What is cash discipline

The current regulations for conducting cash transactions by legal entities/individual entrepreneurs were approved by the Bank of Russia in Instructions No. 3210-U dated March 11, 2014. Current regulations establish the rules for working with cash, including accepting and issuing money, and calculating the cash balance limit. According to clause 4.6 of the Instructions for individual entrepreneurs, there is no need to maintain a cash book if accounting of income and expense transactions or physical indicators (objects of taxation) is organized according to the Tax Code of the Russian Federation. Due to the fact that any entrepreneur, regardless of the taxation system used, keeps tax records in one way or another, we can conclude that all individual entrepreneurs may not keep a cash book.

However, in some cases it will still be necessary to organize cash document flow. First of all, an entrepreneur can independently decide to maintain cash forms to strengthen control and increase transparency of employees’ work. Secondly, the need for filling arises when:

- Availability of accountable settlements between individual entrepreneurs and personnel.

- Issuance of PCO (cash receipt orders) as confirmation of payment for the services offered to customers.

- Cash payments to personnel for salaries.

- Cash issuance of various social benefits to employees - copies of documents for reimbursement of expenses must be submitted to the Social Insurance Fund.

Therefore, the answer to the question: Should an individual entrepreneur keep a cash book? will be negative. At the moment, entrepreneurs are given the opportunity to choose - to draw up cash documents in the general manner with the formation of a cash book and receipt and expenditure orders. Or apply simplified regulations by recording income and expenses in KUDiR or recording physical indicators. The nuances depend on the tax regime used - simplified tax system, PSN, UTII, OSNO or Unified Agricultural Tax.

Cash documents

When talking about whether an individual entrepreneur is obliged to keep a cash book, one cannot help but decide on the complete list of necessary cash documents.

The following main categories are distinguished:

- receipts;

- consumables;

- accounting registers designed to summarize information from primary documents.

The legislation has developed the following types of documents:

- cash receipt order - the purpose is to record the receipt of cash in the cash register;

- expense cash order – intended for processing cash withdrawal from the cash register;

- cash book – to display all transactions with cash registers;

- registration log of PKO and RKO - for accounting;

- book of accounting of accepted and issued funds.

The main requirement for cash documentation is the absence of various types of corrections to accounting registers, as well as erasures. The use of corrector is strictly prohibited.

Corrections can be made:

- If an error is made when registering PKO/RKO. It is allowed to cross out an erroneous form and create a new one. An erroneous and crossed out order must be submitted along with the shift report. Carrying out transactions based on orders with errors is prohibited.

- An error was made in one of the journals or cash book. Corrections are made according to the rules: an incorrect entry is crossed out, and corrections are made above it by indicating the correct value of the amounts or text. Next to the correction, where there is free space, you need to add the inscription “Corrected”, certified by the signatures of the persons responsible for the design documentation. It is important to include a transcript of the signatures and indicate the date. All instances need to be corrected.

The entrepreneur must organize, determine a place for storage, and also formulate a procedure for storing cash documentation for the entire period regulated by law.

General rules for storing documentation:

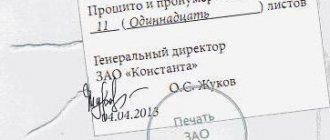

- It costs to stitch documents on a daily basis. The stitching is formed no later than the next day.

- You need to stitch in order: in ascending order of account numbers, from Dt to Kt.

- All sheets are numbered.

- Before transferring to the archive, it is necessary to create an inventory in which to indicate the quantity and names of stitches.

Requirements for storage duration are regulated by the Federal Law “On Accounting”: primary documentation, as well as registers, should be stored for 5 years. At the end of the period, they can be destroyed only if there are no disputes regarding the transactions specified in them or legal proceedings. The countdown begins from the date of the reporting year when the document was generated. The deadline is identical for electronic forms. The exception is personnel payroll records, which must be kept for 75 years.

You can store documentation either independently or with the assistance of companies specializing in this. Firms provide such services under a contract for a fee.

Is an individual entrepreneur required to keep a cash book?

We figured out that according to clause 4.6 of Instructions No. 3210-U, entrepreneurs have the right not to maintain a generally accepted cash book, and also according to clause 2 they may not calculate the cash balance limit. But despite the existing legislative norm, before completely abandoning the cash management regulations, it is necessary to assess the consequences of not accounting for cash. And this is not a matter of responsibility to state control authorities - we have already found out that individual entrepreneurs are not required to maintain cash documents.

The task of any business is to make a profit and ensure the safety of assets, including cash and non-cash funds. And in the case where an individual entrepreneur is distinguished by a large scale of activity, regular cash turnover and a large staff of hired employees, the human factor comes to the fore, which an experienced manager cannot neglect. Correctly establishing accounting for cash transactions will significantly simplify control over the state of finances and help evaluate the work of individual specialists, including responsible cashiers. It’s not for nothing that cash discipline is called that - maintaining unified forms is carried out according to clearly developed regulations and allows you to accurately calculate how much money came in, went out and for what purposes.

Individual entrepreneurs have the right not to set a cash limit (clause 2)

This means that the individual entrepreneur is not obliged to deposit funds in excess of the established limit into the current account, as was the case before. Any amount of money can be kept in the individual entrepreneur's cash register. Legal entities - small businesses - can also take advantage of this right.

However, before June 1, 2014, this limit should have been set for each individual entrepreneur and in each organization. If you choose not to set a cash balance limit, then this choice must be reflected in the Accounting Policy. And is imperative to cancel the old order establishing such a limit. If the previously effective orders are not cancelled, then individual entrepreneurs and small businesses will be forced to maintain the previous order and the previous limits.

Thank you for subscribing!

Individual entrepreneur cash book - how to fill it out

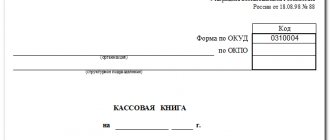

Competently filling out an individual entrepreneur's cash book does not depend on the fact of using a cash register or the use of special modes. The rules for entering data are the same for all business entities; standard forms are approved by the State Statistics Committee in Resolution No. 88 of August 18, 1998. What documents are required to be kept for the general accounting of cash?

Cash document flow includes the preparation of the following forms:

- Cash book KO-4.

- Receipt orders KO-1.

- Expense orders KO-2.

- Sheets – settlement and payment f. T-49, settlement T-51, payment T-53. They are used optionally for payroll settlements with personnel.

The listed documents form the backbone of accounting for cash transactions, and the cash book is a consolidated journal that displays the movement of cash inflows and outflows. The document is opened for the calendar year and maintained in chronological order. Format – electronic or paper. The first is printed at the end of the period, the second is issued for each cash day. The individual entrepreneur’s cashier is appointed as the responsible employee for filling out KO-4; certification of the document is entrusted to the entrepreneur. Let's talk about the rules for filling out the journal.

The procedure for creating an individual entrepreneur's cash book:

- Title page – details of the entrepreneur are given: full name, codes, reporting period.

- Internal sheets - one page is allocated for each cash day, where they indicate data on incoming transactions (by entering PKO numbers/dates) and outgoing transactions (by displaying data on cash register numbers/dates). At the end of the day, the totals for income and expenses are compiled, and the balance in the cash register is calculated. The cashier checks documentary data and actual cash.

- The last sheet is where the book is certified: the magazine is stitched, the pages are pre-numbered, and the number of pages and a signature with the date are indicated on the outside of the document. This norm, according to Instructions No. 3210-U, is no longer mandatory; the lack of firmware and certification is not considered a violation.

The cash book must be filled out without errors, corrections or omissions. If an inaccuracy has been made, the correction is made according to the correction rules - by crossing out the incorrect entry, entering the correct one, and certifying it with the signature of the individual entrepreneur. If no transactions were carried out at the entrepreneur’s cash desk during the day, make entries in f. KO-4 is not required.

Sample of a standard cash book form f. KO-4 is possible.

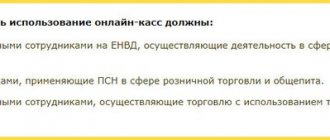

Changes in cash discipline due to the introduction of online cash registers

With the use of online cash registers, the need for some reporting forms has disappeared. The data is stored in the memory of cash register equipment and can be retrieved at any time for control. For persons using a new type of cash register, information is provided on reducing the requirements for the use of forms.

According to clarifications provided by the Ministry of Finance, the forms of primary accounting in trade, established by Resolution of the State Statistics Committee of December 25, 1998 No. 132, are not mandatory for use by enterprises that have switched to the new procedure for using cash registers. The new order refers to the use of online cash registers.

Deputy Director of the Department V.A. Prokaev (Letter of the Ministry of Finance of the Russian Federation dated September 16, 2016 No. 03-01-15 / 54413)

Important! Forms of settlements using cash registers Nos. KM 1-KM 9 approved by Resolution No. 132 may not be used in accounting for transactions.

How to maintain a cash book in 1C

Often, many entrepreneurs use the capabilities of accounting programs such as 1C to keep daily records of business operations. Such developments are aimed more at enterprises, so the movement of funds in them is displayed by entering data through incoming and outgoing orders. That is, without even resorting to special efforts, the individual entrepreneur receives ready-made cash documents, including a cash book. All that remains is to print the documents, sign and store them among other forms.

In this case, you need to pay attention to this aspect. In accordance with Instructions No. 3210-U, individual entrepreneurs may not prepare a cash book, provided they maintain tax records. But he has the right to fill out receipts and expenditure orders. This means that even if there are PKOs and RKOs, it is allowed not to maintain a cash book and limit oneself to the presence of orders in order to reflect transactions in KUDiR. This will not be considered a violation.

Conclusion - in this article we examined whether an individual entrepreneur can not keep a cash book and in what situations it is still more advisable not to deviate from the generally accepted cash accounting regulations. If an entrepreneur decides to fill out the standard KO-4 form, this must be done in compliance with the current regulations according to Directions No. 3210-U dated March 11, 2014.

Comments

Nikolai 11/17/2015 at 11:53 am # Reply

“It should be noted that starting from 2014, individual entrepreneurs who keep a book of income and expenses are exempt from the obligation to issue cash orders.” Actually, since June 1, 2014, Author has been burning: “All individual entrepreneurs are required to keep a book, even those who are on the simplified taxation system (USN).” Carefully read the documents, clause 4.6 of the Directive of the Central Bank of the Russian Federation dated March 11, 2014 N 3210-U

ostapx1 11/17/2015 at 03:17 pm # Reply

Nikolay, thank you for your feedback. You are absolutely right. Apparently, at some point, due to changes in legislation and inattentive editing of the article by its author, this inconsistency occurred. The material has now been edited in accordance with current legislation.

Vyacheslav 12/06/2015 at 04:59 pm # Reply

Hello. I have an individual entrepreneur on UTII, I just ran out of ECLZ on the cash register and I decided to work without it, because... Perhaps from the new year you will need to think about some kind of cash register with the Internet. Previously, I kept a journal for the cashier, wrote out a receipt and filled out the cash book, and wrote out a consumable note (for reporting). What to do now? So, what would be simpler, but according to the rules? Do I need to continue to maintain a cash book?

Natalia 12/06/2015 at 05:56 pm # Reply

Vyacheslav, individual entrepreneur on UTII is exempt from the mandatory use of a cash register, subject to the registration of BSO for clients or customers. Of course, this simplifies documentation and reduces costs. The procedure for using strict reporting forms is approved in the Regulations approved by Decree of the Government of the Russian Federation of May 6, 2008 No. 359. From 06/01/2014, a cash book for individual entrepreneurs is not required, but you can keep it for clear work, especially since individual entrepreneurs are exempt from approving and complying with the cash limit. You can read about BSO forms on our website in the “Accounting for strict reporting forms” section.

Olga 12/08/2015 at 12:51 # Reply

Tell me, if the individual entrepreneur has just opened, there have been no sales yet. Do I need to keep a cash book these days, or wait for the first sale? I have an individual entrepreneur on the simplified tax system, I have a cash register. The start date of the book has not yet been written on the first page. There are no hired workers.

Natalia 12/08/2015 at 02:19 pm # Reply

Olga, the cash book and the relevant documents for it, since 2014, individual entrepreneurs who do not pay wages to employees in cash can use the simplified tax system. Those. in your case, maintaining a cash book is not an obligation, but a right. If there is no cash flow, then do not fill out the book. But when using a cash register, it is mandatory to keep a log of the cashier-operator and a log of calls for technical specialists. The cash register must be registered with the tax office. List of documents for registering a cash register: Application in the established form (for organizations, a seal is required; for individual entrepreneurs, no). Documents for the purchase of cash registers: cash and sales receipts or cash receipt, invoice, invoice or payment order, invoice, invoice. A form (technical passport) of the KKM with a mark from the technical service center (TSC) about the commissioning of the KKM, about the installed holograms - visual monitoring devices (VMS). Passport of the version of the KKM model and an additional sheet to the passport of the version and (and their copies). Agreement (and copy) with the central service center for the maintenance of the cash register. The cashier-operator's journal in the KM-4 form is laced, numbered, certified by the seal of the enterprise and the signature of the manager. A journal for recording calls of technical specialists and recording work performed in the KM-8 form, laced, numbered, certified by the seal of the enterprise and the signature of the manager. Certificate of registration of individual entrepreneurs for tax registration - TIN (original and copy) Certificate of state registration - OGRN (original and copy) Lease agreement for the installation site of the cash register (original and copy) For commissioning in the Tax Inspectorate, the presence of a cash register is required!

Olga 12/08/2015 at 03:47 pm # Reply

Natalya, thank you very much for your answer. You are right, I do not have a cash book, but a journal of the cashier-operator. Form km-4. I didn’t immediately understand that these were different things. Do you need to fill it out if there haven’t been any sales yet? By the way, I already have everything registered.

Natalia 12/08/2015 at 06:33 pm # Reply

Olga, the cashier-operator’s log is filled out immediately after the Z-report is taken. If no amounts have been entered on the cash register during the current day, then it is not necessary to make a report; if you do not work on the cash register, then you do not need to fill out the cashier-operator log.

Olga 12/09/2015 at 10:21 am # Reply

Natalya, I understand. Thank you very much for the answer.

Svetlana 01/18/2016 at 12:55 # Reply

Natalya, please tell me. If there is no cash register, but there is a cash register and the cashier-operator’s journal is filled out, then is it necessary to draw up a report from the cashier-operator, on the basis of which money is deposited into the cash register, which is not maintained?

Natalia 01/18/2016 at 14:54 # Reply

Svetlana, good afternoon. As far as I understand, you do not keep a cash book and do not fill out receipts and expenditure orders. Since 2014, individual entrepreneurs can afford this. You are using a cash register, therefore, you must draw up the following documents: 1. An act on the transfer of readings from meters - drawn up if a new device has been put into operation (form KM-1). 2. Report on taking readings - if the device is subject to repair (form KM-2). 3. Certificate of return of money - if funds are returned on erroneous checks (form KM-3). 4. Cashier's journal (form KM-4). 5. Cashier's report (form KM -6). 6. Meter readings (form KM-7) - is an appendix to KM-6. 7. Call log for TsTO specialists (form KM-8). 8. Cash verification report - drawn up in the event of an unscheduled inspection by the Federal Tax Service (form KM-9).

Olga Sergeevna 02/01/2016 at 22:55 # Reply

Good afternoon Once again I want to clarify everything for myself. I am opening an individual entrepreneur (online trade, simplified tax system), I must purchase a cash register. For every purchase, make a receipt and also include a delivery note, right? Also maintain: 1) Form KM-4 (based on daily Z-reports). 2) Form KM-6 (I don’t understand its meaning, because there are no employees, accordingly, it will contain everything that is in the KM-4 form). 3) I still don’t understand whether it is necessary to keep a cash book, if not, then is it necessary to notify the tax office about this? 4) Should all Z-reports be filed in the cash book, and if there is none, then in the KM-6 form? What else can the Federal Tax Service check, or rather, what else should I keep track of? Is it necessary to make an order stating that there is no cash limit? well, etc.

Natalia 02/02/2016 at 11:26 am # Reply

Olga Sergeevna, good afternoon. If you work with cash, then under the simplified tax system you are required to use a cash register. The law does not oblige individual entrepreneurs to keep a cash book, but it does not prohibit it either. Reflect this in your accounting policies, as well as the absence of a cash limit (if you keep a cash book). Study the Federal Law of May 22, 2003 No. 54 - Federal Law “On the use of cash register equipment when making cash payments and (or) payments using payment cards.”

Ksenia 02/02/2016 at 01:13 pm # Reply

cash book

Hello! I have an individual entrepreneur, registered in the name of my husband. I work by myself. Draft beer store. Am I required to keep a cash book? simplified tax system, I don’t pay salaries to employees

Natalia 02/02/2016 at 14:16 # Reply

Ksenia, good afternoon. In order of questions: According to Federal Law dated November 22, 1995 N 171-FZ (as amended on June 29, 2015), if you sell beer, you are required to use a cash register. The procedure for registering and operating a cash register is prescribed in Federal Law No. 54 of May 22, 2003 “On the use of cash register equipment when making cash payments...” Individual entrepreneurs are not required to maintain a Cash Book. According to the law, you must be registered by the seller as your husband’s individual entrepreneur.

Imposition of sanctions on individual entrepreneurs for violation of cash discipline requirements

For violation of the procedure for conducting cash transactions or handling cash, an individual entrepreneur may be fined in accordance with Art. 15.1 Code of Administrative Offences. The fine is provided in the amount of 4,000 to 5,000 rubles. Sanctions falling within the scope of this article are established by the Tax Authorities (Article 23.5 of the Administrative Code).

The period for imposing administrative punishment is 2 months. An individual entrepreneur brought to justice for the first time may receive a warning. The condition for mitigating the sanction is the provision of evidence of the primary commission of the violation and the absence of damage caused to other persons.