Why compare income based on profit and VAT?

The answer is very simple - the tax office does this, which means we, accountants, need to do this too =)

Tax officials compare VAT and profit returns to find income that the company forgot to charge with VAT.

In the simplest case (if we are analyzing the 1st quarter of the reporting period and we have no accounting difficulties), to reconcile we just need to carefully look at both declarations and check lines 010 + 020 (Sheet 02) in Profit and line 010 (Section 3) in VAT returns.

And this is quite easy to do.

Difficulties begin if we need to compare indicators over 9 months or over a year. Profit is easy to calculate - it is indicated in the declarations on an accrual basis. But with VAT there is already a problem - reporting is quarterly, which means we need to take all declarations from the beginning of the year and summarize their indicators.

Now let’s add some more truths of life:

- refunds to suppliers (increase the VAT base, but no profit)

- customer returns (reduce income in profit, but not in VAT)

- VAT-free income

- different periods of income recognition for export sales

All this leads to the need to understand the discrepancies between VAT and profit

- becomes a very difficult task, requiring a deep dive into accounting, drawing up additional tables and additional checks.

Specialists have a lot of experience in finding VAT and profit differences using Excel tables and “working weekends,” but we are tired of searching everything by hand. We used all our knowledge and experience and developed a special report that allows you to automatically check the convergence of the VAT and Profit base

and take into account common discrepancies. And we are ready to share our findings.

Important: in addition to the adequate reasons for the differences between VAT and Profit, we often find accounting errors that distort the tax base. Our report removes all “resolved” discrepancies and allows you to focus on the actual errors.

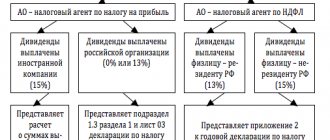

Personal income tax burden

The calculation of the tax burden for personal income tax is determined by the formula:

Tax burden for personal income tax = Calculated personal income tax / Total amount of income from this activity * 100%.

The tax office will require an explanation if the resulting value is too low. For legal entities, an important indicator here will be the dynamics of payments; the Federal Tax Service will pay close attention to the company if:

- Personal income tax amounts decreased relative to previous periods by more than 10% based on the results of the quarter or year.

- Based on the amount of personal income tax, it was revealed that the company pays wages below the regional average.

- The amounts of insurance premiums are also reviewed to see if they have decreased with the same number of employees.

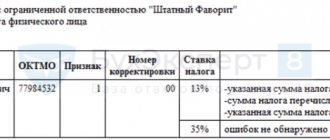

Concept of a report comparing VAT and Income Tax indicators

- During the analysis, we compare data from regulated reports. Moreover, the report includes the latest adjustment declarations

- Program credentials are used to calculate allowed differences

- Indicators are calculated in full rubles

- “Allowed differences” are divided into two groups:

- Carryover differences (differences in the moment of income recognition)

- Constant differences

is zero.

Examples of using the report

Video review of the development

Let's consider the work of the report using the example of one year of the organization's work

1st quarter

In the 1st quarter we see the following situation:

- adjustment declarations are used for analysis (k/1)

- in this quarter, the VAT rate of 0% was confirmed for the amount of 10,878,485 rubles (for income tax purposes, these sales were taken into account in previous quarters)

- For sales in the amount of 3,730,529 rubles, the 0% rate has not yet been confirmed

Result: there are no erroneous differences, all differences are “allowed”

2nd quarter

This quarter we see a similar situation with differences, but the indicators are already considered both quarterly and cumulatively - to facilitate reconciliation. Please note that indicators that are obtained by calculation are highlighted in gray (you will not find these figures in the declarations).

3rd quarter

In the 3rd quarter we see a difference of 33,700 rubles. If you analyze all the data, you can find the reason for the difference - the presence of non-operating income not subject to VAT.

Setting up other income not subject to VAT

There is a special setting in the VAT and Profit reconciliation report that allows you to specify a list of non-operating expenses that should not be subject to VAT and that must be included in the “allowed” differences.

If an item of other income is added to this list, then the detail “Not subject to VAT” is filled in (it can also be set in the directory itself).

This allows you to build SALT for the 91st account, grouped by VAT taxability. By default, this list is filled with unambiguously “allowed” differences. The user can independently supplement the list. In this case, we will add the article “Insurance compensation (MTPL)” to the exceptions.

As a result, we will receive a report in which there are no unresolved differences

4th quarter

In the 4th quarter we see that a whole range of “allowed” differences have been taken into account:

- unconfirmed export 0%

- returns of goods to the supplier

- returns of goods from customers

- non-operating income not subject to VAT

And still we get an unresolved difference. In this case, it means the presence of an accounting error in the VAT or Profit return. Additional data analysis (outside the scope of this report) is required to identify the error. But our primary recommendation is to update the closing of months, the formation of a sales book and refill tax returns.

The cost of development is 6,000 rubles.

One year of free support (if the configuration is updated or the form changes, we will fix everything)

A year of additional support costs RUB 3,000.

Other information: The report was tested on versions: 1C: Enterprise Accounting 3.0.53 and higher

If necessary, we can provide paid consultations on identifying the differences between income tax and VAT.

If it is necessary to take into account individual nuances and modifications to work in changed configurations, the work is paid by the hour.

What is the tax burden

This term refers to the share of revenue paid by the enterprise to the budget. Often, based on the value of this coefficient, the tax office understands whether the business is being conducted fairly. The Federal Tax Service calculates average load values for each type of activity and publishes tables with coefficients.

Banks also use the value of the tax burden when they decide to issue a loan or service a company. If the amount of payments to the budget from the total turnover of the account is less than that established by law, then the business is considered dishonest.

Safe tax burden values in 2021

These values change every year and are published by the Federal Tax Service in accordance with statistical reporting data. Below is a table with the coefficients that tax authorities use in 2020.

| Type of economic activity (according to OKVED-2) | 2019 | |

| The tax burden, % | For reference: fiscal burden for the North, % | |

| TOTAL | 11,2 | 3,5 |

| Agriculture, forestry, hunting, fishing, fish farming - total | 4,5 | 5,2 |

| crop and livestock farming, hunting and provision of related services in these areas | 3,4 | 4,8 |

| forestry and logging | 8,7 | 7,6 |

| fishing, fish farming | 10,1 | 6,0 |

| Mining - total | 41,4 | 1,7 |

| extraction of fuel and energy minerals - total | 50,9 | 1,1 |

| extraction of mineral resources, except fuel and energy | 11,4 | 3,6 |

| Manufacturing industries – total | 7,6 | 2,1 |

| production of food, beverages, tobacco products | 20,9 | 2,1 |

| production of textiles, clothing | 8,0 | 4,3 |

| production of leather and leather products | 10,0 | 5,3 |

| wood processing and production of wood and cork products, except furniture, production of straw products and wicker materials | 1,6 | 3,6 |

| production of paper and paper products | 4,8 | 1,9 |

| printing and copying activities | 8,9 | 3,8 |

| production of coke and petroleum products | 4,2 | 0,2 |

| production of chemicals and chemical products | 3,0 | 2,3 |

| production of medicines and materials used for medical purposes | 6,9 | 3,1 |

| production of rubber and plastic products | 6,9 | 2,8 |

| production of other non-metallic mineral products | 9,3 | 3,4 |

| metallurgical production and production of finished metal products, except machinery and equipment | 4,0 | 2,1 |

| production of machinery and equipment, not included in other groups | 9,9 | 4,4 |

| production of computers, electronic and optical products | 11,7 | 5,1 |

| production of electrical equipment | 7,5 | 3,3 |

| production of other vehicles and equipment | 6,5 | 4,7 |

| production of motor vehicles, trailers and semi-trailers | 5,8 | 1,5 |

| Providing electricity, gas and steam; air conditioning - total | 7,1 | 2,4 |

| generation, transmission and distribution of electricity | 8,3 | 2,1 |

| production and distribution of gaseous fuels | 1,3 | 1,7 |

| production, transmission and distribution of steam and hot water; air conditioning | 7,1 | 10,0 |

If an enterprise is engaged in several types of activities, then you need to focus on the tax burden for the one indicated as the main one. In the event that a company has moved to work in another industry, it is necessary to promptly enter data about this into the Unified State Register of Legal Entities. If the activity of an enterprise does not fall under any of the types indicated in the list above, then you need to look for values for the closest one in your industry.

Updates

We provide new development versions free of charge within a year after purchase.

One year of additional support - 3,000 rubles. Attention, we do not guarantee the functionality of the development for which the additional support period has not been paid for.

The current version of the development can be obtained by writing to us by email. Managers will check whether you have access to support, send a new version or send an invoice.

Version 1.2

- interface fixes

Version 1.3

- the report has been prepared for use in cloud versions

- Fixed errors in report generation for users with limited rights

Version 1.4

- New indicators have been added to the allowed differences: Unconfirmed sales 0% (in case of additional VAT charges)

- Sales according to 90.01.1 without VAT

- Implementation according to 90.02.2 UTII and Patent

- the year-end closing mechanism was taken into account when analyzing accounts 90 and 91

- fixed determination of differences in returns to suppliers and from customers

Version 1.5

- Adjustments to sales taken into account (downward)

- Adjustments to sales downwards from sales from previous years have been taken into account

Version 1.6

- Added control for discrepancies in revenue and other income according to accounting data (90.01 and 91.01) and according to the profit declaration data

Version 1.7

- The 2021 analysis shows a VAT rate of 20%

- Corrected the indicator “Confirmed export sales” (Section 4 line 020) in the 2021 reports

- The difference of 1 ruble between SALT and the Profit Declaration is not controlled

Version 1.8

- We added revenue data for other operations (Appendix No. 3 to Sheet 02) to the analysis of the convergence of accounting and reporting data - this is usually the sale of fixed assets or intangible assets

- Added the ability to open regulated reports via hyperlink (in one click you can open everything you need for reconciliation)

- Added a description of the “Difference” column - the main reasons and necessary actions

Version 1.9

- This release adds checking for discrepancies in gratuitous transfer transactions

Version 1.10

- Added a new indicator “Shipment without transfer of ownership”

- Identified errors have been corrected

Version 1.11

- Added a new indicator “Sales of shipped goods” (actual transfer of ownership)

- We have finalized indicator 040 of section 4 of the VAT return. Now all the lines of this column are summed up

Version 1.12

We decided to make development even more convenient and transferred the functionality to the Extension. This will allow:

- more convenient to open development

- It’s more convenient to set up other income and expense items

- improve checking the compatibility of development with future versions of 1C:Accounting

But we haven’t forgotten about the development of functionality:

- We show differences only if there is something to show

- simplified setting up the item of other income from expenses (the “Not subject to VAT” flag)

- added a certificate for the indicator “Sales at a rate of 0%” (to open you need to click the “?” sign)

Version 1.13

- The extension is adapted to version 1C: Accounting 3.0.75

Version 1.14

The extension has been adapted to the new form of the regulated Profit report from the 4th quarter of 2021 (1C: Accounting 3.0.75)

Version 1.15

- added analysis of returns to the supplier (if it is made on the basis of an adjustment invoice)

- identified errors have been fixed

Version 1.16

- the long-awaited decoding of discrepancy indicators

- other income “Return of goods sold in the previous tax period” has been added to the default exceptions

Version 1.17

- Fixed minor inconvenience of adding other income

- Improved determination of the required declaration in the presence of separate divisions

Version 1.19

In this version, we have updated the declaration forms, corrected several important details and made working with the report even more convenient:

1. The report has been updated for the Profit and VAT declaration forms from the 4th quarter of 2021, the diagnosis of filling errors has been improved due to the update of reporting forms 2. The verification of amounts in the Profit declaration and in accounting data for complex transactions has been corrected 3. The line “ has been highlighted in the analysis Proceeds from the sale of other property" 4. Simplified the work with setting the flag "Not subject to VAT" for other income. After setting the flag, you no longer need to re-open the discrepancy analysis; the new settings will be accepted automatically. 5. Added the ability to quickly open OSV for 91.01 from the report settings form

How to provide explanations when there is a discrepancy between the tax base for profit and VAT

Andrey Snagovsky

December 28, 2021 397

0

Accounting and HR

Submitting reports to regulatory authorities is, of course, a responsible matter and requires careful preliminary checks. Therefore, checking the compliance of indicators in primary documents and reporting declarations is an important task. However, even the most thorough inspection does not guarantee that the inspectorate will not have questions for the taxpayer and will not require appropriate explanations. For example, the Federal Tax Service may request clarification on the discrepancy between the tax base for profit and VAT.

Taxpayers become aware of the existence of a discrepancy after receiving requests from tax authorities. According to paragraph 3 of Art. 88 of the Tax Code of the Russian Federation, the answer must be given within five days, otherwise the taxpayer faces a fine of 5 thousand rubles. If you do not respond to the inspection requirements again within a year, the fine will be 20 thousand rubles.

Let's look at the most common examples of such situations and tell you how to respond to tax requirements.

The organization receives interest on a cash loan

This does not affect the VAT tax base, but the very fact of receipt during the period of interest accrual is reflected in the VAT return. At the same time, amounts received from interest appear in the tax base for profits on the last day of each month.

What to answer in the explanation.

Please inform that there is no error in the declaration. Since non-operating income was reflected in profit (line 100 of Appendix 1 to Sheet 02), discrepancies arose. The amount of interest was not included in the VAT tax base in accordance with clause 3 of Art. 149 and paragraph 1 of Art. 146 of the Tax Code of the Russian Federation.

Use account statements 90.01 “Revenue” and 91.01 “Other income” as supporting documents.

Sales of goods, works and services exempt from taxation

Let's say an organization is engaged in the trade of medical goods, some of which are not subject to VAT. Their implementation does not affect the tax base, but it is reflected in the VAT return. Transactions on the sale of such goods are reflected in the income tax return after ownership passes from the seller to the buyer.

What to answer in the explanation.

There is no error in the declaration. It is necessary to clarify that the company sold medical products for a specific amount (its amount must be indicated in the explanation), which are not subject to value added tax and are reflected in section 7 of the VAT return. Income from the sale of these goods, according to clause 3 of Art. 271 of the Tax Code of the Russian Federation, was reflected in the income tax return (lines 010, 011, 012 of the appendix to sheet 02) after the transfer of ownership of the goods to the buyer.

For confirmation, you can use the purchase and sale agreement and registration certificates of medical devices.

Export operations

The accountant reflects export transactions in the VAT return in the period in which the entire package of documents necessary to confirm these transactions is collected. In profit reporting, the tax base appears at the moment when ownership passes from the seller to the buyer.

What to answer in the explanation.

Report that the company sold goods for export in a certain period for a specific amount (the sales period and the amount of revenue will need to be indicated). In accordance with paragraph 3 of Art. 271 of the Tax Code of the Russian Federation, operations for the export of goods were reflected in the income tax return (lines 010, 011, 012 of the appendix to sheet 02) after the transfer of ownership to the buyer. According to paragraph 9 of Art. 167 of the Tax Code of the Russian Federation, this operation was reflected in the VAT return after the complete package of documents was collected (here you will need to clarify the date of collection of the package of documents).

For confirmation, a purchase and sale agreement with specifications, as well as a bill of lading or an acceptance certificate are used.

The organization receives dividends and interest on deposits

When determining the base for calculating value added tax, dividends are not included. In addition, they are not reflected in the VAT return. The taxpayer reflects information about dividends in the tax return after receiving the money.

What to answer in the explanation. Report that your company received dividends (indicate the date of receipt and the amount of the dividends), and information about this was reflected in the VAT return (line 100 of Appendix 1 to Sheet 02) in accordance with paragraph 8 of Art. 250, paragraph 1, art. 271 Tax Code of the Russian Federation. Please clarify that on the basis of paragraph 1 of Art. 39, pp. 1 clause 1 art. 146 of the Tax Code of the Russian Federation, dividends are not included in the calculation of the tax base for VAT and are not reflected in the declaration.

As supporting documents, use the decision to pay dividends, payment orders or cash documents for the payment of dividends.

There was a positive difference in the exchange rate

Let’s say an organization has entered into a supply agreement with a foreign partner with partial payment. The amount of VAT was charged on the foreign currency advance at the rate of the Central Bank of Russia on the date of shipment of the goods. When the subsequent payment was received, a positive exchange rate difference arose.

Positive exchange rate differences are not calculated or reflected in the value added tax return. But at the time of revaluation of liabilities, it is taken into account when the tax base for profits is formed.

What to answer in the explanation.

Please inform that there are no errors in the declaration. Please specify that the company has entered into an agreement for the supply of goods to a foreign partner with partial payment. The amount of value added tax was charged on the currency advance at the rate of the Central Bank of the Russian Federation, which was in effect at the time of shipment. In accordance with paragraph 8 of Art. 271 and paragraph 10 of Art. 272 of the Tax Code of the Russian Federation, the positive exchange rate difference that arose upon receipt of subsequent payment was included in non-operating income for income tax, and was also reflected in the declaration (line 100 of Appendix 1 to Sheet 2). The difference between the tax base for income tax and VAT arose because the amounts of exchange rate differences are not reflected in the VAT return.

To confirm, use the following statements:

- on account 62 for subaccounts “Settlements for advances received” and “Settlements for shipped goods”;

- under account 91.1 “Other income”.

Free transfer of goods, works, services or property rights

If a company transfers goods or provides services free of charge, the VAT tax base arises after these actions are completed. Since there was no tax base for the profit, the taxpayer does not reflect it in the declaration.

What to answer in the explanation.

Please inform that there are no errors in the declaration. Specify that your company transferred the goods to third parties free of charge (indicate the date of transfer and the amount of the cost of the goods). According to paragraph 1 of paragraph 1 of Art. 146 of the Tax Code of the Russian Federation, this operation was reflected in the VAT return in the corresponding line of section 3 (010, 020 or 030 - depending on the tax rate) for the corresponding period. The tax base for profit did not arise and therefore was not reflected in the declaration (Article 249 and Article 250 of the Tax Code of the Russian Federation).

As supporting documents, use an extract from account 91.02 “Other expenses”, as well as an agreement according to which one party is obliged to provide the other party with something without receiving payment or other counter-provision.

Free receipt of goods, works or services

The tax base for VAT does not arise if the company receives goods free of charge from the counterparty, and therefore is not reflected by the taxpayer in the declaration. In an income tax return, income arises after the company receives the goods.

What to answer in the explanation.

Please inform that there are no errors in the declaration. Please specify that your company received the goods free of charge (you must indicate the period of receipt and the amount of the total cost of the goods), therefore this operation was reflected in the profit declaration (lines 100, 103 of Appendix 1 to sheet 02) in accordance with clause 8 of Art. 250 and pp. 1 clause 4 art. 271 Tax Code of the Russian Federation. Since the tax base for VAT did not arise, it was not reflected in the declaration.

To confirm, use account statement 98.2 “Gratuitous receipts”.

Carrying out construction and installation work for your own needs

Let's say a company is building a warehouse for itself. According to paragraphs. 3 p. 1 art. 146 of the Tax Code of the Russian Federation, income in this case arises when the tax base for VAT is formed. It is reflected in the declaration at the end of each quarter. In this case, the income does not fall into the income tax base and is not reflected in the declaration.

What to answer in the explanation.

Please inform that there are no errors in the declaration. Specify that your company is engaged in construction and installation work for its own consumption (indicate here the period in which the work took place). Based on paragraphs. 3 p. 1 art. 146 of the Tax Code of the Russian Federation, construction operations were reflected in the VAT return (line 060 of section 3) based on the results of each quarter. Since the tax base for profit did not arise, it was not reflected in the profit declaration.

Use account statements as supporting documents:

- 01 “Fixed assets”;

- 08.03 “Construction of fixed assets”.

Based on the results of the inventory, the surplus was capitalized

Identified surpluses are not included in the VAT tax base. The taxpayer does not reflect them in the declaration. In the income tax return, identified surpluses arise at the time the inventory is completed.

What to answer in the explanation.

Please inform that there are no errors in the declaration. Surplus inventory items that were identified as a result of the inventory were included in non-operating income (clause 20 of Article 250 of the Tax Code of the Russian Federation) and reflected in the income tax return (line 104 of Appendix 1 to Sheet 02). Based on paragraph 1 of Art. 146 of the Tax Code of the Russian Federation, at the time of capitalization of the surplus object of taxation, VAT did not arise.

To confirm, use the act of the inventory commission and an extract from account 91 “Other income and expenses.”

Write-off of accounts payable after expiration of the statute of limitations

If a company has written off a debt to a counterparty after the expiration of the statute of limitations, the amount of the write-off does not require restoration in the value added tax return. It also does not fall into the tax base, but it must be included in non-operating income for income tax.

What to answer in the explanation.

Please inform that there are no errors in the declaration. The discrepancies arose due to non-operating income in the form of the amount of overdue accounts payable written off due to the expiration of the statute of limitations. This income was reflected in the income tax return (line 100 of Appendix 1 to Sheet 02). In accordance with paragraph 3 of Art. 149 and paragraph 1 of Art. 146 of the Tax Code of the Russian Federation, this amount was included in the VAT tax base.

Use the following account statements as supporting documents:

- 90.01 “Revenue”

- 91.01 “Other income”.

Sales of recyclable materials by the VAT payer

Let’s say I sold ferrous metal to an address. Both organizations are VAT payers. Since Stroitel will use scrap metal in activities that are subject to VAT, it is this company that must charge the tax - as a tax agent.

will issue an invoice to the address with the note “VAT is calculated by the tax agent.” The buyer of scrap metal must reflect in the declaration all transactions that are associated with the calculation and deduction of VAT at the time of shipment of the goods. This operation is included in the seller’s VAT tax base. However, he is obliged to reflect it in his income tax return.

What to answer in the explanation.

Please report that your company sold recyclable materials using an invoice marked “VAT is calculated by the tax agent.” This operation is not reflected in the VAT return and, according to clause 8 of Art. 161 of the Tax Code of the Russian Federation, does not participate in the calculation of the tax base. Based on clause 3 of Art. 271 of the Tax Code of the Russian Federation, the sale of scrap metal is reflected in the income tax return (lines 010, 011, 012, 014 of Appendix 1 to Sheet 2).

As a supporting document, use an invoice marked “VAT is calculated by the tax agent.”

Important:

There are exceptions in which VAT is calculated by the seller and not the buyer. This happens if:

- in the contract and primary documents it is indicated about;

- the seller no longer has the right to apply the simplified tax system or UTII;

- the seller is no longer exempt from VAT;

- the VAT payer sold the goods to an individual without individual entrepreneur status;

- recyclable materials were sold by the VAT payer for export.

Return of goods

Let's imagine that a company discovers a defect in a purchased product. In this case, she transfers to the seller a statement of defects in the goods, as well as a return receipt. In this case, the seller issues an invoice for the reduction and registers this document in the purchase book.

The tax base in the VAT return is reflected by the buyer through the registration of an entry in the sales book. Since money returned for defective goods is not income, the transaction is not included in the income tax return.

What to answer in the explanation.

Please inform that there are no errors in the declaration. The company purchased a product that was found to be defective and returned it to the supplier. Funds returned by the supplier are not included in income. The cost of the item to be returned is not included in the costs. At the same time, value added tax was assessed on it.

The discrepancies arose due to the fact that there was no income for calculating income tax, and VAT was accrued on lines 010 (020) and columns 3 and 5 of section 3 of the value added tax declaration. After returning the goods, the contract between the company and the supplier was terminated, and a new contract was not concluded.

To confirm, use the statement of defects in the goods, the return delivery note and the adjustment invoice.

Important:

If the goods are returned to the supplier at the initiative of the company, when calculating income tax, it has taxable income, from which the cost of the returned goods can be deducted. Value added tax is charged on the proceeds from the return. Refunds are made at supplier prices, so for purposes of calculating income tax and VAT, the revenue will be the same.

Transfer of a fine, penalty or penalty from the buyer

If goods supplied under a contract are subject to VAT, then if the buyer violates his obligations, the supplier receives a penalty, fine or penalty from him. The money received by the company from the counterparty for violating the terms of the contract is not related to payment for the goods, and therefore is not subject to VAT. The payment of the penalty is not reflected in the value added tax return, but the amount received is included in the tax base for calculating income tax and is reflected in the return for this tax.

What to answer in the explanation.

Please inform that there is no error in the declaration. Based on clause 3 of Art. 250 and pp. 4 paragraphs 1 art. 271 of the Tax Code of the Russian Federation, the amount of the penalty received by the company from the counterparty for violating the terms of the contract was taken into account as part of non-operating income and reflected in the income tax return (line 100 of Appendix 1 to sheet 02. According to clarifications of the Ministry of Finance in letter dated March 4, 2013 No. 03 -07-15/6333, this transaction is not subject to VAT.

As supporting documents, use the supply agreement with the calculation of the penalty and an extract from account 91.01 “Other income”.

Restoring a previously created reserve

Let’s assume that the company’s reserve for doubtful debts at the end of the reporting period was less than the amount of the reserve balance. The difference in this case is included in non-operating income and is reflected in the income tax return (line 100 of Appendix 1 to Sheet 2). Restoration of a previously created reserve is not included in the VAT tax base and is not reflected in the declaration.

What to answer in the explanation. Please inform that there are no errors in the declaration. The amount of the reserve that was calculated as of the reporting date is less than the amount of the balance of the reserve from the previous reporting period. Based on clause 7 of Art. 250 and pp. 5 paragraph 4 art. 271 of the Tax Code of the Russian Federation, the difference is included in non-operating income on line 100 of Appendix 1 to sheet 02 of the income tax return. Restoration of a previously created reserve is not included in the VAT tax base and is not reflected in the declaration.

To confirm, use the statement of account 91 “Other income and expenses.”

Andrey Snagovsky

December 28, 2021 397

0

Was the article helpful?

100% of readers find the article useful

Thanks for your feedback!

Comments for the site

Cackl e

Products by direction

1C-EDO

—> Service for organizing document flow with your counterparties from the 1C program

Astral.EDO

—> New online service for organizing electronic document management with counterparties