To crush or not to crush - that is the question

The transition from the OSN to the simplified tax system is possible only once a year, subject to notification of the tax service before December 31 of the current year.

The advantages of simplification are obvious:

1

Reducing the tax burden. Simplified residents are exempt from 4 taxes: profit, property, VAT and personal income tax (for individual entrepreneurs).

2

The tasks of the accounting department in maintaining tax and accounting records are simplified. For example, invoices are not prepared and there are no income tax registers.

3

The right to choose one of 2 options for paying a single tax: “income 6%” or “income minus expenses 15%”, which is paid in advance payments quarterly, and the final amount is paid at the end of the year.

There are exceptions in the Tax Code of the Russian Federation and in regional legislation, which you need to pay attention to before switching to the simplified tax system.

Reporting under the simplified tax system

“Simplers” report quarterly and at the end of the tax period (1 year).

Every year they must submit a tax return to the Federal Tax Service. Art. 346.23 of the Tax Code of the Russian Federation establishes the deadlines for its filing:

- for organizations - until March 31 of the new year;

- IP - until April 30.

If a company or individual entrepreneur stops working for the simplified tax system at their own request, then they submit a declaration by the 25th of the next month after the change in the taxation regime.

If an organization or individual entrepreneur switches to another regime forcibly, then the declaration is submitted before the 25th day of the month after the quarter in which this happened.

In addition to the declaration, the simplified annual reporting includes:

- balance sheet and profit and loss account;

- certificate of average number of employees;

- certificates of accrued wages (2-NDFL);

- statements of contributions to the Social Insurance Fund, Pension Fund, etc.

Special mode is not for everyone

The conditions for the transition from the OSN to the simplified tax system are established by law in the Tax Code. It is possible to change the tax system if the organization meets 2 main conditions for the revenue limit and staff size:

- number of employees is less than 100 people;

- income and residual value of fixed assets as of October 1 do not exceed 150 million rubles.

For organizations and individual entrepreneurs, the transition from the OSN to the simplified tax system is further complicated by the presence of branches, the share of participation of other companies above 25% and income over 112.5 million rubles. based on the results of 9 months before filing an application to change the tax regime.

In addition to the above, the law establishes a ban on simplifying the nature of activities for such organizations as banking, microfinance, insurance, budgetary organizations, agricultural producers, non-state pension funds, pawnshops and a number of others (more details here).

Transition to simplified tax system from OSNO

To make such a transition, firstly, conditions regarding income, number and value of fixed assets must be met.

Secondly, the taxpayer will have to restore VAT when switching to the simplified tax system (clause 2, clause 3, article 170 of the Tax Code of the Russian Federation). And all because VAT is not paid on the simplified system.

The full tax must be restored on goods and materials that have not yet been used in the company’s activities (for example, they are in a warehouse). You will also have to restore the previously deducted VAT on fixed assets and intangible assets. On them, VAT is restored in proportion to the residual value. Let's look at an example.

In 2021, Progress LLC decided to work on the simplified tax system instead of OSNO. On the company's balance sheet there is a machine that was purchased for 120,000 rubles, VAT was deducted in the amount of 20,000 rubles. At the end of 2021, the residual value of the machine is 74,000 rubles. We will restore VAT as follows:

20,000 x (74,000 / 120,000) = 11,666.67 rubles.

In accounting, the company will reflect the restoration operation with postings (this must be done before the end of 2021):

Debit 19 Credit 68 11,666.67 - VAT on the machine was restored;

Debit 91 Credit 19 for 11,666.67 - restored VAT is charged to other expenses.

There is no need to restore VAT when changing the taxation system if:

- the organization combines the simplified tax system and the OSNO and maintains separate accounting;

- VAT on the purchase of property was not deducted.

Splitting your business is tempting, but is it safe?

Exceeding the income limit over 150 million rubles. forces big business to split the organization into several independent companies or open an individual entrepreneur under the simplified tax system. However, tax inspectors are constantly looking for illegal tax benefit schemes from “special regimes”, especially in cases where simplified organizations are engaged in the same types of activities.

The courts are inundated with appeals from entrepreneurs trying to prove that the division of business was not a violation of the law. Over the past 3 years (2016-2018), more than 450 cases on similar issues have passed through Russian arbitration courts. An average of 30 million rubles was recovered from taxpayer organizations that sued the Federal Tax Service. At risk are large companies whose income has grown to the maximum limit for the simplified account.

At the same time, judicial practice shows that you can win in proceedings with tax authorities if you approach the transition to a special regime correctly. Our company, which has experience in participating in such courts, offers legal support and accounting services for businesses during the transition period.

How to prove the legality of business division?

The following actions will help you avoid additional tax assessments under OSN:

1

Organizations transferred to the simplified tax system actually existed, carried out activities, and independently paid taxes under a simplified system.

2

The optimal division of technological processes between companies will be evidence in court. The scale of business division (into 2 companies or 10) does not matter.

3

Business is not only divided between companies, but they conduct various types of business activities independently of each other, have their own management apparatus and make independent administrative decisions.

4

Newly created enterprises have their own suppliers, business partners and clients, different from the parent company, use the services of other service organizations, have personal certificates, licenses, all the necessary permits, have their own equipment and their own staff.

5

The Federal Tax Service's accusation that a group of companies (general director) has a single management cannot become grounds for deprivation of rights to a special regime.

These and other actions proposed by our company when transferring part of the business from the OSN to the simplified tax system, features

HR and management decisions for a newly created company will help you calmly conduct business without tedious lawsuits.

The transitional stage needs good legal support

, the price of which is hundreds of times lower than a possible tax penalty.

Examples of common mistakes

Example No. 1. Court decision A50-10873/2017

The founders formally divided the LLC into 2 organizations using the simplified tax system. The organization suffered losses in the form of penalties from the Federal Tax Service of more than 40 million rubles.

Where is the mistake?

They used common labor resources, common software, and common material resources. The dependent company did not have permission to carry out the work. The companies also had an excess of the limit of employees for the special regime of the simplified tax system (more than 100), the same suppliers and buyers. After analyzing the movement of funds and interrogating employees of both companies, tax officials proved the presence of intent to evade taxes.

H3: Example No. 2. Judgment A59-2443/2017.

The construction company involved 5 interdependent companies using the simplified tax system for work under a contract. According to the court decision, the company had to pay over 226 million rubles to the budget. additional tax payments.

Where is the mistake?

The counterparties did not have their own production bases, warehouses, vehicles, etc. The construction company had accounts receivable to contractors, did not have its own working capital to pay off the debt, and also lacked its own funds for financial stability.

Becoming a simplifier couldn't be easier

The method of transition to simplified taxation is not complicated. If an organization or individual entrepreneur fits the conditions of the regime, it has no restrictions under Art. 346.12 of the Tax Code of the Russian Federation, then the entire further process consists of submitting a notice of application of the simplified tax system in form No. 26.2-1 to the tax service at the location of the business. When switching from the OSN to the simplified tax system, the deadline for filing an application is established by law - from October to December 31 of the current year.

The notification form is available on the Federal Tax Service website and can be downloaded. If any difficulties arise, our company can assist in filling out this form.

Transition to "simplified"

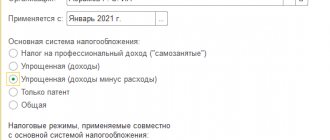

The law provides for a voluntary principle of transition to the “simplified system”. The simplified system is valid only for those who have declared a transfer to the Federal Tax Service. Those who can apply the simplified tax system in 2021 have certain deadlines for the transition:

- New firms and entrepreneurs submit a notification either together with documents for state registration, or separately, but no later than 30 days from the date of state registration.

- Already operating legal entities and individual entrepreneurs can switch to the simplified tax system only from January 1, notifying the tax authorities about this before the end of the year preceding the year of transition. To apply the “simplified tax” from January 1, 2021, a notification in form No. 26.2-1 is submitted to the tax office before January 9, 2021 (since December 31, 2021 is a non-working day).

At the same time, it is worth strictly monitoring the deadlines - if you are late in notifying the tax authorities about the application of the simplified system, the taxpayer will be deprived of the right to use this system and will be able to switch to it only after a year.

If the notification is sent to tax authorities by mail, it is imperative to do this by registered mail with a list of attachments (otherwise it will be difficult to prove that it was the notification about the simplified tax system that was sent).

When visiting the Federal Tax Service in person, it is recommended to draw up a notification in 2 copies so that one of them with a mark from the tax authority remains with the company or individual entrepreneur. The Federal Tax Service does not issue a response confirmation that the required regime has been established, but later you can request confirmation from the tax authorities (by letter drawn up in any form or electronically via TKS) that this particular regime is applied.

Are there any disadvantages to switching to simplified language?

Among the negative consequences of the transition from the OSN to the simplified tax system are the following:

- the need for a transition period and possible difficulties in translating financial statements;

- the requirement of tax authorities during the transition from the OSN to the simplified tax system to restore VAT, first of all, input;

- for large deliveries - a decrease in income due to the departure of large clients working with VAT.

In a situation where the company is operating at a loss, the general regime becomes more profitable than the simplified one:

| Loss-making enterprise rates | |||

| OSN | simplified tax system "income" | Simplified tax system “income minus expenses” | |

| Income tax rate | 0 | 6% (depending on region) | 1% |

| VAT | 0 | No | No |

When switching from the OSN to the simplified tax system, it is necessary to adjust the VAT in contracts concluded before the new taxation. Starting from the new calendar year, simplifiers indicate the price with the note “VAT not subject to.”

Transition from the simplified system to the simplified tax system for business entities: main nuances

Having considered how the transition from OSNO to simplified tax system is carried out, we will study the reverse procedure - when it begins to work within the framework of the general taxation system. At the same time, it will be useful to study the specifics of this phenomenon in relation to the activities of business entities. The fact is that, as a rule, it is LLCs that feel the need to switch to OSN. Entrepreneurs do not often choose to change the taxation system in favor of the OSN, or they become obliged to do so.

The need to switch from the simplified tax system to the simplified tax system most often arises if:

- due to the specifics of the business, work on OCH is justified and profitable;

- the company does not meet the criteria for operating under the simplified tax system - for example, in terms of revenue or staff size.

As in the case of such a procedure as the transition of an LLC from the OSNO to the simplified tax system, the business company must notify the Federal Tax Service of the Russian Federation about the change in the taxation regime. However, this mechanism can be presented in 2 varieties.

If a company switches to the OSN voluntarily, because it considers working under the corresponding scheme more profitable, it must notify the Federal Tax Service about this before January 15 of the year in which it plans to begin paying taxes under the OSN.

If a company is forced to switch to the simplified tax system due to the specifics of its business, it must send a corresponding notification to the tax service within 15 days after the expiration of the reporting period in which it ceased to meet the criteria of the simplified tax system.

conclusions

The tightening of tax legislation from 2021, expressed in 78 changes that also affected simplifiers, suggests that fiscal services are not going to calm down. After the release of No. 163-FZ of July 18, 2017, according to Article 54.1 of the Tax Code of the Russian Federation, the Federal Tax Service took up arms against entrepreneurs with even greater tax audits. The task of tax services is to combat business fragmentation and replenish the budget with additional funds.

The features of the transition from OSN to simplified taxation require a balanced decision. How to escape or avoid being targeted by tax inspectors? Contact MCOB. We will conduct an internal audit of accounting and organize business support. We work - you can easily develop your business!