Intangible assets

Intangible assets include various inventions, trademarks, computer programs, any production secrets, etc.

The document that established the rules for accounting for intangible assets is PBU 14/2007. It was approved by Order of the Ministry of Finance of Russia dated December 27, 2007 No. 153n. It is this PBU that needs to be used when working with an organization’s intangible assets.

When conducting an inventory, intangible assets are checked in accordance with Order of the Ministry of Finance dated June 13, 1995 No. 49:

- whether intangible assets were reflected correctly and on time on the company’s balance sheet;

- does the company have documents that can confirm that it has the rights to use intangible assets.

What is it used for?

This form of inventory list is used when taking inventory of property related to the fixed assets of the enterprise.

These are buildings, machines, any equipment, as well as computer equipment, equipment, production and economic.

This may be due to either the liquidation of the enterprise or natural disasters that damaged the main property.

It is necessary to fill out the INV-1 form strictly in accordance with the financial statements in order to avoid confusion and errors that will lead to shortages or loss of valuable property.

Inventories are written separately for production fixed assets and non-production assets. At the same time, for each structural unit its own inventory list INV-1 is drawn up.

Therefore, when recalculating fixed assets, it is necessary to create separate documents for each department, and the responsible people fill out all fines so that the inventory is complete.

Is it necessary to work with the INV-1a form?

The INV-1a form was developed and approved by the State Statistics Committee of Russia, by resolution No. 88 of August 18, 1998. Until the beginning of 2013, the form was mandatory for use, after which it became only recommended. That is, to conduct an inventory of intangible assets, a company today can use a document developed independently for its own convenience based on INV-1a. However, in this case, management must remember that the unified form cannot be completely changed: the mandatory details must always be on the document, otherwise the inspection authorities will doubt its authenticity.

Not all companies enjoy the right to develop their own forms. For some, it is more convenient to use INV-1a, since this is a familiar form for many experienced workers, and in this case, the inspection authorities will not have questions about these documents.

For your information! The choice of certain forms must be recorded by the company's management in its accounting policies.

INV-1 form and content

The official INV-1 form is not required for use just like other unified inventory forms. A company or entrepreneur can develop their own forms and use them to conduct property inventories. However, companies often prefer to use the official form. Therefore, let's take a closer look at it.

Below we have placed the INV-1 form, which you can download for free.

1737 downloads

We have also prepared for you a sample of filling out INV-1. Please note that the inventory must be made in at least 2 copies (the first for the accounting department, the second for the employee bearing financial responsibility). For leased property, a third copy of the inventory is drawn up for each lessor.

Commission

A special commission is always appointed to conduct any inventory. It may include an accountant, lawyer, administration employees, department heads, and specialists. The composition must be approved by the head of the company (Order of the Ministry of Finance of the Russian Federation dated June 13, 1995 No. 49).

Financially responsible persons are not included in the commission, since the inventory checks their work. The commission is created on an ongoing basis. The number of people is not limited, but usually it is 3-4 employees.

Inventory inventory of intangible assets INV-1a

All property and liabilities of the organization are subject to periodic inventory. During the inventory process, the commission fills out inventory lists. A separate inventory form is filled out for each type of property. In this article we will talk about the inventory of intangible assets.

The standard form for an inventory of intangible assets is INV-1a. It is allowed not to use a unified form, but to develop your own. The inventory list of intangible assets INV-1a, as well as a sample of filling out this form, can be found at the end of the article.

Standard inventory forms have been developed for all types of property: fixed assets - INV-1, inventory items - INV-3.

In relation to cash, the cash register inventory report INV-15 is filled out, and the cash register report INV-17 is filled out for settlements with counterparties.

The completed inventory list is transferred to the accounting department, which, based on identified discrepancies between accounting and actual data, fills out the matching sheet INV-18.

When conducting an inventory of intangible assets, an inventory commission is created, which inspects existing assets and checks for the presence of documents giving an exclusive right to objects of intangible assets. The commission is appointed by order of the head, a sample of which can be downloaded here.

Sample filling

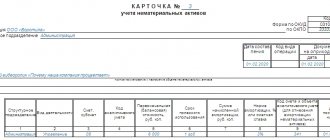

The INV-1a form contains the title part, a table with a list of intangible assets and the final part with the conclusion of the commission and the necessary signatures.

In the title part of INV-1a, information about the organization, the owner of intangible assets, as well as information about the inventory itself is filled out - the date of its start, end, number and date of the order to conduct the inventory, the type of property subject to inspection, its location.

On the first page of the INV-1a form there is a subsection “Receipt”, in which persons responsible for intangible assets put their signatures as a sign that all documents on the assets have been transferred to the accounting department, all objects have been taken into account.

In the table you need to sequentially list all the intangible assets the company has:

- Their name, brief description;

- Number, date and name of the document on registration of the exclusive right to the asset;

- The date when the intangible asset was accepted for accounting;

- Its actual value and accounting value.

Fill out as many sheets with the table as necessary, depending on the number of intangible assets. At the end of each page, the number of serial numbers and the total amount for the objects listed on this page are written down.

After all objects of intangible assets are indicated in the table, the total number of serial numbers according to the inventory as a whole is calculated, as well as the actual total value of all intangible assets.

The inventory commission (each of its members) must sign the completed inventory form. Financially responsible persons also put their signatures as a sign that they are familiar with the contents of the inventory.

After this, the inventory list is transferred to the accounting department, which, if necessary, draws up a matching statement.

How to correctly fill out the INV-1a form

The form consists of three pages. Let's talk in detail about each of them.

First page

Here you need to enter information such as:

- Name of the company, enterprise and structural unit. The name must be the same as in all other documents.

- OKPO code.

- Activity code.

- Details of the document (number and date of preparation) on the basis of which the inventory is carried out. This is an order, decree or direction. As a rule, there is an order.

- Start and end dates of the inventory procedure.

- Type of operation (not always filled in).

- Number and date of compilation of the completed inventory.

- List of intangible assets that are subject to inventory.

- Their location. Here it is noted in which structural unit the intangible assets are located.

This is followed by a receipt stating that all intangible assets have been sent to the accounting department, and the intangible assets themselves have been accounted for or written off. The employees responsible for storing papers on the company’s right to intangible assets put their signatures.

Second page

There is a table on this page. The following data is entered into it:

- Number in order.

- Intangible asset name, function and brief description.

- A document confirming its registration, with details such as name, date of preparation and number.

- Date of registration with the company.

- Actual cost according to primary data.

- Cost according to accounting data.

At the end of the table, the total value of all assets is summarized. Then they summarize the page: indicate the number of serial numbers in the table and the actual amount. These entries must be made in words.

Attention! If the organization has a lot of intangible assets, then you can add the required number of pages to the form. Then each of them will need to be summarized at the end.

Third page

First of all, sum up the overall inventory. Then the chairman and members of the commission put their signatures, after which the persons responsible for the safety of documents on the right to intangible assets sign that all intangible assets were checked in their presence and there are no claims against the commission.

At the end, the accountant signs that he has checked all the calculations in this inventory.

If, based on the results of the inventory, discrepancies were identified between accounting and actual data, then fill out a matching statement in the INV-18 form.

INV-1 sample filling

On the 1st page of the OS inventory list the following information is reflected:

Information about the company (name; structural unit in which the inventory is carried out; OKPO, main OKVED).

Inventory information (details of the inventory order, inventory deadlines).

Information about operating systems undergoing inventory

It should be noted that the inventory can be carried out both in relation to the company’s own property and in relation to fixed assets received by the company for rent. In this case, a separate inventory of such property is drawn up, one copy of which is transferred to the lessor, and information about it is indicated in the inventory.

A receipt from the employee responsible for the property, which confirms that all the property assigned to him has been accounted for.

On the 2nd page a direct inventory of the property is made. The name, characteristics and numbers of the OS are indicated. The actual quantity and cost of fixed assets and according to accounting data are reflected.

On page 3, the inventory list of fixed assets is signed by all members of the commission and the employee responsible for their safety

Please note that the inventory must be carried out in the presence of all members of the commission and the employee who is financially responsible for this property. Violation of this rule entails the recognition of the inventory results as illegal

If discrepancies are identified between the actual state of the fixed assets and accounting data (shortages, surpluses), matching statements are compiled (official form INV-18).

More information about the inventory procedure, the timing of its implementation; cases where it is mandatory; regulatory framework and other issues, see the following video.

What is important to remember

- The inventory can be filled out either by hand or on the computer. In the first case there should be no blots.

- The document is drawn up in 2 copies. The first is transferred to the accounting department, and the second remains with the employee who is responsible for the safety of documents for the right to intangible assets.

- If a factual error is found in the document, it is corrected by notifying all persons involved in the inventory. Incorrect information is crossed out and the correct option is written on top. All participants in the procedure put their signatures.

- Inventory records must be stored in the organization for 5 years.

When is an inventory report drawn up?

Many managers assume that they have the right to conduct or not conduct an inventory at their own discretion. This is not entirely true. In accordance with the norms of the current legislation of the Russian Federation, such a procedure is mandatory in the following cases:

- before drawing up annual financial statements, while an inventory of fixed assets can be carried out once every 3 years, library collections - once every 5 years

- when an organization transfers property for rent, redemption, sale

- when changing financially responsible persons (dismissal, transfer, etc.)

- identification of facts of theft, abuse or damage to property

- during reorganization (change of organizational and legal form) or liquidation of the organization

- in case of fire, natural disaster and other emergency situations

- if the organization has introduced collective (team) responsibility, then an inventory must be carried out when the leader of such a team changes, when more than 50% of its members leave the team, at the request of one or more members.

In addition to these cases, inventory is carried out by decision of the manager. The purpose of the event is to identify the actual availability of property and compare it with accounting data. At the same time, when there is a change of financially responsible persons, in addition to the Inventory Report, an act of acceptance and transfer of entrusted property is drawn up.

What property is subject to inventory? Fixed assets, financial investments, finished products, goods, intangible assets, cash and other financial assets, loans, borrowings and reserves.