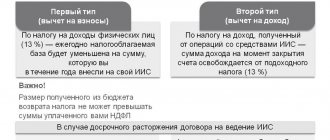

As it was before

Before the introduction of the mentioned norm in the Civil Code of the Russian Federation, VAT, the deduction of which was denied, could not be recovered from the counterparty - the courts did not recognize such a right. The arbitrators indicated: the taxpayer receives a deduction if all conditions specified by law are met and does not have the right to shift responsibility for the refusal to his business partners . The requirement to receive a tax deduction can only be presented to tax authorities who refused to recognize it, and the counterparty has nothing to do with it (resolution of the Plenum of the Supreme Arbitration Court of the Russian Federation dated July 23, 2013 No. 285213 in case A56-45502012, resolution 9AAS dated March 19, 2015 No. 09AP-605415) .

At the same time, the arbitrators pointed out that Article 15 of the Civil Code of the Russian Federation, which talks about compensation for losses, cannot be applied to tax relations related to the refund of VAT from the budget. In addition, the fact that the tax authorities refused to accept a deduction due to the actions of the counterparty does not mean that they were illegal.

As a result, additional charges of VAT, other taxes, as well as penalties and fines that the company received due to the dishonest actions of the counterparty were not recognized by the courts as losses subject to compensation by the other party to the transaction.

Procedure for paying VAT

For the beginning of the example, see the publication:

- Tax agent when purchasing services from a foreigner

The procedure and deadlines for paying VAT when performing the duties of a tax agent (TA) when purchasing services from foreigners are established in clause 4 of Art. 174 Tax Code of the Russian Federation:

“...tax payment is made by tax agents simultaneously with the payment (transfer) of funds to such taxpayers.”

Those. payment of VAT by the tax agent to the budget must be carried out simultaneously with the transfer of payment to the foreign seller, incl. when paying an advance.

The bank servicing the NA does not have the right to accept an order from him to transfer funds in favor of foreigners, if the NA has not also submitted to the bank an order to pay VAT.

Conversion of the tax base from foreign currency into rubles and calculation of the VAT amount is carried out at the rate of the Central Bank of the Russian Federation on the day the income is paid to the foreigner. VAT is paid to the budget in rubles. (Clause 5 of Article 45 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance of the Russian Federation dated January 21, 2015 N 03-07-08/1467; Letter of the Ministry of Finance of the Russian Federation dated December 5, 2016 N 03-07-08/72092).

Payment is made to the Federal Tax Service:

- at the location of the organization or individual entrepreneur (clause 3 of Article 174 of the Tax Code of the Russian Federation).

When issuing a payment order to pay VAT to the budget, code 02 “tax agent” is filled in field 101 “Status of originator”.

The completed payment order for VAT payment looks like this.

Let's take a closer look at the procedure for its formation and payment of VAT to the budget in the program.

On April 03, the Organization entered into a contract with the foreign company POSexpert LLC to provide services for organizing an exhibition in Milan.

The place of sale of services is the Russian Federation (clause 4, clause 1, article 148 of the Tax Code of the Russian Federation), therefore, the Organization acts as a tax agent for VAT (clause 2, article 161 of the Tax Code of the Russian Federation).

On June 01, the Accountant, along with the transfer of an advance payment to a foreign company, prepared a payment order for the payment of VAT to the budget as a tax agent in the amount of 63,900 rubles.

The tax was paid on the same day using a bank statement.

What changed

After the appearance of Article 431.2 in the Civil Code of the Russian Federation, the situation changed. The concept of a “representation of circumstances” introduced by her allows the party that relied on those representations to claim damages or penalties from the party that made them. And if the assurances were significant, you can demand termination of the contract.

In an example it looks like this:

The company has secured the assurance of its potential counterparty that it pays all taxes on time, maintains accounting records and records, draws up all primary documents and, in general, is an exemplary taxpayer. The counterparty assured that he has the goods, and the documents in accordance with which they were received will be provided upon request. Relying on these assurances, the taxpayer decides to enter into an agreement with this counterparty.

Let's assume the delivery was successful and the deal is closed. However, by deducting VAT from this transaction, the taxpayer receives a refusal. Having checked the counterparty’s transactions with its suppliers, inspectors determined that the transactions were formal in nature with the aim of obtaining unjustified tax benefits.

Previously, the company would not have been able to recover VAT from the seller (for reasons stated above), but now this is possible. Let's look at how exactly - using an example from judicial practice.

***

Double standards in the position set forth by the tax department, the Ministry of Finance and arbitration courts give rise to contradictions in the tax accounting of VAT when writing off receivables from a buyer who accepted the amount of VAT paid to the supplier for deduction during the period of transfer of the advance payment.

Since the situation is controversial, it is up to the taxpayers to decide whether or not to write off VAT from the amount of debt that has become hopeless.

Similar articles

- Limitation period for transport tax

- Help for INV-17 (filling sample)

- Statute of limitations for personal taxes

- Write-off of overdue accounts payable VAT posting

- Transport tax: statute of limitations

Facts of the case

The seller assured the buyer of his good faith, namely:

- in paying taxes and submitting reports;

- in accounting and preparation of “primary” documents;

- possession of the object of the transaction by right of ownership.

In addition, he promised the buyer the following:

- include the VAT paid by the buyer in tax reporting;

- provide all the necessary primary documents - invoices, delivery note, acceptance certificate and others.

In confirmation of his serious intentions, the seller promised, and this is enshrined in the contract, to provide documents that would confirm the guarantees given to him within 5 working days after receiving the corresponding request . In addition, he voluntarily accepted the obligation to compensate the buyer for losses that he incurs due to the seller’s violation of tax laws and/or his representations. In accordance with the agreement, the seller agreed to reimburse, among other things, additional VAT, penalties and fines imposed by the tax authorities on the buyer due to the actions of the seller.

When checking the legality of deducting VAT from this transaction from the buyer, the tax authorities examined transactions between the seller and his counterparties. They came to the conclusion that some of them were fictitious, that is, the products were not actually supplied, the transactions were carried out only “on paper” in order to obtain an unjustified tax benefit. As a result, the buyer was denied a VAT deduction for an amount exceeding 12 million rubles .

Having received such a decision from the Federal Tax Service, the buyer went to court. Moreover, he filed the claim not against the tax authorities, but directly against the seller himself. His claims were based on the establishments given by the seller on the basis of Article 431.2 of the Civil Code of the Russian Federation.

Payment order for VAT payment

General details

A payment order for payment of VAT by a tax agent to the budget is generated using the Payment order in the Bank and cash desk section - Bank - Payment orders.

In this case, it is necessary to correctly indicate the type of transaction Tax payment , then the document form takes the form for payment of payments to the budget system of the Russian Federation.

You can also quickly generate a payment order using the Tax Payment Assistant :

- through the section Main – Tasks – List of tasks;

- through the section Bank and cash desk – Payment orders using the Pay button – Accrued taxes and contributions.

Please pay attention to filling out the fields:

tax when performing the duties of a tax agent is not predetermined in the Taxes and Contributions directory, so you can:

- use VAT and manually adjust the Account in the document Write-off from the current account ; But at the same time, it is not recommended to change the parameters in the predefined VAT Taxes and Contributions directory !

- create a new element in the Taxes and Contributions . PDF

In our example, we will not create a separate element in the Taxes and Contributions , but will change the Account manually in the document Write-off from the current account .

- Tax – VAT , selected from the Taxes and Contributions directory. The following parameters are specified for it: the corresponding KBK code;

- text template inserted into the Payment purpose ;

- Account – 68.02 “Value added tax”, which will need to be adjusted manually in the document Debiting from current account.

Recipient details - Federal Tax Service

Since the recipient of the VAT is the tax office with which the taxpayer is registered, it is its details that must be reflected in the Payment order .

- The recipient - the Federal Tax Service, to which the tax is paid, is selected from the Counterparties directory;

- Recipient's account – bank details of the tax authority specified in the Recipient .

Currently, in the 1C program it is possible to use the 1C: Counterparty service, which allows you to automatically fill in and monitor the relevance of the details of government bodies.

If the details are no longer relevant, the 1C:Counteragent will offer to update them in the Counterparties directly from the payment order form. PDF

- Recipient's details - TIN , KPP and Recipient's name , these are the data that are used to print the payment order. If necessary, the recipient's details can be edited in the form that opens via the link.

Filling out payment details to the budget

The accountant needs to control the data that the program fills in using the link Payment details to the budget .

In this form, you need to check that the fields are filled in:

- KBK – 18210301000011000110 “Value added tax on goods (work, services) sold on the territory of the Russian Federation.” KBK is entered automatically from the Taxes and Contributions directory;

If the KBK is not known for any payment to the budget, you can use the KBK Designer by following the link to the right of the KBK .

- OKTMO code is the code of the territory in which the Organization is registered. The value is filled in automatically from the Organization directory ;

- Payer status – 02-Tax agent ;

- UIN - 0 , UIN can only be specified from information in tax notices or requests for payment of tax (penalties, fines);

- Basis of payment - TP payments of the current year , is entered when paying the tax on time;

- Tax period – quarterly payment , since the tax period for VAT is equal to a quarter;

- Year – 2018 , the year for which the tax is paid;

- Quarter – 2 , the number of the quarter for which the tax is paid;

- Document number is 0 , the document on the basis of which the payment is made is a declaration, and it does not have the Number ;

- Document date – 0 , payment is made before the date of signing the declaration, i.e. date is not determined (clause 4 of Appendix No. 2, approved by Order of the Ministry of Finance of the Russian Federation dated November 12, 2013 No. 107n).

Find out more about the details of payments to the budget .

- Purpose of payment - information for identifying the payment, filled in automatically using a template from the Taxes and Contributions directory. The field can be edited if necessary;

To transfer VAT when performing the duties of a tax agent, it is recommended to indicate:

- name of the tax;

- what the tax payment is related to;

- accrual period;

- tax payment deadline;

- payment amount.

In our example, the Payment Purpose will look like this:

- Value added tax withheld by the tax agent from the cost of services purchased from a non-resident POSexpert LLC, for the second quarter of 2021, transferred no later than 06/01/2018. (Amount 63900-00).

You can print a payment order by clicking the Payment order . PDF

Court decisions

The arbitrators found the Federal Tax Service's arguments about the fictitiousness of the transaction between the seller and its counterparty convincing. The seller could not prove that the transactions were real in nature, and also that he himself was responsible for failure to provide a tax deduction to the buyer. Given these circumstances, the courts concluded that the seller had unlawfully given the buyer an assurance of his good faith. In this case, the fact whether the buyer appealed the decision of the tax authority or not does not play any role .

As a result, the courts of all instances recognized that since the seller voluntarily gave assurances about the circumstances and knew that the buyer would rely on them, the latter rightfully demands compensation for losses in the form of VAT, the deduction of which was refused.

To receive a VAT deduction, collect a dossier on the counterparty

Inspectors deny organizations a VAT deduction, charge them more to pay, plus penalties, and issue a fine.

Inspectorate employees ignore that the transaction with the counterparty is real. Over the past year, courts have begun to support inspections. The payer must prove that he purchased goods or services from a counterparty who had the resources to execute the transaction. Read the article on how to convince judges under the new practice that the company has rightfully saved on VAT.

conclusions

So, the case A53-228582016 discussed above and the related Resolution of the Administrative Court of the North Caucasus District dated 06/05/2017 can be called a precedent, since in it the shortfall in VAT amounts was recognized for the first time as losses subject to compensation by the second party to the transaction. To take advantage of this in practice, experts recommend including in the contract provisions for assurance of the circumstances given in terms of taxes and fees . This makes it possible to receive compensation from the counterparty, and in a simplified manner:

- without challenging the decision of the Federal Tax Service in court, unless this is specifically provided for in the contract;

- without the need to establish the fact of the loss and its size (it will be indicated in the decision of the Federal Tax Service - additional assessment of taxes, fines, penalties);

- without the need to prove the guilt of the counterparty (the applicant is based on the assurances given to him that turned out to be unreliable).

When including provisions on assurance of circumstances in the contract, the following must be specified:

- the circumstances for which the assurance is given are significant for the second party to the transaction when concluding and executing the contract;

- the party that gave them understands that the counterparty will rely on them for its financial and economic activities;

In addition, as sanctions for the unreliability of these assurances, it is worthwhile to provide not a penalty, but rather compensation for losses. And then there is a chance to recover the VAT that was not accepted for deduction, along with penalties and a fine, from the other party to the transaction, who gave unfounded assurances.

Payment of VAT to the budget

After paying VAT to the budget, based on the bank statement, you need to create a document Write-off from current account transaction type Tax payment . A document can be created based on a Payment Order using the link Enter document debited from current account . PDF

The basic data will be transferred from the Payment order .

Or it can be downloaded from the Client-Bank program or directly from the bank if the 1C: DirectBank service .

It is necessary to pay attention to filling out the fields in the document:

- from – date of tax payment, according to the bank statement;

- In. Number and In. Date – number and date of the payment order;

- Tax - VAT , selected from the Taxes and Contributions directory and affects the automatic completion of the Account account ;

- Type of liability - Tax ;

- Accounting account - 68.32 “VAT when performing the duties of a tax agent”, is set manually if Tax - VAT .

- selection of the VAT amount based on payment documents to foreign suppliers in the Reflection in accounting Add , Fill out or Selection button .

For settlements with the budget in 1C, the tax agent uses account 68.32 “VAT when performing the duties of a tax agent.”

The account has three sub-accounts:

- Counterparties;

- Treaties;

- Calculation documents.

This analytics must be completely filled out by selecting it in the document Write-off from the current account when reflecting the payment of tax to the budget. Otherwise, VAT will not be automatically deducted in the future.

Postings according to the document

The document generates the posting:

- Dt 68.32 Kt - debt to the budget for VAT decreased by the amount of payment.