Why is account 08 needed?

08 account is used to account for the company’s expenses on property, which will subsequently be taken into account as a fixed asset or intangible asset. In agriculture, account 08 takes into account the costs of forming a herd of productive and working livestock.

Account 08 is active. An increase in the cost of commissioning the acquired property is charged to debit. For example, when purchasing a machine, debit 08 of the account will write off not only the cost of the asset, but also the costs of delivery, installation and commissioning. When an object is accepted for accounting, its value is written off against the loan.

The procedure for using account 08 is fixed in PBU 6/01 and PBU 17/20.

Account 08 in accounting

Non-current assets are subsequently accepted for accounting and tax accounting as a fixed asset, land plot, environmental management facility or intangible asset.

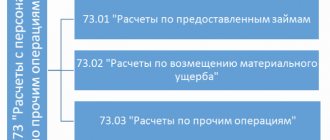

Account 08 “Investments in non-current assets” has the following sub-accounts:

The main aspect of using subaccount 08.03 “Construction of fixed assets” is that the subaccount reflects:

- All costs for the construction of buildings and structures;

- Equipment installation costs;

- Other expenses indicated in the financial estimates for capital construction by contract or business method:

The contract method of construction is construction work and installation work performed in accordance with the concluded construction contract (Articles 740, 743, 746 of the Civil Code of the Russian Federation).

The economic method of construction is construction work and installation work performed by the organization’s employees.

Formation of the initial cost of the OS:

What is an investment in non-current assets?

Investments are expenses of a company that are necessary to create or obtain fixed assets or intangible assets.

Costs on account 08 do not participate in the formation of the financial result in the period in which they are taken into account. Expenses incurred are usually attributed to the cost of land, acquired or constructed real estate, natural objects, and farm animals.

In the future, these costs are written off as expenses through depreciation of fixed assets and intangible assets.

For example, a company bought premises for 10,000,000 rubles in 2020. You cannot accept the entire amount as expenses. When the company puts the facility into operation, it will write off acquisition costs from credit 08 to debit 01, and then it will begin to depreciate this property. Let's say the useful life is 25 years. Then the annual expenses will include:

10,000,000 rub. / 25 years = 400,000 rubles.

That is, 400,000 rubles will be written off as expenses annually.

Postings to account 08 “Investments in non-current assets”

Enter the specified wiring into the Wiring Trainer and be sure to recite the “information” - what the wiring reflects, what “information” (see the description - I give a description for each wiring), 100% memorability, be sure to say it “out loud”.

A capital investment item has been received from the supplier

Posting: D. 08 “Investments in non-current assets” - K. 60 “Settlements with suppliers.”

Description: by posting we recorded “information” about the costs of the capital investment project (account 08) and by posting we recorded “information” about the debt to the equipment supplier (account 60).

Amount: amount WITHOUT VAT, indicated in the invoice or acceptance certificate. Posting date: date of the invoice or delivery certificate.

Document 1C 8.2 creating wiring D.08 - K.60:

doc. “Receipt of goods and services” - receipt of an “object” of fixed assets

— set the transaction type - “equipment” — tab. Equipment, set an “accounting account” for each asset object = account 08.04 — tab. Settlement accounts, set a “accounting account” with the counterparty = account 60.01/ 60.02

doc. “Receipt of goods and services” - receipt of “services” to bring the object to readiness

— set the type of operation - “equipment” — tab. and object = invoice 08.04 + object - issue a “account for settlements” with the counterparty = invoice 60.01 and invoice 60.02

The object of capital investment may be an expense of 100 rubles. (for example, we bought a bag of nails). In the version with a bag of nails, a part of the object was received, which still needs to be assembled into a single whole. If you don’t collect the expenses for this bag of nails on account 08 right away, then you can end up missing a million of these bags, and this is already an object worth 100 million rubles. The main thing is that you must highlight from the entire flow of expenses those expenses that need to be collected separately on account 08, expenses that are directly related to the creation of our future fixed asset.

In my work, I immediately warn managers that they must inform me about the decision to create OS objects, and there were cases when I learned about an object under construction approximately halfway through its construction, and of course I did not correctly reflect the costs of this object, since my accountant wrote off the costs of creating the object simply as expenses for the period, which is NOT correct (distortion of accounting statements, income tax, property tax).

WE ACCEPT the object as part of fixed assets

Posting: D. 01 “Fixed assets” - K. 08 “Investments in non-current assets”.

Description: by posting we recorded “information” about the “initial cost” of the fixed asset (account 01) and by posting we recorded “information” about the completion of the formation of the “initial” cost of the fixed asset (account 08) and the write-off of all expenses to account 01.

Amount: the amount of accumulated expenses, which is listed on account 08 at the time of commissioning of the fixed asset. Posting date: The date the asset was put into operation, usually indicated in the commissioning report. Note: before generating the posting, we check the “attribution limit to the OS”.

Document 1C 8.2 creating wiring D.01 - K.08:

doc. "Acceptance for accounting of fixed assets"

— set the operation type - “equipment” — tab. Fixed assets, set the “accounting account” for the capital investment object = account 08.04 — tab.Accounting, set the “accounting account” for the fixed assets object = account 01.01 — tab.Accounting , we issue a “depreciation account” for the fixed asset object = account 02.01

What subaccounts are opened for account 08

The chart of accounts suggests opening the following subaccounts for account 08, which we have collected in the table.

| Subaccount | We use it for accounting |

| 08.1 | Here we collect all the costs associated with the purchase of a land plot: from the cost of its acquisition to registration fees. |

| 08.2 | Here we summarize all the costs associated with the purchase of environmental management facilities. |

| 08.3 | Here we accumulate all the costs associated with creating an OS yourself. For example, these are the costs of constructing buildings and installing equipment. |

| 08.4 | We take into account all costs associated with the purchase of machines and equipment that do not require installation. |

| 08.5 | Here we reflect the cost of purchased intangible assets. These could be licenses for computer programs, trademarks, and so on. |

| 08.6 | Here we record all the costs incurred by the company for raising young animals. |

| 08.7 | Here we reflect the cost of purchased adult animals, including their delivery. |

| 08.8 | Here we reflect the company's R&D costs. For example, the creation of a new technology or prototype. |

How analytical accounting is carried out on account 08

On account 08, detailed analytical accounting is kept for each object on which costs are incurred. For example, on account 08 the following is kept:

- costs for each individual asset under construction or acquisition;

- costs for each type of design and survey work;

- costs for the acquisition of each intangible asset;

- costs of forming a herd for each type of animal;

- R&D costs by type of work or contracts if R&D is carried out to order.

In addition, costs should be broken down into groups. For example, costs of construction, reconstruction, installation, design and survey work, and so on.

Keep records of exports and imports in the Kontur.Accounting web service. Simple accounting, payroll and reporting in one service

Which accounts does account 08 correspond to?

Account 08 corresponds with most of the accounts by debit. The list of accounts with which he corresponds on the loan is much smaller. For convenience, we have collected all the accounts in a table.

| Account 08 corresponds by debit with | Account 08 corresponds for the loan with |

| 02 “Depreciation of fixed assets” 05 “Depreciation of intangible assets” 07 “Equipment for installation” 10 “Materials” 11 “Animals for growing and fattening” 16 “Deviation in the cost of material assets” 19 “VAT on acquired assets” 23 “Auxiliary production” 26 “General business expenses” 60 “Settlements with suppliers and contractors” 66 “Settlements for short-term loans and borrowings” 67 “Settlements for long-term loans and borrowings” 68 “Settlements for taxes and fees” 69 “Settlements for social insurance and security” 70 “ Settlements with personnel for wages" 71 "Settlements with accountable persons" 75 "Settlements with founders" 76 "Settlements with various debtors and creditors" 79 "Intra-business settlements" 80 "Authorized capital" 86 "Targeted financing" 91 "Other income and expenses » 94 “Shortages and losses from damage to valuables” 96 “Reserves for future expenses” 97 “Deferred expenses” 98 “Deferred income” | 01 “Fixed assets” 03 “Income-earning investments in tangible assets” 04 “Intangible assets” 76 “Settlements with various debtors and creditors” 79 “Intra-business settlements” 80 “Authorized capital” 91 “Other income and expenses” 94 “Shortages and losses from damage to valuables" 99 "Profits and losses" |

Basic postings with account 08

The table contains the main typical transactions with account 08 that every accountant encounters.

| Debit | Credit | The essence of wiring |

| 08 | 02 | We charged depreciation on equipment involved in the creation of a new non-current asset. |

| 08 | 05 | We calculated depreciation of intangible assets involved in the creation of a new asset. |

| 08 | 10 | The cost of materials used to create a non-current asset was written off. |

| 08 | 23 | The cost of auxiliary production services was written off to the cost of the asset. |

| 08 | 26 | We wrote off part of the general business expenses associated with the creation of the asset. |

| 08 | 60 | Purchased OS or intangible assets. |

| 08 | 66 / 67 | Interest on the loan was included in the value of the asset. |

| 08 | 70 | We paid wages to employees involved in the creation of the asset. |

| 08 | 69 | Insurance premiums were calculated from the salaries of employees involved in the creation of a non-current asset. |

| 08 | 75 | We received intangible assets as a contribution to the authorized capital. |

| 08 | 98 | Received a non-current asset free of charge. |

| 01 | 08 | The non-current asset was taken into account as fixed assets. |

| 03 | 08 | The non-current asset was taken into account as fixed assets for subsequent rental on a reimbursable basis. |

| 04 | 08 | The non-current asset was taken into account as an intangible asset. |

| 91 | 08 | The cost of a non-current asset sold or disposed of for another reason was written off. |

We recommend you the cloud service Kontur.Accounting. In our program, you will easily master the accounting of non-current assets and set up all the necessary analytics. You will also be able to keep records, calculate salaries, submit reports and use other accounting tools. We give all newbies a free trial period of 14 days.

Accounting for receipt and disposal of fixed assets and the procedure for their inventory

D 08 - K 60 - reflects the costs of construction and installation work accepted from contractors;

D 19 - K 60 - VAT presented by the contractor for payment to the customer is reflected;

D 01 - K 08.3 - fixed assets put into operation.

When an organization carries out construction and installation work in an economic way, the following entries are made in accounting:

D 10 - K 60 - materials were purchased to carry out work on the construction of the facility;

D 19 - K 60 - VAT on purchased materials is reflected.

The costs for the construction of buildings, structures, installation and other capital construction costs minus VAT are reflected:

D 08 - K 07 - the costs of installing equipment are reflected;

D 08 - K 10 - costs of materials used are reflected;

D 08 - K 70 - wages to employees;

D 08 - K 69 - the amount of insurance contributions from employees' wages;

D 08 - K 19 - non-refundable VAT written off to increase the actual costs of construction and manufacturing;

D 08 - K 68 - VAT is charged on the volume of work performed;

D 60 - K 51 - funds were transferred;

D 68 - K 19 - VAT is reflected on materials purchased, work performed, services provided;

D 01 - K 08.3 - fixed assets were put into operation.

Acceptance of completed work on the completion and additional equipment of a facility, carried out in the order of capital investments, is formalized by an acceptance certificate for repaired, reconstructed and modernized facilities (form No. OS-3). The transfer of equipment for installation is formalized by an act of acceptance and transfer of equipment for installation (form No. OS-15). For equipment defects identified during installation, adjustment or testing, as well as based on inspection results, a report on identified equipment defects is drawn up (Form No. OS-16) [1, p. 128].

One of the ways to receive fixed assets is to receive objects as a contribution to the authorized capital of a newly formed or increasing the authorized capital of an organization. When making contributions to the authorized capital of the organization, the founders act on the basis of the constituent agreement, and when they are made in the accounting records of the organization, the initial value is recognized as their monetary value, agreed upon by the founders of the organization. When accepting for accounting fixed assets contributed by the founders as part of their contribution to the authorized capital of the organization, the following accounting entries are made:

D 75 - K 80 - for the amount of debt of the founders in monetary value for contributions to the authorized capital when creating the organization;

D 08 - K 60 - reflection of delivery costs;

D 08.4 - K 75.1 - receipt of deposits in the form of fixed assets from the founders;

D 19 - K 83 - VAT on contribution to the authorized capital;

D 01 - K 08.4 - acceptance of fixed assets into operation;

D 68 - K 19 - VAT on the contribution to the authorized capital is accepted for deduction.

According to the gift agreement, one party (the donor) gratuitously transfers or undertakes to transfer to the other party (the donee) an item of ownership or a property right (claim) to himself or to a third party, or releases or undertakes to release her from a property obligation to himself or to a third party [17 ]. Fixed assets received under a gift agreement are accepted for accounting at market value. The market value of property is established by documentary or expert means. The costs of establishing and confirming the market price are included in the initial cost of fixed assets. According to PBU 9/99 “Income of an organization,” assets received free of charge are included in other income of the organization [21].

Acceptance for accounting of fixed assets received from other legal entities and individuals under a gift agreement, as well as in other cases of their gratuitous receipt, is reflected in the following accounting entries:

D 08 - K 98 subaccount 2 “Gratuitous receipt” - receipt of fixed assets under a gift agreement;

D 08 - K 60 - reflection of expenses associated with the transportation of fixed assets;

Go to page: 2

Other articles

Pricing policy of a manufacturing company, methods of setting prices for industrial products For the normal functioning of the economy, various levers for managing economic processes, in particular prices, are necessary. Prices answer the question of supply and demand, both in local and global markets, the equilibrium price eliminates obvious shortages or surpluses of goods...