferring money to the card.

Note! When repaying a loan to the founder - an individual, there is no need to run a cash register check with the “expense” sign.

If a company does not have money in its current account, but it does have it in the cash register, it is important to consider the following:

- you cannot issue money from the cash register to repay a loan from proceeds (clause 4 of the Bank of Russia Instruction on the procedure for conducting cash transactions No. 3210-U dated March 11, 2014, Decision of the Moscow City Court dated December 14, 2012 in case No. 7-2207/2012);

- funds from the cash desk are deposited into the current account, and then a transfer is made to the founder on the card with a note in the purpose of payment “Return of funds under the loan agreement dated __ No. __”).

Do not neglect cash restrictions, otherwise you may suffer financially - according to Art. 15.1 of the Code of Administrative Offenses of the Russian Federation, the fine for this type of cash violations is up to 50,000 rubles.

What “cash” requirements are dangerous to ignore are stated in the material “Procedure for conducting cash transactions.”

Accounting entries

From an accounting point of view, the founder’s money transferred to the organization free of charge is considered “other income” (in accordance with paragraph 10, clause 7 of PBU 9/99). They must be recognized on the date they are received into the account; this determines how they are reflected in accounting.

- Money for any purpose can be credited throughout the entire reporting period. The posting should be formulated as follows: debit 51(51), credit 91-1, “Free receipt of funds from an LLC participant (shareholder, founder).”

NOTE! Account 98-2 “Gratuitous receipts of funds” is not suitable here; it is intended to register the transfer of tangible assets, not cash.

EXAMPLE. The founder of Cantata LLC, L.V. Kontrabasov, owns 50% of the company’s authorized capital. In February 2017, he transferred financial assistance to the company to replenish working capital, which amounted to 300,000 rubles. The Cantata account was replenished on February 16, 2021. The accounting records as of this date should contain the following entry: “Debit 50(51), credit 91-1 – 300,000 rubles. – financial assistance was received from the founder L. Kontrabasov.” However, this assistance will not be subject to income tax.

- Funds intended to cover the loss must be deposited exclusively at the end of the accounting year (meaning the loss shown on account 84 “Retained earnings, uncovered loss”), but even before the annual accounting report is generated. 91 debit is not suitable for this. You should use account 75 “Settlements with shareholders”; it is possible to open a sub-account “Funds intended to repay losses”. The wiring will look like this:

- on the date of registration of the minutes of the meeting of participants (or the decision of the sole founder), it is necessary to enter debit 75, subaccount “Funds of the founders aimed at covering the loss”, credit 84 - a decision was made to pay off the loss at the expense of the shareholder (founder);

- on the date of receipt of funds to the account, debit 50 (51), credit 75, subaccount “Funds of the founders aimed at covering losses” is entered - finances were received from the founder to cover losses at the end of the reporting year.

- debit 75, subaccount “R. Proskurov’s funds aimed at covering the loss”, credit 84 – 300,000 rubles. – a decision was made to cover part of the loss by R. Proskurov;

- debit 75, subaccount “N. Probirchenko’s funds aimed at covering the loss”, credit 84 - 300,000 rubles. – a decision was made to cover part of N. Probirchenko’s loss;

- debit 75, subaccount “L. Samoilova’s funds aimed at covering the loss”, credit 84 - 300,000 rubles. – a decision was made to cover part of L. Samoilova’s loss.

EXAMPLE. CJSC Stalprokat applies a general taxation system. According to the financial results of 2021, it shows a loss in the amount of 600,000 rubles. The founders of CJSC Stalprokat are R. I. Proskurov (share in the authorized capital 51%), N. S. Probirchenko (share in the authorized capital 28%) and L. D. Samoilova (share 21%). In February 2021, on the 21st, before the annual reporting for 2021 was generated, the founders decided to cover the loss by donating funds. On February 25, 2021, funds from the founders were deposited into the account of CJSC Stalprokat in the following proportions: R. I. Proskurov contributed 300,000 rubles, and N. S. Probirchenko and L. D. Samoilova - 150,000 rubles each. For February 21, the accounting records:

Read more: How to write a note to a teacher from parents, sample

Notes for February 25:

- debit 51, credit 75 subaccount “Funds of R. Proskurov aimed at repaying the loss” - 300,000 rubles. – funds were received from R. Proskurov to cover the loss;

- debit 51, credit 75 subaccount “N. Probirchenko’s funds aimed at repaying the loss” - 300,000 rubles. – funds were received from N. Probirchenko to cover the loss;

- debit 51, credit 75 subaccount “Funds from L. Samoilova aimed at repaying the loss” - 300,000 rubles. – funds were received from L. Samoilova to cover the loss.

The CJSC did not receive any income from the funds used to repay the loss. The income subject to taxation will include funds received from N. Probirchenko and L. Samoilova, since their share is less than half of the authorized capital. The result was the emergence of a permanent tax liability, which is reflected in accounting as follows: debit 99, subaccount “Permanent tax liabilities”, credit 68, subaccount “Income tax liabilities”. This entry reflects a permanent tax liability on the amount paid to N. Probirchenko and L. Samoilova.

When calculating income tax in February, the Hermes accountant did not include funds received from the founder as income. When calculating income tax in March, the cost of materials written off for production was taken into account as expenses. When and how financial assistance should be included in income when calculating income tax When none of the conditions for exemption from taxation of financial assistance received is met, take it into account as part of non-operating income (clause 8 of Article 250 of the Tax Code of the Russian Federation). Recognize income:

- on the day the money is received in the current account or at the cash desk;

- on the date of receipt of the property (for example, execution of the transfer and acceptance certificate).

These rules apply both to the accrual method and to the cash method (subclauses 1 and 2, clause 4, article 271, clause 2, article 273 of the Tax Code of the Russian Federation).

Loan repayment procedure: what other conditions should be taken into account and on which accounts should be reflected?

When repaying a debt to the founder under a loan agreement and transferring money to his card, do not forget about the need:

- compliance with the loan repayment schedule stipulated in the loan agreement;

- full repayment of the borrowed debt no later than one month from the date specified in the agreement (if a payment schedule is not provided).

When you cannot do without schedules in your current business activities, learn from the materials posted on our website:

- “How to correctly draw up a schedule for the implementation of professional standards?”;

- “What does this mean - a rotational work schedule?”;

- .

In accounting, reflect the repayment of the loan to the founder’s card by writing:

Dt 66 (67) Kt 51 - repayment of the loan to the founder’s card under the loan agreement.

Apply:

- account 66 “Settlements for short-term loans and borrowings” - if you borrowed funds from the founder for a period of less than 12 months;

- account 67 “Settlements for long-term loans and borrowings” - if the loan agreement provides for a longer borrowing period (over a year).

The bank statement will confirm:

- the fact of repayment of debt to the founder;

- volume and details of transfers.

If you are repaying the loan in parts, apply all of the above recommendations for each part of the debt being repaid.

How to return a loan to an individual from a legal entity

The borrower and the lender decide for themselves how to repay the debt. For example, monthly, quarterly or once a year. The contract should specify how often the legal entity pays the loan amount and interest. The parties can create a payment schedule - a document that specifies dates and amounts of money to be paid on certain days.

Repayment of a loan to an individual from a legal entity can be made in cash, to a card or through a cash register. The main thing is to reflect the payments in accounting.

If an individual accepts the loan repayment in cash, he leaves a receipt. The creditor indicates in the receipt that he received the money in full, then puts a date and signature. The receipt helps the entrepreneur prove that he has paid off the debt.

It is easier for the borrower to transfer money by bank transfer. In this case, you do not need to withdraw cash and comply with the cash rule, and the transfer history will reflect that the debt has been paid.

Choose a bank

What to do if you can’t return the loan to the founder’s card?

Repayment of borrowed funds is a mandatory condition of the loan agreement. However, it may be impossible to return the debt to the founder on the card for a number of reasons, for example:

- there are no funds in the current account;

- The bank account is blocked by the tax authorities;

- in other cases (the bank’s license was revoked, etc.).

If financial difficulties are temporary and sooner or later the company will have the opportunity to transfer the debt under the loan agreement to the founder’s card:

- agree with the lender on the extension of the loan repayment period, review the payment schedule;

- formalize the revision of the terms in an additional agreement to the loan agreement, attach an adjusted payment schedule to it;

- check whether, due to the extension of terms, the loan has become a long-term loan - detailed analytics in this matter allows you to correctly fill out the explanations for the accounting statements and provide its users with complete and reliable information about the company’s borrowed obligations.

This publication will tell you in which line to reflect borrowed capital.

If the company’s financial situation does not improve in the near future and there is no possibility of repaying the debt to the founder under the loan agreement, it is necessary to consider other ways to resolve the issue with the hanging debt. Find out about one of these methods in the next section.

Return of an interest-free loan to the founder on the card

Can a founder lend to his company?

Loan agreement with the founder: how to protect yourself from mistakes?

Loan repayment: what to consider first?

Returning an interest-free loan to the founder: which method to choose?

Loan repayment procedure: what other conditions should be taken into account and on which accounts should be reflected?

What to do if you can’t return the loan to the founder’s card?

Resolving the issue with a “stuck” loan

Results

Resolving the issue with a “stuck” loan

Any loan burdens the balance sheet liability - it increases the total amount of the company's debts and affects individual financial ratios, as well as the overall financial position.

Find out what calculations the company’s debt capital indicator involves in the article “Financial leverage ratio - formula for calculation.”

This situation can be easily resolved by the lender himself - the founder of the company. He has the power to relieve his company of the debt burden by forgiving the debt under the loan agreement.

If the founder decides to forgive his company’s debt, he must:

- take into account the fulfillment of the requirements of Art. 415 of the Civil Code of the Russian Federation - the founder can forgive the company’s debt if this does not violate the rights of other persons in relation to the creditor’s property;

- formalize debt forgiveness by agreement or other document;

- reflect the forgiven debt in accounting: in accounting by including the forgiven debt in other income (Dt 66 (67) Kt 91);

- in tax accounting, take into account the amount of debt in non-operating income if the share of the founder who has forgiven his debt to the company does not reach 50% (subclause 11, clause 1, article 251 of the Tax Code of the Russian Federation); if his share is 50% or more, the income is not reflected in tax records.

The founder can forgive both part of the debt under the loan agreement and the entire amount of the interest-free loan.

Results

Borrowed funds can be returned to the founder’s card only by transfer from the company’s current account and provided that the loan was provided in money. This method of loan repayment must be specified in the contract or additional agreement to it.

Sources:

- Tax Code of the Russian Federation

- Civil Code of the Russian Federation

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Registration of free assistance

The decision to provide financial assistance free of charge requires contractual formalization.

IMPORTANT INFORMATION! The Tax Code of the Russian Federation does not impose income tax on transferred funds if the participant of the legal entity that provided assistance owns half or more of the authorized capital of the organization. In other cases, this amount will become part of non-operating income and is subject to income tax.

The necessary document is the founder's decision to provide gratuitous assistance to the company, where it is necessary to clearly indicate the purposes for which the received finances are planned to be directed.