Requirements for intangible assets

In order for property to be classified as intangible assets, it must meet a number of criteria:

- have properties that are inherent in fixed assets (operation for at least a year in order to make a profit, the ability to isolate an object and determine its market value);

- have no physical form.

Equally important is the existence of rights to property - the company must, if necessary, confirm this right with relevant documents.

Based on the above, the following objects can be classified as intangible assets:

- literary, musical and other works;

- all kinds of inventions and prototypes;

- computer software;

- trademarks and service marks;

- Database;

- other objects listed in the list of PBU 14/2007.

Business reputation is also part of the intangible assets. It is defined as the difference between the purchase price and the book value of the company, which means it can be either positive or negative.

The following cannot be classified as intangible assets:

- unregistered intangible assets, utility models and patents;

- scientific work for which the results are negative, unfinished or improperly prepared;

- financial objects, the purpose of acquisition of which is to obtain profit from transfer to third parties for use.

Goods on commission - keeping records with the commission agent and the consignor

Anastasia Gerasimova, auditor, methodologist at FinExpertiza LLC

The use of a commission agreement in trade relations is currently very common, since it gives the parties many advantages compared to classical sales and purchases, in particular, they allow the commission agent to enter into trade at low costs, the principal to expand markets for their products, and also significantly optimize the costs of both.

Commission agreements have many nuances and different options for building relationships, therefore, despite their widespread use, commission relationships never cease to raise questions among accountants.

This article will examine in detail one of the aspects of the commission agreement - accounting for goods on commission, in particular, the procedure for reflecting transactions in the accounting records of the principal and the commission agent, document flow, as well as some features of the taxation of these transactions.

The regulation of relations under a commission agreement is carried out by the Civil Code of the Russian Federation, in particular, Chapter 51 “Commission” is devoted to this.

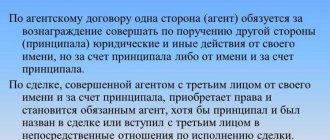

In accordance with paragraph 1 of Art. 990 of the Civil Code of the Russian Federation, under a commission agreement, one party (the commission agent) undertakes, on behalf of the other party (the principal), for a fee, to carry out one or more transactions on its own behalf, but at the expense of the principal.

The commission agent, on his own behalf, enters into contracts with third parties, acquires rights and obligations under a transaction concluded with a third party, even if the principal was named in the transaction or entered into direct relations with the third party for its execution. Thus, all documents related to the transaction are drawn up on behalf of the commission agent, and he is not obliged to indicate that he is acting on the instructions of the principal.

The legal status of things that are the subject of the commission is enshrined in Art. 996 of the Civil Code of the Russian Federation, which states that things received by the commission agent from the principal or acquired by the commission agent at the expense of the principal are the property of the latter.

From the beginning to the end of the fulfillment of his obligations, the commission agent disposes of the goods, but is not its owner.

Commission agreements, according to which the principal transfers the right to the commission agent to dispose of his property, can be of two types:

1. A commission agreement for the sale of goods, upon conclusion of which the principal instructs the commission agent to sell his goods on agreed terms for a certain remuneration.

2. Commission agreement for the purchase of goods, in which the commission agent undertakes, for a fee, to purchase goods for the principal on the agreed terms.

When selling goods, ownership of the goods passes from the principal directly to the buyer, and when purchasing, from the seller to the principal.

The procedure for recording business transactions under a commission agreement in accounting is largely determined by the provisions of the agreement concluded between the parties, for example, whether or not the commission agent participates in the settlements between the principal and the buyer (seller).

Let us consider the accounting of transactions under a commission agreement in the context of both types of agreements. And since the parties to the commission agreement are the principal and the commission agent, therefore, the accounting of transactions should be considered for each of the parties.

Commission agreements for the sale of goods

Accounting with the principal

When shipping goods to a commission agent for sale under a commission agreement, the principal uses account 45 “Goods shipped.”

Shipped goods are reflected in accounting at the actual or standard (planned) full cost, which includes, along with the production cost, costs associated with the sale (sale) of products, works, services, reimbursed in the price of the goods.

When transferring goods for sale, an invoice or an act of acceptance and delivery of goods (acceptance certificate) is drawn up, which indicates the price of the goods agreed upon by the parties.

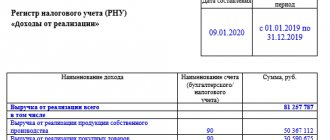

When selling goods or finished products through an intermediary, the principal carries out entrepreneurial activities in the sale of goods or the production and sale of finished products, the proceeds from which are subject to reflection on the credit of account 90 “Sales”. According to clauses 5 and 12 of PBU 9/99 “Organizational Income”, revenue from the sale of goods (products) is income from ordinary activities and is recognized in accounting when the goods are shipped to the buyer based on the commission agent’s report.

To reflect in the accounting accounts settlements with the commission agent, the committing organization can use account 76 “Settlements with various debtors and creditors” subaccount “Settlements with the commission agent”.

The principal must charge and pay VAT on the cost of goods transferred to the commission agent on the date of shipment of the goods by the commission agent to the buyer. The tax base for VAT is determined based on the price of the goods specified in the agreement between the commission agent and the buyer.

Notify the principal of the date of sale of the property by the commission agent in accordance with paragraph. 5 tbsp. 316 of the Tax Code of the Russian Federation is obliged within three days from the end of the reporting period in which such implementation occurred. According to clause 24 of the Rules, the principal is obliged to register in the sales book invoices that reflect the indicators of invoices issued by the commission agent to the buyer (which means the principal must be aware of these indicators).

In order to timely charge VAT by the principal, it is necessary for the commission agent to submit monthly reports to the principal with information on the dates of shipment of goods to customers, confirmed by primary documents.

The accounting entries for the principal under a commission agreement for the sale of goods may be as follows.

| Account correspondence | Contents of operation | Primary document | |

| Debit | Credit | ||

| 45 “Goods shipped” | 41 "Products" | The cost of goods shipped to the commission agent is reflected | Invoice or act of acceptance and transfer of goods |

| 76 “Settlements with commission agent” | 90-1 “Revenue” | Sales of goods to the buyer are reflected | Notice from the commission agent about the shipment of goods to the buyer (posting is made on the date of receipt of the notice) |

| 90-2 “Cost of sales” | 45 “Goods shipped” | Cost of goods sold written off | |

| 90-3 "VAT" | 68 "VAT" | VAT is charged on sales turnover | Invoice issued |

| 44 “Sales expenses” | 76 “Settlements with commission agent” | Commission accrued to the commission agent | Commissioner's report (with attached supporting documents) |

| 90-2 “Cost of sales” | 44 “Sales expenses” | Commission expenses written off | |

| 19 "VAT" | 76 “Settlements with commission agent” | VAT charged on commission fees | Invoice received from the commission agent |

| 68 "VAT" | 19 "VAT" | Submitted for deduction of VAT on commission fees | |

| 51 “Current account” | 76 “Settlements with commission agent” | Received funds from the commission agent for goods sold minus commission* | Payment order |

* The situation with the participation of the commission agent in the calculations is considered.

Accounting with a commission agent

Since things received by the commission agent from the principal are the property of the latter, goods received on commission are not reflected on the commission agent’s balance sheet, but are accounted for in off-balance sheet account 004 “Goods accepted on commission.” Goods accepted for sale under a commission agreement are written off from off-balance sheet account 004 upon sale or upon return of goods to the principal.

Subsequently, the commission agent makes transactions with buyers of products (goods), concluding purchase and sale agreements on his own behalf. Based on clause 3 of PBU 9/99 “Income of the organization”, receipts from legal entities or individuals in favor of the principal are not recognized as income of the commission agent. Accordingly, the disposal of assets under commission agreements, agency and other similar agreements in favor of the principal is not recognized as expenses of the commission agent (clause 3

PBU 10/99 “Expenses of the organization”).

It should be taken into account that since the commission agent makes transactions with third parties on his own behalf, then all the necessary documents must be drawn up on his behalf: agreement, invoices, invoices and others.

Invoices received by the commission agent from the principal for goods transferred for sale, as well as for the amount of payment received, partial payment for upcoming deliveries of goods are not registered in the purchase book. Organizations carrying out business activities in the interests of another person under commission agreements, when selling goods on their own behalf, store invoices for goods and for payment, partial payment for future deliveries of goods received from the principal in the journal of received invoices.

When the goods are shipped to the buyer, the buyer's accounts receivable for payment for goods and accounts payable to the principal are reflected in the commission agent's accounting. To account for settlements with the principal, an organization can use account 76 “Settlements with various debtors and creditors”, for example the subaccount “Settlements with the principal”.

The commission agent must submit to the principal a report with the necessary documents attached (copies of contracts, invoices, invoices, etc.) confirming the fact of sale of goods to customers.

Simultaneously with the report, the commission agent issues an invoice to the principal for the amount of his remuneration. The commission agent registers this invoice in the sales book in accordance with clause 24 of the Rules.

In accordance with clause 5 of PBU 9/99 “Income of the organization”, the amount of commission for the commission agent is income from ordinary activities. In accounting, revenue from ordinary activities is recognized if the conditions provided for in clause 12 of the same PBU 9/99 are met; in this case, these conditions are considered met when goods are sold to the buyer.

The reflection of the accrual of commission in the accounting of the commission agent depends on whether the intermediary is involved in the settlements between buyers and the principal or not.

In the accounting records of a commission agent, transactions when selling goods under a commission agreement can be reflected as follows.

| Account correspondence | Contents of operation | Primary document | |

| Debit | Credit | ||

| 004 “Goods accepted for commission” | Goods received under commission agreement | Invoice or act of acceptance and transfer of goods | |

| 62 “Settlements with buyers and customers” | 76 “Settlements with the principal” | The buyer's debt for goods shipped to him is reflected | Invoice in the form TORG-12 |

| 004 “Goods accepted for commission” | Goods accepted for commission are written off from the off-balance account | ||

| 51 “Current account” | 62 “Settlements with buyers and customers” | Received funds from the buyer for shipped goods | Payment order |

| 76 “Settlements with the principal” | 90-1 “Revenue” | Income recognized in the form of commissions | Commissioner's report |

| 90-3 "VAT" | 68 "VAT" | VAT is charged on the commission amount | Invoice |

| 76 “Settlements with the principal” | 51 “Current account” | Funds transferred to the principal minus commission* | Payment order |

* The situation with the participation of the commission agent in the calculations is considered.

Purchase returns

As noted earlier, when concluding a commission agreement, ownership of the goods until the moment of its sale remains with the principal, who has the right at any time to demand the return of the goods and compensate the commission agent for losses caused. In turn, the commission agent has the right to refuse the order if he is unable to sell the goods within the prescribed period.

In addition, it is possible that a low-quality product may be identified. In accordance with clause 2

Art. 475 of the Civil Code of the Russian Federation, in the event of a significant violation of the requirements for the quality of goods, the buyer has the right to refuse to execute the sales contract.

Under a transaction concluded by a commission agent with a third party, the commission agent acquires rights and becomes obligated. Consequently, the buyer has the right to return the defective goods to the commission agent (unless other conditions are established by the contract).

If the buyer refuses to fulfill the purchase and sale agreement due to a discrepancy in the quality of the delivered goods, in the accounting records of the commission agent, the buyer's debt to pay for the goods returned by him is reduced, and the commission agent's debt to the principal for settlements for the goods sold is also reduced. At the same time, the commission agent reflects the returned goods as a debit to off-balance sheet account 004 “Goods accepted on commission”, since the ownership of it still belongs to the principal.

If the shipment of low-quality goods and its return by the buyer occurred within one month, before the commission agent’s report was approved, then the commission agent makes reversal entries for sales in the report. If the goods are returned by the buyer after approval of the report, then the principal will compensate the commission agent for the amount returned to the buyer.

The principal transfers the returned goods from account 45 “Goods shipped” to the debit of account 41 “Goods”. After returning a defective product, the consignor can also return the product to the supplier. In accounting, this operation is reflected in the credit of account 41 “Goods” in correspondence with the debit of account 76 “Settlements with various debtors and creditors” subaccount “Settlements for claims”.

In addition, upon receiving a notice from the commission agent about the return of the goods by the buyer, the principal, in order to record the real amount of revenue received in the reporting period from the sale of goods and the value of the cost of sales, must reflect their adjustment in accounting by making corrective entries in the relevant accounts.

Commission agreements for the purchase of goods

Accounting with the principal

Accounting for settlements with the commission agent can be carried out using account 76 “Settlements with various debtors and creditors” subaccount “Settlements with the commission agent”.

To reflect the receipt of goods purchased for further resale, the principal should use account 41 “Goods”. If material assets are acquired for other purposes, in particular for use in economic needs, the corresponding account is determined on the basis of the Chart of Accounts and instructions for its use.

The procedure for recording transactions with the principal when purchasing goods under a commission agreement may be as follows.

| Account correspondence | Contents of operation | Primary document | |

| Debit | Credit | ||

| 76 “Settlements with commission agent” | 51 “Current account” | Funds transferred for the purchase of goods | Payment order |

| 41 "Products" | 76 “Settlements with commission agent” | Goods accepted for accounting | Invoice or act of acceptance and transfer of goods |

| 19 "VAT" | 76 “Settlements with commission agent” | VAT charged on goods | Invoice received from the commission agent (for goods) |

| 68 "VAT" | 19 "VAT" | Submitted for deduction of VAT on goods | |

| 41 "Products" | 76 “Settlements with commission agent” | Commission accrued to the commission agent | Commissioner's report |

| 19 "VAT" | 76 “Settlements with commission agent” | VAT charged on commission fees | Invoice received from the commission agent (for commission) |

| 68 "VAT" | 19 "VAT" | Submitted for deduction of VAT on commission fees | |

| 76 “Settlements with commission agent” | 51 “Current account” | Remuneration was transferred to the commission agent and expenses were reimbursed (if any)** | Payment order |

** The situation is considered without the participation of the commission agent in the calculations.

Accounting with a commission agent

Since goods that are the property of the organization are accounted for separately from the goods of other legal entities held by this organization, goods purchased by the commission agent for the principal are reflected by the intermediary on off-balance sheet account 002 “Inventory assets accepted for safekeeping” at the price indicated in the shipping supplier documents. Materials are written off from off-balance sheet accounting at the time of their transfer to the principal.

The commission agent does not have the right to reimbursement of expenses for storing the principal's property in his possession, unless otherwise provided in the law or the commission agreement.

Since the commission agent makes transactions with third parties on his own behalf, all documents from the supplier are drawn up in his name: agreement, invoices, invoices and others, while he is not obliged to indicate that he is acting on the instructions of the principal.

Invoices received by the commission agent from the seller of goods, issued in the name of the commission agent for goods, for the amount of payment, partial payment for upcoming deliveries of goods are not registered in the purchase book.

After executing the order under the commission agreement, the commission agent, in accordance with Art. 999 of the Civil Code of the Russian Federation, must submit a report to the committent and transfer to him everything received under the commission agreement. If the principal has objections to the report, then he must notify the commission agent about them within thirty days from the date of receipt of the report, unless another period is established by the agreement. Otherwise, the report is considered accepted.

Since the form of the commission agent’s report is not established by law, the commission agent can draw up such a report in any form. The main requirement is that it meets the requirements for the primary document in Art. 9 of the Federal Law of November 21, 1996

No. 129-FZ “On Accounting”.

Despite the fact that in Art. 999 of the Civil Code of the Russian Federation there are no requirements to submit, along with the report, documents confirming the data reflected in the report; in paragraph 14 of the Information Letter of the Presidium of the Supreme Arbitration Court of the Russian Federation dated November 17, 2004 No. 85 “Review of the practice of resolving disputes under a commission agreement” it is stated that the commission agent’s report is not evidence the commission agent fulfills his obligations under the commission agreement without confirming it with other evidence.

And such documents should be copies of contracts, invoices, invoices, acceptance certificates, etc., attached to the report.

In the accounting of a commission agent, transactions for the acquisition of goods under a commission agreement may be as follows.

| Account correspondence | Contents of operation | Primary document | |

| Debit | Credit | ||

| 51 “Current account” | 76 “Settlements with the principal” | Received funds from the principal | Payment order |

| 60 “Settlements with suppliers and contractors” | 51 “Current account” | Payment transferred to the supplier | Payment order |

| 002 “Inventory and materials accepted for safekeeping” | The receipt of goods from the supplier is reflected on the off-balance sheet account | Invoice in form TORG-12 from the supplier | |

| 76 “Settlements with the principal” | 60 “Settlements with suppliers and contractors” | Reflects the transfer of ownership of the goods | Invoice or act of acceptance and transfer of goods |

| 002 “Inventory and materials accepted for safekeeping” | Goods transferred to the principal are written off from the off-balance account | ||

| 76 “Settlements with the principal” | 90-1 “Revenue” | Income recognized in the form of commissions | Commissioner's report |

| 90-3 "VAT" | 68 "VAT" | VAT is charged on the commission amount | Invoice |

| 51 “Current account” | 76 “Settlements with the principal” | Commission amount received | Payment order |

** The situation is considered without the participation of the commission agent in the calculations.

Purchase returns

In the event of a significant violation of the quality requirements for the goods, the consignor has the right to refuse it. The commission agent has the right, in turn, to return the defective product to the seller.

If the principal refuses to account for the commission agent, the debt of the principal to pay for the goods returned by him is reduced, and the debt of the commission agent to the seller for settlements for the purchased goods is also reduced. At the same time, the commission agent reflects the returned goods as a debit to off-balance sheet account 002 “Inventory and materials accepted for safekeeping.”

If the shipment of low-quality goods and its return to the seller occurred within one month, before the commission agent’s report was approved, then the commission agent makes reversal entries in the report. If the goods are returned by the principal after approval of the report, then the commission agent compensates the principal for his expenses.

When returning the goods, the principal makes an entry on the credit of account 41 “Goods” in the debit 76 “Settlements with various debtors and creditors” subaccount “Settlements for claims”.

Upon receipt of a notice from the consignor about the return of the goods, the commission agent may make quality claims to the seller in the prescribed manner.

Chart of accounts for accounting financial and economic activities of organizations and instructions for its application, approved by Order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n.

Clause 61 of the Regulations on accounting and financial reporting in the Russian Federation, approved. By Order of the Ministry of Finance of the Russian Federation dated July 29, 1998 No. 34n.

Accounting Regulations “Income of the Organization” PBU 9/99, approved. By Order of the Ministry of Finance of the Russian Federation dated May 6, 1999 No. 32n.

Rules for maintaining journals of received and issued invoices, purchase books and sales books when calculating value added tax, approved. Decree of the Government of the Russian Federation dated December 2, 2000

№ 914.

Chart of accounts for accounting financial and economic activities of organizations and instructions for its application, approved by Order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n.

Accounting Regulations “Income of the Organization” PBU 9/99, approved. By Order of the Ministry of Finance of the Russian Federation dated May 6, 1999 No. 32n.

Accounting Regulations “Organization Expenses” PBU 10/99, approved. By Order of the Ministry of Finance of the Russian Federation dated May 6, 1999 No. 33n.

Clauses 3, 11 Rules for maintaining logs of received and issued invoices, purchase books and sales books when calculating value added tax, approved. Decree of the Government of the Russian Federation dated December 2, 2000 No. 914.

Rules for maintaining journals of received and issued invoices, purchase books and sales books when calculating value added tax, approved. Decree of the Government of the Russian Federation dated December 2, 2000

№ 914.

Chart of accounts for accounting financial and economic activities of organizations and instructions for its application, approved by Order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n.

Clause 2 of Art. 8 of the Federal Law of November 21, 1996 No. 129-FZ “On Accounting”.

Paragraph 2 art. 1001 Civil Code of the Russian Federation.

Clause 11 Rules for maintaining logs of received and issued invoices, purchase books and sales books when calculating value added tax, approved. Decree of the Government of the Russian Federation dated December 2, 2000 No. 914.

Rules for accounting for intangible assets

Information on account 04 consists of the cost of all inventory items recorded on the balance sheet (at initial or actual cost). The account is active: receipts are reflected as a debit, and write-offs as a credit.

Objects are accepted for accounting through account 08 “Investments in non-current assets”. At this stage, the initial cost of the asset is formed and it is debited to account 04 immediately after it is ready for operation. This happens after checking the object for compliance with all the requirements prescribed in the PBU for intangible assets (link above).

Off-balance sheet accounts in the budget: general provisions

Budgetary accounting of MCs on the balance sheet is carried out in a simple way: receipts are subject to reflection on the debit side of the accounts, disposals - on the credit side. Corresponding records are not used when using them. Budgetary organizations can open additional off-balance sheet accounts to collect information necessary for management accounting and internal control over the safety of property.

Accounting for property assets on the balance sheet is carried out using the same primary documents and registers that are used in accounting for MC on the balance sheet. Inventory of off-balance sheet funds is carried out in the same way as for objects on balance sheet accounts.

Subaccounts used

The Instructions to the Chart of Accounts do not specify specific subaccounts for use by the organization. It states only what the analyst needs to conduct in the context of property categories.

Companies prepare a working chart of accounts every year. Account 04 is relevant for universities, design, engineering, and research organizations. In small businesses, account 04 does not occupy a dominant position, since such organizations own a small number of intangible assets.

Off-balance sheet account MC 04 - what is it and how to use it?

MC 04 off-balance sheet account - what is it? Let's look at what the off-balance sheet account MTs.04 is, provided for by the chart of accounts of the 1C: Accounting program, and in what cases it is used.

Why are off-balance sheet accounts of MC needed (MC.01, MC.02, MC.03, MC.04)

Entries on the debit of account MTs.04

Entries on the credit of account MC.04

Inventory of account MC.04

Results

Results

The off-balance sheet account MTs.04 is used by users of the accounting program “1C: Accounting” to account for the inventory and household supplies transferred into operation. Inventory receipts are debited from this account, and disposals are credited to this account. Analytics is carried out in quantitative terms, by item items and financially responsible persons.

You can find more complete information on the topic in ConsultantPlus. Full and free access to the system for 2 days.

Source: https://nalog-nalog.ru/buhgalterskij_uchet/vedenie_buhgalterskogo_ucheta/zabalansovyj_schet_mc_04_chto_eto_i_kak_ego_ispolzovat/

Basic operations for accounting for intangible assets

In order for intangible assets to be displayed correctly on the balance sheet, you need to be able to properly organize their accounting. This is done using three basic operations:

- acceptance for registration;

- sale;

- depreciation.

All these transactions must be reflected in the company's accounting policies. Let's look at each operation in more detail.

Acceptance of intangible assets for registration

Intangible assets can be registered through purchase, creation with one’s own hands, receipt as a gift, or during discovery during inventory. As mentioned earlier, an object is accepted for accounting through account 08.

To account for intangible assets, the following entries are made:

- Dt 08, Kt 60 – purchase costs are reflected;

- Dt 02, Kt 10 / 70 / 69 – expenses for materials for creating the object are reflected;

- Dt 19, Kt 60 – VAT is included;

- Dt 04, kt 08 – the actual cost is formed.

Sale of intangible assets

During the sale of intangible assets, its residual value is calculated. As a result, the book price is reduced by the amount of depreciation. The following transactions are made:

- Dt 62, Kt 91 – the sale is reflected;

- Dt 91, Kt 68 – VAT is allocated;

- Dt 05, Kt 04 – depreciation is written off;

- Dt 91, Kt 04 – the residual value is written off.

Property that was acquired for subsequent sale cannot be classified as non-current assets. This also applies to objects that do not have a material form.

Liquidation of intangible assets

The liquidation of intangible assets is documented using the same transactions as for the liquidation of other non-current assets. The only difference is the use of account 04:

- Dt 91 Kt 04 – writing off the residual value of intangible assets for other expenses.

In case of complete liquidation, the residual value is zero.

Thus, in order to correctly reflect intangible assets on the account and in the financial statements, it is important to understand whether the object belongs to intangible assets and how to register it correctly. If you know all the basic nuances, there will be no problems with taking into account intangible assets.

Which accounts does account 08 correspond to?

Account 08 corresponds with most of the accounts by debit. The list of accounts with which he corresponds on the loan is much smaller. For convenience, we have collected all the accounts in a table.

| Account 08 corresponds by debit with | Account 08 corresponds for the loan with |

| 02 “Depreciation of fixed assets” 05 “Depreciation of intangible assets” 07 “Equipment for installation” 10 “Materials” 11 “Animals for growing and fattening” 16 “Deviation in the cost of material assets” 19 “VAT on acquired assets” 23 “Auxiliary production” 26 “General business expenses” 60 “Settlements with suppliers and contractors” 66 “Settlements for short-term loans and borrowings” 67 “Settlements for long-term loans and borrowings” 68 “Settlements for taxes and fees” 69 “Settlements for social insurance and security” 70 “ Settlements with personnel for wages" 71 "Settlements with accountable persons" 75 "Settlements with founders" 76 "Settlements with various debtors and creditors" 79 "Intra-business settlements" 80 "Authorized capital" 86 "Targeted financing" 91 "Other income and expenses » 94 “Shortages and losses from damage to valuables” 96 “Reserves for future expenses” 97 “Deferred expenses” 98 “Deferred income” | 01 “Fixed assets” 03 “Income-earning investments in tangible assets” 04 “Intangible assets” 76 “Settlements with various debtors and creditors” 79 “Intra-business settlements” 80 “Authorized capital” 91 “Other income and expenses” 94 “Shortages and losses from damage to valuables" 99 "Profits and losses" |

To keep or not to keep off-balance sheet accounting?

The tax service can hold people accountable for the lack of “off-balance sheet” accounting in accordance with Article 120 of the Tax Code of the Russian Federation. Inspectors have the opportunity to classify this offense as a systematic failure to reflect transactions in accounts.

Which, in turn, is a gross violation of accounting rules. These are, perhaps, all possible sanctions from the fiscal authorities. And it will cost you ten thousand rubles, since it is very difficult to prove that the violation relates to more than one tax period.

Although those who have commission agreements should check which accounts the goods accepted for sale are allocated to. There will be no fines, but you may have to defend the correctness of tax calculations in arbitration court. If account 004 “goods accepted for commission” was not used, and the products were reflected in the balance sheet, then the tax authorities will consider such a transaction as a supply. And the arbitrators, please note, will support the fiscals in this point of view (resolution of the FAS North Caucasus District dated July 10, 2007 No. F08-3951/2007-1559A, resolution of the FAS East Siberian District dated December 24, 2008 No. A69-1835 /06-8-F02-6680/08). When taxpayers use off-balance sheet account 004 in accounting, the courts do not reclassify commission agreements as supply agreements (resolution No. F03-A73/07-2/5379 dated December 5, 2007, resolution No. F03-A73/07-2 dated December 5, 2007 /5379).

The tax service can hold people accountable for the lack of “off-balance sheet” accounting in accordance with Article 120 of the Tax Code of the Russian Federation. Inspectors have the opportunity to classify this offense as a systematic failure to reflect transactions in accounts.

Maintaining off-balance sheet accounting helped the company “Joint-Stock Company” to defend the correctness of the calculated property tax. The company purchased the equipment on behalf of another legal entity, which subsequently registered the purchased item as a fixed asset and gave it to JSC Aktsionernaya for safekeeping. You can get acquainted with this situation in more detail in the resolution of the Federal Antimonopoly Service of the East Siberian District dated September 10, 2010 No. A58-2300/2009. In turn, there were letters from fiscal authorities stating that equipment and fixed assets reflected in off-balance sheet accounts are not recognized as objects of taxation for corporate property tax (letter of the Ministry of Finance dated May 15, 2006 No. 03-06-01-04/ 101, letter of the Department of Tax Administration for Moscow dated June 9, 2004 No. 23-10/1/38452).

The main importance of off-balance sheet accounts is to inform users of financial statements about the financial and economic activities of the organization. And the lack of data on these accounts can confuse consumers who will work with the report. And since current legislation is aimed at bringing Russian accounting and international financial reporting standards closer together, it is better to accustom yourself and the company to follow a clear reflection of all existing transactions. One of the methods of bringing IFRS closer to RAS and eliminating possible claims from controllers is a detailed description of “off-balance sheet transactions” in the explanatory note to the balance sheet.

Arbitrators' opinion

Fortunately for taxpayers, arbitrators often side with them. The judges are of the opinion that the information to be reflected in the financial statements on off-balance sheet accounts does not affect the formation of assets and liabilities of the balance sheet, and is not an income or expense of the organization (Resolution of the Federal Antimonopoly Service of the Moscow District dated March 11, 2009 in case No. KA-A40 /1181-09, Decision of the Moscow Arbitration Court dated June 21, 2005 No. A40-14510/05-80-45, Resolutions of the Federal Antimonopoly Service of the East Siberian District dated July 29, 2008 in case No. A19-566/08-20-F02 -3528/08, West Siberian District dated 09/08/2004 in case No. F04-6301/2004 (A75-4445-14). Maintaining off-balance sheet accounting is not very difficult, but the advantages of using such accounts may be much greater, than minuses, especially when turning to Themis for protection.

Svetlana Shchepetilnikova, expert at Calculation magazine