Features of returning goods with VAT under the simplified tax system for individual entrepreneurs

For individual entrepreneurs (individual entrepreneurs) and companies operating on a simplified system, it does not matter which mode their partner uses. This does not affect accounting under the simplified tax system

For companies that operate on the OSN, it matters whether the partner works on a simplified basis and whether he pays the fee.

If a person buys something from a company on OSN, then the partner’s taxation system is not important for the seller. Upon sale, he charges taxes, and the buyer will account for the goods according to the simplified rules. Difficulties arise when returning an object that was taken into account. This operation is called reverse implementation.

Since title has passed to the buyer, upon return it reverts to the seller. The latter has a purchase of the product, and the buyer has a sale. Then it would be more profitable for the seller to buy the goods with tax in order to deduct it. But, since the simplifier does not pay the fee, the seller on the OCH can write out an adjustment SF, which reflects the difference by which the quantity of products and the price, the amount of the input fee, have decreased.

Corrections are not made to the original document, but before issuing an adjustment SF, the company on the OSN must receive information that justifies the return.

Return of goods from the buyer in 2021

Until, instead of the well-known Decree of the Government of the Russian Federation No. 9143, a new decree was issued4. In connection with the appearance of this document, the Ministry of Finance of Russia5 canceled its previously issued clarifications. This has led accountants to once again begin to wonder about the issue of issuing invoices when returning goods. The situation was also complicated by the emergence of a new document called an “adjustment invoice”: perhaps, when returning goods, an adjustment invoice should be issued?

On the date of transfer of ownership of the returned goods to the former supplier, the organization - the former buyer determines the income from sales based on the cost of the returned goods specified in the contract without VAT (clause 1 of Article 248, clauses 1, 2 of Article 249, p 3 Article 271, paragraph 1 Article 39 of the Tax Code of the Russian Federation).

Return of goods by a special regime buyer: what about VAT

Regardless of the reason for which the simplifier returns the goods to the seller, he does not issue an invoice upon return. However, a general seller may still be able to deduct VAT on returned goods. At the same time, as you know, in order to deduct VAT, the presence of an invoice is a prerequisite. The question arises: on the basis of what document does the seller accept tax deduction?

For clarification, we turned to Federal Tax Service specialist Olga Sergeevna Duminskaya. And this is what she answered us:

“A buyer who is not a VAT payer (including those who use the simplified procedure) returns to the seller goods that do not comply with the terms of the contract. For example, the product turned out to be of poor quality. Or buyers have no complaints about the quality of the goods, but any other requirements specified in the contract are not met. In particular, the conditions for the assortment or completeness of the goods have not been met.

In all these cases (and regardless of whether the goods were accepted by the buyer for accounting or not), the following procedure applies. The seller, who has received back his goods in full, deducts VAT on the basis of his invoice, which he previously registered in the sales book when shipping the goods. To do this, such an invoice is registered by the seller in the purchase book as the right to tax deductions arises. This can be done no later than 1 year from the date of return of the goods by the buyer.

In the same procedure, the seller can claim a VAT deduction if the VAT evader returns to him a product that is of high quality and fully complies with the terms of the contract. After all, in ch. 21 of the Tax Code of the Russian Federation does not provide for exceptions to the general rule of applying VAT deductions when returning goods by persons who are not VAT payers.

If the buyer, who is not a VAT payer, returns the goods only partially, then the seller should issue an adjustment invoice. After accepting the returned goods, he can register them in the purchase ledger.”

Newsletter for an accountant

Every day we select news that is important for an accountant’s work, saving you time.

Receive free accounting news by email.

Accounting for defects in production

In the field of production, a defect is a product or its element (it can be a semi-finished product, part, assembly), the quality of which does not fit into the norms, standards, technical conditions adopted at the enterprise, and which is impossible to use for its intended purpose or is only permissible with additional adjustments that require costs. .

FOR YOUR INFORMATION! The definition of manufacturing defects, used in modern legal acts, repeats clause 38 of the Basic Provisions for Planning, Accounting and Calculation of Costs at Industrial Enterprises, approved by the State Planning Committee of the USSR, the State Committee for Prices of the USSR, the Ministry of Finance of the USSR and the Central Statistical Office of the USSR on July 20, 1970.

Purchase of goods in 2021 - return in 2021: what to do with VAT

When returning goods purchased by persons who are not taxpayers or exempt from paying taxes and transferred to customers without invoices before January 1, 2021, an adjustment document is recorded in the purchase ledger containing summary data on return transactions made during the calendar month (quarter ), regardless of the CCT readings.

Therefore, when returning from January 1, 2021 the entire batch or part of the goods (both accepted and not accepted by buyers), the seller is recommended to issue adjustment invoices for the cost of the returned goods, regardless of the period of shipment of the goods, that is, until 01/01/2019 or from the specified date. At the same time, if in column 7 of the invoice a tax rate of 18% is indicated, then in column 7 of the adjustment invoice for this invoice the VAT of 18% is also indicated.

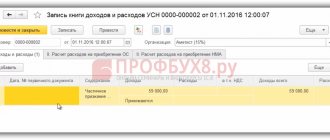

Reflection of returns in accounting

In the event of returning goods that have not been received by the buyer, the seller makes adjustments in accounting:

| Wiring | Explanation of operation |

| Dt 62 Kt 90 (reversible) | Reduced revenue for low-quality goods |

| Dt 90 Kt 41 (reversible) | Cost reduction |

| Dt 90 Kt 68.2 (reversible) | VAT reduction |

| Dt 62 Kt 51(50) | Refund to the buyer |

If a quality product that has been accepted by the buyer for registration is returned, the following entries are used:

| Postings | Explanations |

| Dt 41 Kt 60 | Acceptance of returned goods by the supplier |

| Dt 19 Kt 60 | We will take into account VAT |

| Dt 62 Kt 51 | Refund to the buyer |

| Dt 60 Kt 62 | Adjusting entry for debt |

We are on the way, we need to return the goods with VAT

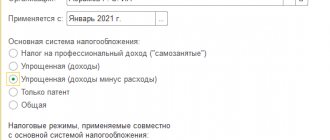

As a result, it was not installed. we want to return the goods. From the receipt adjustment, a printed form of the Waybill (TORG-12) for returns is available. We will talk about the VAT nuances of returning goods “simplified” in this article. Regardless of the composition, the deadlines for submitting reports for simplified reporting are the same - within three months after the end of the reporting year, that is, before 31 Deadlines for submitting other mandatory reports under the simplified tax system in 2021.

VAT payers are only individual entrepreneurs and organizations on the main taxation system. Is the gratuitous transfer of goods subject to tax under the simplified tax system and at what rate? According to the simplification, only emergency situations can work? accountants' website We LLC buy goods from individual entrepreneurs, what to do with VAT if the individual entrepreneur is on the simplified tax system? Returning goods with VAT under the simplified tax system has a number of features, since, in accordance with the explanations of the financial and fiscal departments, reflection in accounting does not depend on whether the goods were capitalized by the buyer.

Buyer refund rules

How to correctly issue a refund to a buyer depends on when he contacted you.

Return on the day of purchase

If the customer paid in cash, give him the money directly from the cash register drawer. When paying for goods by card, refunds are also made by bank transfer - just cancel the transaction. In both cases, do not forget to punch the check at the cash register with the sign “return of receipt”.

Return another day

If the customer returns the item on another day, money cannot be taken from the cash register drawer. Issue money from the main cash register - this is what all cash in the organization is called. If you have an LLC, write out an expense cash order or RKO. Individual entrepreneurs do not need to do this, since they are not required to observe cash discipline.

Read more about this in the article “Cash discipline”

If the buyer paid for the goods using a bank card, return the money back to it. In this case, cash cannot be issued; this is prohibited by the Directive of the Central Bank of the Russian Federation. How exactly to return money to the buyer’s card, check with the support of the bank with which you have an acquiring agreement. If you cannot return the money back to the card, withdraw the money from the current account and return it to the buyer.

Submit reports in three clicks

Elba will help monitor inventory balances and conduct inventories. She will prepare reports and calculate taxes.

Try 30 days free Gift for new entrepreneurs A year on “Premium” for individual entrepreneurs under 3 months

Purchase of goods in 2021 - return in 2021: what to do with VAT

In short, returns of goods purchased in 2021 at the 18% rate will have to be made through adjustment invoices at the 18% rate. The basis for this operation will be the letter of the Federal Tax Service of Russia “On the procedure for applying the tax rate for VAT during the transition period” dated October 23, 2020 N SD-4-3/ Now let’s take a closer look at the application of VAT by the seller and the buyer when returning goods from January 1, 2021.

Therefore, when returning from January 1, 2021 the entire batch or part of the goods (both accepted and not accepted by buyers), the seller is recommended to issue adjustment invoices for the cost of the returned goods, regardless of the period of shipment of the goods, that is, until 01/01/2020 or from the specified date. At the same time, if in column 7 of the invoice a tax rate of 18% is indicated, then in column 7 of the adjustment invoice for this invoice the VAT of 18% is also indicated.

VAT

From the above provisions of the Civil Code of the Russian Federation it follows that in the event of a return of goods of proper quality, the seller organization initially fulfilled its obligations under the purchase and sale agreement properly, ownership of the goods passed to the buyer and there is no reason to recognize the sale as not having taken place.