When to use the TORG-4 act Certificate of acceptance of goods received without a supplier’s invoice

There are cases when suppliers bring goods to an organization without accompanying documents , and it turns out that it is registered with the company in safekeeping. Sometimes papers for invoice valuables are still found and transferred later, but most often the documents never arrive, or they exist, but not in full. And then it will not be possible to establish what price to assign to the product after capitalization, and what the cost of the entire delivery will be.

The TORG-4 act is intended to help in this situation, so that a warehouse employee can take into account the supply and determine the values for storage before prices and other data are known. Form TORG-4 reflects the actual availability of delivered goods.

Basically, an act in the TORG-4 form comes in handy when delivering goods by rail or water transport , since here the absence of a package of accompanying documents has become a fairly common occurrence. The goods arrive, but the only paperwork contains instructions for its transportation.

How to work with a document

The paper is made in two copies. One is handed over to the accountant, and the second should remain with the financially responsible person.

The filling is carried out by a specially convened commission. It must include an employee under whose responsibility the goods are transferred. It is advisable to also include a representative of the supplier on the commission. After registration, the goods must remain in safekeeping until the company receives the necessary accompanying documents.

Attention! The act must be signed by all members of the commission, otherwise it will not be considered valid. The head of the company must sign “I approve”

After receiving the act, the accountant needs to check whether these goods have not been paid for earlier, whether they have the status of being in transit or not removed from warehouses. It is also checked whether the cost of these inventory items is a receivable.

Who fills out the TORG-4 act

For the competent and legal drawing up of the TORG-4 act, it is necessary to assemble a commission consisting of at least three people , the participants of which must be an employee of the enterprise financially responsible for the property he has accepted, and a representative of the supplier of these goods (for example, the delivery driver). After the meeting, all members of the commission sign an act drawn up on the basis of the supply agreement and the order on the creation of the commission, on the first page of which the director of the recipient organization puts the stamp of approval. Next, a copy of the act goes to the accountant, a second copy to the supplier, and a third to the employee who accepted the delivery.

Rules for drawing up the TORG-4 act

In order to register TORG-4, you will need to collect a commission. It must include an employee who is financially responsible for the safety of incoming goods. It is to this person that the goods will be transferred in quantity. Also, a representative of the supplier must also be included in the commission.

The act is drawn up in 2 identical copies, the 1st of which is sent to the accounting department, and the 2nd is kept by the person financially responsible for the goods. The act must be signed by all members of the commission, and the approval stamp must be affixed on the first page by the head of the recipient of the goods and materials.

If you want to file a claim for refusal of goods and termination of the contract due to the lack of documents related to the goods, a sample of such a document can be found in ConsultantPlus. Trial full access to the system can be obtained for free.

When filling out the TORG-4 act for the first time, many may have a lot of questions. For example, not everyone will immediately guess what should be indicated in the “Weight of station goods” column. It must indicate the weight of the cargo, determined first at the departure station and then at the arrival station.

The column “Packaging Condition” must be filled in without fail. If the cargo arrives in a whole package, it is marked with the words “Undamaged”; if there is something wrong with the package, then its condition is described in detail. In column 3 of the tabular part, the characteristics of the goods must be described in accordance with Art. 10 of the Law “On Protection of Consumer Rights” dated 02/07/1992 No. 2300-I .

For other nuances of goods acceptance, read the material “What must be included in the goods acceptance certificate (form)?” .

Rules for drawing up the TORG-4 act

First of all, it is necessary to clarify what kind of acts are generally drawn up when accepting deliveries without accompanying documentation:

- raw materials or supplies arrive at the warehouse , but there are no papers on them, an act is drawn up in form No. M-7 .

- When goods are supplied for further sale without delivery notes and invoices, Act No. TORG-4 .

- If there is a need, an act is also drawn up in form No. TORG-5 on the receipt of packaging , about which there is no information in the supplier’s invoices.

The TORG-4 form was not registered and published by the Ministry of Justice; therefore, organizations can develop proprietary, simpler forms. The act must indicate the actual presence of inventories, quantity and cost .

Methods for determining the price of goods received without papers:

- Look at the documents for the previous delivery of similar goods;

- Check with the supply agreement;

- Set the average market value.

The line “ Packaging Condition ” cannot be ignored. When the integrity is preserved, the mark “Intact” is placed, but if the wrapper is not intact, its appearance must be described in detail. Weight of station goods is in doubt ; the weight of goods weighed first at the point of departure and then at the point of receipt is recorded here. Read also the article: → “Form TORG-2. How to fill out a statement of discrepancy (shortage of goods)?”

Important! It is imperative to verify the quantity of goods received. The calculation must be carried out in the same units as were specified in the agreement concluded with the supplier. The accounting department, having not received any documents for the registered property, is obliged to conduct additional checks regarding the delivered goods. Property may be listed on the books as something for which payment has already been made earlier, but which for some reason was not removed from the warehouse. Or goods may be in transit, but listed as purchased. A check is made to see if the cost of these goods is included in the accounts receivable.

Procedure for filling out the TORG-4 form

The TORG-4 act is filled out as follows:

- At the top of the document you must indicate: the name and address of the recipient organization, OKPO code, information about the Supplier and the Shipper must also be entered.

- Next, indicate the number and date of the document. Nearby there is a field for signature and full name. head of the recipient organization.

After this, in the TORG-4 act you must indicate:

- place of acceptance of goods;

- available supporting documents;

- address and name of the supplier company, name of the departure station;

- the number of places indicated in the invoices;

- weight of the goods at the departure and destination stations - here you need to enter the weight of the cargo that was determined at the departure and arrival stations;

- details of the commercial act;

- packaging condition - information about the condition of the packaging must be indicated. If there is no damage on it, indicate “not damaged” in the corresponding line; if there are defects, they must be described in detail.

If there are no accompanying documents, the act indicates actual information about the goods (type, characteristics, quantity). Products are delivered at a price determined by agreement or at market value (if there is no agreement).

The next stage is to indicate information about incoming goods in a special table in the act:

- name of the product, its characteristics, code;

- consumer characteristics;

- unit of measurement;

- number of goods (places, in one place, pieces);

- weight (gross, net);

- price;

- price.

The completed document is signed by all members of the commission, including the financially responsible person. A completed sample form for LLC TORG-4 will be given below.

An important point: if no documents have been received for the posting of goods, the accounting department of the purchasing company must conduct an additional check regarding such goods. They may already be on your invoices as previously paid items. You should also check whether the cost of this product is included in the accounts receivable.

Filling out the TORG-4 form (sample)

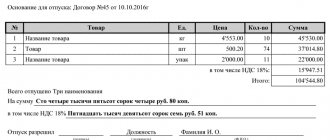

SuperAvto LLC, whose main activity is the resale of batteries and some types of household appliances, on October 10, 2015, accepted 20 boxes of 10 batteries each from its supplier Kul LLC, but there was no invoice or delivery note. Last month, the company already received similar batteries under an agreement with Kul LLC, and the price for them was 3,300 rubles apiece.

Let's enter the information received into the TORG-4 form:

Basic information about the TORG-4 form

There is a unified form TORG-4 (approved by Resolution of the State Statistics Committee of the Russian Federation dated December 25, 1998 No. 132), but it is not necessary to use it to formalize the procedure for accepting received goods and materials. Organizations are given the right to develop and use their own forms. It is important that the independently developed form indicates the actual quantity of goods received, their cost and all the necessary details.

The act is usually drawn up in 2 copies. One of them is transferred to the accounting department, and the second remains with the materially responsible storekeeper. You can make another copy for the supplier company.

The report must be drawn up on the day the products arrive at the warehouse. Form TORG-4 is drawn up on the basis of a supply agreement and an order to create a commission.

Accounting needs this document to post goods that were received without a supplier's invoice. Goods are received at accounting (if there is an agreement) or market prices.

The received products remain in secure storage in the warehouse until the missing accompanying documents are received.

How to take into account the TORG-4 act when paying taxes

Be that as it may, the property delivered under the contract, even if an accompanying package of papers was not attached to it, is considered the property of the recipient on the basis of an agreement with the supplier.

The accountant is obliged to reflect the receipt of goods on account 41 “Goods” or 10 “Materials” , and also enter data into account 60 “Settlements with suppliers and contractors” .

1) Income tax.

| The goods received were not sold, the supplier brought documents | Valuables delivered without documentation were used in production or were sold |

| The price indicated in the invoice is set; data from TORG-4 is not taken into account. | The profit from the sale of these goods is indicated, but their cost, indicated in the TORG-4 act, does not reduce the amount of income tax, since there is no evidence of the costs incurred (they could be accompanying documents), and only documented expenses are subject to deduction. If the supplier sends papers, the accountant will record the cost of goods sold in the list of costs or (if the goods were used in the production process as materials) will take into account their cost (excluding VAT) in the goods sold by submitting an updated declaration or adjusting the tax base of the current reporting period. |

2) VAT. It is not possible to take into account VAT on deliveries without invoices, because an invoice is required. But when the supplier provides it, the “input” tax can be deducted (precisely at taxation for the month when the papers were delivered). The tax office will require proof that the deduction was made late. To present the date of receipt of documents, a note in the register of incoming correspondence and a stamp on the letter (if the documents arrived by mail) are suitable.

Typical errors when drawing up a TORG-4 act

Error : 2 copies of the TORG-4 act are drawn up, one is stored in the organization, the second is given to the supplier.

Comment : It is advisable to draw up this act in triplicate, since another participant in the preparation of the act is the financially responsible person, and having him with a copy will not be superfluous.

Error : Refusal of any registration of goods for which the supplier does not require money due to the lack of documentation on them.

Comment : In this situation, the brought goods will become gratuitously given property; the accountant is obliged to take into account its market value and include it in the list of income subject to taxation. It is illegal to contribute this amount to expenses; it is possible to write off these costs by conducting an inventory and recording the resulting surplus.

Error : The accountant draws up a TORG-4 act when the enterprise receives cargo for the supply of which there was no contract, or it was delivered by mistake. Comment: This situation does not apply to goods without an invoice. Accounting will simply reflect the goods off-balance sheet in account 002, and then they will be written off from off-balance sheet accounting.

Error : Lack of signature of the supplier's representative on the TORG-4 act due to the fact that the delivery was carried out by the driver of the recipient company or a transport company.

Comment: The signature must be in any case; it is necessary to ask the forwarder TC or another uninterested person to sign the acceptance certificate.

Error : Inaction of the accountant when the materials and equipment had not yet been used, and the supplier provided documentation for their supply after the preparation of the TORG-4 act.

Comment: It will be necessary to adjust the cost of the inventory; it is impossible to leave the previously drawn up TORG-4 act.

Error : Inaction of the accountant after the supplier sent the missing documents after the execution of the TORG-4 act, when the received goods had already been sold.

Comment: The accounting employee is obliged to take into account the difference between the documented proven cost of the goods used and the price previously taken into account in the TORG-4 act. The data will be reflected in account 91 “Other income and expenses”.

How to automate work with documents and avoid filling out forms manually

Automatic filling of document forms. Save your time. Get rid of mistakes.

Connect to CLASS365 and take advantage of the full range of features:

- Automatically fill out current standard document forms

- Print documents with signature and seal image

- Create letterheads with your logo and details

- Create the best commercial offers (including using your own templates)

- Upload documents in Excel, PDF, CSV formats

- Send documents by email directly from the system

- Keeping records of goods

With CLASS365 you can not only automatically prepare documents. CLASS365 allows you to manage an entire company in one system, from any device connected to the Internet. It is easy to organize effective work with clients, partners and staff, to maintain trade, warehouse and financial records (trade management description). CLASS365 automates the entire enterprise.