How to keep records when receiving a subsidy

According to clause 1 of Article 346.17 of the Tax Code of the Russian Federation, subsidies for the first two years in “simplified terms” are reflected in income in proportion to the expenses actually incurred through subsidies.

If at the end of the second year the amount of the subsidy exceeds the amount of recognized expenses, then the difference in full is reflected in the income of this tax period.

This procedure for recognizing income is used by taxpayers who use “Income minus expenses” as an object, as well as for the object “Revenue”, provided that they keep records of payment amounts.

Thus, these incomes should appear in KUDiR (column 4) in the amount of expenses incurred from them (column 5). The amounts will be the same. This will be the accounting of subsidies.

Those taxpayers who use “Income minus expenses” make expenses for the first two years and immediately display KUDiR income. If you have not spent the entire subsidy in two years and have a balance, then in the third year you include the subsidy as income, regardless of the expense.

Subsidy in accounting: postings in examples

Example 1

Due to the subsidy allocated by Stroyka LLC, the company acquired a plot of land for development in January 2017 worth RUB 3,500,000. According to the concluded agreement, the construction of the house will continue from February 1, 2021 to July 30, 2021 - 18 months. Accounting for the subsidy in the company’s accounting will be reflected in the following entries:

Operations D/t K/t Sum Budget funds credited 51 86 3 500 000 The cost of the site is reflected in the company’s capital investment structure 08 60 3 500 000 The site has been registered 01 08 3 500 000 Reflection of subsidies in the accounting of deferred income 86 98/2 3 500 000 Monthly write-off of a share of the subsidy amount into non-operating income (3,500,000 / 18 months) for non-depreciable property, such as a land plot 98/2 91/1 194 444

Example 2

In May 2021, Radon LLC purchased a set of equipment as part of the state support program in the amount of RUB 560,000. The monthly depreciation of the complex amounted to 4,666.67 rubles. (560,000 / 10 / 12 months), it was accrued from June 2021 to May 2021 - 12 months.

A year later (in May 2018), an audit revealed a violation of the intended use of the allocated subsidy, and the subsidy was returned to the budget on the basis of a drawn up act. The accountant recorded the transactions with the following entries:

Operations D/t K/t Sum Subsidy repayment debt 86 76 560 000 The amount of depreciation is taken into account as part of deferred income (4666.67 x 12) 98/2 91/1 56 000 Subsidy funds were restored in the amount of accrued depreciation (4666.67 x 12) 91/1 86 56 000 The subsidy amount has been restored (560,000 – 56,000) 98/2 86 504 000 The subsidy is transferred to the budget 76 51 560 000

How to receive a subsidy in 1C 8.3

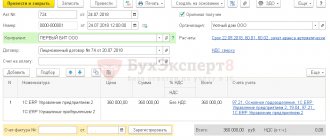

Step 1. Received a subsidy for the purchase of materials

There may be different options with methodology; according to the chart of accounts, you can provide your own methodology. For example:

- A subsidy was received on the current account: posting Dt 51 Kt 76.09. Executed by the document “Receipt for settlement”, type of operation “Other receipts”;

- Subsidy calculation: posting Dt 76.09 Kt 86.01. Documented in the document “Operation entered manually.” At the same time, as much as was received was accrued according to the CT account 86.01.

Step 2. Purchased materials

Receipt of materials: posting Dt 10.01 Kt 60.01. It is drawn up with the document “Receipt (act, invoice)”. At the same time, an entry is made in the “STS Expenses” register.

Step 3. Transferred funds to the supplier

Money was transferred to the supplier for materials: posting Dt 60.01 Kt 51. Documented in the document “Write-off from the current account” with the type of transaction “Payment to the supplier”. And at this moment, after the transfer, there is an expense to KUDiR in the amount of the cost of purchased materials and input VAT.

Step 4. Income is recognized in the amount of expenses incurred

When an expense appears, it is necessary to simultaneously record income in the Income and Expense Book. Recognize income in accounting by posting Dt 86.01 Kt 91.01 with the document “Operation entered manually” and make an entry in KUDiR manually:

In other words, as much is reflected in the expense, you manually include this document in income. And so it was exactly for the first two years. This will be “keeping records of subsidy amounts,” that is, income is equal to expenses.

On the PROFBUKH8 website you can find other free articles and video tutorials on the 1C Accounting 8.3 configuration.

The features of the simplified taxation system, the capabilities of the 1C 8.3 program when applying the simplified tax system and how to avoid errors in accounting under the simplified tax system are discussed in our master class, where you can understand and understand how the legal requirements for the simplified tax system should be reflected in the 1C 8.3 Accounting program .

Give your rating to this article: (

4 ratings, average: 5.00 out of 5)

Registered users have access to more than 300 video lessons on working in 1C: Accounting 8, 1C: ZUP

Registered users have access to more than 300 video lessons on working in 1C: Accounting 8, 1C: ZUP

I am already registered

After registering, you will receive a link to the specified address to watch more than 300 video lessons on working in 1C: Accounting 8, 1C: ZUP 8 (free)

By submitting this form, you agree to the Privacy Policy and consent to the processing of personal data

Login to your account

Forgot your password?

Accounting and tax accounting of subsidies for disinfection and prevention of coronavirus

The rules for the formation in accounting of information on the receipt and use of state assistance provided to commercial organizations (except for credit organizations) are established by PBU 13/2000 “Accounting for state assistance” (approved by order of the Ministry of Finance of Russia dated October 16, 2000 No. 92n). To account for targeted financing, budgetary funds and other similar funds, account 86 “Targeted financing” is intended (Chart of accounts for accounting of financial and economic activities of organizations and Instructions for its application, approved by order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n).

According to 1C experts, for a situation where subsidies are provided as reimbursement (compensation) for expenses already incurred, account 86 need not be used.

The subsidy received by the organization to compensate for the costs incurred is attributed to the increase in the financial result of the organization and is taken into account in accounting as part of the organization’s other income (clause 10 of PBU 13/2000; clause 7 of PBU 9/99 “Income of the organization”, approved by order of the Ministry of Finance Russia dated 05/06/1999 No. 32n).

If the subsidy received will be used for future expenses, it is also inappropriate to post it through account 86, since the subsidy does not imply any reporting on the use of the funds received.

At the same time, an organization can optionally use account 86 to account for funds received, since there are no prohibitions on using account 86 in this situation.

Costs for which the subsidy was received are reflected in accounting as expenses in the usual manner.

“1C: Accounting 8” (rev. 3.0): how to prepare and send to the Federal Tax Service an application for a subsidy for coronavirus prevention measures

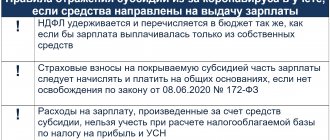

Subsidies received by SMEs from the federal budget due to the unfavorable situation associated with the spread of the new coronavirus infection are not taken into account in income for the purpose of calculating income tax (clause 60, clause 1, article 251 of the Tax Code of the Russian Federation).

At the same time, expenses due to subsidies specified in subclause 60 of clause 1 of Article 251 of the Tax Code of the Russian Federation are also not taken into account for the purpose of calculating income tax (clause 48.26 of Article 270 of the Tax Code of the Russian Federation).

note

, that subparagraph 60 of paragraph 1 of Article 251 of the Tax Code of the Russian Federation and paragraph 48.26 of Article 270 of the Tax Code of the Russian Federation were introduced by Federal Law No. 121-FZ of April 22, 2020 and apply to legal relations that arose from January 1, 2020.

VAT on goods (work, services) acquired through subsidies, including fixed assets, intangible assets and property rights, can be deducted in the general manner (clause 1 of Article 2 of Law No. 121-FZ).

When applying the simplified tax system (STS), neither subsidies received from the federal budget nor the costs for compensation of which subsidies were received are taken into account for the purpose of calculating tax when applying the simplified tax system (clause 1, clause 1.1, article 346.15, clause 2, art. 346.16 Tax Code of the Russian Federation).

1C:ITS

For more information about subsidies for small and medium-sized businesses affected by coronavirus, see the “Handbook of Business Operations. 1C: Accounting 8" section "Instructions for accounting in 1C programs", in the reference book "Answers to questions on 1C: Accounting 8 (rev. 3.0)".

Transactions with subsidies for capital investments

Budgetary (autonomous) institutions reflect transactions with these subsidies in the following order*(2):

1. Debit KDB1 6,205 62,561 Credit KDB1 6,401 40,162 - accrual of deferred income for the provision of subsidies for capital investments in the amount of the Agreement. 2. Debit KBK2 6,201 11,510 (increase in account 17, analytics code 150, KOSGU 162) Credit KDB1 6,205 62,661 - reflects the receipt of a capital subsidy. 3. Debit KDB1 6,401 40,162 Credit KDB1 6,401 10,162 - recognition of income in the form of a subsidy for capital investments as current year income based on information about the achievement of the conditions for the provision of a subsidy (Notice, Report, other document provided for by the Agreement). 4. Debit KDB1 6,401 40,162 Credit KDB1 6,205 62,661 - decrease in deferred income for subsidies for capital investments on the basis of the amended Agreement and (or) additional Agreement. 5. Formation at the end of the year of settlements for subsidies for capital investments on the basis of the Notice, Report on the fulfillment of the terms of the Agreement (transactions are reflected on the last day of the reporting year, unless otherwise provided by the founder): 5.1. Debit KDB1 6 401 40 162 Credit KBK3 6 303 05 731 - closing settlements in the amount of unused balances of the subsidy for capital investments, subject to return to the budget in the next year. 5.2. Debit KDB1 6,401 40,162 Credit KDB1 6,205 62,661 - closing settlements in the amount of unused financial support for the subsidy, if it was not transferred to the institution. 5.3. Debit KDB1 6,401 40,162 Credit KDB4 6,303 05,731 - formation of settlements for the unused balance in the presence of obligations assumed at the expense of it and unfulfilled (the need to confirm the need for these funds). When confirming the need, the entry is reflected: Debit KDB4 6,303 05,831 Credit KDB1 6,401 40,162. 5.4. If settlements with the founder under the subsidy are “closed” completely, but the institution still has accounts payable accepted at the expense of the subsidy funds (accepted and unfulfilled monetary obligations), then there is no need to record additional entries. The balance of funds in the personal account in the next year will be used to repay the accepted monetary obligation. 5.5. If, at the expense of a subsidy for capital investments, an advance was paid that was not confirmed by the counterparty’s documents for the reporting year, then the difference between the indicators Dt 6,205,62,000 and Kt 6,401,40,162 is equal to this advance. If a decision is made to return (not confirming the intended nature of the accepted monetary obligations), the operation specified in clause 5.1 is reflected in the next financial year. 6. Debit KBK3 6 303 05 831 Credit KBK2 6 201 11 510 (increase in account 18, analytics code 610, KOSGU 610) - return of the unused balance of the subsidy for capital investments of previous years.

More on the topic: Depreciation of fixed assets in government institutions

Operations with targeted capital subsidies

Budgetary (autonomous) institutions reflect transactions with these subsidies in the following order*(2):

1. Debit KDB1 5,205 62,561 Credit KDB1 5,401 40,162 - accrual of deferred income for targeted capital subsidies in the amount of the Agreement. 2. Debit KBK2 5,201 11,510 (increase in account 17, analytics code 150, KOSGU 162) Credit KDB1 5,205 62,661 - reflects the receipt of a capital subsidy. 3. Debit KDB1 5,401 40,162 Credit KDB1 5,401 10,162 - recognition of income in the form of a targeted capital subsidy as current year income based on information about the achievement of the conditions for the provision of a subsidy (Notice, Report, other document provided for by the Agreement). 4. Debit KDB1 5,401 40,162 Credit KDB1 5,205 62,661 - decrease in deferred income for targeted capital subsidies based on the amended Agreement and (or) additional Agreement. 5. Formation at the end of the year of settlements for capital subsidies on the basis of the Notice, Report on the fulfillment of the terms of the Agreement (transactions are reflected on the last day of the reporting year, unless otherwise provided by the founder): 5.1. Debit KDB1 5 401 40 162 Credit KBK3 5 303 05 731 - closing settlements in the amount of unused balances of targeted capital subsidies subject to return to the budget in the next year. 5.2. Debit KDB1 5,401 40,162 Credit KDB1 5,205 62,661 - closing settlements in the amount of unused financial support for the subsidy, if it was not transferred to the institution. 5.3. Debit KDB1 5,401 40,162 Credit KDB4 5,303 05,731 - formation of settlements for the unused balance in the presence of obligations assumed at the expense of it and unfulfilled (the need to confirm the need for these funds). When confirming the need, the following entry is reflected: Debit KDB4 5,303 05,831 Credit KDB1 5,401 40,162 5.4. If settlements with the founder under the subsidy are “closed” completely, but the institution still has accounts payable accepted at the expense of the subsidy funds (accepted and unfulfilled monetary obligations), then there is no need to record additional entries. The balance of funds in the personal account in the next year will be used to repay the accepted monetary obligation. 5.5. If, due to a targeted capital subsidy, an advance was paid that was not confirmed by the counterparty’s documents for the reporting year, then the difference between the indicators Dt 5,205,62,000 and Kt 5,401,40,162 is equal to this advance. If a decision is made to return (not confirming the intended nature of the accepted monetary obligations), the operation specified in clause 5.1 is reflected in the next financial year. 6. Debit KBK3 5 303 05 831 Credit KBK2 5 201 11 510 (increase in account 18, analytics code 610, KOSGU 610) - return of the unused balance of the targeted capital subsidy of previous years.

More on the topic: Filling out report 0503128 (0503738): what an accountant should know (Video materials for the 2021 annual reporting - topic 4)