Instructions for filling

The certificate for the INV-17 act is filled out as follows:

- 3rd column - information about what the debt was received for is indicated. That is, they write what type of obligations this debt is listed under - credit, reporting, products.

- 4th column - indicate the date when the debt was received. This point is very important in order to correctly calculate the statute of limitations.

- Column 7 indicates the name of the paper that confirms the debt. Such a document may be: an invoice for the goods;

- act of service rendered or work performed;

- a contract that specifies the period when the counterparty must repay its obligations;

- act of inventory of debts at the end of the reporting period.

If the limitation period was interrupted, for example, in connection with the preparation of a reconciliation act, the “reconciliation act” is written in this column and the date of its formation is indicated.

- Column 8 – indicates the date of drawing up the document that confirms the debt.

Certificate inv 17 for the inventory report sample

The table provides general data on debts, as well as supporting documents.

The basis for reference is primary accounting, which includes documents on accepted work, invoices, reconciliations, and invoices issued. It happens that several accounts serve as the basis. In this case, all numbers and dates are indicated in columns 8 and 9, although the amount for the counterparty remains total. — several payment orders for one debt Please note that the certificate does not define the final figures, since both debit and credit obligations are placed in the form.

If there are not enough rows in the table, you can increase their number by adding a row to the table. The same applies to the main act.

The certificate is a mandatory addition to the INV-17 act and serves as the basis for drawing up the inventory act itself. The certificate explains the amount of debt for each debtor and creditor, the reason for its occurrence, the date the debt arose, and its amount.

Unlike the inventory report, the certificate is drawn up in one copy and is also stored for five years.

Uncollectible accounts receivable

Accounts receivable may arise under the following circumstances:

- the borrower did not repay the loan that the organization issued to him;

- the company employee did not report on the amounts he received for reporting;

- the supplier has already received an advance payment, but has shipped the products to the buyer;

- the buyer did not pay for the goods supplied to him, services provided or work performed.

Accounts receivable in accounting must be written off in the following cases:

- after the statute of limitations has expired;

- in other cases when the debt becomes impossible to collect, for example, upon liquidation of the company.

Inventory report of receivables and payables sample

The State Statistics Committee of the Russian Federation, in Resolution No. 88 dated August 18, 1998, developed not only the form of the act itself used when reconciling obligations, but also approved the annex to it. However, neither the State Statistics Committee of Russia nor the Ministry of Finance of the Russian Federation have developed an official sample for filling out INV-17 in their Methodological Recommendations.

The first page of the document contains general information about the enterprise, its division, and also indicates the start and end of the reconciliation, its basis, the number and date of the act itself. To follow the procedure for filling out INV-17, the code of the type of activity of the enterprise should be reflected on the title page.

Filling out the form is done on a computer or with a black or blue pen.

After reflecting the specified data, information on receivables is entered into the act form.

The reverse side of the document form is intended to reflect information on relationships with creditors.

The data included in the act of inventory of settlements with buyers, sellers, debtors and creditors is certified by members of the commission.

The basis for drawing up the initial form is a certificate, which is an appendix to form No. INV-17, without which the inventory act cannot be considered issued in accordance with Russian legislation.

Information in the specified application is entered in accordance with the data of the synthetic accounting accounts of the enterprise.

We invite you to read: Article 159 of the Civil Code of the Russian Federation ➔ text and comments. Oral transactions.

Electronic requirements for payment of taxes and contributions: new referral rules

Recently, tax authorities updated forms for requests for payment of debts to the budget, incl. on insurance premiums. Now it’s time to adjust the procedure for sending such requirements through the TKS.

It is not necessary to print payslips

Employers are not required to issue paper payslips to employees. The Ministry of Labor does not prohibit sending them to employees by email.

Online cash registers in online stores

Depending on how the online store organizes payment for goods, it either needs to use cash register or not. For example, the seller will not have to issue a check if payment is made through a paying agent. A tax specialist explains the nuances of using cash register systems in online stores.

We send personal income tax to the budget from May vacation pay and benefits

May 31 is the deadline for transferring personal income tax on vacation pay and temporary disability benefits (including benefits for caring for a sick child) paid to employees in May.

The list and quantity of goods at the time of payment are unknown: how to issue a cash receipt

Statute of limitations

As a general rule, the statute of limitations is three years. However, it can be increased or decreased. The duration of this period is determined in the following order:

- for obligations for which the deadline for fulfillment is clearly established - upon completion of the deadline for fulfilling this obligation;

- for obligations for which the fulfillment period is not established - from the moment the creditor makes a demand to fulfill the obligation.

Similar articles

- Statute of limitations for personal taxes

- Inventory report of receivables and payables (sample)

- Inventory of settlements with debtors and creditors

- Transport tax: statute of limitations

How to fill out the form

Form INV-17 must be prepared by the inventory commission. The composition of this commission is determined by the head of the organization.

This document is generated in two copies. One copy remains with the commission, and the second is transferred to the chief accountant.

During the inventory of receivables and payables, it is necessary to conduct a verification analysis of transactions with funds, customers, suppliers, customers and employees.

Before you start filling out the INV-17 form, you need to create a certificate application. This help contains the following information:

- about creditors and other persons, indicating their contacts;

- reasons for debt;

- documents on which debts arose;

- date of occurrence of the debt;

- amount of debt.

The form and sample for filling out a certificate for form INV-17 can be found in the article.

After completing this certificate, you can begin filling out the act form. A sample act of inventory of receivables and payables is presented below.

The form consists of two pages. The first page displays information about accounts receivable, and the second - about accounts payable.

Filling out the first page involves providing the following information:

- name of the debtor;

- account number of accounting transactions performed with it;

- total balance for this debtor (third column);

- certified amount of debt (fourth column);

- uncertified amount of debt (fifth column);

- the amount of debt for which the statute of limitations has expired (sixth column).

If there is more than one debtor, information for each of them is filled out separately, and at the end the total is calculated.

The second page of the INV-17 settlement inventory act is filled out in the same order, only for accounts payable.

After completion of the registration, all members of the commission must put their signatures on the act.

Inventory of funds on a current account sample

Inventory of funds on a current account sample

Strict reporting forms are: receipt books, certificate forms, diplomas, various subscriptions, coupons, tickets, forms of shipping documents, etc.

The timing and procedure for conducting an inventory of the cash register and funds stored in current and other bank accounts are established by the head of the organization and are enshrined in the order on accounting policies.

The cashier bears financial responsibility for the safety of all funds and documents available at the organization's cash desk.

An inventory of cash is carried out on the basis of an order (instruction) from the head of the organization by a commission consisting of a representative of the administration, the chief accountant, and the cashier (as the financially responsible person).

Before checking the availability of cash and other valuables in the cash register, the cashier draws up a final cash report.

The Civil Code of the Russian Federation states that non-cash payments made between companies (IP) are carried out through a bank (special accounts). One of the main tasks for entrepreneurs and legal entities before submitting reports is the inventory of the current account, which begins with the following procedures:

- Verification of concluded contracts.

- Finding out which banks had open account accounts at the time of inventory.

What's the point?

An inventory of funds in a current account is organized to identify differences between the current volume of assets and liabilities of the entity, as well as the real data mentioned in the accounting registers.

Sample inventory of funds in a current account

The process involves:

- Checking the currency and current account by examining the balance of money on the account.

- Control of turnover on credit and debit accounts.

Information is taken from two documents:

- Bank statements.

- Information from accounting.

The remaining balance at the end of the period on the previous statement should be equal to the balance at the beginning of the period on the next month's statement. The result of the work carried out is an act of inventory of the current account .

But more about everything.

What is to be studied?

The start of the inspection is preceded by an order from the director, who appoints members of the commission (there should be no more than 3).

Inventory of funds on the current account sample filling

It may include any employees, except financially responsible employees.

You can read more about the inventory commission in the article.

Which banking contracts should be checked?

During the inventory, the following contracts signed by banks and legal entities should be checked:

- Agreements that provide for mutual settlements in rubles.

Such accounts are called settlement accounts. Each company can open as many of these accounts as it likes. The check is carried out on each open account in each bank. - Contracts that provide for mutual settlements with counterparties in foreign currencies. Such accounts are called foreign exchange accounts. They can be opened in both Russian and foreign banks.

All of them are subject to mandatory inventory of funds and settlements.

Important

For each document, the inventory commission determines the timeliness of crediting the transfer to the bank account. If necessary, written requests can be made to the bank or post office about the reason for the delay in crediting or transfer.

The results of the inventory of funds in transit are given in the act (inventory) reflecting the amounts by direction of transfers listed as “transfers in transit.” For each amount, the number and date of the document is indicated (receipts from banks, post offices, copies of accompanying statements for the delivery of proceeds to collectors, etc.). The results of the inventory act are verified with the analytical accounting data in account 57 and the amount reflected in line 264 of the second asset section of the balance sheet.

Accounting for funds in account 57 “Transfers in transit” is carried out in rubles and foreign currency.

Sample act of inventory of funds on a current account

Opens in a domestic bank and in a credit institution in other countries.

- Assets that relate to targeted financing.

- Settlement deposits, where the movement of funds in different amounts is recorded:

- National currency.

- Foreign banknotes.

- Funds on checkbooks.

- Bank letters of credit.

- Other forms of papers for making payments.

Algorithm of actions

Taking inventory of a current account involves performing a number of procedures:

- It is found out in which banks and in what quantity agreements for settlement and cash services have been opened, after which the terms of the agreements are reconciled.

- The legality of opening the account is checked, as well as the correctness of the choice of the payment form.

- Bank statements are being examined.

Inventory report of funds on the current account, sample filling

Receipt

By the beginning of the inventory, all expenditure and receipt documents for funds were submitted to the accounting department and all funds, various valuables and documents received under my responsibility were capitalized, and those that were withdrawn were written off as expenses. Financially responsible person:

cashier position signature transcript of signature

The act was drawn up by a commission that established the following:

1) cash _____________________________________ 31,300 rub. 00 kop. 2) stamps _____________________________________________ 250 rub. 00 kop. 3) vouchers to sanatoriums _________________________________ 40,000 rubles. 00 kop. 4) service IDs ____________________________ 200 rub. 00 kopecks.

The cashier presented partially paid payroll slips No. 9-14 (payment deadline is December 2-4) in the amount of 5,200 rubles.

Inventory report of funds on the current account sample form

If at the time of inventory there are open payrolls in the cash register (according to which wages are paid), the amounts paid on such slips are included in the inventory report and are equated to cash. The cashier calculates the amounts paid for each statement and at the end of the statement makes a note about the amount paid.

In practice, to disguise the facts of embezzlement of funds, various types of receipts are often used as accounting documents, which cannot serve as documentary evidence of the expenditure of funds, since they do not correspond to the unified form of an expense cash document and do not contain the signatures of the recipient of the money, the chief accountant and the head of the organization .

Inventory report of funds on a current account sample in 1s 8.3

For operating cash desks operating using cash register machines, a special inventory procedure has been established. Cash is subject to inventory.

The inventory commission, in the presence of a cashier-operator, takes readings from the counters of cash registers at the time of inventory. These readings, reflecting the amount of revenue, are checked against the cash register tape data for their identity.

By comparing meter readings at the beginning of the day and at the time of inventory, the daily sales revenue is determined, corresponding to the amount of money that should be in the organization's operating cash register.

At the time of inventory, the cashier-operator draws up the last report, in which he must indicate the cash register meter readings at the beginning and end of the working day, as well as the amount of revenue received for the day.

Sample act of inventory of non-cash funds on a current account

Amounts for such documents or receipts are not included in the cash balance of the cash register and are considered as a shortage (clause 27 of the Procedure for conducting cash transactions in the Russian Federation).

The chairman of the inventory commission endorses all incoming and outgoing cash orders attached to the cashier’s report, indicating “before inventory on “____” (date).” This report, compiled at the time of inventory, serves the organization’s accounting department as the basis for determining the accounting balances of funds and documents.

The cashier must give a receipt stating that by the beginning of the inventory, all incoming and outgoing documents confirming the movement of funds and documents were submitted to the accounting department or transferred to the commission, and all cash received under his responsibility was capitalized, and the cash that was withdrawn was written off as an expense.

Inventory act of funds on the current account sample filling

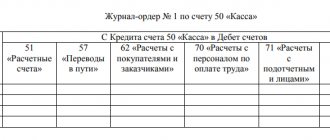

Debit 76/2 “Calculations for claims” Credit 51,52,55.

The following entry is made in accounting for the amounts of received payments:

Debit 51,52,55 Credit 76/2 “Calculations for claims.”

To document the results of an inventory of settlements with credit institutions for claims made for amounts erroneously written off (transferred) to the organization’s accounts, an act of inventory of settlements with buyers, suppliers and other debtors and creditors is used (form No. INV-17), to which a certificate is attached, reflecting information about the balances of amounts listed in subaccount 76/2 “Calculations for claims”.

Accounting for funds in transit is kept in account 57 “Transfers in transit.” An inventory of funds in this account is carried out by checking the documentary substantiation of the amounts reflected in it.

Source: https://advokat-martov.ru/inventarizatsiya-denezhnyh-sredstv-na-raschetnom-schete-obrazets

Generating inventory results in any form

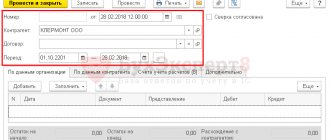

To quickly track debt and generate a custom form, you must uncheck the “Use the unified form INV-17” (Fig. 4).

Rice. 4. Free form details

In this case, on the “Parameters” tab, in addition to the date as of which the debt should be reflected, you can set the following parameters:

- The “Debt Type” detail indicates the type of debt of the counterparties that should be reflected in the report:

- accounts receivable and accounts payable;

- accounts receivable;

- creditor.

- In the “Counterparty” detail, you can specify a specific counterparty for which the debt reflected in the report will be selected. The report can also be generated for all counterparties.

- In the “Accounts for which inventory is carried out” window, a list of accounts for which inventory should be carried out is specified. The list contains subaccounts of settlements for which accounting is kept under the subaccount “Counterparties”. In order for a subaccount to participate in report generation, it must be marked in the list of accounts.

- In the “Options for possible information groupings” window, the order and types of data grouping in the report are specified. The following types of grouping are possible:

- "Account"

- "Counterparty".

Changing the grouping order is done using the arrow buttons.

To generate a report, click the “Generate” button (Fig. 5).

Rice. 5. Generating a free-form report

The report “Inventory of settlements with counterparties” displays the following information: in the “Counterparty” column - the name of the counterparty indicated in the counterparty card; in the column “Agreement” - the name and expiration date of the agreement specified in the subordinate directory “Grounds”; in the “Account” column - an accounting sub-account for which, as of the date the report is generated, there is a debt under the counterparty (agreement); in the columns “Accounts receivable”, “Accounts payable” - receivables and payables, respectively. The amounts of receivables (payables) for counterparties are given for each basis of calculation - in the context of elements of the subordinate directory “Bases” for which there is a debit (credit) balance as of the reporting date.

When specifying grouping by accounts, the data in the report is grouped by subaccounts with summing up for each subaccount.

When specifying a grouping by counterparties, the data in the report is grouped by counterparties, indicating the full name of the counterparty, and summing up the results for each counterparty.

In the report lines, it is possible to detail the data: when deciphering the columns “Counterparty”, “Agreement”, “Account”, elements of the directories are opened for viewing; When deciphering the columns “Accounts receivable” and “Accounts payable”, the “Account balance sheet” report is generated with the possibility of further detailing the data.

We also recommend using this report to identify accounting errors. For example, when grouping “by counterparties”, it is possible to identify for the same counterparty the same amounts of receivables and payables for different calculation bases or subaccounts. This indicates possible errors in entering information into the system or incorrect use of the subconto, for example, when entering transactions for debiting funds, one basis of calculation is indicated (Invoice, Agreement), and when posting goods, works, services, another (Invoice, Invoice). This error is illustrated in Figure 6.

Rice. 6. Identifying accounting errors using a free-form report.

If such errors are detected, corrections should be made to the information base. Corrections are made according to the general rules:

- if for the period in which the error was discovered, reporting has not yet been submitted, corrections are made to the documents that recorded settlements with the counterparty;

- if for the period in which the error was discovered, reporting has already been submitted, corrective entries are entered.

Where to download INV-17

The form of the unified form INV-17 was put into effect by the Decree of the State Statistics Committee of Russia “On approval of unified forms of primary accounting documentation for recording cash transactions and recording inventory results” dated August 18, 1998 No. 88. But it is not required for use since 2013. It is possible to use a self-developed form of similar content instead. However, the INV-17 form contains fields for filling in all the information that must be reflected in such a form, and therefore continues to be actively used.

The INV-17 form is available for download on our website.

The inventory report in form INV-17 is accompanied by a certificate (appendix to form INV-17), detailing (by counterparties) the data on existing debt and reflecting information on the availability of documents confirming its amount. In the INV-17 form itself, if there is a significant number of counterparties, consolidated total data on accounting accounts can be entered without breakdown by counterparties. And if there are few counterparties, then INV-17 may also contain their names.

A sample of filling out an act in form INV-17 is available for download on our website.

How is debt inventory carried out?

Before starting the inventory, employees who are financially responsible must present reconciliation reports to their counterparties. After this, the director of the company issues an order appointing an inventory commission. This body, through documentary checks, must verify the authenticity of the following information:

- accounts receivable and accounts payable;

- settlements with employees;

- settlements with accountable persons;

- settlements with control authorities;

- other payments made by the organization.

When completing a debt inventory, you must fill out a certificate (Appendix to form INV-17), the certificate reflects in detail the details of the counterparty: name, address, telephone number and “debt history”: why the debt arose, details of the document that created the debt. Automatic completion of such a certificate is not provided for in standard 1C configurations.

https://www.youtube.com/watch?v=https:accounts.google.comServiceLogin

This document provides for filling out the debt with data from the accounting register, as well as filling out forms INV-17 and INV-22.

Inventory of accounting accounts

Note 1

In order to ensure the reliability of accounting data and financial statements, all enterprises conduct an inventory of property and liabilities. The positive value of inventory is that in its process there is a check and confirmation through payment documentation of the presence and condition of the company’s property and obligations.

The inventory and the procedure for its conduct, including their number for the reporting year, dates, inventory of property and liabilities, must be determined by the head of the enterprise, excluding some cases in which the inventory is carried out without fail. Among such cases are:

- transfer of property for rent, redemption, sale, transformation of a state or municipal unitary organization;

- preparation of financial statements for the year;

- identification of facts of theft, abuse or damage to property;

- natural disasters, fires or other emergencies caused by extreme conditions;

- reorganization or liquidation of the company.

In accordance with the completeness of coverage, inventory operations can be divided into continuous and selective, and depending on the nature of the inventory, it can be mandatory or optional.

Classification of accounting accounts

Inventory of accounting accounts considers accounting accounts, which are presented in a special way of grouping, current reflection and control of changes in individual homogeneous accounting objects.

An account can be represented in the form of a two-sided table, the left side is called debit, the right side is called credit.

Note 2

Accounting has been using these concepts since its inception in Western Europe. At that time, accounting covered only trade and credit transactions, and the concepts of debit and credit were used in relation to the calculations of merchants and bankers. In the modern world, concepts are losing their former meaning, turning into technical terms.

According to the content, accounting accounts are divided into:

- active accounts, which are necessary to record property by availability, composition and location (Fig. 1);

- passive accounts reflecting property by source of education (Fig. 2).

Picture 1 . Active account

If we consider active accounts, then a positive or zero balance can only be in debit.

Figure 2 . Passive account

Passive accounts have a positive balance or a balance equal to zero, which can only be on a loan.

In addition to asset and liability accounts, accounting practice widely uses active-passive accounts, which have features of both accounts. This type of account is used more often to record certain calculations (Table 1).

Table 1 . Active-passive account

| Debit | Credit |

| Accounts receivable (beginning balance) | Accounts payable (beginning balance) |

| Debit | Credit |

| Turnover - debt repayment, increase in receivables | Turnover - increase in debt to creditors, decrease in receivables |

| Accounts receivable (total balance) | Accounts payable (total balance) |

Active-passive accounts have both debit and credit balances.

There is also a special group of accounts outside the balance sheet (off-balance sheet). They are used when accounting for values that do not belong to the company or require special control. Such objects include fixed assets that the enterprise has under the current lease; inventory items in safekeeping; strict reporting forms, etc.

Help and Application

The State Statistics Committee of the Russian Federation, in Resolution No. 88 dated August 18, 1998, indicated the use of act No. INV-17 for proper registration of inventory results:

- accounts payable and receivable;

- settlements with buyers and sellers;

- other obligations.

The specified form is filled out in two copies. After they are signed by all members of the commission:

- one of the acts remains with the inspection workers;

- the second form is transferred to the accounting department of the enterprise.

https://www.youtube.com/watch?v=ytpolicyandsafetyru

The basis for drawing up the act is a certificate for INV-17, the attachment of which to the form is a necessary condition for the correct registration of the results of the inventory of receivables and payables.

When filling out this certificate, you should indicate:

- name of the enterprise and its structural division;

- details of the act to which it is attached;

- date of debt reconciliation with creditors and debtors;

- Fill out the table according to the column names.

Correctly filling out this certificate on a computer or by hand (using blue or black ink) is a prerequisite for the proper verification and registration of inventory results. Ignoring this document will inevitably lead to the invalidity of the reconciliation of accounts payable and receivable with the accounting data of the enterprise.

Sample of filling out a certificate for form INV-17

Before preparing financial statements, companies must make an inventory of their liabilities and assets. This helps to correctly fill out the balance sheet, as well as timely identify discrepancies between the accounting data and the information of counterparties.

Inventory must also be carried out in the following cases:

- change of persons carrying the mat. responsibility;

- Liquidation of company;

- theft in an organization.

In addition to the act itself, when reconciling settlements with suppliers and counterparties, a certificate is attached, on the basis of which the INV-17 act is subsequently drawn up.

In turn, the basis for drawing up the certificate is the data from the financial statements, which must contain all information about the debt and the amount.

After this, the debt is divided into three groups: confirmed by the debtor, unconfirmed by the debtor and expired debt. After filling out the certificate, the received accounting data is detailed in the INV-17 form.

However, there are no special legal requirements for filling out the INV-17 certificate. Those who are faced with the need to carry out this procedure for the first time will find the instructions for filling out the certificate for the INV-17 act useful.

Column 4 contains information about the exact date when the debt arose. This column must be filled out especially carefully due to the fact that the statute of limitations is calculated on the basis of this date, and when going to court, it may be impossible to collect the debt from the debtor.

In graphene 7, you must write down a document that confirms the existence of the debt. As such a document you can use:

- waybill;

- act on the provision of services or performance of work;

- an agreement that specifies the deadline for the counterparty to fulfill its obligations under the agreement;

- the amount of debt for the reporting period.

If situations arise where the statute of limitations had to be interrupted because a reconciliation act was being generated, it is necessary to indicate the reconciliation act as a supporting document and indicate the exact date when it was created.

https://www.youtube.com/watch?v=ytpressru

Column 8 contains information about the date of generation of the document confirming the debt.