Issues discussed in the material:

- In what cases does an individual entrepreneur overpay taxes?

- What sources can you find information about overpayment of taxes by individual entrepreneurs?

- Is it possible to reconcile with the tax office and write an application for a refund of overpaid taxes for individual entrepreneurs online?

- Is it possible to return an overpayment of taxes to an individual entrepreneur if more than 3 years have already passed?

The main task of the Federal Tax Service (FTS) is to replenish the state budget and control tax contributions. This determines the primary focus of its actions - ensuring timely and full tax payments, which is achieved through various means of influence, including financial sanctions. In practice, the opposite phenomenon is often encountered, namely, excessive payments to the state treasury. What can an individual entrepreneur do in such a situation? How to return overpayment of taxes to individual entrepreneurs? Let's find out.

Why does an individual entrepreneur overpay taxes?

Of course, no one will deliberately deduct excess tax. As a rule, the cause of this phenomenon is trivial errors, for example, in calculating the tax itself or in filling out the payment order form.

In addition, overpayment is possible for other reasons:

- The entrepreneur was not aware of the special reduced rate under the simplified tax system “Income minus expenses”, which is valid in the corresponding region, and paid tax at a rate of 15%.

- A declaration was submitted with clarifications for the previous period, due to which the payment was due in a smaller amount.

- Preferential conditions that were available for use, for example, from the beginning of this year, and were introduced by regional authorities later.

- Under the simplified tax system “Income minus expenses,” the entrepreneur transferred more funds in quarterly advance payments throughout the year than is required for the final tax amount for the annual period.

- Lack of awareness that a specific type of activity is subject to preferential taxation.

Top 3 articles that will be useful to every manager:

- How to choose a tax system to save on payments

- How to minimize taxes and not interest the tax authorities

- How to create an electronic signature quickly and easily

Accounting for a returned advance under the object “income minus expenses”

Using the “income minus expenses” object, there should not be any special problems taking into account returned advances.

So, “simplified” expenses are recognized as expenses after they are actually paid.

Payment is recognized as the termination of the obligation of the taxpayer - the purchaser of goods (work, services, property rights) to the seller, which is directly related to the delivery.

In this regard, the amounts of advances towards future deliveries of goods (works, services) are not taken into account when determining the tax base as part of expenses.

Thus, the advance payment transferred by the taxpayer cannot be recognized as an expense. Such clarifications are contained in Letters of the Ministry of Finance of Russia dated March 30, 2012 N 03-11-06/2/49, dated December 12, 2008 N 03-11-04/2/195, Federal Tax Service of Russia for Moscow dated November 10, 2005 N 18- 11/3/82713.

From this, officials conclude that the amounts of advance payments returned by suppliers of goods (works, services) are not included in income when determining the tax base for the “simplified” tax (Letter of the Ministry of Finance of Russia dated June 16, 2010 N 03-11-06/2 /93).

We recognize the advance as income

Firms using the simplified tax system use the cash method of recognizing income and expenses 1. In this case, income is recognized on the day:

- receipt of funds to bank accounts and (or) cash desk;

- receipt of property and (or) property rights to it;

- repayment of debt to the company in another way.

However, the refund of the prepayment can be within the same or different reporting (tax) periods. Let's look at examples of filling out a book of income and expenses depending on the moment of return of the prepayment.

Extract from the book of income and expenses (for example 1) Prepared using the GARANT system

Section I. Income and expenses

date and number of the primary document

Payment order dated March 1 No. 77

An advance payment was received under the contract for the provision of services dated February 28 No. 280211

Payment order dated March 11 No. 113

Refund of prepayment under the contract for the provision of services dated February 28 No. 280211

Total for the first quarter

Extract from the book of income and expenses (for example 2) Prepared using the GARANT system

I. Income and expenses

date and number of the primary document

Payment order dated May 16 No. 123

Refund of prepayment under the contract for the provision of services dated February 28 No. 280211

Total for the second quarter

Total for the half year

Companies using the simplified tax system often participate in refund transactions. You have to return advances received or act as a recipient of advances returned from suppliers. Let's consider the procedure for reflecting the return of an advance payment in accounting and tax accounting.

Situation: the company received an advance payment from the buyer, the contract was subsequently terminated and the amount received as an advance payment was returned.

In the book of accounting for income and expenses (approved by order of the Ministry of Finance of Russia dated October 22, 2012 No. 135n (hereinafter referred to as the Book)), returned advances are reflected as part of income (column 4 of section I) with a minus sign.

— 100,000 rub. - the advance has been credited to the bank account.

The entry in the Book will be as follows (see below).

Reflection of the advance received in the Income and Expense Book

— 100,000 rub. — the debt is reflected in the amount of the advance repayment.

DEBIT 76 Credit 51

— 100,000 rub. — the advance was returned to the buyer.

The entry in the Book will be as follows (see below).

Reflection of the returned advance in the Income and Expense Book

As the author believes, this point of view is not controversial. After all, tax legislation does not limit the amount of the returned advance taken into account. Some courts also consider it unlawful to conclude that it is possible to reduce the tax base by the amount of the returned advance only within the limits of income received during the specified period (Regulation of the Supreme Court of the Russian Federation of January 19, 2015 No. F02-5409/2014).

Situation: the company transferred an advance to the supplier, but later the transaction was canceled and the supplier returned the advance.

Accordingly, the amounts of advance payments returned by suppliers are not included in income (letters of the Ministry of Finance of Russia dated June 16, 2010 No. 03-11-06/2/93, dated December 12, 2008 No. 03-11-04/2/195, dated 02/08 .2007 No. 03-11-05/24) and are not reflected in the Book.

https://youtube.com/watch?v=BRgjl0KCcl4%26list%3DPL0y1go9RFkdpu7buLZG9uR8NNdOIYp5yA

How to find out about overpayment of taxes as an individual entrepreneur

There are two ways to clarify this issue: receive a notification from the Federal Tax Service or deal with it yourself (through the taxpayer’s personal account).

- Notification from the Federal Tax Service

May take the form of a telephone call. For example, at the Federal Tax Service they found an overpayment and call you on your mobile, introducing themselves something like this: “Hello, this is the tax office.” In this case, be sure to write down which branch you are calling from and what tax was paid in excess. Pay special attention to recording the phone number or address of the branch where your overpayment was detected.

If excess tax is detected, the Federal Tax Service may require documentation, such as acts, contracts, invoices and even a cash register for double-checking. There is no point in obstructing, because these measures serve your interests, and, moreover, refusal to implement them can result in a fine of about 10,000 rubles. And the sooner you provide the data and allow the tax inspectorate to clarify everything, the sooner you can return the erroneously transferred funds.

- Taxpayer personal account

You can use your personal account on the official website of the Federal Tax Service; Among other things, it helps to find out whether overpayments exist and monitor the progress of applications for their return. If you have an EDS (electronic digital signature), you will be able to transfer your reporting and contacts with the tax office into digital format, giving up paper documents and personal visits.

Just register on the Federal Tax Service website and you will be able to track the entire progress of your tax payments in your personal account.

There is another way. You can clarify the existence of an overpayment and return it through a personal visit to the tax office and the Russian Post. If it is more convenient for you to personally ask for information and have all relationships fixed on paper, you can choose this path. Just while reading the article, replace “electronic appeals” with “visiting the tax office at the place of registration” and “letter with a list of attachments” - in general, the algorithm is common.

How to return overpayment of taxes to individual entrepreneurs: step-by-step instructions

We provide step-by-step instructions to help you, which will tell you how an individual entrepreneur can return an overpayment for the simplified tax system, UTII and in other cases.

Step 1. Reconciliation with the Federal Tax Service

Determine the amount of overpaid funds. This is carried out through reconciliation of mutual settlements (and execution of the appropriate act).

The act of reconciliation with the tax service has a regulated form. To obtain such a document, the taxpayer needs to write an application and submit it to his Federal Tax Service office.

The application can be drawn up in free form; make sure that it contains the main elements:

- full designation of the Federal Tax Service body, its address;

- information about the tax payer (last name, first name and patronymic, TIN, address, contact telephone number);

- reconciliation parameters (period subject to reconciliation; type of taxation – UTII, simplified tax system, etc.);

- method of receiving the reconciliation report (by mail or in person at the tax office);

- date of writing the application.

Having submitted such an application, the entrepreneur will receive a reconciliation report within five working days. The document will be provided in 2 copies and completed by the Federal Tax Service. Enter your part of the data into it (in accordance with how payments were actually accrued and made), sign. Provide one copy to the tax office, the second remains for you.

The amount of tax overpayment can be seen in the line called “Positive Balance”.

The calculations will be reconciled, the data on them will be agreed upon, and the amount to be returned will be confirmed when the positive balance indicators from both the tax service and the entrepreneur are the same.

Returned advance exceeds income

In some cases, the amount of the returned advance payment may exceed the income received by the “simplified” person during the period of return of the advance payment. This is where the problem arises. This is especially true for “simplified” people who use the object of taxation “income”. As the Ministry of Finance of Russia explained in Letter No. 03-11-11/224 dated July 30, 2012, if there is no income during the tax period, the tax base cannot be reduced. Apparently, the logic here is that expenses are not taken into account for the simplified tax system with such a taxable object. Accordingly, a “minus” result is simply excluded.

At the same time, one can argue with the officials in this case. The fact is that by returning the advance after the fact, the taxpayer will not receive any economic benefit. Therefore, the tax paid on this amount represents an overpayment of “simplified” tax, which is subject to refund or offset against future payments.

On the other hand, given the position of the regulatory authorities, most likely you will have to defend your right to return the “surplus” in court.

How to return overpayment of taxes to an individual entrepreneur through a tax agent (in terms of personal income tax)

If a tax agent withholds excess personal income tax from your income, it is this agent who must return it himself (grounds: clause 14 of article 78, clause 1 of article 231 of the Tax Code of the Russian Federation; clause 34 of the Resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated July 30, 2013 No. 57). This refers to the return of personal income tax collected incorrectly as a result of an error. For example, the accountant withheld the appropriate percentage of earnings from income that is not subject to taxation.

What should your actions be in this case? Here's an algorithm to help.

Stage 1. Submitting an application to the tax agent.

There is no regulated form, write freely. Be sure to indicate the bank account number where your funds should be transferred. The employer, by law, has the right to return overpaid taxes only by non-cash means (Clause 1, Article 231 of the Tax Code of the Russian Federation).

Application deadlines are limited: an application can be submitted within three years from the date of transfer of the excessively collected amount to the state budget.

Please note that your ability to get your money back will not be affected by whether you are still employed by the company or have already left.

Stage 2. Receipt of erroneously withheld personal income tax (to the designated account).

The employer is obliged to return the funds no later than three months from the receipt of the application by the employer. If after the specified period the money has not been received into the account, you are additionally entitled to a certain percentage for each overdue calendar day. The size of this percentage will be determined by the current refinancing rate of the Central Bank of the Russian Federation (basis: paragraph 3, 5, paragraph 1 of Article 231 of the Tax Code of the Russian Federation).

Return from the supplier of the tax system income minus expenses

Do not include funds received from the supplier upon refusal to fulfill the contract as income, since their receipt does not lead to an increase in the economic benefits of the buyer (Clause 1, Article 39, Article 41 of the Tax Code of the Russian Federation).* At the same time, the cost of previously purchased and unsold goods , subject to refund, when calculating the single tax on the difference between income and expenses, do not take into account expenses (subclause 2, clause 2, article 346.17 of the Tax Code of the Russian Federation).

we inform you the following

: Since this return was carried out due to the fact that the supplier transferred the goods in quantities less than stipulated in the contract (clause 1 of Article 466 of the Civil Code of the Russian Federation), that is, on the basis provided by law, then received from the supplier upon refusal to fulfill the contract Do not include funds in income, since their receipt does not lead to an increase in the economic benefits of the buyer (Clause 1, Article 39, Article 41 of the Tax Code of the Russian Federation).

Nuances of refunding overpayments on taxes for individual entrepreneurs

1. First of all, find out which Federal Tax Service you need to contact.

This will depend on your place of registration, the region where you operate, and the type of taxation you prefer.

For the most part, taxes are paid at the place of registration of the individual entrepreneur, which is based on his registration. For example, a person is registered in the Tver region, which means that his registration as an individual entrepreneur will be attached to this region. At the same time, he can carry out activities in the Nizhny Novgorod region, but he will still fulfill tax obligations in Tverskaya.

Registration of an individual entrepreneur at the place of his official residence does not at all limit the field of his activities - it can be freely carried out within the entire Russian Federation. You will not need to change your place of registration for this.

An entrepreneur's tax obligations correspond to the rate of the region where he is registered. For example, an individual entrepreneur chose the simplified tax system and registered in Crimea, where he is registered. He runs his business in Moscow. The tax rate in Crimea is 3%, and in Moscow 6%. Tax payments are subject to a rate of 3%. If they are carried out at the place of business (6%), the individual entrepreneur pays them in error and in excess.

However, some entrepreneurs are entitled to tax binding to another region. When are there exceptions?

- Patent applies. In this case, the individual entrepreneur is subordinated to the tax inspectorate at the place where the patent was acquired. In addition, there cannot be an overpayment here, because tax obligations in this option are fixed and are included in the initial cost. At the same time, all other taxes continue to be paid in accordance with the region of residence of the individual entrepreneur.

- UTII is applied. Here you will need to register only with the tax office whose jurisdiction is indicated first in your application to conduct business. However, you will need to submit reports to different inspectorates - according to the regions of the country or intra-city territories that have separate tax authorities where you conduct your business.

- The simplified tax system is applied, commercial real estate has been purchased where the activity is carried out. In this situation, registration is required at the place of purchase - there you will pay taxes on the real estate itself, and others - as before, at the place of your registration.

The taxation system that applies in your case can be clarified in the taxpayer’s personal account.

Important Note:

If there was an overpayment, and you registered with several inspectorates, to get the money back, contact exactly the one where the excess payment was sent.

2. Be sure to assist the Federal Tax Service in establishing the overpayment.

Reconciliation with the budget (as well as a certificate of the status of settlements) will help with this. These measures are not mandatory, but help confirm the excess tax payment and return it sooner.

Reconciliation of your calculations with the budget is information about how much money you were supposed to transfer over a certain period and how much was actually paid. For example, in 2021, tax liabilities amounted to 25,000 rubles - and you (let’s say, by mistake) sent 250,000 rubles. All this will be reflected.

It is convenient to carry out such a verification procedure from your personal account. In the “Calculations with the budget” section, select “Submit an application to initiate the procedure...”, and then follow the algorithm that will be proposed.

3. Reconciliation will take 10-15 business days.

You can request a certificate about the status of your payments to the budget. It is not related to the reconciliation process and may well be issued in parallel. This document reflects overpayments and debts as of a specific calendar date. You can also request it from your personal account: in the “Get a certificate” section, click “Get a certificate on the status of tax payments...”, then follow the instructions.

4. Preparation of the certificate takes approximately 5 working days.

Don't agree to re-apply. It may happen that an individual entrepreneur submits an application for a refund of the overpayment, then an act of reconciliation of mutual settlements with the Federal Tax Service - and at this moment he is sent to write a new application. Refuse: according to the law, one is enough.

The timing of the decision on the refund of funds will depend on whether you submitted your application immediately with a reconciliation report or initially without it, that is, in two stages.

- If both documents are submitted at once (and also if the tax office does not find it necessary to check), the decision will be made within 10 days.

- If the tax office conducts an audit, the result will take 20–25 days.

When talking about the three-year allowable period within which an overpayment can be returned, the starting point does not mean the date of discovery of the tax surplus or submission of the application, but the date of submission of the declaration.

The result of your request, as well as the status of its consideration, can be tracked through your personal account.

Let us remind you once again: the refunded funds will arrive approximately a month after a positive decision.

If this period has expired and the money has not arrived in the current account, the Federal Tax Service will pay you interest for each overdue day. The percentage will depend on the current refinancing rate of the Central Bank (for example, 7.75% per annum).

“Limit” calculations

In the case where advances were received and returned within one reporting period, no special problems arise on the simplified tax system. It’s another matter when these operations are separated, as they say, in time. In such situations, a number of issues still arise.

First of all, let us remind you that in the case when the income of a “simplified person”, determined based on the results of the reporting (tax) period, exceeds 60 million rubles, he is considered to have lost the right to apply this special regime from the beginning of the quarter in which the specified excess was allowed (p 4 Article 346.13 Tax Code). The specified limit is subject to indexation. For the purpose of applying the simplified tax system, the deflator coefficient for 2014 is set at 1.067 (Order of the Ministry of Economic Development of Russia dated November 7, 2013 N 652). Thus, in 2014, taking into account this indicator, the indicated maximum amount of income is 64.02 million rubles.

For 2015, by Order of the Ministry of Economic Development of Russia dated October 29, 2014 N 685, for the purposes of applying the simplified tax system, the deflator coefficient was set at 1.147. Thus, in 2015, taking into account this coefficient, “simplers” are allowed to “earn” no more than 68.82 million rubles.

Be that as it may, a “failed” advance may well play a fatal role for a “simplified” seller. After all, it may well happen that during the period of its receipt, income from sales will exceed the established limit and then the right to the simplified tax system will be lost. And the fact that in the next period you will return this advance to the buyer will no longer allow you to “replay” the situation. After all, income is adjusted to the amount of the returned prepayment precisely during the period of repayment of the advance payment. The Ministry of Finance, in particular, adheres to this position. In the Letter of the Financial Department dated October 31, 2014 N 03-11-06/2/55215, officials recalled that in accordance with paragraph 1 of Art. 346.17 of the Code, “simplified” advances are included in the tax base in the period of their receipt. And when a previously received prepayment is returned, the income of the tax (reporting) period in which the refund was made is reduced by the amount being returned. The Ministry of Finance decided that the maximum amount of income would be determined in the same manner, allowing taxpayers to retain the right to use the simplified tax system.

How to return overpayment of taxes to an individual entrepreneur if it is closed

If you sent an excess payment before the termination of your activity, again try to return the funds through an application to the Federal Tax Service. The tax surplus will be transferred according to the details that you provide in this application. In this case, a debit card will also work.

In this case, the reconciliation should be ordered through the tax service using a separate document flow system.

How to return overpayment of taxes to an individual entrepreneur after closure? You can also use your taxpayer account. However, in case of termination of activity, the entrepreneur will still need to personally visit the Federal Tax Service to reconcile mutual settlements. Do not forget that the application must be filled out and printed in duplicate.

One of them is handed over personally to the authorized inspector, and the other serves to confirm the acceptance of the first - it must be returned with a special mark with the date. It is mandatory to have your passport with you. The inspection will prepare a reconciliation report within five days.

The document will be sent to you by mail, or you will be notified that it is ready for personal receipt. It happens that the tax reconciliation result is given on the day of application. If he confirms the absence of both debt and overpayment, everything is in order. If a debt is discovered, you can calmly pay it off; it will be registered with you as an individual outside of entrepreneurial activity.

If you find out that you overpaid, the news is also good: most likely, with simple steps you will return the funds back. Send the received reconciliation report to the Federal Tax Service along with a separate application for a refund of overpaid tax. Overpayment will be refunded.

An application of this type can be submitted within three years from the date of transfer of the excess payment. For example, the overpayment occurred in 2021, and the termination of activity in 2019. You can request a refund until 2021.

So, how to return the overpayment of taxes to an individual entrepreneur when he closes his activities? The application is fully prepared, duplicated, both copies are submitted to the tax office at your place of residence, one is immediately returned to you (with a stamp of acceptance and date). Refusal is not allowed.

The Tax Office will review your application within 10 days and provide a decision. If the overpayment is confirmed, it must be returned to you within one month. In practice, however, things may be different.

Delays in returning overpaid taxes for individual entrepreneurs

The tax office may not provide you with a decision on time for various reasons: the application was lost, it was not possible to consider it within the required period, there was a glitch in the program, etc. Not 10, but 15 days have passed - no response has been received? Submit another application with a request to issue you a decision from the Federal Tax Service (this is done through the same taxpayer account).

Do they unmotivatedly refuse to return your funds or leave you without an answer even after the second application? File a complaint with the Federal Tax Service, which manages all territorial divisions. Your personal account on the website will again help with this: find the “Contact the tax authority” section, where you click “Write a request” and follow the instructions.

If this measure does not bring results, you should contact the Arbitration Court. This can be done no later than three years from the date the overpayment was established.

How much can I get back?

The entire tax surplus must be returned by law. However, if you have a parallel debt, the tax office can pay it off with overpayments and, accordingly, deduct this amount from the refund.

At the same time, keep in mind that both issues can be resolved with such a convenient offset only with taxes of the same type. For example, in 2019 you overpaid income tax, but for 2021 you still owe the same - the tax office will make a offset and send a notification about this within 5 days (track it in your personal account).

The situation is completely different if the overpayment occurred for income tax, and the debt was for property tax. Here you cannot cover one with the other. The overpayment can be returned, but the debt will remain and will be supplemented by penalties. It will have to be repaid separately.

Do you want to speed up the offset or cover the debt for one tax with the excess paid from another? Write this when you apply for a refund: just add in free form that you are asking to use the overpayment to pay off debts. If the latter exceeds the overpayment, specify what debts you are asking for it to be used to repay.

Thus, the entire excess payment may be used to cover the existing tax debt, and nothing will be transferred to you. But the size of the debt will decrease.

Refund of overpaid tax

The procedure for returning an overpaid “simplified” tax is no different from the procedure for returning any other tax “overpaid” to the budget.

note

Currently there are standard samples of applications for tax credits and refunds. They were approved by order of the Federal Tax Service dated March 3, 2015 No. ММВ-7-8/ [email protected] Until this time, we would like to remind you that companies and entrepreneurs submitted applications for offset or refund of tax payments in free form.

You can return the overpayment under the simplified tax system in two cases:

- if you yourself overpaid the tax;

- if the tax authorities made additional charges to you, and you challenged them with the Federal Tax Service or in court and proved that they were illegal.

In such situations, you can only return the overpaid amounts to your current account. Overpayments are not refunded in cash.

And entrepreneurs have the right to indicate in the application for a tax refund the account of their personal bank card (determination of the Supreme Arbitration Court of the Russian Federation dated September 17, 2013 No. VAS-12390/13). In this case, three years must not pass from the date of payment of the excess amount of taxes (Clause 7, Article 78 of the Tax Code of the Russian Federation). Calculate three years from the date of filing the declaration for the year, but no later than the deadline established for its submission (Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated June 28, 2011 No. 17750/10, letter of the Ministry of Finance of Russia dated June 15, 2012 No. 03-03-06 /1/309).

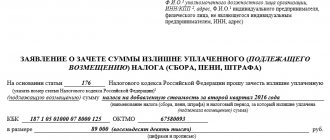

To return the overpayment, submit an application to the Federal Tax Service in the form approved in Appendix No. 8 to the order of the Federal Tax Service of Russia dated March 3, 2015 No. ММВ-7-8/ [email protected]

In the application, indicate the name of the inspection and your details: name of the company or surname, first name, patronymic of the entrepreneur.

Also fill out the basis for the return - the article of the Tax Code in accordance with which the return is made. For overpaid amounts this is Article 78 of the Tax Code, and for overcharged amounts - Article 79. And mark the type of overpayment - what amount you want to return: overpaid or overcharged.

Then indicate the tax for which the overpayment was incurred and the period to which it relates, KBK and OKTMO, as well as the amount you are asking to be returned, in full rubles, in numbers and in words.

Here is a sample application for a “simplified” tax refund:

Inspectors will return the overpayment only to the current account. Therefore, be sure to indicate in the application the details of this account to which the tax authorities must transfer money to you: name of the bank, correspondent account, BIC, INN, KPP, the account number of the company or businessman. In addition, be sure to indicate in the application who exactly is returning the overpayment - the taxpayer, the payer of the fees or the tax agent. Include the date the application is completed and the signature of the person who is returning the overpayment.

Submit the application to the Federal Tax Service on paper or electronically (clauses 4, 6 of Article 78 of the Tax Code of the Russian Federation). Within 10 days from the date of receipt of your application for a tax refund or from the date of signing the act of joint reconciliation of taxes paid, if such a joint reconciliation was carried out, the tax office must make a decision on the return of overpaid or collected tax (clause 8 of article 78 of the Tax Code of the Russian Federation) . Within five working days from the date of the decision, tax authorities are required to inform you about the decision made (clause 9 of Article 78 of the Tax Code of the Russian Federation).

The inspection will return the overpayment within a month after it receives your application (Clause 6, Article 78 of the Tax Code of the Russian Federation). But if you have tax arrears identified during the tax reconciliation, those will be paid first. And the controllers will return the remaining funds to you. If the tax inspectors violate the one-month deadline, then you will be entitled to interest for the delayed return. They are accrued for each calendar day of delay based on the refinancing rate of the Bank of Russia (Clause 10, Article 78 of the Tax Code of the Russian Federation).

How to return an overpayment of “simplified” tax to your current account, read in the berator “STS in practice”

How to return overpayment of taxes to individual entrepreneurs if more than 3 years have passed

Option 1. Go to court

If the excess payment is determined after the 3-year refund period has already expired, try the following to resolve the problem:

Step 1: Prepare evidence of when the overpayment was discovered (specific date).

Step 2. Submit a motivated application to the tax office to return or offset the overpaid funds.

Step 3. File a claim with the court within three months. This period is counted:

- or from the moment when they received a refusal from the Federal Tax Service to return or offset the funds;

- or from the moment when 10 days have elapsed from your submission of the application, and no official response has been received.

If you want to get back money you overpaid due to an incorrect withholding by the IRS rather than your own error, the process is the same.

Option 2. Write off the debt amount

If the court legally refused to return the overdue tax surplus due to the expiration of the statute of limitations (or the entrepreneur simply decided not to initiate legal proceedings), the existing overpayment can be used to pay off the current income tax. An individual entrepreneur’s application is not necessary for this.

The Federal Tax Service does not have the right to write off an outdated overpayment, at least for those taxpayers who did not request this, but continue to conduct their business and submit reports on it on time (grounds: Letter of the Federal Tax Service of Russia dated November 1, 2013 No. ND-4-8/ [ email protected] ).

Possible consequences for unrefunded overpayment of taxes for individual entrepreneurs

What happens if you do not file the excess tax refund? No penalties will be charged and no penalties will follow.

Most likely, your inspectorate will take this excess into account in a future period of the same tax. For example, in 2021 you overpaid transport tax; You did not submit an application to return it. In this case, the Federal Tax Service will simply reduce your transport tax for 2021 by this amount.

If you stopped using corporate transport and, accordingly, paying tax on it, and did not return the overpayment, the tax office will not take any action against it in the new period. Here you have three years from the date of payment of the excess to return it or take it into account in another form of tax. If you don't do this, the money will simply disappear.

Is that exactly what happened? Then it is better to write off the outdated overpayment under the guise of a “bad debt.” This is the name of the amount that cannot be returned for objective reasons, such as the bankruptcy of the debtor company or the expiration of the permissible statute of limitations.

In accounting, a written-off debt is treated as an expense that is covered by income, resulting in the convergence of debits and credits. As a result, the amount of income subject to taxes decreases. The Federal Tax Service perceives debt write-off as a reduction in tax payments, so it carefully checks (sometimes more than once) cases of loss write-off.

The order of the Ministry of Finance on accounting allows you to write off a non-refundable overpayment as a bad debt, but in a real situation of this kind you may be refused. Here the actions will depend on the amount in question and whether it would be beneficial for you to have it written off. If the answer is yes, enlist the help of qualified lawyers and accountants who will bring this issue to a victorious conclusion.

Example 1. Advance and return within one reporting month

On February 25, 2014, in our case, the Contractor, entered into an agreement with the organization “Curtains and Draperies,” that is, the Customer, for the sale of certain goods, subject to the payment of a 100% deposit.

On March 23, Curtains and Draperies transferred the required advance payment in the amount of 70 thousand rubles. As expected, it was taken into account in the tax base as income for the first quarter. But on March 29, they were forced to return this deposit, since, by mutual agreement of the parties, the contract was terminated.

Now the accountant must reflect this fact in the book of income and expenses. In section 1 of the book, in column 4, he must enter the amount of the returned prepayment with a minus value.

Since this entire operation occurred in one quarter, that is, in one tax period, it does not affect the size of the advance payment in any way. And if so, then there is no need to pay tax to the state treasury on this prepayment.

How to return an overpayment of taxes to an individual entrepreneur if the tax office refuses to issue a refund

If the inspection delays its response, which is why you cannot return the funds, do not waste time - act.

First, check what payment details you provided on your application. You still have one copy, you can easily check this information for errors. If they simply did not accept your application during a personal visit, this is illegal action. Send it to the tax office anyway, for which you have two ways: a registered letter (with notification of delivery to the sender) and an online application (available only with a qualified digital signature).

If you are not given a decision, in a dialogue with a representative of the Federal Tax Service, mention the period indicated in the Tax Code of the Russian Federation within which the overpayment is supposed to be returned - 1 month from the date of receipt of the application. This period has expired and the situation has not changed? Write complaints to a higher authority. Please submit this only by letter (with acknowledgment of delivery).

The Federal Tax Service should answer you in the same way, in writing. It will not be possible to return the funds more quickly by calling by phone: these dialogues will not be recorded, you may be given false information, and you will not be able to attach the result of such an appeal to court proceedings.

All the deadlines have passed, but you don’t have a definite answer, and you also couldn’t get your money back? You will have to draw up a statement of claim and send it to the court. This document includes a requirement to pay the tax surplus with interest for late payments.

Note that such lawsuits are usually won by taxpayers. As a rule, the court takes the side of the Federal Tax Service only in cases of incorrectly completed documents that were submitted for the return of overpayments.

Refunds are not included in expenses

Things defined by generic characteristics include money and other replaceable things that have the same characteristics and are determined by number, weight, measure (for example, a ton of sand or 100 linear meters of cable). The loan agreement is considered concluded from the moment the items are transferred. A loan agreement for an amount up to 1000 rubles (not inclusive), which is concluded between individuals, incl.

In this case, the return of money must be confirmed by primary documents that make it possible to determine the fact, basis and amount of the amount 9. Free legal consultation: You must have the following documents: