Home / Taxes / What is VAT and when does it increase to 20 percent? / Declaration

Back

Published: 07/28/2017

Reading time: 6 min

0

434

According to the purchase and sale agreement, the seller's side is obliged to transfer the goods to the buyer into his ownership, and the buyer is obliged to accept it and pay the price - in monetary terms. In case of termination of the contract, the obligations cease.

The parties can agree and establish the return of what was carried out by them before the termination of the agreement. Thus, goods that are of poor quality and accepted for registration by the buyer are subject to return, provided that at the time of acceptance of the goods it was not discovered that their quality does not correspond to the terms of delivery.

If the sale of goods does not take place in the order of returning the goods to the seller, the original purchase and sale agreement is terminated and the original transfer of ownership is cancelled.

- Buyer Return Procedure

- The procedure for returning goods from a buyer without VAT to a supplier with VAT

- Accounting for VAT on goods return transactions

- Accounting entries

- Reflection in the declaration

Buyer Return Procedure

The buyer may exercise the right to refuse goods that were purchased under a sales contract, as well as the right to demand a refund of the amount paid for the goods, if:

- the seller transferred the goods in quantities less than those specified in the contract;

- a discrepancy between the range of transferred goods and the data in the contract was discovered;

- The product was found with irreparable quality defects in the form of defects or non-compliance with parameters.

- a fact was discovered that the product package did not correspond to that specified in the documents.

The parties to the contract may provide other reasons for the return, but if the above or other grounds are absent, the buyer does not have the right to demand a refund under the current sales contract.

Return may be possible by bilateral agreement: after it, the contract is considered terminated (Article 450 of the Civil Code of the Russian Federation). A document confirming termination must be made in the same form as the contract.

Returning goods may be possible before the invoice is certified and after, which means when ownership changes.

Products that do not meet the quality may be returned only with the consent of both parties. In this case, the seller and buyer change places for a while. Returns due to poor quality are subject to invoicing by the former buyer to the supplier for an amount equivalent to the product being returned.

If there was a fact of returning a product of inadequate quality, then in this case it is necessary to draw up a report on the discrepancy or defect, according to which the return process took place.

From the buyer

Let's look at an example of how it is necessary to reflect the return of goods to the supplier in order to correctly reflect the VAT deduction on the returned goods.

Initially, the receipt of goods from the buyer in accounting should be reflected in the document “Receipt of goods and services”, and on the basis of this document a “Invoice received” was created. The return of goods to the supplier must be reflected in a document of the same name (see Fig. 1). The way the return is reflected in accounting and VAT accounting is influenced by:

- Indication of the receipt document in the return document;

- Organizational accounting policy settings:

— maintaining batch accounting on accounting (Accounting policy (accounting) - Method of assessing inventories “FIFO” or “LIFO”);

— maintaining batch accounting for VAT accounting (Accounting policy (tax accounting) - The organization carries out sales without VAT or with 0% VAT);

- Maintaining analytical accounting of settlements with counterparties according to documents (Setting up accounting parameters - Analytical accounting of settlements with counterparties).

Rice. 1

Return indicating receipt document

When returning materials to the supplier indicating the receipt document (the “Receipt Document” detail of the “Return of Goods to Supplier” document), the return is reflected in the sales book. The return document generates movements for accrual of VAT in the corresponding registers “VAT accrued” (the line “VAT recovery” appears), “VAT settlements with suppliers”. Corresponding entries are generated in accounting and tax accounting.

If batch accounting is maintained for accounting and VAT purposes, and the specified batch is not found, this is reported to the user. In accounting, the posting of the document is stopped, and for VAT purposes the document is posted, but without movements in the “VAT on consignments of goods” register.

If a batch is found, movements are generated in the “VAT by inventory batches” register.

If upon receipt VAT on the specified document was included in the price, register movements and postings are formed taking this fact into account.

The “VAT included in the price” flag of the return document does not affect the processing.

Return without indicating receipt document

To reflect the sales ledger entry, the number and date of the invoice on which the return is reflected must be indicated. If the receipt document is not specified, based on the return, an “Invoice received” is created, which indicates the corresponding number and date, for which a hyperlink in the document form becomes available (see Fig. 2). This situation is possible when it is difficult to determine a specific receipt document. For example, valuables are purchased repeatedly from the same supplier.

Rice. 2

The return document itself is used as a document for VAT accounting purposes in the “VAT accrued” register.

If batch records are kept for accounting purposes, the returned batch is determined based on its data. The same batch is written off for VAT accounting purposes. In the case of the “average” method of assessing inventories, the batch for VAT purposes is determined according to VAT batch accounting data.

In this case, the written off batch does not affect the reflection of VAT in the sales book. If VAT on returned goods was included in the price upon receipt, you need to set the “VAT included in price” flag. In this case, there is no need to issue an invoice, since VAT will not be reflected in the sales ledger.

Postings for accounting and tax accounting are similar to the previous case; a return document is set as a subaccount “Invoices received” for the posting to the subaccount of the 19th account.

Payments to suppliers upon return

The reflection of settlements with suppliers for VAT purposes depends on the settings of the accounting parameters - the “Maintain settlements according to documents” flag in the “Analytical accounting of settlements with counterparties” section.

If the flag is not set, the return in the accounts payable registers is reflected as payment for the entire amount of the return, indicating it as a document. Payment for VAT purposes is reflected in the document “Registration of payments to suppliers for VAT”, which generates movements in the registers “VAT settlements with suppliers” (writing off debt on the receipt document and payment on the return document) and “VAT accounting of distributed payments to suppliers”. If the flag is checked, the return document reflects the write-off of the debt on the receipt document for VAT purposes; the debt is determined according to accounting data.

When part or all of the receipt has already been paid to the supplier, the return reflects the write-off of the debt only for the unpaid part (by the return document itself, or by the document “Registration of payment to the supplier”). The remaining refund amount is reflected as an advance to the supplier, which can then be returned by a payment document, or offset by another receipt document (both are reflected in the VAT subsystem as an advance offset (promptly) or by the document “Registration of payment to the supplier”).

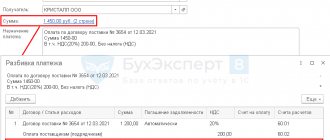

Issuing an invoice for returns

As explained in the letter of the Ministry of Finance of Russia dated March 7, 2007 No. 03-07-15/29, when returning goods to the supplier, the taxpayer must issue an invoice for the returned values and register it in the sales book.

To reflect the corresponding operation, you need to set the flag “The supplier is issued an invoice for return” in the document “Return of goods to the supplier”, and, using the hyperlink, create the document “Invoice issued” (see Fig. 3).

Rice. 3

When posting the document, VAT will be charged upon the return.

Reflection of returns in the sales book

An entry in the sales book is reflected in the document “Creating sales book entries.” The tabular part “VAT restored” is filled in automatically according to the data in the “VAT accrued” register.

If necessary, VAT restoration is reflected in line 190 of section 3 of the declaration.

If the return was reflected, as explained in the letter of the Ministry of Finance of Russia dated 03/07/2007 No. 03-07-15/29, VAT in the sales book is reflected as an accrual, the “VAT on sales” tab is filled in. In this situation, the return is reflected in the declaration as a VAT charge in lines 010-030 of section 3.

Reflection of returns in the purchase book

The configuration uses the same method for reflecting returns as in the sales book: if a receipt document is specified, this document is reflected in the “VAT presented” register; if not specified, the return document is reflected and an invoice is created.

If the return is reflected before applying the deduction on the receipt document, and with the indication of the receipt document itself, the entry in the purchase book is not reflected.

If the return is reflected in another tax period, after applying the deduction, or a canceling entry is reflected on the return document (return without indicating the receipt document), an entry for a negative amount is displayed in the purchase book. The entry is reflected in the “VAT Restoration” document.

The procedure for returning goods from a buyer without VAT to a supplier with VAT

If the buyer is recognized as a VAT defaulter, the procedure depends on whether the goods will be returned in whole or in part.

A full refund is issued in the seller's purchase book, namely, the previously issued invoice is registered. This is done on the date when he received the documents from the buyer.

A partial refund must be issued by the seller with a corrective invoice, which in amount must match the amount of the buyer's refund.

If the seller transferred the goods without providing an invoice, but using a cash register, then he needs to reimburse the buyer by entering the cash register details in the purchase book. In addition, the supplier needs to prepare a return receipt document.

However, despite the fact that the goods were returned by a VAT non-payer, the supplier can exercise the right to deduct VAT.

We process the return of goods - options are possible

The seller can deduct VAT on returned goods (work, services).

If the buyer has not returned all the goods, then VAT is deducted only on the cost of the “returned” goods. Please note: the deduction must be applied no later than one year from the date of return of the goods (clause 4 of Article 172 of the Tax Code of the Russian Federation).

Previously, there were two ways to process a product return.

- Refund based on adjustment invoice . If the buyer did not have time to register the returned goods, the seller issued him an adjustment invoice for the difference equal to the cost of the returned goods or part thereof. VAT on goods returned by the buyer was deducted by the seller on the basis of this adjustment invoice.

- Reverse implementation . If the buyer managed to register the returned goods, he had the right to reflect the return as a regular sale. At the same time, he issued an invoice to the former seller, registering it in the sales book. Based on this invoice, the former seller could deduct VAT on the returned goods.

Accounting for VAT on goods return transactions

The return of goods must be reflected in the accounting accounts. Return accounting periods :

- the purchase and return of goods were made in the same reporting period;

- after the end of the implementation year and before the period for submitting the declaration for the current year;

- upon submission of the annual declaration during which the goods were sold.

Land surveying of a summer cottage is a mandatory procedure for many transactions. Do I need to obtain a building permit if the land is owned? Find out about it here.

How to properly lease agricultural land? We talked about this in our article.

Return of goods to the supplier where reflected in the VAT return

There are also other legal grounds for refusal of obligations under the contract. However, the item must be sent back. Let's say because it is not in demand. This is possible when there is a corresponding provision in the contract. Or if you agree with the counterparty. The peculiarity of this situation is that the ownership of the purchase has already transferred to the buyer.

VAT payers at customs are persons recognized as taxpayers in connection with the movement of goods across the customs border of the Russian Federation and determined in accordance with the Customs Code of the Russian Federation. VAT charged when importing goods into the customs territory of the Russian Federation, according to Art. 318 of the Labor Code of the Russian Federation, is one of the types of customs payments. Since VAT payers at customs are determined according to the norms of customs law, Art.

We recommend reading: If the Dacha Costs Less than 1 Million Rubles and 5 Years have Not Elapsed since Privatization, Will There be a Sales Tax?

Both enterprises on OSN

In this case, both parties are VAT payers and delivery and return transactions are processed in the same way.

In order to return the goods to the seller, the transferring party issues the same set of documents that he received when purchasing the products. This is an invoice and delivery note for the transfer of goods. VAT must be included in the invoice.

Postings

The buyer must make such accounting entries:

- Dt 62 – Kt 90/1 – a return is issued (reverse sale).

- Dt 90/2 – Kt 41 – cost written off.

- Dt 90/3 - Kt 68 - shows VAT payable to the budget.

- Dt 60 – Kt 62 – mutual claims were offset.

The seller issues a return like this::

- Dt 41 – Kt 60 – goods from the buyer are accepted back to the warehouse.

- Dt 60 – Kt 51 – money returned.

- Dt 19 – Kt 60 – VAT allocated.

- Dt 68 – Kt 19 – accepted for VAT deduction.

Is it necessary to allocate tax for reimbursement?

The supplier, having received his goods back, must record this as a purchase and allocate VAT for reimbursement . Therefore, the refund amount is entered in line 120 of section III.

The buyer has a sale, which is reflected on line 010 of section III, and the amount of VAT payable is indicated on line 120 of the same section.

How to indicate receipt of income?

The corresponding entries must be made in the income tax return.

- If the return occurred in the same tax period as the shipment, then the supplier reduces the figures on lines 010 and 030 of sheet 02 by the amounts of delivery and return.

- In the case when the goods were returned in the next tax period, the amount of expenses must be reflected according to period 010 on sheet 02, Appendix No. 2.

The buyer must show the proceeds from the sale, i.e. line 010 of sheet 02 reflects the refund amount.

Returning goods to the supplier in the VAT declaration

The opinion of the controllers was voiced in subcategory 101.19 EBNZ 1. “... when returning a preliminary (advance) payment to a VAT defaulter, the supplier does not adjust tax liabilities, regardless of the reasons for such a return, including in connection with the termination of an agreement for the supply of goods/services.” However, now the status of the clarification has been changed to “not valid”, and in the current response from subcategory 101.07 EBNZ, the controllers have already made a positive conclusion for taxpayers: “... the seller - a VAT payer has the right to write out a calculation of the adjustment to the tax invoice and reduce the accrued amount of tax liabilities for VAT.”

Let's consider the operation of returning goods by a buyer in the program using a specific example. Suppose that on 05/18/07 the organization Rassvet shipped to the counterparty Buyer a batch of goods in the amount of 100 units. total cost 23,600 rubles.

Returning goods to the supplier VAT declaration

In the event that the buyer returns objects from the seller to the seller, the sales turnover for these objects is reduced by the amount of sales turnover for the tax period in which the objects were returned (clause 5 of the Instructions on the procedure for filling out the purchase book, tax return (calculation) for value added tax , tax return for value added tax on goods imported from the Russian Federation, calculation of reimbursement from the budget for amounts of value added tax, approved by Resolution of the Ministry of Taxes of the Republic of Belarus dated 02/05/2021 No. 22 (hereinafter referred to as Instruction No. 22)).

In this case, the seller can claim VAT on the advance payment. Also, the right to deduct tax accrued on the proceeds from the sale arises with the selling company and upon their return by the buyer. For the procedure for applying VAT deductions in such situations, read the article prepared based on the materials of the reference book “Annual Report – 2021” by the Garant-Press publishing house.

Resale or return of goods accepted for accounting

The procedure for processing a return depends on whether the product is accepted for accounting or not. Civil law considers return only the transfer of goods/services of inadequate quality or inappropriate parameters. Therefore, when returning high-quality goods by agreement of the parties, we can talk exclusively about fraternal sales, and not about return, since all the conditions of the original contract were fulfilled by the counterparties.

When deciding to transfer the purchased goods back, the parties enter into a new agreement in which their responsibilities change - the former buyer becomes the seller, draws up documents accompanying the sale of goods (agreement, invoices, invoices), records the transaction in the sales book, pays VAT accepted earlier for deduction (letter of the Ministry of Finance of the Russian Federation dated 04/07/2015 No. 03-07-09/19392).

For the supplier (and in the case of a return transaction, the buyer), the invoice is the basis for reflecting in the purchase book and deducting previously paid VAT.

Such actions are regarded by the Tax Code of the Russian Federation as a fact of ordinary sales, i.e. they do not entail any tax consequences, even if the goods were accepted and “returned” in different reporting periods.

When selling goods back, you do not need to submit an updated declaration. In this case, the return to the supplier will be reflected in the VAT return as follows:

- the buyer records the cost of the returned (and essentially sold) goods in lines 010 (VAT 18%) or 020 (VAT 10%) of section 3 of the declaration,

- the seller indicates the amount of deduction for goods received back in line 120 of section 3.

Example:

Trio LLC supplies furniture to Duet LLC in the amount of 118,000 rubles. (including VAT 18,000 rubles). Duet LLC receives the goods, but then, due to reorganization, refuses it, and Trio LLC agrees to return it. Duet LLC formalizes the transaction by drawing up a purchase and sale agreement, issues an invoice, and a delivery note for the same amount. In the VAT return, both companies will indicate in the 3rd section on page 010 in gr. 3 the amount of goods sold is 100,000 rubles, according to gr. 5 the amount of VAT is 18,000 rubles, on line 120 - the amount of tax to be deducted is 18,000 rubles.

Reflection of returns in the seller's accounting

Like any other fact of the economic life of an organization, returns must also be reflected in accounting. Moreover, entries made earlier will have to be reversed. The reversal will have to be made according to the following postings.

| Operation | Contents of operation |

| D62 K90/Revenue | The amount of revenue is reversed by the cost of goods that were returned |

| D90/Cost price K41 | A reversal of the cost that was written off for returned goods is carried out. |

| D90/VAT K68/VAT calculations | VAT is deductible from the cost of goods that were returned. |

Returning goods to the supplier in the VAT declaration

In the previous issue, we analyzed in detail the issues related to the return of low-quality goods in the wholesale trade. At the same time, the seller and buyer have every right in the supply agreement to provide for the grounds and procedure for returning quality products to the seller. Let's consider the accounting procedure for such business transactions.

In accordance with paragraph 5 of Article 171 of Chapter 21 Value Added Tax of the Tax Code of the Russian Federation, amounts of value added tax presented by the seller to the buyer and paid by the seller to the budget when selling goods are subject to deduction in the event of their return. When returning goods accepted for registration, the buyer is obliged, in the manner established by paragraph 3 of Article 168 of the Code, to issue the corresponding invoice to the seller and register a second copy of the invoice in the sales book.

What is the procedure for accounting for VAT when returning goods to the supplier?

However, officials think differently: from their point of view, the return of goods by the buyer is recognized as a sale if the goods are registered on the date of return. The reasons why the item is returned does not matter. This means that such returns of goods are subject to VAT on a general basis. In this case, the buyer must issue an invoice (see, for example, letters of the Ministry of Finance of Russia dated November 29, 2021 N 03-07-11/51923, 08/10/2021 No. 03-07-11/280, 08/07/2021 No. 03-07- 09/109 and 07/31/2021 No. 03-07-09/100, as well as the Federal Tax Service of Russia dated 07/05/2021 No. AS-4-3/). In other words, the buyer issues a return of low-quality goods through regular sales and charges VAT.

We recommend reading: Agreement on Compensation of Damage for Lost Rented Property

Since there is no transfer of ownership of the defective goods, the buyer does not issue an invoice on his own behalf, and the supplier issues an adjustment invoice, having agreed on the amount of the defective goods with the buyer (resolution of the Federal Antimonopoly Service of the Volga District dated 02.12.2021 in case No. A65-14995 /2021, resolution of the Federal Antimonopoly Service of the Moscow District dated December 7, 2021 in case No. A40-54535/12-116-118).

HOW TO REFLECT THE RETURN OF GOODS IN THE VAT DECLARATION

- in section 8 – information about the invoice registered in the purchase book when returning goods by the buyer (clause 45 of the Procedure for filling out the declaration). Read about which invoice is registered in the purchase book when returning a quality product here, and a low-quality product here;

the buyer returns the goods to him, the seller accepts for deduction the VAT accrued upon their shipment. In the VAT return for the quarter in which the returned goods were received from the buyer, the seller reflects: