Report 6-NDFL: general concepts

The sixth income form contains a summary of data on all individuals who earned money from their tax agent, on tax deductions, the amount of taxes withheld and everything else that may affect the calculation of tax transfers to the treasury.

The deadline for submitting the annual form is the beginning of April, the next year after the reporting year. The information in the form is accumulated and submitted to the regulator on an accrual basis for each quarter. More information about the dates for filing 6-NDFL in 2021 is in the infographic below:

The report form itself is unified and approved by the regulator. The report includes two parts:

- General indicators.

- Dates and amounts of actual income received and income withheld.

Below we consider the basic requirements for filling out the form:

- General information. The report is based on information about recorded income paid to individuals from a tax agent, all required deductions, taxes paid according to tax registers

- Income. The 1C user must include in the report all income received by an individual during the reporting period.

- Deductions. The report must reflect the right to tax deductions of all possible options, as well as their actual provision.

- Personal income tax amount. The report contains the calculation and amount of income transferred to treasury accounts.

Personal income tax accounting operations in 1C

Personal income tax is charged not only on wages, but also on vacation, sick leave and other income, except for income provided for by law (for example, child care benefits).

Let’s look at personal income tax in the “Payroll” document. It is located on the tab of the same name in this document. Deductions also apply here. After posting, this data is included in the postings.

The tax is withheld on the date on which the document is posted. It does not withhold personal income tax on other income, such as sick leave, vacations, and dividends. For this purpose, use the “Personal Tax Accounting Operation”.

In the “Salaries and Personnel” menu, select “All personal income tax documents”. In the list form that opens, create a new document with the type of operation “Personal Income Tax Accounting Transaction”.

The main register of tax accounting for personal income tax in 1C 8.3 is the accumulation register “Calculations of taxpayers with the budget for personal income tax”.

Report 6-NDFL in 1C: how to generate it step by step

The machine fills out the data in the report on its own, provided that the initial information is entered correctly into the accounting registers.

In order to start working on drawing up a regulated 6-NDFL report in 1C, you should find a special functionality for this. It is placed in the reporting and references field in 1C-Reporting. Next, a step-by-step algorithm for your further actions is proposed so that the process takes you a minimum of time and is as correct as possible.

Step 1 – Use the create option to tell the machine to display a new working window.

Step 2 – In the list of report types, select the one you need by clicking on the command of the same name.

Step 3 – In the window that opens, enter the following information:

- the name of the required company, provided that the machine accompanies accounting procedures for several of them;

- deadlines for drawing up the reporting form;

- complete the stage by clicking on create.

There are cases where a company has branches that are part of the company and do not have their own separate balance sheet. In such a situation, the parent company needs to prepare a report separately for all branches and send them to the Federal Tax Service where they are actually located.

Step 4 – So that you can make calculations simultaneously for all available tax authorities where branches of your company are registered, use the creation switch for several tax authorities. Then follow the link from the tax authorities and tick off the list exactly where the divisions are registered and thus where the completed report form will be sent. The next step is to select and create fields. The machine understands your procedures as a call for the formation of separate calculations for each branch for a specific tax authority. It is recommended not to rely on automatic calculation and still double-check the numbers issued by the machine for each line.

Step 5 – Next you will need to enter the encoding where the report will go to the regulator. It is indicated in the title in the cell at the location (accounting) (code). All domestic companies put the 220th position here.

Step 6 – A separate copy of the calculation in Form 6-NDFL for the main office of the company and all its branches is created, provided that such creation is not specified automatically. So, you select in the cell submitted to the tax authority (code) the desired option for registration with the tax office and then form the calculation using the filling command.

Formation of 6-NDFL in “1C: ZUP” (“Salaries and personnel management”)

1C developer specialists quickly responded to changes in legislation and supplemented the releases with a new reporting form. Like all other tax reporting forms in 1C, after the reporting period, 6-NDFL can be filled out automatically using software. Let's consider this process using the example of “1C: ZUP” (3.0).

To generate 6-NDFL in 1C: ZUP in the main menu “Reporting. Certificates" you should select "1C - Reporting", then the "Create" item and in the drop-down menu "6-NDFL".

In the window that appears, to fill out 6-NDFL, you must select an organization and indicate the period for which the report is generated.

NOTE! Under the fields to be filled in in the 6-NDFL window you will see information about the edition of the form that the program will fill out. In the future, in case of changes, in order to create a correct report, you will need to track the correct edition of the form.

Press Enter and you will be taken to the form page. We check the data (in addition to information about the organization and period, the type of report (primary or corrective), date of signing, etc. will also be visible). Then click “Fill”, and “1C” transfers the data from the personal income tax accrual registers for the reporting period to the form. The draft report is ready!

It remains to check it. This can be done manually by generating a payslip for the same period in the same “1C”. If the report is filled out correctly, the indicators in lines 020 “Amount of accrued income” and 040 “Amount of calculated tax” in 6-NDFL must coincide with the totals in the columns “Total accrued” and “Total withheld” in the payroll statements for the same period.

Correcting errors for generating 6-personal income tax is a separate, extensive issue. In this article we will not dwell on it in detail. We only note that if discrepancies are found during reconciliation with the payroll sheet, then the 6-NDFL project has a line decoding function available. To do this, place the cursor on the desired line (for example, 020) and either double-click on it with the left mouse button, or press the right mouse button once and select “Decrypt” from the drop-down menu. It is convenient to check the resulting decoding with the payroll sheet to identify differences.

For information on sending a report to the Federal Tax Service via electronic communication channels, read the article “Is it possible to fill out form 6-NDFL online?” .

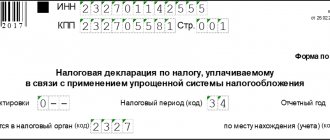

How to fill out the cover page of the 6-NDFL report

Filling out the form requires the user to be attentive, but does not create inconvenience or extreme difficulties in the work. At the top, indicate in the checkpoint field the reason why your company or its branch was registered in the form of a code at the place of registration with the Federal Tax Service. The TIN involves adding information about the tax agent.

The machine, according to the regulations, has the initial calculation settings for the report, which means submitting the form for verification to the regulator for the first time in this reporting period. Therefore, the correction number contains a zero code.

Know that the machine sets the submission deadline (code) and tax period (year) automatically, pulling it from the initial form. The position of submission to the tax authority (code) involves specifying the encoding in the form of a four-digit number of the Federal Tax Service where your company is registered and where you regularly send all reports. The location (accounting) field (this also refers to the code) is where you enter all other places where the tax agent sent miscalculations.

The position of the code according to OKTMO involves telling the encoding machine of the municipality where your company with all its branches is actually located.

All of the above information on the company and its divisions, which are on a separate balance sheet, is recorded in the directory of organizations in the section of the general settings of the company. Everything else is pulled from the organization’s directory, like:

- initials of the tax agent;

- his contact details;

- Company name.

It may happen that there will be empty fields in the report and you do not have the technical ability to enter them manually. The machine informs the user about this by filling the cells with yellow. This only means one thing: the machine was not initially given the initial parameters so that it would involve them in 6-personal income tax. It is possible to correct the current situation by entering informative information into the accounting registers and updating the data through the functionality.

Filling out 6-NDFL in 1C: Enterprise Accounting 8 - VIDEO

Published 04/05/2016 07:46 In this video I will tell you how to create form 6-NDFL in the 1C: Enterprise Accounting 8 edition 3.0 program. How to find a new report in the program, and how is it filled out? How should the amounts of vacation pay, sick leave and wages themselves be reflected in 6-NDFL? Let's submit documents together and see how the information gets into the 6-NDFL report.

You will learn more about filling out 6-NDFL in 1C by watching the recording of the webinar “6-NDFL: from the basics with practical examples in 1C”

Video author: Olga Shulova

Let's be friends on Facebook

Did you like the video tutorial? Subscribe to the newsletter for new materials

Add a comment

Comments

+1 #52 Nadezhda HOA Vega 10/18/2017 22:02 Hello. The income amounts are not filled out in the 6 personal income tax report - page 130. In the accumulation register “Accounting for income for calculating personal income tax” I found the column “do not take into account income in the 6 personal income tax” and there are checkmarks there. Those. this is the reason. How can I remove them? what settings should I go to?

Quote

0 #51 Olga Shulova 07/19/2017 21:10 I quote Natalya Vladimirovna:

Good afternoon, please tell me whether personal income tax on bonuses with code 2002 accrued in June, with the date of payment of income on July 10, 2021, should be included in line 080 in the report for the 2nd quarter, as not withheld?

Good afternoon

Shouldn't, because... This line includes only the tax that cannot be withheld until the end of the tax period. For example, if your organization made expensive gifts to dismissed employees, but there is no way to withhold personal income tax, etc. If the tax was withheld in the 3rd quarter, then it should not be on line 080. Quote 0 #50 Natalya Vladimirovna 07/19/2017 20:17 Good afternoon, please tell me whether personal income tax on bonuses with code 2002 accrued in June, with the date of payment of income on July 10, 2021, should be included in line 080 in the report for the 2nd quarter, how is it not retained?

Quote

0 #49 Olga Shulova 06/10/2016 09:35 I quote Ekaterina:

Olga, would it be correct to conclude from your and my reasoning that only wages can be accrued in one reporting period (and reflected in page 020), and paid in the next (and do not fall into Section 2 YET). In other cases (vacation pay, sick leave, dividends), the amounts should fall into both Section 1 and Section 2, since for these incomes the payment, not the accrual, is decisive. It is so?

I agree with your reasoning.

Perhaps the author was simply mistaken? Since indeed, there are contradictions in the article Quote 0 #48 Ekaterina 06/07/2016 01:38 Quote Author:

Hello, Ekaterina! I adhere to this opinion, it seems logical and justified to me. I quote Ekaterina: this is income not related to salary, which means it is considered received (for personal income tax purposes) when it is paid, and it does not matter here when it is accrued. The accrual is taken into account for settlements with the employee and with funds.

But I’m not familiar with the article from the Simplified magazine that you write about.

Can you tell me which legislative acts the author refers to, and explain my position? The article is as follows: “Private situations We record sick leave benefits in 6-NDFL” M.A. Zarechnaya expert of the magazine “Simplified” I quote: “...In addition, it matters for the report when you issued the sick leave benefit. But for what month it was accrued is unimportant for form 6-NDFL..” Examples follow, the second of which contradicts what was said at the beginning of the article: “Situation No. 2. The benefit was accrued, but was not issued until the end of June. In section 2 of the half-year report, do not record benefits that were not paid before the end of the second quarter. You will show it in the report for 9 months after you give the money to the employee. (-this is understandable) In section 1, reflect the sick leave benefit as follows. In the indicator on line 020, add the accrued amount of benefits (), in line 040 - the calculated personal income tax. In line 070, do not reflect the tax on the benefit amount. Since you have not paid benefits as of the reporting date...” The analysis of this Situation 2 does not provide any references to legislative acts. Maybe I'm misunderstanding something? Olga, would it be correct to conclude from your and my reasoning that only wages can be accrued in one reporting period (and reflected in page 020), and paid in the next (and do not fall into Section 2 YET). In other cases (vacation pay, sick leave, dividends), the amounts should fall into both Section 1 and Section 2, since for these incomes the payment, not the accrual, is decisive. It is so? Quote 0 #47 Olga Shulova 06.06.2016 21:32 Hello, Ekaterina! I adhere to this opinion, it seems logical and justified to me. I quote Ekaterina:

This is income not related to salary, which means it is considered received (for personal income tax purposes) when it is paid, and it does not matter here when it is accrued. The accrual is taken into account for settlements with the employee and with funds.

But I’m not familiar with the article from the Simplified magazine that you write about.

Can you tell me which legislative acts the author refers to, and explain my position? Quote 0 #46 Ekaterina 06/03/2016 20:18 Olga, please dispel my doubts. If it became clear with the salary accrued in March and paid in April, then I cannot figure out the sick leave accrued in March and paid in April. 1c ZUP 2.5 puts this amount in Section 1 of the report for the half-year (the payment is, of course, for the half-year). But here is the date of the accrual document... I was sure that the income was accrued in March, which means it would also be included in the report for the 1st quarter in R.1. But then I read that this is income not related to salary, which means it is considered received (for personal income tax purposes) when it is paid, and it does not matter here when it is accrued. The accrual is taken into account for settlements with the employee and with funds. But yesterday I came across an article in the electronic magazine “simplified”, which says that we enter the accrual of sick leave in March in R.1 6-NDFL, and the payment in April will be reflected in R.2 for the half-year...... And where is the truth ?

Quote

-1 #45 Olga Shulova 05/31/2016 19:51 I quote Ekaterina:

Olga, I watched your video before making the report. I went to a seminar. Everything was clear. And I felt calm. As soon as it came to MY situation, the problems began. Only now have I figured out my task, and even then, I’m not 100% sure. How UNCLEAR everything turned out to be in this 6-NDFL form! I spent a lot of time figuring it out! And the 1C ZUP 2.5 program filled out and filled out in its own crooked way - so I was the first and sent the corrective reports filled out MANUALLY. On the Moscow line, 1C consultations are unsubscribed, there is zero help. It seems that they have screwed it up so much that it’s impossible to understand other people’s cockroaches. Problems, apparently, begin when not everything in life is as beautiful as in the demo examples - we delay salaries, pay dividends in pieces, and as soon as money falls from the sky like rain, it unexpectedly falls to us. Let me note: we have a microform! There are 10 people, but the autofill is not working properly.

Hello! Yes, I also spent a lot of time working with 6-NDFL, especially with ZUP 2.5 (UPP, KA). Now clarifications are coming out, after this letter buh.ru/…/47950 it became a little clearer, we are waiting for it to be implemented in 1C. Although I still have many questions, for example, how will the withheld personal income tax be verified in 2-NDFL and 6-NDFL by year if the filling algorithms are different? I think these are not the last clarifications, so I don’t want to rush into making adjustments. My clients and I will wait until July. By then I will try to make a detailed video on ZUP 2.5. Filling out automatically is possible, but difficult. With some clients, we achieved fully automatic filling in organizations of about 100 people, in others there were manual adjustments, but small ones.

Yes, I also spent a lot of time working with 6-NDFL, especially with ZUP 2.5 (UPP, KA). Now clarifications are coming out, after this letter buh.ru/…/47950 it became a little clearer, we are waiting for it to be implemented in 1C. Although I still have many questions, for example, how will the withheld personal income tax be verified in 2-NDFL and 6-NDFL by year if the filling algorithms are different? I think these are not the last clarifications, so I don’t want to rush into making adjustments. My clients and I will wait until July. By then I will try to make a detailed video on ZUP 2.5. Filling out automatically is possible, but difficult. With some clients, we achieved fully automatic filling in organizations of about 100 people, in others there were manual adjustments, but small ones.

But I agree with you, in life it turned out to be more difficult than in seminars. Although we will definitely manage it anyway! Quote 0 #44 Ekaterina 05/31/2016 18:20 Olga, I watched your video before making the report. I went to a seminar. Everything was clear. And I felt calm. As soon as it came to MY situation, the problems began. Only now have I figured out my task, and even then, I’m not 100% sure. How UNCLEAR everything turned out to be in this 6-NDFL form! I spent a lot of time figuring it out! And the 1C ZUP 2.5 program filled out and filled out in its own crooked way - so I was the first and sent the corrective reports filled out MANUALLY. On the Moscow line, 1C consultations are unsubscribed, there is zero help. It seems that they have screwed it up so much that it’s impossible to understand other people’s cockroaches. Problems, apparently, begin when not everything in life is as beautiful as in the demo examples - we delay salaries, pay dividends in pieces, and as soon as money falls from the sky like rain, it unexpectedly falls to us. Let me note: we have a microform! There are 10 people, but the autofill is not working properly.

Quote

0 #43 Ekaterina 05/31/2016 18:07 I quote Author:

I quote Ekaterina: Olga, thank you for your work! Please tell me: the salary for March will be reflected in Section 1 (020, 030, 040), and on line 080 there will be the amount of personal income tax transferred to the 2nd quarter for transfer to the budget at the time the salary for March is paid in April - similar to “ There is fear of debt for the payer. contributions at the end of the reporting period" in the report to 4-FSS. That is, str 080 will NOT be equal to zero in most cases?

Hello! Yes, at the moment, in line 080, the March personal income tax will be reflected if wages are paid in April. If no new clarifications appear I quote the Author:

I quote Ekaterina: Olga, thank you for your work! Please tell me: the salary for March will be reflected in Section 1 (020, 030, 040), and on line 080 there will be the amount of personal income tax transferred to the 2nd quarter for transfer to the budget at the time the salary for March is paid in April - similar to “ There is fear of debt for the payer. contributions at the end of the reporting period" in the report to 4-FSS. That is, str 080 will NOT be equal to zero in most cases?

Hello! Yes, at the moment, in line 080, the March personal income tax will be reflected if wages are paid in April. If no new clarifications appear , it turned out that page 080 is filled out only if we can never withhold the calculated personal income tax (income in kind, a gift of 10,000 rubles to a FORMER employee, etc.).

The amount of personal income tax on the salary of the last month, after which we report to 6-personal income tax (March, June, September..), will be the difference between lines 040 and 070, i.e. more was calculated, but less was withheld, because the salary is on 31.03 (30.06 , 30.09) has not yet been paid and personal income tax has not been withheld. Although! 1C ZUP 2.5 fills out line 080 for me as personal income tax not withheld according to the March salary. Quote 0 #42 Oksana 05/15/2016 10:25 Quote Author:

I quote Oksana: Good afternoon! Excellent video, everything is clear and understandable. But our program is version 8.2. and for some reason, section 2 is filled out incorrectly, for example, wages are not paid at all. Could you please create a video for version 8.2. And another question: sick leave and vacation pay must be paid separately or can be paid together with wages. Thank you in advance for your answer.

Hello!

Do you work in the 1C: Enterprise Accounting 8 edition 2.0 program? Or in 1C: Salaries and personnel management edition 2.5? They both work on the 1C 8.2 platform, and the algorithms are completely different 1C: Salaries and personnel management edition 2.5 Quote 0 #41 Olga Shulova 05/04/2016 08:08 Quoting Oksana:

Good afternoon! Excellent video, everything is clear and understandable. But our program is version 8.2. and for some reason, section 2 is filled out incorrectly, for example, wages are not paid at all. Could you please create a video for version 8.2. And another question: sick leave and vacation pay must be paid separately or can be paid together with wages. Thank you in advance for your answer.

Hello!

Do you work in the 1C: Enterprise Accounting 8 edition 2.0 program? Or in 1C: Salaries and personnel management edition 2.5? They both work on the 1C 8.2 platform, and the algorithms are completely different Quote 0 #40 Olga Shulova 05/04/2016 08:06 Quote Marina SK:

Good afternoon. I had the following problem - after all the steps taken according to your instructions, form 6-NDFL is not filled out. Why?

Hello!

Do you work in 1C: Enterprise Accounting 8 edition 3.0 (as shown in the video)? Check the movements of documents for accrual and payment of wages in the register “Calculations of taxpayers with the budget for personal income tax.” Are there any records there? And another important question - what release of the program do you have installed? Full number Quote 0 #39 Marina SK 05/01/2016 20:04 Good afternoon. I had the following problem - after all the steps taken according to your instructions, form 6-NDFL is not filled out. Why?

Quote

+1 #38 Oksana 04/30/2016 19:54 Good afternoon! Excellent video, everything is clear and understandable. But our program is version 8.2. and for some reason, section 2 is filled out incorrectly, for example, payment of wages does not fall at all. Could you please create a video for version 8.2. And another question: sick leave and vacation pay must be paid separately or can be paid together with wages. Thank you in advance for your answer .

Quote

0 #37 Olga Shulova 04/28/2016 14:41 I quote Marina Chief Accountant:

I quote Marina Glavbukh: I do payroll in 1c on the last day of the month (for which the salary is calculated). But for some reason, in 6 personal income taxes, accruals for December 15, etc. for the months of 16 are indicated as 12/01/15, 01/01/16, 02/01/16, 03/01/16. For you it is 02/29/16. What am I doing wrong? Why do my dates start with months?

Answer me please!

Most likely, you need to correct the dates of receipt of income in the “Payroll” document, personal income tax tab. In previous versions of the program, until the end of 2015, the start date of the month was automatically set as the date. And from 2021 it’s over. In the event that the program was not immediately updated in 2021, and the calculation was carried out in the old version, the dates turned out to be incorrect. This is my guess. If this is indeed the case, then they need to be corrected and salary payments re-issued. Quote 0 #36 Marina Glavbukh 04/28/2016 1:56 pm Quote Marina Glavbukh:

I do payroll in 1c on the last day of the month (for which the salary is calculated). But for some reason, in 6 personal income taxes, accruals for December 15, etc. for the months of 16 are indicated as 12/01/15, 01/01/16, 02/01/16, 03/01/16. For you it is 02.29.16. What am I doing wrong? Why do my dates start with months?

Answer me please!

Quote 0 #35 Olga Shulova 04/27/2016 21:22 Quote Mafita:

Hello! Tell me, please, how to reflect the accrual and payment of rent to an individual and the withholding and transfer of personal income tax in the 8.3 Accounting program so that it falls into 6-NDFL?

Hello!

To reflect 6-NDFL in the report, it is enough to fill out the document “Personal Tax Accounting Operation”: tabs income, calculated and withheld Quote 0 #34 Olga Shulova 04/27/2016 21:20 Quote People_accountant:

Similarly, line 130 1C: Enterprise Accounting 8 release 3.0.43.195 is not filled out in 6-NDFL. In the “Retained on all bets” tab, the amount of income and the transfer period are indicated, but it’s all to no avail - in line 130 there is 0.

Look at the document entries in the register “Calculations of taxpayers with the budget for personal income tax”, special attention to the last columns.

Was all the information filled out correctly during the process? What date was personal income tax withheld? In general, the dates in section 2 are filled out correctly, only line 130 is zero? Quote -1 #33 Mafita 04/27/2016 00:19 Hello! Tell me, please, how to reflect the accrual and payment of rent to an individual and the withholding and transfer of personal income tax in the 8.3 Accounting program so that it falls into 6-NDFL?

Quote

0 #32 People_accountant 04/26/2016 16:54 Quote Author:

I quote Tatyana: Good afternoon, Olga, thank you very much for your lessons, they help a lot. Question about 6-personal income tax: line 130 of section 2 is not filled in. Dividends in the amount of 19,000 were accrued and paid on 1 day, 01/25/2016, personal income tax in the amount of 2470 was also paid on 01/25/2016. When filling out 6-NDFL: line 025 of section 1 - 19000 line 045 of section 1 - 2470 line 130 of section 2 - empty (with the date 01/25/2016) line 140 of section 2 - 2470 (with the date 01/25/2016). What's wrong???

I quote Marina Glavbukh:

Similarly with Tatyana, line 130 1C: Enterprise Accounting 8 release 3.0.43.195 is not filled out in 6-NDFL.

Hello!

For dividends, the document “Personal Income Tax Accounting Transaction” must be entered. Pay special attention to filling out the table on the “Withheld at all rates” tab, the amount of income must be indicated, the deadline for transferring personal income tax too. Similarly, line 130 1C: Enterprise Accounting 8 release 3.0.43.195 is not filled out in 6-NDFL. In the “Retained on all bets” tab, the amount of income and the transfer period are indicated, but it’s all to no avail - in line 130 there is 0. Quote 0 #31 Olga Shulova 04/25/2016 21:08 Quoting Tatyana:

Good afternoon, Olga, thank you very much for your lessons, they are very helpful. Question about 6-personal income tax: line 130 of section 2 is not filled in. Dividends in the amount of 19,000 were accrued and paid on 1 day, 01/25/2016, personal income tax in the amount of 2470 was also paid on 01/25/2016. When filling out 6-NDFL: line 025 of section 1 - 19000 line 045 of section 1 - 2470 line 130 of section 2 - empty (with the date 01/25/2016) line 140 of section 2 - 2470 (with the date 01/25/2016). What's wrong???

I quote Marina Glavbukh:

Similarly with Tatyana, line 130 1C: Enterprise Accounting 8 release 3.0.43.195 is not filled out in 6-NDFL.

Hello!

For dividends, the document “Personal Income Tax Accounting Transaction” must be entered. Pay special attention to filling out the table on the “Withheld at all rates” tab, the amount of income must be indicated, the deadline for transferring personal income tax must also be Quote 0 #30 Marina Glavbukh 04/25/2016 12:55 Similarly, with Tatyana, line 130 1C is not filled out in 6-NDFL: Enterprise Accounting 8 release 3.0.43.195

Quote

0 #29 Tatyana 04/23/2016 12:46 I quote Author:

I quote Tatyana: Good afternoon, Olga, thank you very much for your lessons, they help a lot. Question about 6-personal income tax: line 130 of section 2 is not filled in. Dividends in the amount of 19,000 were accrued and paid on 1 day, 01/25/2016, personal income tax in the amount of 2470 was also paid on 01/25/2016. When filling out 6-NDFL: line 025 of section 1 - 19000 line 045 of section 1 - 2470 line 130 of section 2 - empty (with the date 01/25/2016) line 140 of section 2 - 2470 (with the date 01/25/2016). What's wrong???

Hello!

Which 1C program are you working in and what configuration release? It is better to look at this information in the help, for example, it could be 1C: Enterprise Accounting 8 release 3.0.43.174. Now this information is extremely important, everything is changing very quickly. Good afternoon, I work in 1C: Enterprise 8.3 (8.3.8.1652), basic, edition 3.0.43.187 Quote 0 #28 Marina Glavbukh 04/22/2016 22:22 I do payroll calculations in 1C on the last day of the month (for which salaries are calculated) . But for some reason, in 6 personal income taxes, accruals for December 15, etc. for the months of 16 are indicated as 12/01/15, 01/01/16, 02/01/16, 03/01/16. For you it is 02/29/16. What am I doing wrong? Why do my dates start with months?

Quote

0 #27 Olga Shulova 04/21/2016 19:47 I quote Tatyana:

Good afternoon, Olga, thank you very much for your lessons, they are very helpful. Question about 6-personal income tax: line 130 of section 2 is not filled in. Dividends in the amount of 19,000 were accrued and paid on 1 day, 01/25/2016, personal income tax in the amount of 2470 was also paid on 01/25/2016. When filling out 6-NDFL: line 025 of section 1 - 19000 line 045 of section 1 - 2470 line 130 of section 2 - empty (with the date 01/25/2016) line 140 of section 2 - 2470 (with the date 01/25/2016). What's wrong???

Hello!

Which 1C program are you working in and what configuration release? It is better to look at this information in the help, for example, it could be 1C: Enterprise Accounting 8 release 3.0.43.174. Now this information is extremely important, everything is changing very quickly. Quote 0 #26 Tatyana 04/19/2016 12:44 Good afternoon, Olga, thank you very much for your lessons, they are very helpful. Question about 6-personal income tax: line 130 of section 2 is not filled in. Dividends in the amount of 19,000 were accrued and paid on 1 day, 01/25/2016, personal income tax in the amount of 2470 was also paid on 01/25/2016. When filling out 6-NDFL: line 025 of section 1 - 19000 line 045 of section 1 - 2470 line 130 of section 2 - empty (with the date 01/25/2016) line 140 of section 2 - 2470 (with the date 01/25/2016). What's wrong???

Quote

0 #25 Olga Shulova 04/18/2016 20:19 Quoting Leyla:

Good afternoon, Olga. Thanks for the clear video. I have a question regarding payments with code 1400 (rent). In my 1SKA for these payments, I fill out the document Adjustment of personal income tax accounting with the payment date d-yes. As a result, in 6-NDFL, lines 020, 040,070,100,110,120,140 are filled in for these incomes. Page 130 for some reason is not filled in, although logically it should. I have a configuration in edition 1.1 (1.1.70.2) 1C:Enterprise 8.3 (8.3.5.1517)

Hello!

I would advise you to hold off on submitting the report from the CA for now. Now changes are being made to the algorithms for filling out line 130, tomorrow they promise a new release for ZUP 2.5. I think next will be a release for KA. Perhaps after the update something will change and the problem will go away on its own. BUT in general, line 130 is for reference purposes, it is not in the published control ratios Quote 0 #24 Olga Shulova 04/18/2016 20:16 I quote Lyudmila Aleksandrovna:

Hello Olga! Tell me, please, if there are several vacation pay in one month, should they be shown in one amount or separately for each person? And some also have a deduction for children, personal income tax will be less, won’t this be taken as a mistake?

Hello!

Section 2 is completed in terms of the dates of receipt of income; if vacation pay was paid to several employees on the same day, then they will be reflected together. If the payment was made on different days, then the lines will be different. The use of deductions to which taxpayers are entitled is not a mistake Quote 0 #23 Olga Shulova 04/18/2016 19:44 Quote Tatyana:

I quote Author: I quote Tatyana: Thank you very much! Please tell me how to reflect the deduction and accrual of personal income tax when an employee is dismissed before the end of the month?

Hello!

We are also talking about the 1C: Enterprise Accounting configuration, as in the video? Or do you work in 1C: Salary and HR management? Thank you! I work in 1C Accounting. In 1C: Accounting, everything is quite simple: make a separate document on payroll with the date of dismissal (this date will appear in the report as the date of receipt of income), then a statement and payment. The date of payment will be taken as the withholding date, the transfer period will be the day following the day of payment Quote 0 #22 Leyla 04/18/2016 15:22 Good afternoon, Olga. Thanks for the clear video. I have a question regarding payments with code 1400 (rental payments). In my 1SKA for these payments, I fill out the document Adjustment of personal income tax accounting with the payment date d-yes. As a result, in 6-NDFL, lines 020, 040,070,100,110,120,140 are filled in for these incomes. Page 130 for some reason is not filled in, although logically it should. I have a configuration in edition 1.1 (1.1.70.2) 1C:Enterprise 8.3 (8.3.5.1517)

Quote

0 #21 Lyudmila Aleksandrovna 04/18/2016 11:23 Hello Olga! Tell me, please, if there are several vacation pay in one month, should they be shown in one amount or separately for each person? And some also have a deduction for children, personal income tax will be less, won’t this be taken as a mistake?

Quote

0 #20 Tatyana 04/14/2016 22:13 I quote Author:

I quote Tatyana: Thank you very much! Please tell me how to reflect the deduction and accrual of personal income tax when an employee is dismissed before the end of the month?

Hello!

We are also talking about the 1C: Enterprise Accounting configuration, as in the video? Or do you work in 1C: Salary and HR management? Thank you! I work in 1C Accounting. Quote 0 #19 Olga Shulova 04/14/2016 20:24 I quote Marina Vyacheslavovna:

The personal income tax refund was generated due to the fact that the employee was on vacation from 02/01/2016 to 03/09/2016. And since she is a single mother, she provided double deductions for two children, i.e. 5600 rub. Vacation pay was paid in January 2021, along with a salary in the amount of 17,404 rubles. (Personal income tax RUR 1,535). There was no salary in February but deductions are provided. In March, the salary was 8,117 rubles (including 1,000 mat aid, not subject to personal income tax). for March the amount for personal income tax is 8117-1000-5600-5600 = -4083. Personal income tax -531 rub.

I can’t answer this question with confidence, because...

There are still not enough explanations for filling it out. In my opinion, you are reasoning logically when describing the distribution by rows in the previous message. In line 140 then, logically, there should be a difference, i.e. the amount that was actually withheld and transferred to the budget. But I didn’t see line 140 at all in the published control ratios, so it’s not clear how this indicator will be checked. Quote 0 #18 Olga Shulova 04/14/2016 20:07 I quote Tatyana:

Thank you very much! Please tell me how to reflect the deduction and accrual of personal income tax when an employee is dismissed before the end of the month?

Hello!

We are also talking about the 1C: Enterprise Accounting configuration, as in the video? Or do you work in 1C: Salary and HR management? Quote 0 #17 Olga Shulova 04/14/2016 20:05 I quote Tatyana Leonidovna:

Good afternoon Olga! Help me figure it out, the OS accounting card does not include the initial cost of the OS and, accordingly, I cannot depreciate the OS.

Hello!

Questions on the topic 6-NDFL are discussed here, please, in the “Question and Answer” section or in the comments to articles on fixed assets accounting. Thanks for understanding! Quote 0 #16 Tatyana 04/13/2016 19:32 Thank you very much! Please tell me how to reflect the deduction and accrual of personal income tax when an employee is dismissed before the end of the month?

Quote

0 #15 Tatyana Leonidovna 04/13/2016 13:52 Good afternoon Olga! Help me figure it out, the initial cost of the fixed assets does not appear on the asset accounting card and, accordingly, I cannot depreciate the fixed assets.

Quote

0 #14 Marina Vyacheslavovna 04/13/2016 08:11 The personal income tax refund was formed due to the fact that the employee was on vacation from 02/01/2016 to 03/09/2016. And since she is a single mother, she provided double deductions for two children, i.e. 5600 rub. Vacation pay was paid in January 2021, along with a salary in the amount of 17,404 rubles. (Personal income tax RUR 1,535). There was no salary in February but deductions are provided. In March, the salary was 8,117 rubles (including 1,000 mat aid, not subject to personal income tax). for March the amount for personal income tax is 8117-1000-5600-5600 = -4083. Personal income tax -531 rub.

Quote

0 #13 Olga Shulova 04/12/2016 21:28 I quote Marina Vyacheslavovna:

Hello! I had a personal income tax refund in March 2021. 531 rubles. Taking into account the return, personal income tax payable is 7373 rubles. 04/15/2016. Will it be correct in line 080 - 7904 rubles, in line 090 - 531 rubles, in line 140 - ???

Hello!

What was the reason for the return? And for what period? Quote 0 #12 Olga Shulova 04/12/2016 21:27 I quote Ekaterina:

Olga, if dividends for 2014 were accrued in the Accounting program on April 15, 2015. However, due to the financial difficulties of the organization and extremely unstable payments from customers, they were paid in parts - as money was received in the current account. Thus, in January and February 2021, such payments were made to the founders. The parts were calculated in the Salary Program. 6-NDFL is formed in ZUP. What is the actual date? receipt of income (p.2, page 100) in our case, should it be set correctly - 04/15/15 or 01/22/16 and 02/11/16?

I think that it is necessary to compress the dates of income payment Quote

0 #11 Olga Shulova 04/11/2016 15:03 Quote Ekaterina:

Olga, thank you for your work! Please tell me: the salary for March will be reflected in Section 1 (020, 030, 040), and on line 080 there will be the amount of personal income tax transferred to the 2nd quarter for transfer to the budget at the time the salary for March is paid in April - similar to “ There is fear of debt for the payer. contributions at the end of the reporting period" in the report to 4-FSS. That is, str 080 will NOT be equal to zero in most cases?

Hello! Yes, at the moment, in line 080, the March personal income tax will be reflected if wages are paid in April. If no new clarifications appear Quote

+1 #10 Marina Vyacheslavovna 04/08/2016 12:26 Hello! I had a personal income tax refund in March 2021. 531 rubles. Taking into account the return, personal income tax payable is 7373 rubles. 04/15/2016. Will it be correct in line 080 - 7904 rubles, in line 090 - 531 rubles, in line 140 - ???

Quote

0 Ekaterina 04/08/2016 02:49 Olga, if dividends for 2014 were accrued in the Accounting program on 04/15/2015. However, due to the financial difficulties of the organization and extremely unstable payments from customers, they were paid in installments - as money arrived at the settlement check. Thus, in January and February 2021, such payments were made to the founders. The parts were calculated in the Salary Program. 6-NDFL is formed in ZUP. What is the actual date? receipt of income (p.2, page 100) in our case, should it be set correctly - 04/15/15 or 01/22/16 and 02/11/16?

Quote

0 Ekaterina 04/08/2016 02:35 Olga, thank you for your work! Please tell me: the salary for March will be reflected in Section 1 (020, 030, 040), and on line 080 there will be the amount of personal income tax transferred to the 2nd quarter for transfer to the budget at the time the salary for March is paid in April - similar to “ There is fear of debt for the payer. contributions at the end of the reporting period" in the report to 4-FSS. That is, str 080 will NOT be equal to zero in most cases?

Quote

-1 Olga Shulova 04/06/2016 19:38 I quote Marina Vyacheslavovna:

Thank you very much! You explain everything clearly and clearly. And most importantly, everything fits into place in my head thanks to your calm and pleasant voice.

Thanks for the nice words!

I tried very hard Quote +4 Marina Vyacheslavovna 04/06/2016 18:35 Thank you very much! You explain everything clearly and clearly. And most importantly, everything fits into place in my head thanks to your calm and pleasant voice.

Quote

0 Olga Shulova 04/05/2016 20:10 I quote Nadezhda Aleksandrovna:

Is it possible to transfer personal income tax in advance of a larger amount one time, and not on the date following the payment of salary and the last day of the month?

No, you cannot pay personal income tax in advance.

The fact is that the organization is only a tax agent, and personal income tax payers are individuals. Accordingly, an organization cannot pay tax from its own funds; it must first withhold it from individuals. persons, and this occurs at the time of payment of wages or other monetary rewards. When paying personal income tax in advance, there is a high probability of getting a fine, because Amounts paid from the enterprise's funds are not personal income tax by definition. And accordingly, it is considered that the organization did not fulfill its duties as a tax agent, since the amount calculated and withheld from individuals. persons the tax was not paid to the budget within the required period. Quote 0 Olga Shulova 04/05/2016 20:05 I quote Yulia:

Thank you, everything is very accessible. Are you planning to talk about the MP-sp form? Thank you

I don’t plan to in the near future, but I’ll write it down as a wish Quote

+1 Nadezhda Aleksandrovna 04/05/2016 17:02 Is it possible to transfer personal income tax in advance of a larger amount as a one-time payment, and not on the date following the salary payment and the last day of the month?

Quote

0 Natalya Latysheva 04/05/2016 15:22 Thank you, Olya! Everything is clear and accessible!

Quote

0 Yulia 04/05/2016 13:45 Thank you, everything is very accessible. Are you planning to talk about the MP-sp form? Thank you

Quote

Update list of comments

JComments

Date of signing of the 6-NDFL report

The date of signature of the report is an explicit parameter and the machine automatically uses the date indicated in your PC. The calendar number that is assigned on the title page mainly directly affects the auto-filling of calculations according to the form algorithm specified by the developers. This refers to line 080 of the first section of the reporting form, informing the user about the amount of income not withheld by the tax agent

Similar information is pulled up from the machine’s accounting registers, inclusive of the date of signing your report.

Deadlines for submitting 6-NDFL in 2021

- First quarter - 05/04/2016

- Half year – 08/01/2016

- 3 quarters – 10/31/2016

- For the entire 2021 – 04/01/2017

There should be no questions asked when completing the first section of the form. Here we indicate general indicators, such as the percentage tax rate, total amounts and the number of employees of the enterprise who received income.

Of greater interest is filling out the second section of 6-NDFL.

Here you will need to fill in all the dates of income actually received, the amount of income and the amount of personal income tax withheld from a specific income. In addition, it will be necessary to indicate the date of transfer of withheld personal income tax. Moreover, if different types of income fall on the same date of receipt, but the deadlines for paying the tax are different, then they must be posted on different lines. Nowadays there is a lot of talk about the fact that the declaration is filled out with final data, without analytics on employees, and filling it out is not difficult. Everything said above suggests the opposite.

Form 6 personal income tax (according to KND 1151099) in Excel format can be found here.

Here is a small example of filling out 6-NDFL on the second sheet:

I gave a simple example of four employees, at one interest rate, for three months. It’s already dazzled in the eyes.

Now let’s try to figure out how we can now keep track of personal income tax in the 1C program: “Salaries and personnel management.” And what are the forecasts for automating the completion of this declaration.

Features of filling out the first section of the 6-NDFL report

This section of the report shows the general indicators of the income of all individuals, as well as the calculated and paid income from it since the beginning of the year on a cumulative basis using the amount of deductions established at the legislative level. In a situation where there was a transfer of income to the treasury by the same company, but at different interest rates, the first section should be filled out line by line for each such percentage, in addition to positions 060-090.

The user must remember that the amounts of paid earnings are subject to income tax either partially or in full. All non-taxable income listed in the Tax Code of the Russian Federation should not be added here.

The amount of actual earnings received for work performed by an individual, that is, having a tax code of 2000, 2530, and all other material benefits, will refer to the last day of the month when the employer accrued such earnings. For all other types of income, a calendar date will be indicated, which implies such payment, indicated in the accounting documents for their calculation.

Based on such dates of earnings received, you have the right to determine the required month of the tax period and the reporting period itself to include the earnings received by an individual. This requirement is completely similar to the preparation of certificates in form 2-NDFL.

For example, we can cite the case of income taxation at a 35 percent rate as a material benefit from savings for the use of borrowed funds. No tax deduction can be applied to such interest, and as a result, in line 020 you enter the amount of income accrued by you, and on line 040 enter the amount of calculated income tax.

Filling out section 1 of form 6-NDFL

This section indicates the amounts of accrued income, calculated and withheld tax, aggregated for all individuals, on an accrual basis from the beginning of the tax period at the appropriate tax rate.

If we have payments to individuals during the tax period, taxed at different rates, then section 1 will be filled out by the program for each tax rate.

Section 1 states:

- Line 010 – tax rate. By clicking on the cell, we can select the bet we need;

- In line 020 – accrued income is reflected on a cumulative basis

If wages or travel allowances were accrued in March, but paid in April, then such employee income will be included in the report for the first quarter, because according to these types of payments, the date of actual receipt of income is the date of accrual (Letter of the Federal Tax Service of the Russian Federation dated 01.08.2016 No. BS-4-11/). The situation is different with sick leave, vacation pay and other payments. For their types of payments, the date of actual receipt of income is the date of payment. For this reason, if they were accrued at the end of March, but paid in April, they will not be included in the report for the first quarter, but will be reflected in 6-NDFL for the half year.

Registers of entries will help you analyze personal income tax amounts. What it is? In essence, accounting in 1C is the recording of documents. Each document has a result, for example, records accrual amounts. These results can be viewed using reports that can summarize the results across documents and show the user the total. However, there are usually a lot of documents, so the documents record their results (“movements”) in special tables - 1C registers, which themselves summarize the results so that the report simply displays the pre-calculated totals.

The “1C” register is a table, the same as in Excel; each document writes one or several lines of its movements (results) with some sign – plus or minus – into the “1C” register. This means that the total of the “1C” register has changed to the corresponding number.

To open the registers of records responsible for reflecting personal income tax amounts, we will need:

The first option: go to “Payroll and contributions” - “More” - “Document movement”. In the “Output only” field, select two registers: “Calculations of taxpayers with the budget for personal income tax” and “Accounting for income for calculating personal income tax.”

Second option: “All functions - “Accumulation registers” - select one by one “Calculations of taxpayers with the budget for personal income tax” and “Accounting for income for calculating personal income tax.”

- In section 1, the amount of deductions for income from line 020 is reflected in line 030 . For example, professional, standard, property, social.

To find out what deductions were applied in a particular month and what income they relate to, we will need the “Personal Income Tax Analysis by Month” report. It clearly demonstrates the deductions applied. The report is located in the section “Taxes and Contributions” – “Tax and Contribution Reports” – “Personal Income Tax Analysis by Month”.

- Line 040 indicates the total amount of calculated personal income tax on income, which is reflected in line 020, minus deductions.

- Line 050 indicates the total amount of fixed advance payments by which the calculated tax amounts were reduced.

In section 1, you can manually add or delete a block of lines 010-050. To add another block, click on the link “Add lines 010-050”; to delete this block, click on the red cross located near line 010.

In addition to lines 020 - 050, the first section also contains lines 070 - 090. They are not filled in by the date of receipt of income.

Adjustment of the 6-NDFL report in 1C

The first reporting section allows the user some freedom of action in the form of deleting or additionally entering a block of lines 010-050's. Using the functionality of the same name, you can implement this option.

You have the right to remove unnecessary lines by clicking on the cross marked in red next to the 010th line. You also have the opportunity to manually assign income taxable to tax in the agreement in order to eliminate cases of double taxation. You will see the results of the section on tax rates in fields 060 – 090. Anything that is not clear to you for any reason, you have the right to decipher for your understanding when using the functionality of the same name.

Entering data into the first section of form 6-NDFL

This section contains summarized income for all individuals, information on accrued tax payments and those due for payment. All data is presented on a cumulative basis. They are summarized from the beginning of the tax period, indicating the applicable tax rate.

If the company made payments to individuals in the tax period under review, to which different tax rates must be applied, then the program will perform a separate calculation for each rate.

Section 1 contains:

- field 010 - tax rate. The cell is active; by hovering the mouse cursor over the field, the specialist can independently select the value;

- field 020 indicates the amount of accrued income on a cumulative basis.

For example, if salaries or travel accruals were made in March, but were actually transferred in April, then such income is included in the calculation for the first quarter. Letter No. BS-4-11/ [email protected] clearly characterizes this situation.

The situation is different with sick leave and other social benefits. The law interprets the date of receipt of income only as the date of its actual transfer. That is, if such payments were accrued in March and made in April, then they are reflected in the report for the first half of the year.

Analysis of personal income tax accruals can be carried out using registers of records. According to the method of operation, the 1C platform is a large repository of recorded documents. Each amount and document leaves a trace in the digital database of the platform. Therefore, it is easy to calculate and analyze any charges.

But the volume of documents stored in some organizations is simply enormous. Therefore, the developers created special registers that contain information about each primary accounting document entered and posted.

Registers have the ability to independently calculate the amount by adding the totals of each document. The 1C platform register is a table similar to Excel, in which each document changes the value of several related rows in the table. The final value can be either decreased or increased.

In order to gain access to data registers that contain information of interest to the user about reflected personal income tax values, the user must perform the following actions:

Option 1. Go to the “Salaries and Contributions” tab, activate the “More” option, then “Document Movement”. In the “output only” tab we take two registers “Calculations with the budget for personal income tax”, as well as “Accounting for income for the purpose of calculating personal income tax”.

In section 1, the total amount of deductions for income from paragraph 020 is transferred to paragraph 030. Professional, social and some other charges relate to them.

In order to find out exactly what deductions were used and to what composition of income they were applied, you need to activate the “Monthly Personal Income Tax Analysis” tab. In such a report, you can most clearly see exactly what deductions and deductions were taken into account. The report itself is located in the “Taxes and Contributions” tab, in the “Taxes and Contributions Reports” subgroup.

Field 040 contains information about the total amount of personal income tax, which was calculated according to information about income from field 020. It must be remembered that the amount from field 020 should be reduced by the deductions made.

Field 050 contains information about the amount of fixed advance payments, due to which the tax amount was reduced.

In the first section, it is possible to make adjustments manually. This applies to field block 010 -050. To add a block or line, the user must activate the option “Add fields 010 - 050”. To remove unnecessary ones, use a red cross.

The first section contains fields 070-090; information is entered into these fields not from the date of receipt of payments.