The release of finished products is often accompanied by the formation of residues of raw materials, which to one degree or another have lost their original properties. They are called waste, and if it is possible to reuse it in the main or auxiliary production, as well as resell it to consumers, then such waste is returnable. For example, dairy production is always accompanied by the formation of whey products, and forest processing - sawdust and chips; returnable waste in the confectionery industry is benign residues after cutting candy layers, deformed candy bodies (depending on the composition, they are reused in the preparation of special types of candies, syrups).

And although the concept of “returnable waste” is absent in accounting legislation, it is specified in some industry instructions. In particular, paragraph. Methodological recommendations for accounting for production costs, approved. by order of the Ministry of Agriculture dated 06.06.2003 No. 792, this term denotes the remains of raw materials, goods and materials, coolants and other resources formed during the production of products, which have to some extent lost the properties of the original material and are therefore used with an increase in costs (reduction in product yield). Let us recall the features of accounting for such assets.

Returnable waste in accounting

So, returnable production waste is the by-products of processing raw materials in the main production, the occurrence of which requires appropriate accounting. It is regulated by clause 111 of the Guidelines for accounting for inventories, approved. by order of the Ministry of Finance of the Russian Federation No. 119n dated December 28, 2001, requiring:

- determine the value of waste based on the price of possible use or sale;

- deliver to the warehouse using invoices indicating the name and quantity;

- release returnable waste (WW) for further use in the manufacture of products according to the invoice requirements.

The cost of recorded waste should reduce the cost of inventory items released into production. Let us clarify: we are talking about reducing the cost of raw materials, during the processing of which waste was generated. They must be received at the time of their occurrence, and in the same reporting period the cost of initial resources should be reduced. VO is assessed depending on the prospects for further use:

- at the price of possible use, if the waste is subjected to subsequent processing in the enterprise;

- at the market value of inventory items, if VOs are sold as a full-fledged resource.

The enterprise is obliged to choose a method for setting the price of VOs at which they must be accounted for, fixing it in its accounting policies.

Examples

Let's consider how the return of goods to the supplier is processed (accounting entries in different conditions, naturally, will differ).

The seller shipped valuables in the amount of 11.8 thousand rubles. (VAT - 1800 rubles). Cost – 8 thousand rubles. The buyer paid the invoice for the full amount, and then discovered the defect and returned the entire shipment to the seller.

| Amount (thousand rubles) | DT | CT | Operation |

| 8 | 90.2 | 41 | Cost written off |

| 11,8 | 62 | 90.1 | Revenue taken into account |

| 1,8 | 90.3 | 68 | VAT charged |

| 11,8 | 51 | 62 | Payment taken into account |

| 11,8 | 62 | 76 | A claim has been made |

| -11,8 | 62 | 90.1 | The goods sale operation is reversed |

| -1,8 | 90.3 | 68 | |

| -8 | 90.2 | 41 | |

| 11,8 | 76 | 51 | Money returned |

The goods were returned to the supplier after payment. Therefore, account 76 “Settlements with debtors and creditors” was introduced in the postings. After reversal, the buyer incurred accounts payable. This amount is reflected in account 76. After the funds are returned, the final balance is reset to zero. That is, the same account is used for settlements with debtors and creditors. Here's how to return goods to the supplier after payment for the shipment.

| Sum (thousand roubles.) | DT | CT | Operation |

| 10 | 41 | 60 | Goods received |

| 1,8 | 19 | 60 | VAT |

| 1,8 | 68 | 19 | The tax is deducted |

| 11,8 | 60 | 51 | Payment for goods |

| 11,8 | 76 | 60 | The supplier accepted the claim |

| -10 | 41 | 60 | The sales transaction is reversed |

| -1,8 | 19 | 60 | |

| -1,8 | 68 | 19 | VAT restored |

| 11,8 | 51 | 76 | Money returned |

Such postings are generated if goods are returned of inadequate quality, of a different assortment, or with incorrectly executed documents.

Returnable production waste: postings

Since in accounting VOs are materials, their accounting in accordance with the Chart of Accounts is carried out in a specially opened subaccount to account 10 “Materials” - 10/12 “Other materials”.

To control the safety of VO, the company organizes analytical accounting by types and places of occurrence, arriving by posting D/t 10/12 K/t 20, 23, 29, thus reducing the cost of goods and materials transferred to production.

The algorithm for collecting and transferring VO to the warehouse is fixed by the company’s internal local regulations. In accordance with the specifics of production, the amount of generated waste is calculated in the most appropriate way - by weighing, recalculation or, if it is impossible to directly determine their quantity, by applying the established standard to the volume of finished products produced for a specific period.

The receipt of returnable waste from production to the warehouse is formalized with a delivery note, a receipt order (Form M-4), a demand invoice (Form M-11) or an invoice for internal movement (TORG-13). The transfer of VO from the warehouse for subsequent processing is accompanied by the preparation of a new demand-invoice, and for sale - one of the forms M-15 or TORG-12. An enterprise has the right to operate with other primary accounting documents approved for use in accounting policies.

Accounting entries for accounting for returnable waste in production will be as follows:

| Operation | D/t | K/t |

| Raw materials for production were transferred from the warehouse | 20,23,29 | 10/1 |

| Returnable waste from the main production has been capitalized | 10/12 | 20,23,29 |

| VO transfer: | ||

| - for further use in production | 20 | 10/12 |

| - for implementation | 91/2 | 10/12 |

| Proceeds from the sale of VO | 62 | 91/1 |

| VAT is charged on the cost of VO | 91/2 | 68 |

We return materials with defects discovered after acceptance

How can a manufacturing enterprise record the purchase of materials, their return to the seller due to the fact that defects were found in them after acceptance, as well as the submission of transportation costs to him for reimbursement?

The manufacturing enterprise (buyer), under a purchase and sale agreement with the condition of subsequent payment, purchased materials in the amount of 2,400 rubles, including VAT (20%) of 400 rubles. According to the contract, transportation costs are borne by the buyer. To transport materials, the company entered into an agreement with a transport organization with the condition of subsequent payment in the amount of 60 rubles, including VAT (20%) 10 rubles.

Having discovered deficiencies after accepting the materials, the company, in accordance with the contract, returned the materials to the seller, for which it used the services of a transport organization. The cost of transportation of returned materials is 55 rubles, including VAT (20%) 9.17 rubles.

The company filed a claim with the seller for damages (transportation costs for delivery and return of low-quality materials) in the amount of 115 rubles. In the same month, funds were received into the company’s bank account as reimbursement for transportation expenses.

At the time of return, the company had not paid for the materials. According to the accounting policy, the company does not use accounts 15 and 16. The return of low-quality materials to the seller (supplier) in accordance with the contract is reflected in accounting records as reversal entries.

General provisions

Under a purchase and sale agreement, the seller undertakes to transfer ownership, economic management, and operational management of the property (thing, product) to the buyer, and the buyer undertakes to accept this property and pay a certain amount of money (price) for it <*>.

Requirements for the quality of goods are the most important element of the purchase and sale agreement. Thus, the seller is obliged to transfer to the buyer a product whose quality meets the requirements specified in the sales contract. If these are not established, the seller must transfer to the buyer goods suitable for the purposes for which goods of this kind are usually used. In cases where the requirements for the quality of the goods being sold are established by law, the seller must transfer the goods that meet these requirements <*>.

Checking the quality of the goods, as well as the procedure for its implementation, may be provided for by law or the purchase and sale agreement. If such a procedure is not determined by either one or the other, they are guided by the usually applied conditions for checking the goods to be transferred under the purchase and sale agreement <*>.

The buyer may discover a discrepancy in the quality of the goods after acceptance. In this case, a report on hidden defects is drawn up, which is presented to the seller within the time limits allotted by law or the contract for the buyer to identify hidden defects of the product <*>.

A buyer who has been sold a product of inadequate quality has the right to refuse to fulfill the sales contract and demand that he be compensated in full for the losses caused, unless otherwise provided by law or an agreement corresponding to the law <*>. And the seller is obliged to compensate the buyer for losses caused by non-fulfillment or improper fulfillment of contractual obligations <*>.

In this situation, the seller compensates the buyer for losses associated with the delivery and return of low-quality materials, namely the cost of delivery and return of low-quality materials.

Accounting

Materials, as they are received, are accepted for accounting as inventories at actual cost, which is the sum of the organization's actual costs for their acquisition and includes, among other things, transportation costs for delivery <*>.

Actually received materials are accounted for as a debit to account 10 and a credit to account 60 <*>.

The basis for acceptance and posting of materials are accompanying documents (TTN, TN, etc.) (clause 26 of Instruction No. 133).

In the situation under consideration, according to the accounting policy, the receipt of materials is reflected without using accounts 15 and (or) 16. This means that transportation and procurement costs are accepted for accounting by directly (directly) including them in the actual cost of the material (attachment to the purchase price of the material) with a debit reflection accounts 10 <*>.

If the buyer returns materials of inadequate quality, the purchase and sale agreement is terminated. Return of materials using transport is issued by TTN. The seller reflects the business transaction for the return of materials in the accounting accounts on the date of its completion, namely on the date of return <*>.

The buyer, according to the author, can show the return of low-quality materials in accordance with the contract in accounting with reversal entries, enshrining this procedure in the accounting policy <*>.

Settlements for claims presented to sellers are recorded in account 76-3 “Settlements for claims.” The buyer, for the amount of transportation costs for the delivery and return of materials subject to reimbursement, makes an entry to the debit of account 76-3 and the credit of account 60 <*>.

The difference between the amount to be reimbursed by the seller and delivery costs excluding VAT, in the author's opinion, relates to other income from current activities in the reporting period in which the seller acknowledged the claim. In the accounting of the enterprise, it is reflected in the debit of account 76-3 in correspondence with the credit of account 90 90-7 <*>.

The receipt of funds to the buyer from the seller as compensation for losses is shown in the debit of account 51 and the credit of account 76-3 <*>.

Repayment of obligations to the transport organization is reflected in the debit of account 60 and the credit of account 51 <*>.

VAT

VAT amounts presented by the seller and transport organization for purchased materials and transport services are tax deductions for the organization. They are subject to deduction after being reflected in accounting and the purchase book (if maintained) on the basis of the ESCHF, received respectively from the seller and the transport organization and signed with the electronic digital signature of the enterprise <*>.

The submitted VAT is reflected in the accounting as the debit of account 18 and the credit of account 60. The VAT subject to deduction is shown in the debit of account 68-2 and the credit of account 18 <*>.

In case of a full return of materials, the seller sends the buyer an additional ESCHF with reference to the original <*>.

The buyer makes a downward adjustment of tax deductions regardless of the fact that he signed or did not sign an additional ESCHF in the reporting period in which the goods are returned, in section II and in line 1 of section IV of the VAT declaration <*>.

In accounting, the amount of VAT claimed for deduction is reversed. Invoice 18 is adjusted on the basis of the TTN, which is used to document the return of the goods to the seller.

The amount of reimbursement of transportation costs by the seller is not subject to VAT from the buyer, since in the situation under consideration there is no fact of sale of these services <*>.

Situations where amounts of “input” tax are not deductible are indicated in clause 24 of Art. 133 NK. This does not include reimbursement of transportation costs by the seller to the buyer in connection with the return of low-quality materials. Thus, the enterprise has the right to accept for deduction the amount of VAT presented by the transport organization in the generally established manner, taking into account the conditions specified in subparagraph. 5.1 clause 5 art. 132 NK.

Income tax

Reimbursement of transportation costs by the seller as an amount transferred to compensate for losses is reflected by the buyer as non-income on the date of receipt from the seller <*>.

Within the limits of this compensation, losses from writing off transportation costs are taken into account as non-expenses. Such expenses are reflected on the date of receipt of compensation, but not earlier than their actual implementation <*>.

Accounting Entry Table

Sub-accounts have been opened for account 60:

— 60-1 “Settlements with the seller”,

— 60-2 “Settlements with transport organizations.”

| Contents of operation | Debit | Credit | Amount, rub. | Primary document |

| When purchasing materials | ||||

| The posting of materials is reflected (2400 — 400) | 10 | 60-1 | 2000 | TTN, warehouse card, receipt order, contract of sale |

| VAT is reflected on purchased materials | 18 | 60-1 | 400 | TTN |

| Accepted for deduction of VAT on purchased materials | 68-2 | 18 | 400 | ESChF, TTN, purchase book (if maintained), accounting certificate-calculation |

| Transport services for the delivery of purchased materials are included in the increase in their cost (60 — 10) | 10 | 60-2 | 50 | Certificate of work performed (services rendered), accounting certificate-calculation |

| VAT is reflected on transport costs for the delivery of purchased materials | 18 | 60-2 | 10 | Certificate of work performed (services rendered), accounting certificate-calculation |

| Accepted for deduction of VAT on transport costs for the delivery of purchased materials | 68-2 | 18 | 10 | ESChF, certificate of work performed (services provided), purchase book (if maintained), accounting certificate-calculation |

| Payment to the transport organization for delivery is transferred | 60-2 | 51 | 60 | Payment order, bank account statement |

| When returning materials | ||||

| REVERSE Receipt of materials (return of materials) | 10 | 60-1 | 2000 | Hidden Defects Act, TTN, warehouse card, accounting certificate-calculation, contract of sale |

| REVERSE VAT on purchased materials | 18 | 60-1 | 400 | TTN, accounting certificate-calculation |

| REVERSE Accepted for deduction of VAT on purchased materials | 68-2 | 18 | 400 | ESChF, TTN, purchase book (if maintained), accounting certificate-calculation |

| STORNO Transport services for the delivery of purchased materials | 10 | 60-2 | 50 | Certificate of work performed (services rendered), accounting certificate-calculation |

| Reflects the cost of transport services for the delivery of low-quality materials, subject to reimbursement, excluding VAT | 76-3 | 60-2 | 50 | Claim, accounting certificate-calculation |

| The cost of transport services for the return of low-quality materials subject to reimbursement is reflected, excluding VAT (55 — 9,17) | 76-3 | 60-2 | 45,83 | Claim, accounting certificate-calculation |

| VAT is reflected on transportation costs for the return of purchased materials | 18 | 60-2 | 9,17 | Certificate of work performed (services rendered), accounting certificate-calculation |

| Accepted for deduction of VAT on transportation costs for the return of purchased materials | 68-2 | 18 | 9,17 | ESChF, certificate of work performed (services provided), purchase book (if maintained), accounting certificate-calculation |

| The difference between the amount to be reimbursed by the seller and delivery costs excluding VAT is reflected as part of other income from current activities when the claim is recognized by the seller (115 — 50 — 45,83) | 76-3 | 90-7 | 19,17 | Accounting certificate-calculation, claim, letter of acceptance of claim |

| Received funds from the seller as compensation for losses <*> | 51 | 76-3 | 115 | Payment order, bank account statement |

| Payment to the transport organization for delivery is transferred | 60-2 | 51 | 55 | Payment order, bank account statement |

| ——————————— <*> The amount of reimbursement of transportation costs is 115 rubles. taken into account when taxing profits as part of non-income on the date of its receipt from the seller <*>. As part of non-expenses when taxing profits, losses from writing off transportation costs (excluding VAT) in the amount of 95.83 rubles are taken into account. (50 + 45.83) on the date of receipt of compensation, but not earlier than their actual implementation <*>. | ||||

Read this material in ilex >>*

* following the link you will be taken to the paid content of the ilex service

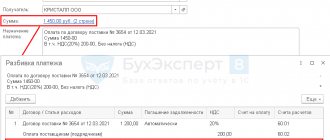

Return of materials from production to the warehouse in 1C Accounting 8

In enterprises, especially production materials, materials are released from the warehouse every day, but sometimes it happens that materials are returned back.

In this article we will look at how the return of materials from production to the warehouse is reflected in the 1C Accounting program 8th edition. 3.0. In accounting, the return of materials to the warehouse is documented by posting:

Dt 20 Kt 10 reversible. In the program it is shown in red and with a minus sign.

Also, the debit may have a different account, for example, 23, if the materials are returned not to the main, but to auxiliary production.

For income tax purposes, returned materials are not considered an expense (clause 5 of Article 254). The return of materials also does not count as income, so they are not taken into account in tax accounting.

For enterprises using the simplified tax system with a taxable income minus expenses, the procedure for recognizing material expenses will be similar to the income tax. Therefore, the cost of materials returned from production will not be an expense. This will not apply to income either.

Return of materials from production to the warehouse in 1C Accounting 8 ed. 3.0

In the 1C Accounting program 8th edition. 3.0 the return of materials from production to the warehouse is reflected in the document “Production Report for the Shift”. You can find it on the “Production” tab, “Product Output” section.

The document will contain the “Returnable waste” tab. At the top you need to indicate the account from where the materials will be returned. In our example, this will be the account 20.01. The warehouse to which materials will be transferred and the department from which they are returned.

In the tabular part of the document, you need to select from the product catalog the material that is being returned to the warehouse, indicate the quantity, price and product group, if it is not filled in automatically. The item group will be filled in if it is indicated in the material card; if not, it must be filled in manually.

After posting the document, the following posting will be generated:

The transaction amount is shown with a minus, which means that it will be subtracted when calculating the totals.

Have a question for a lawyer?

Delivery of the material - the costs of its transportation are business expenses of the contractor himself and should not be paid by you; in this case, you only pay for the material itself according to those invoices with their cost that the contractor will present to you

The provisions of Art. 32 of the Law “On the Protection of Consumer Rights” the consumer has a special right to unilaterally refuse to provide services or perform work by the contractor. Moreover, it can only be based on the personal desire of the consumer and should not have any specific grounds. The opinion of the contractor in this situation is not taken into account; he, having received from the consumer a notice of refusal of a bilateral contract, is obliged to return the funds paid upon its conclusion. When making settlements with the consumer, he can deduct from the refunded amount the expenses that were actually incurred by him in performing these particular works or providing services, depending on the nature of the agreements.

It is important that when making deductions, the contractor must justify them appropriately by providing the consumer with evidence of expenses. At the same time, the terms for the return of funds are not regulated by current legislation, therefore the consumer has the right to take advantage of the provisions of Art. 314 of the Civil Code of the Russian Federation and demand a refund within 7 days from the date of receipt of the notification. If you disagree with the amount of the refunded amount, the consumer has the right to file a claim in court.

Elena, if you have any questions, ask, I will be happy to answer. You can also write to me in the chat and order a personal consultation or preparation of a document on your question. All the best!