The filling height is taken to be the average measurement value, rounded to 1 cm. 4.2.5. Determining the filling height remotely (from the control panel) during inventory is not allowed. 4.3. Sampling 4.3.1. Fuel samples are taken in accordance with GOST 2517-85. 4.3.2. Fuel samples must be taken sequentially from top to bottom. 4.3.3. Point samples from vertical tanks to compile a combined sample (see Appendix 1) are taken with portable samplers from three levels: the top - 250 mm below the fuel surface; middle - from the middle of the height of the fuel column; lower - 250 mm above the bottom of the tank. Samples from the upper, middle and lower levels are mixed in a ratio of 1:3:1. 4.3.4. When the fuel level in the tank is no more than 2000 mm, spot samples are taken from the upper and lower levels according to clause 4.3.3.

Inventory of fuels and lubricants at the enterprise

Attention

The act of removing residual fuel from car tanks is used to monitor the use of fuel and lubricants by drivers. Each enterprise establishes with its accounting policies the rules and deadlines for performing control functions. This norm is especially important for organizing order and reliability in accounting for fuel and lubricants.

Info

The availability of fuel is checked by a commission, which is appointed by the manager and consists of heads of departments, accounting departments, and technical workers. Remaining withdrawals are made monthly. According to the report, a statement is drawn up, which establishes the result of using fuel and lubricants for the month. This act is drawn up in one copy and filled out manually or using computer technology.

When entering information, you must indicate the date on which the document is drawn up and the composition of the commission.

Why do you need an act for writing off fuel and lubricants?

The act relates to primary documentation and is of great importance for the accounting and tax accounting of the organization. It allows you to calculate the expenses incurred by the company on fuels and lubricants in order to subsequently deduct them from profit, thus reducing the tax base.

It should be noted that in addition to the write-off act, to carry out this procedure, you must have one more document: the driver’s waybill, which reflects in detail information about the fuel and lubricants spent, kilometers traveled, time spent on the road and other data.

Waybills must be issued at the beginning of the working day, after which drivers are required to submit them to the accounting department (with an advance report that records the expenditure of cash issued for fuel, as well as checks and receipts).

Commission approval

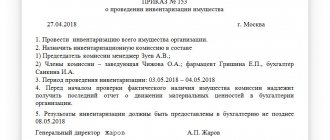

In order to legally write off fuels and lubricants, as well as to correctly draw up the act, the organization must create a special commission consisting of at least two people. For her appointment, the head of the enterprise issues a separate order. The commission should include employees from various departments, as well as a financially responsible person. In this case, it is advisable to allocate a chairman and ordinary members to the commission.

The commission’s tasks include reconciling actual fuel costs with the standards established by the company (it should be noted that they are different for each type of transport and must be approved separately), conducting test trips with drivers to check the amount of daily fuel, oil consumption, etc. , as well as collection of waybills for the reporting period.

NOTE! The creation of a commission is required only in large organizations; small businesses can do without it: here, to write off fuel and lubricants, a simple written decision of the head of the company is sufficient.

Folk tricks

A stationary device that could measure the amount of fuel in the tank with an accuracy of up to a liter is not included in any of the most complete configurations of modern cars. But among car enthusiasts and specialists, on automotive forums, you can find a lot of advice on determining these residues: from rocking the car to evaluate the sound (the less gasoline, the louder the splashes) to weighing it and comparing it with the weight in the owner’s manual. One of these original algorithms for measuring fuel residues is to drain it from the tank into a measuring container, and then pour it back into the tank.

Of course, there are more reasonable methods that are suitable in road conditions.

By instruments

If the fuel indicator is working, the first solution is to navigate it. For example: the volume of the tank is 50 liters, 10 divisions are conventionally marked on the scale, which means that each “beats” 5 liters. When estimating the remaining fuel in this way, remember that the result will be approximate, and pay attention to the location of the car: the car must be strictly horizontal, otherwise the indicator will not correspond to reality.

More accurate readings can be obtained using a special probe. The gas tanks of some old cars were supplied with it from the factory, but by analogy you can do it yourself, having studied the topic well. The distance between the cutoffs depends on the size and shape of the tank; the length of the ruler must be at least one and a half meters, and the material from which it is made must not contain metal and not create sparks.

Using diagnostic mode

If your car has a dashboard from the Renault family, which selectively includes LADA, Nissan and some others, you can find out how much gasoline is in the tank, accurate to the nearest liter, in the panel diagnostic mode.

To run diagnostics on the device, you need to:

– before turning on the ignition, hold down the daily mileage reset button for 5 seconds, then turn on the ignition and release the button when the instrument needles begin to move;

– use the same button to switch the diagnostic mode of the instrument panel, finding the gas pump icon in the upper right corner.

Below this icon a number is displayed that exactly corresponds to the volume of fuel remaining in the gas tank.

You can check whether the diagnostic mode of the instrument panel will work on a specific car experimentally.

The act of removing fuel residues from car tanks

Important

Persons responsible for the safety of fuels and lubricants give a receipt stating that by the beginning of the inventory, all expenditure and receipt documents for fuels and lubricants were submitted to the accounting department and all fuels and lubricants that arrived at the warehouse under their responsibility were recorded, and those disposed of were written off as expenses. 7.8. In the event of a change in financially responsible persons, both persons are present during the inventory, and in the act of removing the remains of fuel and lubricants, the person who accepted the fuel and lubricants signs for their receipt, and the person who handed them over signs for their delivery. Reception and transfer of fuel and lubricants is carried out according to their actual quantity, taking into account the natural loss and error of measuring instruments.

7.9. Before conducting an inventory, pipelines must be completely filled or emptied. Control is carried out using air valves installed on elevated or lower sections of the pipeline.

How to calculate your own standard

If there is no limit approved by the Ministry of Transport for a machine, or the organization decides to use a different value, it has the right to calculate its own limit. Typically, in such a situation, companies act in one of two ways.

The first way is to borrow information about fuel consumption from the technical documentation for the car. This approach corresponds to the position of the Russian Ministry of Transport (see “The rules for determining fuel consumption standards for passenger cars have changed”).

The second way is to create a commission and take measurements. To do this, you need to pour a certain amount of gasoline into the empty tank of the car, for example, 100 liters. Then the car should be driven until the tank is completely empty. Based on the speedometer readings, you need to determine how many kilometers it took to completely empty the tank. Finally, the number of liters must be divided by the number of kilometers. The result will be a figure showing how much gasoline the car consumes when driving one kilometer. This indicator should be recorded in the act and signed by all members of the commission.

Since fuel consumption depends on travel conditions, it is better to make control measurements “for all occasions”: separately - for a loaded and empty car, separately - for summer and winter trips, separately - for idle time with the engine on, etc. All obtained results should be reflected in the act drawn up and signed by the commission.

There is a simpler option: to approve one basic standard (for example, for the summer period) and increasing coefficients: for winter trips, for trips on congested roads, etc.

content and procedure for inventory of fuels and lubricants

RULES for technical operation of power plants and networks. M.: Energoizdat, 1977. 10. STANDARD instructions for the operation of fuel oil facilities of thermal power plants.: TI 34-70-009-82. SPO Soyuztekhenergo, 1982. 11. GOST 26976-86. GSI. Oil and petroleum products.

Mass measurement methods. 12. RULES for fuel accounting at power plants. M.: SPO Soyuztekhenergo, 1982. CONTENTS 1. General part. 1 2. Safety precautions during inventory. 2 3.

Accounting for fuel consumption in an organization

The introduction of a fuel consumption monitoring system does not exclude the need to organize fuel and lubricants accounting, starting with primary documents.

Accounting for fuel consumption at the enterprise is carried out on the basis of the Regulations “On Accounting and Reporting”.

Gasoline is accepted for accounting at its actual cost - the purchase price excluding VAT to account 10 “Materials” subaccount 3 “Fuel”.

There are no restrictions in the legislation regarding the write-off of the cost of fuel and lubricants to the cost of production. The main condition that allows this to be done is the availability of documents confirming the use of fuel in business activities.

This is evidenced by waybills and waybills additionally attached to them. These documents contain all the information about mileage, refueling and the weight of the transported cargo necessary to calculate the normal gasoline consumption for a particular car.

Fuel consumption standards are set depending on the car brand, year of manufacture, modification, design, trailer, etc. All this information is contained in the Consumption Standards for motor vehicles approved by the Ministry of Transport of the Russian Federation on March 14, 2008 No. 23.

For the purpose of calculating taxable profit, fuel costs can be taken into account in two ways: as part of material costs and other expenses related to the main activities of the enterprise.

Business representatives turning to outsourcing companies for HR services is becoming increasingly popular. This is explained by the desire to receive professional help and create a system of effective personnel management, providing oneself with good personnel.

The work of a personnel officer can be very intense, especially if the enterprise is large and there are many employees. Some programs come to the rescue, greatly simplifying personnel accounting in the company. Read about HR management software.

The choice of method depends on the purpose of the car: for production purposes these costs are included in material costs, for management needs - in other costs. Expenses for fuel and lubricants are written off at actual costs. They must be documented and justified from an economic point of view (Article 252 of the Tax Code of the Russian Federation).

The process of accounting for fuel and lubricants is simplified by purchasing it using fuel cards. This is an effective and fairly simple method that allows you to keep accurate fuel records and eliminate unauthorized gasoline refills. To reflect these expenses in the company's accounting, the documents provided by the processing center are sufficient.

Economical fuel consumption and its strict accounting are the most important tasks, the solution of which is a prerequisite for the effective operation of a business entity.

Inventory of fuels and lubricants at the enterprise

7 List of used literature.. 7. After approval, the commission submits one copy of the Act to the financial department, and the second to the head (storekeeper) of the fuel and lubricants warehouse. 7.20. In cases of detection of shortages or surpluses in excess of permissible measurement errors, the commission conducts a thorough investigation. Those responsible for this will be held accountable. For all shortages and surpluses, the commission must receive written explanations from financially responsible persons. Explanations are attached to the act of withdrawal of balances. In the case when, when setting off shortages with surpluses by re-grading, the cost of the missing fuel and lubricants is higher than the cost of the fuel and lubricants found in surplus, this difference in cost should be attributed to the guilty parties. The procedure for writing off shortages and receiving surplus fuel and lubricants is determined by the current “Regulations on Accounting Reports and Balance Sheets.” 7.21.

Fuel fraud

Before setting up a fuel control system, you should find out how it is stolen.

There are a lot of options, but the most common fuel theft fraud schemes are as follows:

Providing “left” fuel receipts to the accounting department. This scheme works in those enterprises where drivers purchase fuel and lubricants in cash and report receipts to the accounting department. Drivers, citing exceeding the established norms for fuel write-off, purchase refueling receipts from third parties and receive compensation for them from their company.

Draining fuel and lubricants from work vehicles. Often there is unused fuel left in the tank of cars. It is used by unscrupulous drivers to refuel their own vehicles or to sell at a low price.

Extra flights. Without proper control of waybills, drivers can make trips at their own discretion. For example, to transport building material to a dacha or to make a couple more trips by minibus and not have to account for them.

Adjusting the odometer. With the help of special devices, drivers can adjust the meter to the required readings after a work shift. For the difference between the actual and inflated values, drivers buy “left” receipts or drain gasoline from the tank.

There are still plenty of options to deceive a company. The organization itself suffers losses mainly not from stolen fuel, but from the forced downtime of the vehicle.

How to measure gasoline in a tank during inventory

In cases where the chairman of the commission is temporarily unable to perform his duties for valid reasons (illness, vacation, study, etc.), by order of the head of the airline, a temporary new chairman is appointed from among the members of the inventory commission. 7.4. Members of inventory commissions for entering into the act of removal of residuals deliberately incorrect data on the actual balances of fuel and lubricants in order to conceal their shortages, waste or surpluses are subject to liability in the manner prescribed by law. 7.5. The inventory of fuels and lubricants is carried out on the first day of each month following the reporting month in the presence of the head of the fuels and lubricants warehouse or another financially responsible person. The inventory must be carried out with the full composition of the inventory commission. Fuel and lubricants in the warehouses of VT enterprises are carried out in order to compare the actual availability of each brand of fuel and lubricants, measured in units of mass on the day of inventory in tanks, process pipelines, refueling means (TZ, MZ), small containers and other containers, with accounting data on movement and storage of fuels and lubricants for the reporting period. 7.2. Inventory is carried out without fail: - within the time limits established in accordance with the “Regulations on Accounting Reports and Balance Sheets” (for oil and petroleum products - at least once a month); - in case of a change of financially responsible persons - on the day of acceptance and transfer of cases; - when establishing facts of theft, robbery, theft or abuse, as well as damage to fuel and lubricants - immediately following the establishment of such facts; - after a fire or natural disaster (flood, earthquake, etc.) - immediately after the end of the fire or natural disaster. 7.3. During the inventory, working and “dead” (Appendix 1) fuel residues are determined at actual humidity and for “dry” weight (minus operating humidity). 1.7. After the inventory, an act is drawn up in accordance with Appendix 2, in which the results of measurements and calculations are entered. The act is approved by the director of the power plant. 1.8. Fuel is taken as a “dead” residue: - in supply tanks - at a level exceeding by 20 cm the mark at which the pumps fail at the nominal hourly fuel consumption at the power plant, taking into account the flow rate in the recirculation line; - in reserve tanks - what remains after the failure of one pump-out pump at 30% supply; — in receiving tanks — at a level 10 cm higher than the mark at which one transfer pump fails at its nominal flow. 1.9. Total balance: at actual moisture content 14385.421 tons; for dry weight 14037.042 tons. Note. In columns 9 and 10, the mass of fuel is indicated as a fraction: in the numerator - at actual humidity, in the denominator - per dry mass. The measurement was carried out by the Chairman of the commission Signature Members of the commission Signature Measured parameters, operation Name of the device, GOST Characteristics of the device Additional instructions Fuel level in the tank Float level gauges with spring balancing according to GOST 13702-78 and TU 25-070374-79.

Measuring metal tape 10 and 20 m long according to GOST 7502-80 Measurement error at local reading ±4 mm. The division value is 1 mm. The use of other types of level gauges with the specified error is allowed. Sampling Samplers in accordance with GOST 13196-85 and GOST 2517-85. Portable samplers in accordance with GOST 2517-85 Provides the collection of combined samples.

Fuel and lubricants inventory report sample of a budget institution

In accordance with clause 27 of the Regulations on maintaining accounting and financial statements in the Russian Federation, approved by the Order of the Ministry of Finance of Russia dated July 29.

1998 N 34n, inventory is mandatory: - when transferring property for rent, redemption, sale, as well as when transforming a state or municipal unitary enterprise; — before drawing up annual financial statements (except for property, the inventory of which was carried out no earlier than October 1 of the reporting year).

In this case, the following error values are taken in the calculations (according to GOST 26976-86): 0.8% - for containers containing up to 100 tons, 0.5% - for containers containing 100 tons and above, as well as to determine the error when spending through the counter.

The inventory commission calculates the loss of fuel and lubricants according to the norms of natural loss (Appendix 32) and the error in measuring fuel and lubricants by meters, based on the amount of fuel and lubricants pumped through them.

How to draw up an order for an inventory

A sample order for inventory is usually required in some cases listed in paragraph.

27 of the order of the Ministry of Finance of the Russian Federation dated July 29, 1998 No. 34n, in particular:

- before drawing up the annual report;

- when appointing new financially responsible persons, including in connection with the transfer of property to third parties;

- after thefts or natural or man-made emergencies (fires, floods, explosions, etc.).

Typically, the order to begin an inspection is issued by the head of the organization, either scheduled or unscheduled. The person responsible for such an event is usually the chief accountant or another accounting employee.

A special commission is engaged in counting material assets, the members of which must be familiarized with the relevant local act upon signature.

A unified sample order for inventory (2019) can be found in the resolution of the State Statistics Committee of Russia dated August 18, 1998.

Sample fuel inventory

content and procedure for inventory of fuels and lubricants

- Fuel and lubricants issue record sheet

- Inventory report - sample 2021

- Inventory of vehicles: features of the league 2009-11-01

- Sample fuel and lubricants inventory report

- Form of inventory of fuels and lubricants Inventory of fuels and lubricants at the enterprise Data on the date of acquisition or construction of rolling stock objects not reflected in the accounting records are given in the inventory sheets.

Info Moreover

Inventory results report

The participation of the full commission and the presence of accountable persons is necessary.

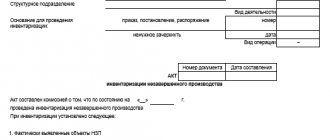

The act consists of three parts:

- the content part, where a block of information about the inventory is recorded. It lists the members of the commission, the objects of the inspection and its results;

- header with the name and code of the document, the name of the entity that executed the act, the date of preparation;

- the formal part, i.e., the signatures of the members of the inventory commission with a transcript of the signatures and an indication of positions.

The completed document is submitted for approval to the head of the institution or government agency.

Fuel and lubricants write-off act

For her appointment, the head of the enterprise issues a separate order. The commission should include employees from various departments, as well as a financially responsible person.

NOTE! The creation of a commission is required only in large organizations; small businesses can do without it: here, to write off fuel and lubricants, a simple written decision of the head of the company is sufficient. There is no standard unified, mandatory sample act for write-off of fuels and lubricants.

How is inventory carried out in a budget institution?

4 stages in 2019

An inventory is also necessary in cases where the theft and misappropriation of state property by the guilty party is suspected. An inventory is required when certain situations occur, which include:

- emergency due to a natural disaster.

- reorganization of the institution;

- preparation of annual financial and accounting statements;

- suspicions of theft or theft;

- change or dismissal of financially responsible persons;

(understand how to keep accounting records in 72 hours) purchased > 8000 books The purpose of inventory in a budgetary institution is to determine whether accounting records are being maintained correctly in the organization, whether it complies with regulatory legislation and whether illegal actions are committed by responsible persons. In accordance with with the specified goal, it is possible to identify tasks that can be solved

Inventory of fuels and lubricants

In accordance with paragraph.

An inventory of fixed assets can be carried out once every three years, and of library collections - once every five years.

In organizations located in the Far North and equivalent areas, inventory of goods, raw materials and materials can be carried out during the period of their smallest balances; - when changing financially responsible persons; - upon detection of facts of theft, abuse or damage

How to carry out an inventory without errors: we draw up reports

Since there is no fine for failure to carry out mandatory control measures, many, especially small enterprises, often do not carry them out.

Such actions directly contradict the position of the state, which obliges all business entities to carry out accounting and control of the reliability of financial statements, which is impossible without internal control measures.

Source: https://advokatssr.ru/akt-inventarizacii-gsm-obrazec-bjudzhetnogo-uchrezhdenija-12148/

Vehicle inventory sample

As for how to correctly measure the remaining fuel, it should be noted that it is quite difficult to determine the actual remaining fuel in the car’s tank with a sufficiently high degree of accuracy.

In practice, the most common cases are when measurements are made using a metal rod or measuring rods (probes).

Before conducting an inventory, pipelines must be completely filled or emptied. Control is carried out using air valves installed on elevated or lower sections of the pipeline.

When the fuel level in the tank is no more than 2000 mm, spot samples are taken from the upper and lower levels according to clause 4.3.3.

In this article, inventory is considered not only from the point of view of legal requirements, but also from the point of view of the correctness of registration and conduct of inventory at large economic entities.

There are also guidelines in this regard. In theory, it is recommended to calculate fuel consumption using a formula.

Fuel and lubricants in the warehouses of VT enterprises are carried out in order to compare the actual availability of each brand of fuel and lubricants, measured in units of mass on the day of inventory in tanks, process pipelines, refueling means (TZ, MZ), small containers and other containers, with accounting data on movement and storage of fuels and lubricants for the reporting period. 7.2.

Inventory of fuels and lubricants in containers and tanks

When conducting an inventory of fuels and lubricants received from manufacturers or suppliers in sealed containers that are not opened due to storage conditions, their actual quantity is checked and the volume or mass of fuels and lubricants in them is calculated. If necessary, the weight of sealed containers is rechecked.

To ensure reliable assessment of the volume and quantity of fuels and lubricants in tanks and containers, measuring equipment is used: meter rods, metal tape measures with weights, etc.