Calculation form

The new form of tax calculation was approved by order of the Federal Tax Service of Russia dated March 2, 2021 No. ММВ-7-3/115. The procedure for filling it out is given in the same order. The order took effect on April 10, 2021 and applies to settlements that organizations file after that date. In this regard, the Federal Tax Service of Russia explained that calculations for the first quarter of 2016 (for quarterly reporting) or January–March 2021 (for monthly reporting) can be submitted on both new and old forms (letter dated April 11, 2021 No. SD-4-3/6253). In both cases, tax inspectorates must accept them. Starting with reporting for the half-year (January–April) 2021, submit calculations only using the new form.

Calculation of amounts of income paid to foreign organizations - form, deadline and procedure for submission

The obligation to provide calculations of amounts paid to non-resident companies is enshrined in clause 4 of Art. 310 of the Tax Code of the Russian Federation and arises in the reporting period in which such payment was made.

The report is submitted at the place of registration of the Russian organization before the 28th day of the month following the end of the reporting quarter. When submitting annual reports, there is a deadline of March 28. If a company pays income tax using advance payments once a month, then the deadline for submitting the report is the 28th day of the month following the reporting month. You can submit the calculation to the Federal Tax Service both in paper and electronic form.

The form and procedure for filling out the calculation are regulated by the order of the Federal Tax Service of Russia “On approval of the calculation form for income paid to foreign companies and withheld taxes and the procedure for filling it out” dated 03/02/2016 No. ММВ-7-3/115 (hereinafter referred to as the Procedure for filling out).

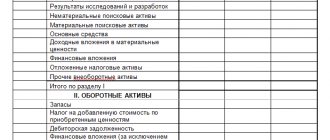

Composition of the calculation

The calculation includes:

- title page;

- section 1;

- section 2;

- section 3 (subsections 3.1, 3.2, 3.3).

Start filling out the calculation from the title page and subsections 3.1, 3.2 and 3.3 of section 3. After that, fill out section 2 and lastly, section 1. If there is no data for subsection 3.3 of section 3, do not include it in the calculation.

Number all pages in order, indicating their numbers in the boxes at the top. For example, the first page (title page) is “001”, the 12th page is “012”.

Title page

On the title page, indicate general information about the organization - tax agent.

TIN and checkpoint

At the top of the sheet, indicate the TIN and KPP of the organization. Take the TIN and KPP from the registration notice issued by the Federal Tax Service of Russia upon registration. Fill out the cells reserved for the TIN, starting from the first cell. Place dashes in the remaining free cells.

If the calculation is submitted by the largest taxpayer, indicate the checkpoint assigned by the interregional or interdistrict inspection (clause 5 of the appendix to the order of the Ministry of Finance of Russia dated July 11, 2005 No. 85n). Take it from the notice of registration as the largest taxpayer.

Correction number

How to fill out this field depends on what kind of calculation the organization submits. If this is the usual (first) calculation for the period, put “0—” in the “Adjustment number” field. It’s another matter if the organization has already submitted calculations for the past period, but wants to correct some information in it. In this case, enter the serial number of the correction (for example, “1—” if this is the first clarification, “2—” for the second clarification, etc.).

Tax (reporting) period

In the line “Tax (reporting) period (code)”, indicate the code of the period for which you are submitting the calculation. The calculation is made for the reporting (tax) period in which the tax agent actually paid income to foreign organizations (clause 1 of Article 310 of the Tax Code of the Russian Federation). Tax agents who report income taxes quarterly and monthly fill out the “Reporting (tax) period” field differently. For example:

- code 21 – for the first quarter;

- code 34 – for the year when submitted quarterly;

- code 37 – three months;

- code 46 – for a year with monthly filing.

All codes for this field are given in Appendix 1 to the Procedure, approved by Order of the Federal Tax Service of Russia dated March 2, 2021 No. ММВ-7-3/115.

In the “Reporting year” line, reflect the year for which you are submitting the calculation. Let's say you file your 2021 tax return for the first quarter of 2021. Then enter “2016” here.

Submitted to the tax authority

Submit your tax calculation to the inspectorate at the location of the organization. If the organization is classified as the largest, submit the calculation to the inspectorate at the place of registration as the largest taxpayer (clause 1 of Article 289 of the Tax Code of the Russian Federation). In the line “Submitted to the tax authority...” enter the inspection code. It is indicated in one of the documents issued by the Federal Tax Service of Russia:

- notification of registration;

- notification of registration as a major taxpayer.

In the line “at location (accounting) (code)”, enter the code depending on the capacity of the organization submitting the calculation. So, for example, provide the code:

- 214 – if this is an ordinary organization;

- 213 – if it is the largest taxpayer;

- 245 – if it is a permanent representative office of a foreign organization;

- 335 – if this is a separate division of a foreign organization in Russia.

The codes for this line are given in Appendix 1 to the Procedure approved by Order of the Federal Tax Service of Russia dated March 2, 2021 No. ММВ-7-3/115.

Name of the organization

In the line “Full name of the organization”, indicate the name of the legal entity exactly as stated in the constituent documents. If it is registered in Latin transcription, enter it. Enter capital letters of the name into the cells of the field, starting from the left edge. In the cells that are left empty, put dashes.

Reorganization or liquidation

Fill out the lines “Form of reorganization (liquidation) (code)” and “TIN/KPP of the reorganized organization” only if you are submitting a payment for the reorganized organization. In other cases, put dashes here. If the reorganized organization has not submitted calculations for the last year before the date of deregistration, it is submitted by the legal successor to its tax office.

On the cover page of the payment for the reorganized organization, indicate:

- in the field “at location (registration)” - code “215” (at the location of the legal successor who is not the largest taxpayer) or “216” (at the place of registration of the legal successor who is the largest taxpayer); 0 – upon liquidation;

- in the upper part of the title page - TIN and KPP of the successor organization;

- in the fields “Full name of the organization”, “TIN/KPP of the reorganized organization” - the name, TIN and KPP of the reorganized organization.

In the “Form of reorganization (liquidation) (code)” field, enter the code, for example:

- 0 – upon liquidation;

- 1 – during reorganization in the form of transformation;

- 2 – during reorganization in the form of a merger.

This is provided for in clause 2.5 of the Procedure approved by order of the Federal Tax Service of Russia dated March 2, 2021 No. MMV-7-3/115. Codes for forms of reorganization and liquidation are given in Appendix 1 to this Procedure.

Telephone

In the line “Contact telephone number”, indicate the mobile or landline telephone number of the accountant or tax representative, that is, the one who prepared the calculation.

Section 3

In section 3, provide the following information:

- about foreign organizations to which the tax agent paid income in the last quarter or month;

- about income paid in this period and taxes withheld;

- about persons having actual rights to these incomes.

Important: if there were no payments in the last quarter (for quarterly reporting) or in the last month (for monthly reporting), do not include section 3 in the calculation (letter of the Federal Tax Service of Russia dated April 13, 2021 No. SD-4-3/6435) .

Foreign organizations that receive income in Russia are divided into four categories. Each category is assigned its own code - a sign of the income recipient. These are the codes:

- 1 – foreign bank;

- 2 – a foreign organization whose income is taxed under Article 310.1 of the Tax Code of the Russian Federation;

- 3 – a foreign bank, whose income is taxed under Article 310.1 of the Tax Code of the Russian Federation;

- 4 – other foreign organizations.

For each foreign organization, fill out as many sections 3 as the number of characteristics of the recipient that correspond to it. Let’s assume that a foreign bank was paid both income taxed under Article 310.1 of the Tax Code of the Russian Federation and other income. In this case, fill out two sections 3 with information about this bank, income paid to it and taxes withheld.

Assign each section 3 a unique number - write it under the section name. Number all sections 3 in order. In this case, all cells must be filled in. For example, the first section 3 is “000000000001”, the twenty-fourth is “000000000024” (clause 6.1 of the Procedure approved by order of the Federal Tax Service of Russia dated March 2, 2021 No. ММВ-7-3/115).

Filling

The previously mentioned order of the Federal Tax Service dated March 2, 2016 No. ММВ-7-3/ established not only the form and electronic format of the reporting document in question, but also explanatory instructions for calculating amounts paid to foreign organizations.

The basic principle for filling out this report is on an incremental basis from the beginning of the year. Moreover, indicators in Russian currency are given in full rubles, but in foreign currency they are not rounded.

The control ratios from the Federal Tax Service letter dated June 14, 2016 No. SD-4-3/10522 will help you check the correctness of the calculation of amounts paid to foreign organizations in 2021.

In clarifications dated April 13, 2021 No. SD-4-3/6435, the Russian Tax Service notes that the tax agent does not include Section 3 in the report if in the last completed quarter or month of the reporting (tax) period he did not make payments to foreign companies. That is, only Sections 1 and 2 will be sufficient.

Read also

20.04.2018

Subsection 3.1 section 3

For each unique number of section 3, fill out a separate subsection 3.1. In it, indicate information about the foreign organization to which the tax agent paid income in the last quarter (month).

Full name, country of registration (incorporation) code, address

This is the full name of the foreign organization - the recipient of the income. If it has a name in both Latin and Russian transcription, indicate both options in subsection 3.1. If the documents contain one version of the name (either Latin or Russian), indicate only that. If there is a document confirming the permanent location (residence) of the organization in a foreign country, rewrite the name from there.

At the bottom of subsection 3.1, provide the details of this document: date, number and country code according to the OKSM classifier.

Address of the foreign organization

Take the data for this detail from the primary documents on the basis of which the income of the foreign organization was paid (for example, from an agreement or contract). The line may not be filled in if the income was paid to the bank for which the SWIFT code is indicated below.

Taxpayer code in the country of registration (incorporation)/SWIFT code

Please provide your tax code or its equivalent here. It is assigned to a foreign organization in the country of registration (incorporation). Enter it if income is paid:

- to a foreign bank whose SWIFT code is unknown;

- another foreign organization.

If you know the SWIFT code of a foreign bank, enter it in this field.

Subsection 3.2 section 3

For each unique number of section 3, fill out a separate subsection 3.2. In it, indicate information about the income paid to the foreign organization in the last quarter (month) and the taxes withheld from them.

Serial number, code and symbol of income

Assign a number in order to each income that is paid to a foreign organization. For example, the first income is “000000000001”, the twentieth “000000000020”, etc. Fill out as many sheets of subsection 3.2 as the amount of income paid by unique number.

Take the income code from Appendix 2 to the Procedure approved by Order of the Federal Tax Service of Russia dated March 2, 2021 No. ММВ-7-3/115. For example:

- 01 – dividends;

- 12 – income from the use of intellectual property rights in the Russian Federation;

- 17 – income from the sale of movable property.

Indicate the income symbol if the recipient of the income is a foreign bank. In other cases, put a dash in this field. Income symbols are given in the Rules for Accounting in Credit Institutions, approved by Bank of Russia Regulation No. 385-P dated July 16, 2012.

Amount of income before tax

In line 40, enter the income that is due to the foreign organization under the agreement - in the currency in which this income was paid. In some cases, it is not the entire amount of income that is taxed, but the difference between income and documented expenses. In particular, this rule applies to the sale of Russian real estate (subclause 6, clause 1, clause 4, article 309 of the Tax Code of the Russian Federation).

If there are documents confirming the expenses of a foreign organization, indicate in line 40 the difference between income and expenses. If there are no such documents, provide here the entire amount of income accrued under the agreement.

Currency code, date of payment of income, date of calculation (withholding) of tax

For line 050, take the currency code in which the foreign organization receives income from the All-Russian Currency Classifier.

On line 060, indicate the date when the money was debited from the bank account or issued from the cash register. If the income was paid in kind, enter here the date when the items were transferred. If the obligations are repaid by offset - the date when the agreement on it was signed. On line 080, indicate the day when the tax was calculated and withheld from the recipient’s income.

Tax rate

This line is for the tax rate at which tax is calculated on income paid to a foreign organization. Either fill in or cross out all cells in the field. For example, if the tax rate is 15 percent, enter “15.—” here, if the tax rate is 0 percent, enter “0-.—”. Profit tax rates are established by Article 284 of the Tax Code of the Russian Federation.

If preferential tax treatment is applied to the payment, please indicate here:

- reduced rate (for example, “7-.5-” – if the tax rate is 7.5%);

- “99.99” – if the income is exempt from taxation.

Apply benefits if a foreign organization has submitted documents confirming that its activities are subject to an international treaty (agreement on the avoidance of double taxation) (clause 1 of Article 312 of the Tax Code of the Russian Federation).

Place 3 dashes in lines 080–140 of subsection 3.2 of section if:

- income is exempt from taxation;

- tax rate 0 percent;

- the person has the actual right to income (in line 020 of subsection 3.3 of section 3 the code “2” or “4” is indicated). In this case, also cross out line 160.

This follows from paragraphs 2.4, 8.1 and 8.7 of the Procedure approved by Order of the Federal Tax Service of Russia dated March 2, 2021 No. ММВ-7-3/115.

Tax amount and payment deadline to the budget

On line 100, indicate the amount of tax that was withheld from the income of the foreign organization - in the currency in which it received the income. To do this, multiply the amount of income before tax (line 040) by the tax rate (line 070).

The deadline for paying tax to the budget is the deadline established by paragraphs 2 and 4 of Article 287, as well as paragraph 11 of Article 310.1 of the Tax Code of the Russian Federation.

Official ruble exchange rate on the date of tax transfer to the budget

If a foreign organization received income in rubles, put a dash here. If the money was paid in foreign currency, indicate its exchange rate established by the Bank of Russia on the date when the tax was transferred to the budget.

Amount of tax in rubles and date of transfer of tax to the budget

The tax amount in rubles (line 140) is the product of the tax amount in foreign currency (line 100) and the official exchange rate on the date of payment of the tax to the budget (line 120). It happens that the tax agent did not remit the tax in the last quarter or month, since the deadline for payment fell on the next reporting (tax) period. In this case, the procedure for filling out line 140 depends on how the income was paid - in rubles or in foreign currency.

If a foreign organization received income in rubles, put a dash in line 130, and in line 140 - the tax amount in rubles. If the income is paid in foreign currency, it is important whether the withholding agent paid the tax before filing the calculation. If at this moment the tax is transferred to the budget, fill out both line 130 and line 140. If the tax is not transferred, put dashes in lines 120–140. Do not take into account the amount of this tax in line 040 of section 2 and in line 040 of section 1 of the calculation.

When calculating for the period in which the tax payment date fell, fill out a separate section 3 for the income from which the tax was withheld. Indicate there the amount of tax in rubles, the date of its payment and the official exchange rate on this date. Include the amount of tax paid in line 040 of section 2 and line 040 of section 1.

Such rules are established by clause 8.13 of the Procedure approved by order of the Federal Tax Service of Russia dated March 2, 2021 No. ММВ-7-3/115.

Code of actual right to income

The actual right to income paid to a foreign organization may not be held by it, but by someone else. Enter here the code from Appendix 1 to the Procedure approved by Order of the Federal Tax Service of Russia dated March 2, 2021 No. ММВ-7-3/115. For example:

- 00 – if the tax agent does not know who has the actual right to the income;

- 01” – if the tax agent knows who has the actual right to the income.

Basis for reduced tax rate or tax exemption

A reduced tax rate or exemption of income from tax may be established by the Tax Code of the Russian Federation or an international treaty (agreement). Indicate in line 160 of subsection 3.2 of section 3 the desired subclause, paragraph, article of this document. Fill in the cells of the field with capital letters, and put dashes in the remaining empty cells.

Information about the issuer of issue-grade securities

Fill in this field if you paid a foreign organization income on equity securities (except for income on state or municipal securities).

Procedure for calculating and withholding tax

If you need to calculate and withhold Russian income tax on the income that you are going to pay to a foreigner, you need to correctly determine the tax base and transfer the tax to the budget in a timely manner.

Determining the tax base

In most cases, the tax base is the amount of income paid. Therefore, calculating the tax is simple: you need to multiply the amount of income by the appropriate rate (Clause 3 of Article 247, paragraph 1 of Article 274, paragraph 3 of Article 275, paragraphs 1, 4 of Article 286 of the Tax Code of the Russian Federation). But there are also transactions for which the tax base is determined as income minus expenses incurred (Clause 1 of Article 310 of the Tax Code of the Russian Federation): - sale of real estate located in the Russian Federation, or shares of Russian enterprises, the assets of which are 50% of such real estate ( Clause 4 of Article 309 of the Tax Code of the Russian Federation). Expenses for the acquisition of real estate or shares are determined in the manner prescribed by Art. Art. 268 and 280 of the Tax Code of the Russian Federation; — provision of property on lease (Subclause 7, clause 1, Article 309 of the Tax Code of the Russian Federation). The lessor's expenses take into account the cost of the leased item; — distribution by the organization in favor of a foreign participant of property, in particular, upon liquidation of the organization or withdrawal of a foreigner from the LLC. Income is taxed only in that part that exceeds the contribution made by a foreign participant to the authorized capital (Subclause 1, clause 2, Article 43, subclause 2, clause 1, Article 309 of the Tax Code of the Russian Federation; Letters of the Ministry of Finance of Russia dated November 1, 2010 N 03- 08-05, dated 03.08.2010 N 03-03-06/1/519; Letter of the Federal Tax Service of Russia for Moscow dated 30.10.2008 N 20-12/101953). Such expenses are taken into account only if by the date of payment of income you have documents confirming them (in particular, a real estate purchase and sale agreement, payment documents, etc. (Letter of the Ministry of Finance of Russia dated April 19, 2011 N 03-08-05) ). Expenses are calculated in the same currency in which income is paid (if necessary, recalculated at the official rate (cross rate) of the Central Bank of the Russian Federation on the date of their implementation) (Clause 5 of Article 309 of the Tax Code of the Russian Federation).

We withhold and pay tax

The tax to be withheld is calculated in the currency in which you will pay the income. But you need to transfer it to the budget in rubles at the exchange rate of the Central Bank of the Russian Federation on the date of transfer. Moreover, this must be done no later than the next working day after the day the income was paid to the foreigner (Clause 5, Article 45, paragraphs 2, 4, Article 287, paragraph 1, Article 310 of the Tax Code of the Russian Federation). A problem may arise if the income is paid in kind or your obligation to the foreigner is terminated in a non-monetary manner, such as by offsetting a counterclaim. The Tax Code of the Russian Federation obliges in such a situation to transfer the tax to the budget, reducing the non-monetary income of the foreign company accordingly (Clause 3 of Article 309, clause 1 of Article 310 of the Tax Code of the Russian Federation). But how to do that? After all, even if we, for example, supply a foreigner with fewer goods than we owe under a barter contract, we will not get any money from it. Theoretically, one can refer to the fact that tax is withheld only from money paid to a foreigner (Subclause 1, Clause 3, Article 24 of the Tax Code of the Russian Federation). And the Supreme Arbitration Court of the Russian Federation explained that it is possible to fine an agent for failure to transfer tax (Article 123 of the Tax Code of the Russian Federation) only if he had the opportunity to withhold the corresponding amount from the money paid to the foreigner. This means that it is enough to inform the tax authority in writing about the impossibility of withholding tax (Subparagraph 2, paragraph 3, Article 24 of the Tax Code of the Russian Federation). But these arguments may not work. Both the tax authorities and the court proceed from the fact that once an obligation has been established, it must be fulfilled. Thus, recently the court found it lawful to collect a fine under Art. 123 of the Tax Code of the Russian Federation from an organization that did not transfer tax on the income of a foreigner for the reason that the obligation to pay interest to him was converted into a bill of exchange (Resolution of the Federal Antimonopoly Service of the Eastern Military District dated August 18, 2010 in case No. A28-20189/2009). So-called tax clauses in contracts will help to avoid such problems. All you need to do is write that the contract price increases by the amount of taxes payable for a foreign organization on the territory of the Russian Federation. Then you will clearly know how much you owe to the foreigner and how much to the state.

Subsection 3.3 of section 3

The actual right to income paid to a foreign organization may not have it, but someone else: a legal entity or an individual. If there is information about this, indicate it in subsection 3.3 of section 3 of the tax calculation. For each such income, fill out a separate subsection 3.3 of section 3 of the calculation.

Serial number of income

Indicate the serial number assigned to the income on line 010 of subsection 3.2 of section 3. The amount of income is indicated in line 040 of subsection 3.2 of section 3.

Facial attribute code

Enter the code of the person entitled to actual income in this field:

- 1 – legal entity – resident of Russia, income is exempt from taxation;

- 2 – individual – resident of Russia;

- 3 – legal entity – non-resident of Russia;

- 4 – individual – non-resident of Russia;

- 5 – foreign structure without forming a legal entity.

For foreign organizations, the characteristics of a resident are given in Article 246.2, and for individuals - in Article 207 of the Tax Code of the Russian Federation. See also the recommendation How to determine status (resident or non-resident) for personal income tax purposes.

Message number and date

If a resident of Russia has the actual right to income paid to a foreign organization, send a message about this to the inspectorate at the place of registration of the tax agent (subclause 1, clause 4, article 7 of the Tax Code of the Russian Federation). The form of the message and the procedure for filling it out are given in the letter of the Federal Tax Service of Russia dated April 20, 2015 No. GD-4-3/6713. Indicate the date and number of the message on lines 030 and 040 of subsection 3.3. section 3.

If a message is submitted, lines 050–300 of this subsection need not be completed. Put dashes in them. If the message was not submitted, indicate in these lines information about the actual recipient of the income - a legal entity or an individual.

Information about the legal entity

In lines 080–140, indicate information about the organization or foreign structure without forming a legal entity that has the actual right to income. If the actual recipient of the income is a person, put dashes in these lines.

Information about an individual

In lines 150–300, enter information about the person who has the actual right to the income paid to the foreign organization. If the actual recipient of the income is a legal entity or another foreign structure without forming a legal entity, put dashes in these lines.

Section 2

In section 2, indicate the amount of tax (in rubles) that the tax agent calculated, withheld from the income of foreign organizations and transferred to the budget - for each income code. Enter here the cumulative data from the beginning of the year. Do not include in section 2 information about income paid to foreign organizations if an individual has the actual right to them (code “2” or “4” is indicated on line 020 of subsection 3.3 of section 3).

Revenue code

Fill out this line in the same way as line 020 of subsection 3.2 of section 2. Take the income code from Appendix 2 to the Procedure approved by order of the Federal Tax Service of Russia dated March 2, 2021 No. ММВ-7-3/115. For example, code “01” – dividends, etc.

Tax amount since the beginning of the tax period

This is the total amount of tax in rubles that the tax agent assessed on income paid to foreign organizations during the year. It consists of the following sums:

- tax paid on income paid in previous reporting periods (line 030);

- tax paid on income paid in the last quarter (month) of the reporting (tax) period (line 040);

- tax for which the payment deadline did not occur in the reporting (tax) period (line 050).

Amount of tax on income paid in previous reporting periods

Take this amount from line 020 of section 2 of the calculation for the previous reporting period.

Amount of tax on income paid in the last quarter (month)

This is the total amount of tax that the tax agent transferred to the budget in the last quarter or month of the reporting (tax) period. In section 2 of the calculation, it is indicated separately for each income code of a foreign organization.

Amount of tax for which payment is not due

It happens that the tax agent did not transfer tax on income paid to foreign organizations in the last quarter or month. The reason is that the payment deadline fell on the next reporting (tax) period. In this case, the order in which line 050 will be filled out will be as follows.

If a foreign organization received income in rubles, indicate the tax amount in line 050. If the income was paid in foreign currency, the rules are different. In this case, it is important whether the tax agent paid the tax before submitting the tax calculation to the inspectorate. If at this moment the tax was transferred to the budget, indicate the amount of this tax in line 050. If the tax was not transferred, put a dash in this line. Do not take into account the amount of this tax in line 040 of section 1 of the calculation.

Section 1

In section 1 of the calculation, reflect the amount of income tax due to be paid to the budget on income that was paid in the last quarter or month. Distribute these amounts according to budget classification codes. Do not include in section 1 information about paid income if an individual has the actual right to it (in line 020 of subsection 3.3 of section 3 the code “2” or “4” is indicated).

OKTMO and KBK codes

In the “OKTMO Code” field, indicate the code of the territory where the tax agent is registered. It can be determined in one of three ways. First: according to the All-Russian Classifier, approved by order of Rosstandart dated June 14, 2013 No. 159-st. Second: using the “Find out your OKTMO” service. And finally, the third way is to look at the website of the Federal Tax Service of Russia. Cross out the cells remaining empty.

On line 020, indicate the budget classification code (BCC) by which the tax agent must transfer the tax to the federal budget.

Payment deadline

The deadline for paying the income tax that the tax agent withheld from the income of a foreign organization is no later than the next working day after the payment of income (Article 246, paragraphs 2 and 4 of Article 287, paragraph 1 of Article 310, paragraph 6 of Art. 6.1 Tax Code of the Russian Federation). For each income payment and each BCC, indicate the amount of tax and the deadline for its payment in section 1 separately.

Amount of tax payable to the budget (in rubles)

Enter here the amount of tax to be paid to the budget in rubles. It happens that the tax agent did not remit the tax in the last quarter or month, since the deadline for payment fell on the next reporting (tax) period. In this case, the order in which line 040 will be filled out will be as follows.

If a foreign organization received income in rubles, still indicate the amount of tax withheld on line 040 of section 1 for the expired reporting (tax) period. If the income is paid in foreign currency, it is important whether the tax agent paid the tax before submitting the calculation to the inspectorate. If at this moment the tax is transferred to the budget, enter its amount in line 040 of section 1 for the expired reporting (tax) period. If the tax is not transferred, put dashes in line 040 of section 1 of the calculation for the expired reporting (tax) period.

What payments to foreign organizations are included in the report?

A Russian company or individual entrepreneur becomes an income tax agent in case of payments to foreign companies:

- Interest and dividends on placed funds on repurchase transactions, securities, including municipal and state securities (subclause 1, clause 4, article 282 of the Tax Code of the Russian Federation, clause 6, article 282.1 of the Tax Code of the Russian Federation, clause 5, article 286 of the Tax Code of the Russian Federation, art. 310.1 Tax Code of the Russian Federation).

- Distributed profits (dividends) from participation in domestic organizations (clauses 1, 3 of Article 275 of the Tax Code of the Russian Federation).

- Income to a non-resident without a registered representative office in Russia related to (clause 1 of Article 309 of the Tax Code of the Russian Federation): intellectual property rights;

- sale of real estate and financial instruments (including property rights in the form of shares and shares of enterprises), consisting of more than 50% of it;

- real estate rental, leasing operations;

- levying penalties in connection with violation of contractual obligations;

For an example, see here.

- sale of shares in rental-type mutual funds or real estate funds;

- other income.

Clause 2 art. 310 of the Tax Code of the Russian Federation provides for the exemption of certain categories of payments to non-residents from withholding tax. In such cases, the Russian organization does not become an intermediary in the transfer of tax amounts and does not submit the corresponding reports.

Calculation submission

Submit calculations of income paid to foreign organizations to the tax office at the location of the organization (paragraph 2, paragraph 1, article 289 of the Tax Code of the Russian Federation). The exception is organizations that belong to the category of largest taxpayers. They submit the calculation to the tax office at the place of registration as the largest taxpayer (paragraph 3, paragraph 1, article 289 of the Tax Code of the Russian Federation, letter of the Federal Tax Service of Russia dated November 9, 2010 No. ШС-37-3/15036).

The deadline for submitting the calculation is the 28th day of the month following the reporting period (clause 3 of Article 289 of the Tax Code of the Russian Federation). For example, submit your report for the first quarter no later than April 28. The final calculation drawn up at the end of the year must be submitted to the inspectorate no later than March 28 of the following year (clause 4 of Article 289 of the Tax Code of the Russian Federation).

An example of filling out a tax return on income paid to foreign organizations

On January 28, Alpha LLC paid dividends to its shareholder, Liberia Company (Netherlands), in the amount of 30,000 euros.

Paragraph 2 of Article 10 of the Agreement between Russia and the Kingdom of the Netherlands of December 16, 1996 and subparagraph 3 of paragraph 3 of Article 284 of the Tax Code of the Russian Federation provide for the same tax rates on dividends - 15 percent. Therefore, Alpha calculates the tax without a document confirming the permanent location of the company shareholder in the Netherlands.

The amount of tax that must be withheld from the income of a foreign counterparty is equal to:

30,000 EUR × 15% = 4,500 EUR.

The conditional euro exchange rate on the date of transfer of tax to the budget is 85.84 RUB / EUR.

The amount of tax payable to the budget is equal to:

4500 EUR × 85.84 RUB/EUR = 386,280 RUB.

On April 28, Alpha submitted to the inspectorate a tax calculation of the amounts of income paid to foreign organizations and taxes withheld for the first quarter.

Calculation structure and sequence of its formation

Detailed instructions regarding filling out the calculation are attached to the order for its approval. The document consists of a title page and three sections. In the latter, three more subsections must be completed.

| Sections | Content |

| Title | Information about the name of the company, all its details and signatures of the tax agent representative are recorded here. Part of the section is filled out by tax specialists. This confirms that the payment was submitted on time. |

| 1 | The amount of tax that should be sent to the treasury |

| 2 | Amount of tax on income paid |

| 3 | Information about the company that received the income, and the calculation itself |

| 3.1 | information about the foreign company |

| 3.2 | determination of tax amount |

| 3.3 | information about an individual entitled to income |

It is reasonable to form the calculation in the reverse order.

| Subsequence | Explanation |

| Work is being done on the lines of R. 3 (when the enterprise has the necessary data) | Information on the foreign counterparty (each separately) is recorded. A number is assigned that is unique. Information about a foreign company is recorded in Russian and Latin transcriptions. Number of divisions 3.1 and foreign companies are equal. Number of divisions 3.2 for each partner is equal to the amount of income previously paid. Numerical amounts reflecting the amount of income and taxes are carefully recorded |

| Formation of R. 2 and R. 1 | R. 2 must be filled out with a cumulative total. Here you should indicate the tax amount in RUB, which was determined at the enterprise, withheld from the foreign company and sent to the treasury in the context of each individual income code. R. 2 should not contain amounts paid in the form of income to a foreign company if it actually belongs to a specific person. The appendices to the procedure for filling out the document contain all possible codes |

| Title page | It can be filled out independently of other sections of the document |

Important! R. 3 is formed when money transfers were made to foreign counterparties in the last reporting period. Otherwise, the cells remain empty.

When the calculation is prepared electronically, the program will tell you whether everything was done correctly. She will not let the calculation pass until she checks its correctness.

Sample calculation of the amounts of income paid to foreign organizations

Example. On March 27, 2021, Vector LLC paid dividends to its shareholders, including the British one - 25,000 pounds. The tax rate on dividends is 15%.

- Tax withheld from the income of a foreign partner: Currency quote on the date of transfer to the treasury – 78.10 RUB/£

- Tax that needs to be sent to the budget: It was about the listed dividends that the foreigner submitted a calculation to the tax office in the prescribed form. According to the established deadlines, the document was sent on April 14 (deadline no later than April 28).

Liability for failure to provide

Situation: what are the consequences of untimely submission of tax reports on income paid to foreign organizations and taxes withheld?

The organization will be fined 200 rubles. for every document not submitted, and its officials may be held administratively liable.

A tax calculation of the amounts of income paid to foreign organizations and taxes withheld is a document required for tax control (subclause 4, clause 3, article 24 of the Tax Code of the Russian Federation). If the tax agent does not submit it within the prescribed period, the tax inspectorate has the right to present him with a fine, which is provided for in paragraph 1 of Article 126 of the Tax Code of the Russian Federation. The fine is 200 rubles. for each document not submitted.

Administrative liability is also provided for such a violation. At the request of the tax inspectorate, the court may fine officials of the organization (for example, the manager) in the amount of 300 to 500 rubles. (clause 1 of article 15.6 of the Code of Administrative Offenses of the Russian Federation).

Liability under Article 119 of the Tax Code of the Russian Federation does not apply in this situation. The tax inspectorate has the right to fine an organization under this article only if the tax return was submitted late. A tax calculation of income paid to foreign organizations is not a declaration (Clause 1, Article 80 of the Tax Code of the Russian Federation).

Situation: does the inspectorate have the right to fine a tax agent who has not submitted a calculation of income paid to foreign organizations? Income is exempt from income tax under an international agreement (treaty).

Yes, you have the right.

Based on the results of the past reporting (tax) period, the tax agent must draw up and submit to the inspectorate a calculation of the amounts of income paid to foreign organizations and taxes withheld (clause 4 of Article 310 of the Tax Code of the Russian Federation). Income tax is withheld and transferred to the budget with each payment (Clause 1, Article 310 of the Tax Code of the Russian Federation).

The exception is when an organization is exempt from the obligation to withhold tax. They are listed in paragraph 2 of Article 310 of the Tax Code of the Russian Federation. However, tax exemption does not remove the organization’s status as a tax agent. That is, in these cases, she is obliged to submit to the inspectorate the documents necessary for tax control (subclause 4, clause 3, article 24 of the Tax Code of the Russian Federation). Calculation of income paid to foreign organizations refers to such documents. Therefore, if it is not submitted, the tax inspectorate has the right to impose a fine on the organization under paragraph 1 of Article 126 of the Tax Code of the Russian Federation.

Information on the income of foreign organizations that are exempt from income tax is reflected in the calculation for the period in which the tax agent paid this income. This follows from paragraph 1 of Article 310 of the Tax Code of the Russian Federation. The document confirming the right to preferential taxation is indicated in line 160 of subsection 3.2 of section 3 of the calculation (clause 8.7 of the Procedure approved by order of the Federal Tax Service of Russia dated March 2, 2021 No. ММВ-7-3/115).

Delivery methods

Calculation of income paid to foreign organizations can be submitted to the inspection:

- on paper (for example, through an authorized representative of the organization or by mail);

- in electronic form via telecommunication channels. If the average number of employees for the previous year (in newly created or reorganized organizations for the month of creation or reorganization) exceeds 100 people, then in the current year calculations can only be made in this way. This also applies to organizations that are classified as the largest taxpayers. They must submit tax reports electronically via telecommunications channels to interregional inspectorates for the largest taxpayers.

This is stated in paragraph 3 of Article 80 of the Tax Code of the Russian Federation.

Attention: failure to comply with the established method of submitting tax reports electronically will result in tax liability. The fine is 200 rubles. for every violation. This is stated in Article 119.1 of the Tax Code of the Russian Federation.

What methods are available for making payments?

The calculation completed by the enterprise can be provided to the tax authorities in several ways to choose from:

| Calculation method | Advantages | Flaws |

| 1. In paper form: Send by mail | Lack of personal contact | The need to clarify the document in case of errors identified by tax authorities, writing explanatory notes and oral explanations to representatives of regulatory authorities |

| Submission of documents in person by an employee of the enterprise | Opportunity to clarify unclear questions with a competent specialist | |

| 2. In electronic form: Through telecommunication channels | Save time. No need for direct communication with tax specialists. The installed program checks the correctness of each section, so the possibility of errors is minimal | Not available to everyone, as the company requires: – reliable and fast Internet; – relevant software; – electronic signatures of the manager and chief accountant executed in accordance with the established procedure |

For enterprises with a workforce of more than 100 people or more, as well as for those organizations that are called “large taxpayers,” a procedure has been established for submitting calculations and other tax documents only using software.