When an organization owns and manages one or more company vehicles on its balance sheet, it is constantly faced with the task of purchasing fuel, justifying its use, and writing it off as expenses.

Current tax rules allow you to reduce the income tax base due to this write-off, but only if they are correctly justified in the relevant reporting documentation.

Therefore, it is extremely important to correctly keep records of spent fuels and lubricants and comply with the write-off standards established by the Ministry of Transport of the Russian Federation.

Let's consider what standards for fuels and lubricants are relevant today, how they depend on the season, as well as the nuances that may arise when justifying their write-off in ambiguous cases. We will show with an example how to correctly calculate the standard calculation of write-off of fuel and lubricants.

How to recognize expenses for fuel and lubricants for tax purposes ?

The concept of fuel and lubricants standards

Fuel consumption on company vehicles cannot occur uncontrollably and irregularly, otherwise overexpenditures and possibly even waste cannot be avoided. To control and account for the amount of fuel and lubricants, the concept of fuel consumption rate - an economically sound indicator that reflects the average need for fuel (gasoline, gas, diesel fuel) for various types of service vehicles for a certain mileage.

The generally accepted and most convenient method is to calculate fuel consumption per 100 km.

Regulatory regulation

The document that sets fuel consumption standards is order No. AM-23-r dated March 14, 2008. The recommended fuel consumption standards for 2021 are approved by the Ministry of Transport of the Russian Federation; the latest edition of the methodological recommendations was published in September 2018. Changes were made by order of the Ministry of Transport of the Russian Federation dated September 20, 2018 No. IA-159-r.

The Ministry of Transport recommends calculating the volume of gasoline consumed as follows:

- fuel consumption.

— base fuel consumption rate (set in l/100 km).

S — vehicle mileage.

D is the correction factor.

The order establishes basic indicators for most car models. The table of fuel consumption standards for car brands is differentiated by type of vehicle (passenger cars, trucks, etc.) and contains thousands of items. Its beginning looks like this.

The correction factor is calculated based on surcharges to the base tariff established in connection with operating conditions.

Who sets the standards for fuels and lubricants?

The Ministry of Transport of the Russian Federation gives recommendations on fuel rationing. However, they have remained unchanged since 2015 (the latest order of the Ministry of Transport of the Russian Federation regarding fuel standards No. AM-23-r is dated July 14, 2015), which does not fully reflect the current situation today.

The Ministry of Finance of the Russian Federation made an official clarification on this matter: Letter No. 03-03-06/1/48789 dated August 19, 2021 states that following the standards established by the Ministry of Transport is a right, not an obligation, of an entrepreneur. Tax authorities do not have the right to insist on compliance with these particular indicators when writing off fuel and lubricants.

the write-off of fuel and lubricants in excess of established standards in the accounting records of an organization ?

Fuel consumption and write-off standards in force for each specific company must be adopted, approved and recorded in internal documentation.

NOTE! For motor transport companies, unlike other legal entities and entrepreneurs, accounting for fuel costs according to the recommendations of the Ministry of Transport is mandatory.

Winter fuel consumption standards in 2018-2019

In 2021 - 2021, the organization has the right to apply fuel and lubricants write-off standards that are approved by the Ministry of Transport, but this is not mandatory. At the same time, it is safer to revise the standards if they differ significantly from the approved ones (Order of the Ministry of Transport of Russia dated March 14, 2008 No. AM-23-r).

To justify the write-off of fuel and lubricants, approve fuel consumption standards. Basic consumption rates and increasing factors are recommended in the Methodological Recommendations, which were approved by Order of the Ministry of Transport dated March 14, 2008 No. AM-23r. Also take into account climatic conditions, road quality, technical condition of the car, whether it has air conditioning or climate control.

From what date should we switch to winter fuel consumption standards in 2018-2019? This issue is regulated by an organization order. For example, you can switch to winter standards from November 1, 2019.

Here is a table with basic values of winter costs by region of Russia

| Item no. | Subject of the Russian Federation or part thereof | Number of months and validity period of winter allowances | Maximum amount of winter allowances no more than, % |

| The names of the subjects of the Russian Federation are given in accordance with the Constitution (Basic Law) of the Russian Federation - Russia as amended for 2021. | |||

| 1 | 2 | 3 | 4 |

| 1 | Moscow | 5.0 01.XI..31.III | 10 |

| 2 | Belgorod region | 4.0 15.XI..15.III | 7 |

| 3 | Bryansk region | 5.0 01.XI..31.III | 10 |

| 4 | Vladimir region | 5.0 01.XI..31.III | 10 |

| 5 | Voronezh region | 5.0 01.XI..31.III | 10 |

| 6 | Ivanovo region | 5.0 01.XI…31.III | 10 |

| 7 | Kaluga region | 5.0 01.XI…31.III | 10 |

| 8 | Kostroma region | 5.0 01.XI…31.III | 10 |

| 9 | Kursk region | 5.0 01.XI…31.III | 10 |

| 10 | Lipetsk region | 5.0 01.XI…31.III | 10 |

| 11 | Moscow region | 5.0 01.XI…31.III | 10 |

| 12 | Oryol Region | 5.0 01.XI…31.III | 10 |

| 13 | Ryazan Oblast | 5.0 01.XI…31.III | 10 |

| 14 | Smolensk region | 5.0 01.XI…31.III | 10 |

| 15 | Tambov Region | 5.0 01.XI…31.III | 10 |

| 16 | Tver region | 5.0 01.XI…31.III | 10 |

| 17 | Tula region | 5.0 01.XI…31.III | 10 |

| 18 | Yaroslavl region | 5.0 01.XI…31.III | 10 |

| 19 | Saint Petersburg | 5.0 01.XI..31.III | 10 |

| 20 | Republic of Karelia | 5.5 01.XI…15.IV | 12 |

| 21 | Komi Republic (except for the urban district of Vorkuta and the urban district of Inta) | 6.0 01.XI…30.IV | 15 |

| 21.1 | Vorkuta urban district and Inta urban district of the Komi Republic | 6.5 15.X…30.IV | 15 |

| 22 | Arkhangelsk region (except for the Nenets Autonomous Okrug) | 6.0 01.XI…30.IV | 15 |

| 23 | Nenets Autonomous Okrug | 6.0 15.X…15.IV | 18 |

| 24 | Vologda Region | 5.0 01.XI…31.III | 10 |

| 25 | Kaliningrad region | 4.0 15.XI..15.III | 7 |

| 26 | Leningrad region | 5.0 01.XI…31.III | 10 |

| 27 | Murmansk region | 6.0 01.XI…30.IV | 15 |

| 28 | Novgorod region | 5.0 01.XI…31.III | 10 |

| 29 | Pskov region | 5.0 01.XI…31.III | 10 |

| 30 | The Republic of Dagestan | 3.0 01.XII…1.III | 5 |

| 31 | The Republic of Ingushetia | 3.0 01.XII…1.III | 5 |

| 32 | Chechen Republic | 3.0 01.XII…1.III | 5 |

| 33 | Kabardino-Balkarian Republic | 3.0 01.XII…1.III | 5 |

| 34 | Karachay-Cherkess Republic | 3.0 01.XII…1.III | 5 |

| 35 | Republic of North Ossetia–Alania | 3.0 01.XII…1.III | 5 |

| 36 | Stavropol region | 3.5 01.XII..15.III | 5 |

| 37 | Republic of Bashkortostan | 5.5 01.XI…15.IV | 12 |

| 38 | Mari El Republic | 5.0 01.XI..31.III | 10 |

| 39 | The Republic of Mordovia | 5.0 01.XI..31.III | 10 |

| 40 | Republic of Tatarstan | 5.0 01.XI…31.III | 10 |

| 41 | Udmurt republic | 5.0 01.XI…31.III | 10 |

| 42 | Chuvash Republic | 5.0 01.XI…31.III | 10 |

| 43 | Kirov region | 5.5 15.X…31.III | 12 |

| 44 | Nizhny Novgorod Region | 5.0 01.XI…31.III | 10 |

| 45 | Orenburg region | 6.0 15.X…15.IV | 15 |

| 46 | Penza region | 5.0 01.XI…31.III | 10 |

| 47 | Perm region (except for the Komi-Permyak district) | 5.5 01.XI…15.IV | 10 |

| 47.1 | Komi-Permyak district of Perm region | 6.0 01.XI…15.IV | 18 |

| 48 | Samara Region | 5.0 01.XI…31.III | 10 |

| 49 | Saratov region | 5.0 01.XI…31.III | 10 |

| 50 | Ulyanovsk region | 5.0 01.XI…31.III | 10 |

| 51 | Kurgan region | 5.5 01.XI…15.IV | 10 |

| 52 | Sverdlovsk region | 5.5 01.XI…15.IV | 10 |

| 53 | Tyumen region (with the exception of the Khanty-Mansiysk and Yamalo-Nenets Autonomous Okrugs) | 5.5 01.XI…15.IV | 12 |

| 54 | Khanty-Mansiysk Autonomous Okrug, Tyumen Region | 6.5 15.X…30.IV | 18 |

| 55 | Yamalo-Nenets Autonomous Okrug, Tyumen Region | 6.5 15.X…30.IV | 18 |

| 56 | Chelyabinsk region | 5.5 01.XI…15.IV | 10 |

| 57 | Altai Republic | 5.5 01.XI…15.IV | 15 |

| 58 | The Republic of Buryatia | 6.0 01.XI…30.IV | 18 |

| 59 | Tyva Republic | 6.0 01.XI…30.IV | 18 |

| 60 | The Republic of Khakassia | 6.0 01.XI…30.IV | 18 |

| 61 | Altai region | 5.5 01.XI…15.IV | 15 |

| 62 | Krasnoyarsk Territory (with the exception of Taimyr Dolgano-Nenets, Evenki, Turukhansk, North Yenisei districts) | 5.5 01.XI…15.IV | 15 |

| 62.1 | Taimyrsky Dolgano-Nenetsky district of the Krasnoyarsk Territory | 7.0 15.X…15.V | 18 |

| 62.2 | Evenki district of Krasnoyarsk region | 7.0 15.X…15.V | 18 |

| 62.3 | Turukhansky district of Krasnoyarsk Territory | 7.0 15.X…15.V | 18 |

| 62.4 | Severo-Yeniseisky district of the Krasnoyarsk Territory | 7.0 15.X…15.V | 18 |

| 63 | Irkutsk region | 6.0 01.XI…30.IV | 18 |

| 64 | Kemerovo region | 6.0 01.XI…30.IV | 15 |

| 65 | Novosibirsk region | 5.5 01.XI… 15.IV | 12 |

| 66 | Omsk region | 5.5 01.XI… 15.IV | 12 |

| 67 | Tomsk region | 5.5 01.XI… 15.IV | 12 |

| 68 | Transbaikal region | 6.0 01.XI…30.IV | 18 |

| 69 | The Republic of Sakha (Yakutia) | 7.0 15.X…15.V | 20 |

| 70 | Primorsky Krai | 5.5 01.XI…15.IV | 12 |

| 71 | Khabarovsk Territory (except Okhotsk region) | 5.5 01.XI…15.IV | 12 |

| 71.1 | Okhotsk district of Khabarovsk Territory | 6.5 15.X…30.IV | 18 |

| 72 | Amur region | 6.0 01.XI…30.IV | 15 |

| 73 | Kamchatka Krai | 6.0 01.XI…30.IV | 15 |

| 74 | Magadan Region | 6.5 15.X…30.IV | 18 |

| 75 | Sakhalin region (with the exception of Kuril, Nogliki, Okha, North Kuril, South Kuril regions) | 5.0 15.XI…15.IV | 12 |

| 75.1 | Kurilsky district of the Sakhalin region | 6.0 01.XI…30.IV | 15 |

| 75.2 | Nogliki district of Sakhalin region | 6.0 01.XI…30.IV | 15 |

| 75.3 | Okhinsky district of the Sakhalin region | 6.0 01.XI…30.IV | 15 |

| 75.4 | Severo-Kurilsky district of the Sakhalin region | 6.0 01.XI…30.IV | 15 |

| 75.5 | Yuzhno-Kurilsky district of the Sakhalin region | 6.0 01.XI…30.IV | 15 |

| 76 | Jewish Autonomous Region | 5.5 01.XI…15.IV | 12 |

| 77 | Chukotka Autonomous Okrug | 6.5 15.X…30.IV | 20 |

| 78 | Islands of the Arctic Ocean and seas of the Far North | 7.0 01.XI…31.V | 20 |

| 79 | Republic of Adygea | 3.0 01.XII…1.III | 5 |

| 80 | Republic of Kalmykia | 5.0 15.X…15.III | 10 |

| 81 | Krasnodar region | 3.0 01.XII…1.III | 5 |

| 82 | Astrakhan region | 5.0 15.X…15.III | 10 |

| 83 | Volgograd region | 5.0 15.X…15.III | 10 |

| 84 | Rostov region | 4.0 15.XI..15.III | 7 |

| 85 | Republic of Crimea | 4.0 01.XI..01.III | 5 |

| 86 | City of Sevastopol | 4.0 01.XI..01.III | 5 |

Accounting for fuel and lubricants standards

IMPORTANT! A sample of filling out a fuel write-off report from ConsultantPlus is available here

When drawing up a balance sheet, the accountant enters the fuel consumption indicator for write-off:

- in the column “Material expenses”, if the quantity fits into the standards established by the enterprise;

- partially - in the column “Non-operating expenses”, if the spent fuel and lubricants exceed the limits (the amount that exceeds the norm is entered in this column).

For this purpose, account 10 “Fixed assets” with the corresponding subaccounts is used.

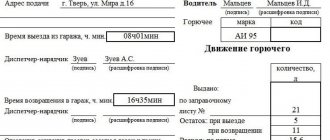

The supporting document on the basis of which the calculation of actually consumed fuel is made is a waybill , the form of which the enterprise is allowed to develop independently, as well as coupons, checks, certificates, etc., confirming the purchase of fuel at a certain price.

How to record the write-off of fuel (fuel) purchased in cash ?

List of cars

The order of the Ministry of Transport of the Russian Federation for reporting created a list of cars, which included:

- "cars";

- cars with vans;

- vehicles owned by the Ministry of Health;

- the country's bus fleet;

- trucks;

- special equipment;

- tow trucks and so on.

As for passenger vehicles, which are considered to be the leaders in the number of units in Russia, the fuel consumption rate is calculated by the formula:

- Qн = 0.01 x Hs x S x (1 + 0.01 x D).

Consumption is indicated by the symbols Qн in liters. The established rate of fuel consumption per 100 kilometers is designated Hs. Vehicle mileage is indicated by the symbol S. The coefficient D is used to correct the total, displayed as a percentage of the standards.

It should be noted that, according to the directive document of the Ministry of Transport, this formula is recognized as meeting the needs of automobile fuel accounting for statistical records.

What determines the value of the fuel and lubricants indicator?

Recommended by the Ministry of Transport of the Russian Federation or independently developed by the enterprise, fuel write-off standards depend on objective factors:

- type of transport (passenger car, truck, truck, special purpose vehicle, etc.);

- specific car brand;

- its mileage;

- the period during which the car is in operation;

- basic fuel consumption;

- some established coefficients - seasonal, territorial, road, load-lifting, etc.

General provisions

- Methodological recommendations “Consumption standards for fuels and lubricants in motor transport” (hereinafter referred to as fuel consumption standards) are intended for motor transport enterprises, organizations involved in the management and control system, entrepreneurs, etc., regardless of the form of ownership, operating automotive equipment and special mobile vehicles. composition on car chassis on the territory of the Russian Federation.

- These recommendations provide the values of basic, transport and operational (including surcharges) fuel consumption standards for general purpose automotive rolling stock. Also, fuel consumption standards for the operation of special vehicles, the procedure for applying standards, formulas and methods for calculating standard fuel consumption during operation, reference standard data on the consumption of lubricants and special liquids, the values of winter allowances, etc.

- The consumption rate of fuel and lubricants in relation to motor vehicles implies an established value for the measure of its consumption during operation of a vehicle of a specific model, brand or modification.

The consumption standards for fuels and lubricants in road transport are intended for calculating the standard value of fuel consumption at the point of consumption, for maintaining statistical and operational reporting, determining the cost of transportation and other types of transport work. And also for planning the needs of enterprises for the supply of petroleum products, for calculations of taxation of enterprises, implementation of economy and energy saving regimes for consumed petroleum products, settlements with vehicle users, drivers, etc.

When rationing fuel consumption, a distinction is made between the basic value of fuel consumption, which is determined for each model, brand or modification of a car as a generally accepted norm, and the calculated standard value of fuel consumption, which takes into account the transport work being performed and the operating conditions of the vehicle.

What does the Ministry of Transport say?

The document-order of the Ministry of Transport establishing recommended standards is methodological in nature. It provides basic indicators of gas, diesel, and gasoline consumption for specific brands of vehicles, also differentiated by class and model. Using these tables you can conveniently keep fuel records.

Below are fuel standards for the most common representatives of the company fleet. A complete list of all vehicles provided by the Russian Ministry of Transport (about 800 brands) with the corresponding standards for fuel and lubricant costs can be downloaded from the link below.

FILES

Self-calculated fuel consumption

Despite the fact that the organization has the right to use the standards of the Ministry of Transport, which sometimes turns out to be preferable, since it is recommended by tax authorities, you can make your own calculations based on the fuel and lubricants standards established by internal regulations.

A simplified version involves finding the quotient of the amount of fuel spent and the kilometers traveled (to establish a percentage, the figure is multiplied by 100). The result will be an indicator in the “usual” form, reflecting the required amount of fuel and lubricants for 100 km of travel on a given vehicle. Then, if necessary, you can apply the appropriate coefficients to it.

A more complex formula used to calculate this indicator takes into account the specific brand of car and the fuel standard established for it (from the Ministry of Transport table or internal regulations of the organization itself). The amount of cargo or passengers on board the vehicle, the driving mode, and some other errors (winter coefficient, correction for road type, etc.) are also taken into account.

Nexp. = 0.01 x Npres. x (1 + x K x 0.01)

Where:

- Nexp. – calculated fuel consumption rate for write-off (measured in liters);

- Npresupposed – the standard provided for in the documents of the organization or by the Order of the Ministry of Transport of the Russian Federation;

- S – mileage traveled by this car;

- K is the coefficient taken into account when taking into account various corrections.

Example of a specific calculation

A company car belonging to Volta LLC, a Toyota Corolla with an engine capacity of 1.6 liters, made a trip marked on the waybill with a distance of 650 km. At the same time, he spent 62 liters of gasoline. There was no cargo on board (documents were delivered). The trip was made in winter; the winter surcharge established by Volta LLC is 5%. The company uses indicators from the table of the Ministry of Transport of the Russian Federation for calculations.

Let's calculate fuel consumption for write-off. According to the Order of the Ministry of Transport, the fuel consumption rate for a car of this brand traveling without a load is 9 liters per 100 km. We take the winter coefficient as 5. This trip on a car of this brand does not provide for any other surcharges under the given conditions. Let's calculate using the formula: 0.01 x 9 x 650 (1 + 5 x 0.01) = 0.09 x 650 x 1.05 = 61.4 liters.

As you can see, the driver of a company car practically did not exceed the gasoline consumption required by the standard.

How else can the fuel consumption rate for gas be set?

The given standards of the Ministry of Transport are mandatory for use by motor transport enterprises and organizations of management and control systems, and for other business entities (companies and individual entrepreneurs) these standards are advisory in nature. This also follows from letters of the Federal Tax Service of Russia dated 06/03/2013 No. 03-03-06/1/20097 and the Ministry of Finance dated 01/30/2013 No. 03-03-06/2/12. Currently, enterprises are not required to use the standards established by the Consumption Standards of the Ministry of Transport, therefore the following options for establishing standards for the write-off of gas fuel are possible:

- use the standards specified in the technical documentation of the vehicle or gas equipment manufacturer;

- contact scientific organizations that develop individual fuel consumption standards for a specific type of transport (in the absence of standards approved by the Ministry of Transport);

- develop standards yourself using control measurements.

Consumption rates must be approved by the company’s internal administrative document.