Working hours - what is it?

Most employers make a mistake when they confuse two concepts - “summary accounting” and “working hours”.

Summarized accounting is not a working time regime, but a method of keeping records of working time, a method of fulfilling the requirement contained in Art. 91 of the Labor Code of the Russian Federation states that the employer is obliged to keep records of the time actually worked by each employee. The concept of working hours is defined in Art. 100 of the Labor Code of the Russian Federation, where you should especially pay attention to the norm, which sounds imperative: “the working hours must provide for...”. The following lists everything that should be specified by the employer in the internal labor regulations or, if the working hours for the employee differ from the established rules (for example, he is a part-time worker or an employee with whom an agreement on part-time work is agreed), in the employment contract:

- length of the working week (five-day with two days off, six-day with one day off, working week with days off on a rotating schedule, part-time work week);

- work with irregular working hours for certain categories of workers;

- duration of daily work (shift), including part-time work (shift);

- start and end times of work;

- time of breaks from work;

- number of shifts per day;

- alternation of working and non-working days, which are established by internal labor regulations and an employment contract.

A special type of working time recording – summarized

Summarized accounting is, in fact, a special operating mode based on compliance with certain schedules (as a rule, these are “sliding” or shift schedules).

The basis for establishing such schedules is the reason “by contradiction” - when it is not possible to plan the regime in such a way that the working week is the fixed number of hours provided for by the norms of Art. 91-92 Labor Code of the Russian Federation:

- 24 – for youth under 16 years of age;

- 35 – for those with a disability group;

- 36 – for teachers and workers in hazardous industries;

- 39 – for doctors

- 40 hours is the standard duration.

A working week cannot include more than 40 hours.

With RMS, shortcomings during one period can be compensated by processing in other time intervals, which in total reaches the result required by the standard.

Flexible working hours

Flexible working hours are the only working hours that eliminate the need to prescribe the duration of daily work and the start and end times of the working day. According to Art. 102 of the Labor Code of the Russian Federation, when working in flexible working hours, the beginning, end or total duration of the working day (shift) is determined by agreement of the parties. The employer ensures that the employee works the total number of working hours during the relevant accounting periods (working day, week, month and others).

The alternation of weekends and working days, the length of the week will be determined in the labor regulations. In this case, it is impossible to change the schedule unilaterally. To change the schedule, you must either ask for the employee’s consent, or justify this by changes in organizational or technological working conditions.

Despite the fact that the Labor Code does not say a word about the fact that with a flexible working time schedule it is necessary to keep summarized records, the concept of a flexible schedule itself presupposes the introduction by the employer of summarized recording of working hours, since he will not be able to ensure that the norm is worked out within a certain day and will set the accounting period - week, month, etc.

Online training on current topics in accounting and tax accounting

To learn more

Salary calculation

Salary or tariff rate is the most common form of remuneration in Russia. The employer assigns the employee a specific salary or rate for a fully worked norm. The calculation of overtime working hours at a salary is calculated based on the hourly share of the salary or rate.

First, the accountant calculates the cost of one hour of work for a specific specialist. There are several ways to calculate the hourly rate. For example, it is enough to divide the official salary by the number of working hours in the billing month. Or another option: we divide the salary by the average annual working time (standard working hours per year / 12 months).

IMPORTANT!

The method for calculating the hourly share of the salary or tariff rate must be enshrined in the local acts of the institution. Calculation based on the average annual working time is more beneficial for workers (Letter of the Ministry of Labor dated 08/09/2002 No. 1202-21).

The result obtained remains to be multiplied by the number of hours worked, taking into account the increasing factor. That is, we multiply the hourly salary by a factor of 1.5 for the first 2 overtime hours. The remaining processing time is calculated with a factor of 2.

Shift work

In a situation with summarized accounting of working hours, concepts such as “shift work” and “working week with days off on a staggered schedule” are often confused. It is worth keeping in mind that these are two different working hours.

Art. 103 of the Labor Code of the Russian Federation defines shift work as work in two, three or four shifts, which “is introduced in cases where the duration of the production process exceeds the permissible duration of daily work, as well as for the purpose of more efficient use of equipment, increasing the volume of products or services provided” .

The most important condition for shift work is the rotation of workers (one shift/team replaces another). In case of shift work, the employer is obliged to familiarize the employee with the shift schedule no later than one month before it comes into force. Working two shifts in a row is prohibited.

With a shift schedule

When calculating total time, the most common mode is working in shifts. It is being implemented in companies with round-the-clock work, as well as in those where the duration of daytime work exceeds 8 hours a day.

In the first case, the number of shifts, taking into account the need for proper rest and recovery after work, should not be less than 3 - 4. It all depends on the duration of work. If it is within 12 hours a day, then 2 shifts of employees are sufficient.

In this case, the employer is obliged:

- distribute workers into shifts evenly in order to fully cover the entire technological process;

- determine how long a shift takes to complete, taking into account rest;

- draw up a shift schedule for the entire duration of the period;

- familiarize all employees with this document and sign it.

The shift schedule is drawn up taking into account annual leave periods (they should be provided according to a predetermined schedule), as well as a small reserve in case of illness of individual employees.

The required reserve is calculated by dividing the total unworked time for the previous year by the normal duration of work time for the same period. Calculations help you decide whether to hire additional people or pay extra to existing ones.

Remember, the duration of the summary accounting period when working in shifts is set so as to exclude overtime after its completion.

Basic rules of summarized accounting

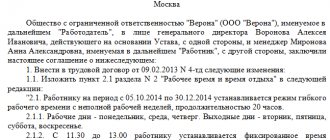

Non-standard working hours, flexible working hours, staggered days off, shift work require keeping a summary record of working time.

The main document that needs to be relied upon in this case is Art. 104 Labor Code of the Russian Federation. It answers the question in which cases the introduction of summarized accounting is allowed: when the daily or weekly duration established for a given category of workers (including workers engaged in work with harmful and (or) dangerous working conditions) cannot be observed.

The meaning of summarized recording of working time is to select a certain accounting period so that, based on its results, the duration of working time does not exceed the normal number of working hours.

To account for the working time of workers engaged in work with harmful and (or) dangerous working conditions, the Labor Code establishes an accounting period of three months, however, there is a caveat: for workers engaged in work with harmful and (or) dangerous working conditions, due to the peculiarities technological process or for seasonal reasons, it is possible to increase such an accounting period for a period of more than three months, but in the presence of an industry agreement and a collective agreement and to no more than one year.

The normal number of working hours for the accounting period is determined based on the weekly working hours established for this category of workers. For employees working part-time (shift) and (or) part-time week, the normal number of working hours for the accounting period is reduced accordingly.

Hassle-free HR records management

Try it

What length of working hours will an employee working on a “every three days” schedule have? In this case, we must proceed from the generally accepted norm: normal working hours do not exceed 40 hours per week. The employer establishes a certain accounting period within which these hours are distributed as desired, the main thing is to reach the standard hourly rate based on the results of the accounting period.

Moreover, if the employer does not take the generally accepted working hours - 40 hours a week, but, for example, a 39-hour work week, then he will have to create his own production calendar.

The Order of the Ministry of Health and Social Development of the Russian Federation dated August 13, 2009 No. 588n states the rules by which the standard working time is determined: “the length of the working week (40, 39, 36, 30, 24, etc. hours) is divided by 5, multiplied by the number of working days according to the calendar of the five-day working week of a particular month and from the resulting number of hours the number of hours in a given month is subtracted by which working hours are reduced on the eve of non-working holidays.”

Judicial practice shows that the essence of the summarized accounting of working time is to adjust the duration of time worked within the accounting period (month, quarter or year), if it deviates from the established norm, that is, overtime on some days is compensated by underwork on others (Resolution of the Federal Antimonopoly Service of the Central District dated 07/03/2006 in case No. A62-5389/2005).

Summarized accounting of working time, according to Art. 104 of the Labor Code of the Russian Federation, is carried out in accordance with established internal labor regulations.

Thus, to introduce summarized accounting it is necessary to follow a certain algorithm:

- determine the duration of the accounting period;

- determine the standard hours for the accounting period based on the weekly working hours established for this category of employees;

- make a schedule;

- establish a procedure for determining overtime hours;

- establish a procedure for paying overtime and work on weekends/non-working holidays.

Accounting periods and norms

In any organizations, and not just those where summarized recording of working hours is established, it is very important that the norm of hours worked, which is recorded by the schedule and time sheet, is observed. Only in this case will it be possible to say that the labor legislation of the Russian Federation is not violated.

Before the production rate that one or another mode of work activity implies is indicated, it is necessary to understand what the accounting period is.

What is an accounting period? An accounting period is a specific time period that can last a quarter, a month, a year, but not exceed a period of more than 1 year. In addition, legislative rules establish that if the enterprise has conditions that are harmful or life-threatening to employees, then in such a case the accounting period cannot exceed 3 months.

Only in this situation will the labor standard be observed.

Thus, we come to the conclusion that the accounting period is a period that allows you to correctly calculate the number of hours worked by an employee and enter them into the time sheet. If the production rate is exceeded, then in such cases we can talk about such a phenomenon as overtime.

The provision on cumulative recording of working hours allows us to calculate when hours worked will be carried out as normal and when as overtime. To do this, let us turn to the articles of the Labor Code of the Russian Federation. Working days and rest days for ordinary categories of workers are distributed in a 5/2 ratio.

In addition, in most cases, the hours worked during the pay period (in this case a week) will be 40 hours. If there are other conditions specified in the employment contract, then the hours can be reduced to 39, 36 or even 24.

However, if the enterprise has found its use of a shift work schedule (for example, working days of 2 days are followed by rest days, and the duration of the shift varies from 11 hours during the day and 12 hours at night), then in this case the legislative rules oblige the employer to keep summarized records of working hours . In this case, the calculation will be carried out for a period of 1 month, and not a year or a quarter.

To do this, a production schedule is drawn up for a year, quarter or month in accordance with internal regulations, which stipulate working hours, holidays and weekends. Correctly calculating time for a period (month, quarter or year) is the direct responsibility of the employer, since this determines whether the weekly production norm will be met, as well as the employee’s salary, and in case of overtime (overtime), additional payment.

Summary accounting: overtime pay

In accordance with Art. 152 of the Labor Code of the Russian Federation, overtime work is paid at least one and a half times the rate for the first two hours of work and at least double the rate for subsequent hours. However, the code does not answer more detailed questions: how exactly to pay, that is, where to get one and a half sizes from?

There are other difficulties: in order to figure out how to pay for overtime hours when accounting for working hours together, you need to focus on the chosen wage system - salary or tariff.

So, for example, if an employee has a salary system and the salary is 15,000 rubles, then the employer is guaranteed to pay him this amount. And only at the end of the accounting period, if there is overtime work, he will receive payment in the form of the first two hours at one and a half times the rate, and for subsequent hours at least double the rate.

Example

Payment for January, February and March - 15,000 rubles. for every month. During the accounting period, the employee worked 10 hours overtime. The rate for 1 hour of work is 100 rubles. We calculate how much he needs to pay extra:

2 hours * 1.5 * 100 rub. = 300 rub.

8 hours * 2 * 100 rub. = 1600 rub.

Total: 1900 rub.

Please note that Rostrud experts recommend establishing a tariff system of remuneration for workers for whom summarized working hours are kept - either hourly or daily.

How should overtime be calculated in this case?

Example

The employee has a tariff system of remuneration, the rate for 1 hour is 100 rubles. The accounting period is 1st quarter. Within this period, we notice that in January the employee actually worked 150 hours, which was included in the schedule. Accordingly, at an hourly rate we pay him 15,000 rubles.

In February, instead of 148 hours included in the schedule, the employee actually worked 156 hours (reflected in the report card). It turns out 15,600 rubles. At the same time, 149 hours were planned in March, but in fact it turned out to be 151 hours. You need to pay 15,100 rubles.

Evgenia Konyukhova, an expert in the field of labor legislation and personnel records management, in the webinar “Summary accounting of working time. Registration and payment" draws attention to the fact that with the tariff system of remuneration within the accounting period at a single rate, overtime work has already been paid.

The expert believes that the norm from Art. 152 of the Labor Code of the Russian Federation works well with a salary system of remuneration. As we saw above, in this case, at the end of the accounting period, you need to take 10 hours of overtime work and calculate the amounts: the first 2 hours - at one and a half times, and the remaining 8 hours - at double.

But if the employee has a tariff system of remuneration, then the first 2 hours should be paid only in the amount of 0.5, since the single rate has already been paid. And the remaining hours are not double, but single.

So, based on the fact that we had 10 hours of overtime, we get:

2 hours * 0.5 * 100 rub. = 100 rub.

8 hours *1 * 100 rub. = 800 rub.

Total: 900 rub.

If the employee has a salary system or a monthly wage rate, then you need to figure out how to determine how much to pay for one hour of overtime work. The fact is that the Labor Code does not answer this question. There are several examples of how this can be implemented in practice.

Option 1: The salary is divided by the number of working hours in the month when the employee was involved in overtime work.

So, if the salary is 20,000 rubles, then you need 20,000 / 160 hours = 125 rubles. per hour of work.

Option 2: According to Letter of the Ministry of Health of the Russian Federation dated 07/02/2014 N 16-4/2059436, the salary is divided by the average monthly number of hours per year (for example, for employees with a 40-hour working time in 2021, the average hourly number of working hours is 1979 hours / 12 month = 164.9 hours), respectively, hourly rate = 20,000 rubles. / 164.9 = 121.28 rub.

Option 3: The amount of salaries accrued for the accounting period is divided by the standard working time according to the employee’s schedule for the accounting period in months.

Option 4: The entire salary (including additional payments, allowances) is divided into one of the above options. But the employer is not obliged to calculate the hourly wage rate based on all payments. The Supreme Court believes that only the salary is sufficient.

Often, in addition to salaries, employers also provide a system of additional payments and allowances, which raises the question: should the entire salary in this case be divided by the number of hours in the month when the employee was involved in overtime work or by the average monthly number of hours for the year? Only the employer himself can answer this question in local regulations (Decision of the Supreme Court of the Russian Federation dated June 21, 2007 N GKPI07-516). It is recommended to do this, among other things, to avoid problems with employees and inspectors.

The position of the Ministry of Health and Social Development is that in the case of cumulative accounting of working time, based on the definition of overtime work, the calculation of overtime hours is carried out after the end of the accounting period. In this case, work in excess of the normal number of working hours for the accounting period is paid for the first two hours of work in no less than 1.5 times the amount, and for all other hours - no less than double the amount (Letter of the Ministry of Health and Social Development of the Russian Federation dated August 31, 2009 No. 22- 2-3363).

Depending on the remuneration system - salary or tariff - payment will be either one and a half to double, or 0.5 and single.

But there is another approach, indicated by judicial practice (Review of the Supreme Court of the Russian Federation of the practice of courts considering cases related to the implementation of labor activities by citizens in the regions of the Far North and equivalent areas" (approved by the Presidium of the Supreme Court of the Russian Federation on February 26, 2014)). There are clarifications according to which overtime pay is taken at one and a half times for the first 2 hours, which falls on average for each working day of the accounting period, and at double the rate for subsequent hours of overtime work. But when using this approach, the amount of payments for overtime work will be less, and therefore conflicts with employees are inevitable.

How are processing times calculated?

The working hours for each specialist are calculated separately. For example, a 40-hour work week is considered the standard (Article 90 of the Labor Code of the Russian Federation). But for some specialists, reduced work hours are established. For example, for teachers or doctors. For them, the calculation of overworked hours is not calculated from the 40-hour week, but from the reduced norm.

The volume of processing is strictly limited by law. The following cannot be involved in overtime work (Part 6, Article 99 of the Labor Code of the Russian Federation):

- 4 hours two days in a row;

- more than 120 hours per year.

Overtime hours should be recorded on time sheets. The procedure for reflecting overtime depends on the form of the report card used in the organization.

The calculation of overtime fees depends on the duration. For the first two hours you will be paid one and a half times the standard rate. For the rest of the time - no less than double the amount. The norms are regulated in Art. 152 Labor Code of the Russian Federation.

The employer has the right to increase overtime pay rates. The specific amount of allowances is determined individually, depending on the financial situation of the company. But you cannot pay less than what is enshrined in the Labor Code. The specific amounts of payments should be fixed in a local act of the organization. The legislation does not contain a minimum or maximum amount of payments.

IMPORTANT!

An employee has the right to refuse an increased premium for overtime work, replacing the money with additional rest time. To do this, the subordinate must write an application for time off. This must be done no later than the last day of the month or billing period in which the processing took place.

Payment for holidays or weekends with summarized accounting

If an employee’s working day falls on a non-working holiday, then the code “РВ” is entered in the working time sheet, despite the fact that this working day is included in the employee’s schedule. In this case, the employee is also subject to the provisions of Art. 153 of the Labor Code of the Russian Federation on increased payment for work.

According to the Recommendations of Rostrud dated June 2, 2014, when introducing summarized working time recording, work on holidays must be included in the monthly working time standard.

If an employee was involved in work on his day off or on a non-working holiday in excess of the monthly norm established for him or in excess of the norm in accordance with the accounting period, then such work will be subject to payment in accordance with Art. 153 Labor Code of the Russian Federation. The employee can also take another day of rest.

If within the accounting period the employer has already paid for non-working holidays, then at the end of the accounting period he does not need to pay for them as overtime. The Decision of the Supreme Court of the Russian Federation dated November 30, 2005 N GKPI05-1341 provides an explanation for this case: “Since the legal nature of overtime work and work on weekends and non-working holidays is the same, payment in an increased amount is simultaneously based on Art. 152 of the Labor Code of the Russian Federation, and Art. 153 of the Labor Code of the Russian Federation will be unreasonable and excessive.”

Answers to common questions about summarized accounting during processing

Question #1:

Do I need to notify employees about the transition to cumulative time tracking?

Answer:

If the internal labor regulations provide for the possibility of switching to summarized accounting during the period of validity of the employment contract, then the employee must be familiarized with the changes made.

Question #2:

Is it necessary to change the terms of the employment contract after the introduction of summarized working time recording at the enterprise?

Answer:

Yes, if the operating mode changes simultaneously with the introduction of summarized accounting. In this case, there is a change in the terms of the individual employment contract, and it is necessary to draw up an additional agreement to the contract.