Although slowly, the state is responding to problems arising in business. One of them is violation of payment terms for products supplied or services provided. Therefore, from 2021, the conditions for the creation and calculation of doubtful debts, the reserve of which is deducted from the tax base, have been updated. As a result, it has become profitable for legal entities and entrepreneurs paying taxes under OSNO to create a reserve for doubtful debts in the balance sheet.

The editors of the VKreditBe.Ru website examine in detail the regulatory framework and principles of forming a reserve for doubtful debts, methods of reflection in accounting, as well as the write-off procedure.

Normative base

Regulation of all issues related to the creation, accounting and write-off of the reserve for doubtful debts is carried out on the basis of the following documents:

- Federal Law “On Accounting” dated December 6, 2011 N 402-FZ as amended;

- Tax Code of the Russian Federation (Part 2) dated August 5, 2000 No. 117-FZ, as amended, entered into force on March 1, 2015;

- Regulations on accounting and financial reporting in the Russian Federation, approved by Order of the Ministry of Finance of the Russian Federation dated July 29, 1998 No. 34n;

- Accounting provisions PBU 4/99 “Accounting statements of an organization”, approved by Order of the Ministry of Finance of the Russian Federation dated July 6, 1999 No. 43n;

- Order of the Ministry of Finance dated June 13, 1995 No. 49 (as amended on November 8, 2010) “On approval of the Methodological Guidelines for the Inventory of Property and Financial Liabilities”;

- Accounting Regulations 21/2008 “Changes in Estimated Values”. Approved by order of the Ministry of Finance of the Russian Federation dated October 6, 2008 No. 106n.

- Resolution of the State Statistics Committee of Russia dated August 18, 1998 No. 88.

- Letters of the Ministry of Finance of the Russian Federation dated July 10, 2015 No. 03-03-06/39756 and dated January 14, 2013 No. 03-03-06/1/7.

What are doubtful debts

The definition of doubtful debt is given in Art. 266 of the Tax Code of the Russian Federation, where the specified term means any debt to the taxpayer that arose as a result of late payments within the time limits specified by contractual obligations and not secured by a pledge, surety, bank guarantee and other means of ensuring the fulfillment of obligations .

Any receivables reflected in the debit of the accounts fall under the doubtful category:

- 60 “Settlements with suppliers and contractors”;

- 62 “Settlements with buyers and customers”;

- 76 “Settlements with various debtors and creditors.”

In addition, a loan not repaid on time, reflected in subaccount 58-3 “Loans provided,” can be classified as doubtful debt.

From doubtful debt to hopeless debt

Doubtful debt is debt associated with the sale of goods, works, services, if it is not repaid within the time limits established by the agreement and is not secured by a pledge, surety, or guarantee.

The doubtful debt will either be repaid by the debtor in the future (in whole or in part), or will turn into a bad debt.

It is impossible to collect an uncollectible debt. That is, part of the money or assets is completely lost. There is a loss. Such a loss can be attributed to non-operating expenses or written off against the created reserve for doubtful debts.

The reserve is created only for doubtful debts arising in connection with the sale. No reserve is created for overdue advances to suppliers.

Firms that create a reserve for doubtful debts write off debts recognized as bad debts from this reserve. If the reserve is not enough, the difference is charged to non-operating expenses.

Those who do not create a reserve also reduce their tax liabilities, but not before the moment when the debt is recognized as bad.

But not every debt can be considered bad enough to be written off.

The debt is recognized as a bad debt and is taken into account as part of non-operating expenses of the reporting period on the date of expiration of the limitation period, as well as upon the occurrence of the circumstances listed in clause 2 of Art. 266 Tax Code of the Russian Federation.

Types of doubtful debts

All doubtful debts can be divided into four large groups depending on the possibility of their collection (see Table 1).

Table 1. Types of doubtful debt.

| Type of debt | Characteristics |

| Overdue | Debt not repaid within the terms specified in the contract, but with the prospect of forced collection in the future, including through the court |

| Restructured | The debtor was granted an installment plan or deferment through peaceful negotiations or a court decision |

| Doubtful | Debt that is not secured by any guarantees, with the prospect of becoming uncollectible |

| Hopeless | The statute of limitations has expired |

All of the above in simple language: a doubtful debt is a debt that is unlikely to be collected using legal means .

The procedure for opening and maintaining a reserve in accounting

When creating a reserve to cover overdue debts of debtors, the organization’s accountant is guided by the same rules:

- Debts whose payment terms have expired are being identified.

- The presence of counterclaims on the part of the debtor is analyzed.

- The security of obligations is checked.

- Debtor insolvency risk coefficients are calculated.

- The amount of coverage is calculated based on the ratio of days of delay.

The unused balance can be used in another reporting period. If the fund's funds are insufficient, problematic arrears are covered through other expenses.

The provision for doubtful debts should also be reflected in accounting

Conditions for forming a reserve for such debts

At the legislative level, the mechanism for creating a reserve for doubtful debts is not specified. Enterprises must themselves develop a regulatory framework for accounting, on the basis of which the amount of the reserve will be formed and reflected in accounting. The document must be put into effect by order of the manager. It says:

- methodology for determining the level of solvency of the debtor;

- lists the insolvency criteria on the basis of which doubtful debts are reflected in accounting;

- the rules for the formation and accounting of reserves are outlined.

Important: with a simplified taxation system (STS), a reserve does not need to be created.

Rules for writing off doubtful debts

In order to insure against the bankruptcy of an enterprise due to the occurrence of doubtful and bad debts, at the direction of senior managers, the accounting department creates a reserve. The provided amount of the reserve can be no more than 10% of the organization’s revenue from the beginning of the year to the current date.

From the standpoint of legislation (clause 5 of Article 266 of the Tax Code of the Russian Federation), when a taxpayer decides to create a reserve for doubtful debts, they are written off, if necessary, from the amount of this reserve. If bad debts exceed the allowance amount, the difference is recorded as a loss and reflected in non-operating expenses.

If an enterprise has formed a reserve for doubtful debts, the costs of deductions from it are recorded in line 200 in Appendix No. 2 of sheet 02 of the income tax return. Unrealized expenses - bad debts that cannot be covered by the reserve for doubtful debts are reflected as losses in line 300 and are subsequently allocated in line 302.

Methodology for determining the level of solvency

A delay in payment for services or goods should alert the lender's management. Its specialists should immediately begin assessing the financial condition of the debtor. This can be done in different ways, within the framework of the law:

- ask for an extract from the Unified State Register of Legal Entities or Unified State Register of Individual Entrepreneurs in case of liquidation of a legal entity;

- request financial statements for the last quarter from the counterparty or Rosstat. This will allow you to analyze the financial condition of the debtor:

- profitability;

- liquidity;

- amount of debt;

- amount of assets, etc.

- order an analysis on the State Services portal, but here, firstly, you will have to pay, and secondly, fill out the application correctly - the report data is a commercial secret.

Attention: application submission to Rosstat and the State Services portal is carried out in accordance with Rosstat order No. 183 dated May 20, 2013.

Criteria

To classify a debt as doubtful when determining the amount of taxation, it must:

- arise as a result of the sale of products, works or services. Debt on other grounds, such as prepayment for goods or services, fines and penalties for violation of the terms of the contract, is not considered doubtful. Debt under a loan agreement cannot be considered the same;

- be overdue - the money did not arrive in the creditor’s settlement account on time, within the terms specified in the purchase and sale or delivery agreement.

Regulations for establishing a fund in tax accounting

The creation of a reserve for doubtful debts in tax accounting in 2018 relates to the right of the enterprise, and is not a strict requirement of the law. If the manager comes to the conclusion that it is necessary to correct or reduce the tax base, then it is worth taking into account the requirements of Art. 266 Tax Code of the Russian Federation.

For tax purposes, debt arrears on transactions directly related to trading activities are considered doubtful if two conditions are met:

- Repayment deadline missed.

- There is no security for contractual obligations.

- The amount of receivables exceeds the counter-obligations payable to the counterparty.

Unpaid obligations under transactions for the provision of loans, credits, transfer of advance payments for upcoming deliveries, penalties are not taken into account when calculating the reserve. The bank has the right to include in the coverage the amount of interest accrued after 01/01/2015, regardless of the presence of collateral. Insurance companies, using the accrual option, do not form a provision fund for insurance premiums.

Doubtful debts must be reflected in tax records

The procedure for organizing the coverage base is reflected in tax accounting as part of costs not related to trading activities on the last day of the reporting period. The accountant applies the following methodology for calculating the amount of resources to cover doubtful receivables in the OU:

- Obligations for which the period of arrears exceeds a quarter are attributed entirely to the fund.

- If the contractual obligation is overdue by 45-90 days, only half of the amount is applied to the reserve.

- Debtor arrears that have not been repaid for one and a half months are not included in the formation of the crisis fund.

The procedure for identifying unrealistic debts for collection must be accompanied by documentation: an inventory list, an order from the manager, a certificate from an accountant. Only fully confirmed expenses can reduce the income tax base.

It is important that the total amount of the reserve cannot exceed a tenth of revenue minus VAT. In relation to the created fund, the rule of targeted spending applies: it can only be used to secure overdue debts of debtors. Accounting is carried out in the context of analytics.

Formation rules

For each debt, reserves can be calculated using several methods. Here is one example:

- if the debt is overdue for more than 3 months, the entire amount of the debt, 100%, is included in the reserve;

- if the delay is more than 1.5 months, but less than 3 - 45%;

- up to 45 days - no accounting entries are made for the debt.

At the next stage, the reserve amounts for each debtor are summed up. Here you need to remember that there is a limit established by legislative acts - the amount of the reserve should not exceed 10% of gross revenue. If it is more, you will have to reduce it to the standard.

The maximum contribution amount can be calculated using the formula:

SPO = Vd x 10 / 100 , where:

- SPO - amount of maximum deductions, rub.;

- Vd - the amount of revenue from the sale of goods, works, services for the reporting period (excluding VAT), rub.

- 10 - percentage of maximum deductions (4 Article 266 of the Tax Code of the Russian Federation).

Based on the results of the calculations, an act is drawn up in the form INV-17 or developed directly in the organization (approved by order along with guidelines for the formation of the reserve).

The procedure for creating a reserve for doubtful debts in tax accounting

Reserves for doubtful debts are created by organizations that are payers of income tax (clause 7, clause 1, article 265, article 266 of the Tax Code of the Russian Federation).

When forming a reserve, you must act as follows (clause 4 of Article 266 of the Tax Code of the Russian Federation).

Step 1. On the last day of the reporting (tax) period, conduct an inventory of receivables. The results of the inventory shall be documented in an act in a form developed by the organization independently, taking into account the provisions of Art. 9 of Law No. 402-FZ, or using the unified form INV-17, approved by Resolution of the State Statistics Committee of Russia dated August 18, 1998 No. 88.

When analyzing accounts receivable, you need to identify debts that, in accordance with paragraph 1 of Art. 266 of the Tax Code of the Russian Federation are recognized as doubtful, and on the basis of which a reserve will be created.

Doubtful debt is understood as debt incurred during the sale of goods (performance of work, provision of services), not repaid within the period stipulated by the contract and not secured by a pledge, surety, or bank guarantee. That is, if there is a pledge or guarantee, then a reserve cannot be created for such debt, even if the guarantor is bankrupt (letters of the Ministry of Finance of Russia dated July 10, 2015 No. 03-03-06/39756, dated January 14, 2013 No. 03-03-06/ 1/7).

From 2021, a direct provision of the Tax Code of the Russian Federation establishes that only part of the debt that is not covered by the counter debt of the same counterparty should be included in the reserve. That is, if a company has a counter-obligation to a debtor counterparty, then only the amount that exceeds the amount of this obligation is considered doubtful debt. At the same time, the reduction of such debts to the creditor of an economic entity is carried out starting from the first debt in time (Clause 1, Article 266 of the Tax Code of the Russian Federation).

See also: “The Ministry of Finance explained how a “doubtful” reserve is formed in the presence of a counter creditor .

It should be noted that when creating a reserve for doubtful debts, the organization should not take into account those amounts of receivables that arose during the period of application of a taxation system other than the general one, for example UTII (letter of the Ministry of Finance of Russia dated December 21, 2012 No. 03-11-06/3/ 90).

See also:

- “Should the advance payment be taken into account in the “doubtful” reserve?”;

- “An insured debt cannot be doubtful”.

Step 2. For each doubtful debt, determine the percentage of deductions and calculate the total estimated amount of deductions (RSO) according to the following principle:

- if more than 90 days have passed since the occurrence of the doubtful debt, then the debt in full (100%) is included in the reserve,

- if the period of doubtful debt is from 45 to 90 days (inclusive), then 50% of the debt amount is transferred to the reserve,

- if the debt arose less than 45 days ago, then no reserve is created for it.

Step 3. Determine the maximum amount of contributions to the reserve using the formula:

PSO = B × 10%,

where B - for the reserve based on the results of the tax period - the amount of revenue from the sale of goods (work, services, property rights) received based on the results of the tax period; for the reserve, which is formed based on the results of the reporting period, the largest amount of the amounts: revenue for the previous year or for the current reporting period;

10% - limit on the amount of the created reserve (4 Article 266 of the Tax Code of the Russian Federation).

The limitation may be less than 10% of the amount of revenue (Resolution of the Federal Antimonopoly Service of the North Caucasus District dated October 25, 2004 No. F08-5008/2004-1902A). The organization has the right to independently choose the standard percentage, and it must be fixed in the accounting policy. Typically, a decision to establish a lower standard is made when contributions to the reserve according to the general standard of 10% can lead to a loss or zero financial result (for example, with high revenue but small profit).

Step 4. Compare the estimated amount of deductions (RSA) and the maximum amount of deductions (PSO), i.e. results of actions (2) and (3):

- if RSO ≥ PSO, then the amount of deductions corresponding to PSO must be included in the reserve.

- if RSO < PSO, then the amount of deductions corresponding to RSO is included in the reserve.

The calculated amount of deductions should be included in non-operating expenses for the last day of the reporting (tax) period (clause 3 of Article 266, subclause 7 of clause 1 of Article 265, subclause 2 of clause 7 of Article 272 of the Tax Code of the Russian Federation).

If you have access to ConsultantPlus, check whether you have correctly calculated the reserve for doubtful debts in tax accounting. If you don't have access, get a free trial of online legal access.

NOTE! Any uncollectible debt is written off from the reserve, regardless of whether it participated in the formation of the reserve or not.

See here for details.

Methods for creating a reserve

Creating a reserve for doubtful debts of an organization (enterprise) can be carried out in the following ways:

- interval;

- expert;

- statistical.

Interval method. The interval method of reserve formation is one of the most accurate, but also more labor-intensive methods for determining the reserve amount. The bottom line: each debt for a month or quarter (reporting period) is taken and, depending on the time of delay in days, it is multiplied by the percentage (50 or 100%) established by law, as mentioned above.

Expert method. You can do it differently: estimate the amount of debt that will not be received by the company, based on data on the financial solvency of debtors, without taking into account the period of delay.

Statistical method. Statistics know everything. Therefore, we take the same reporting period for several previous years and find the average amount of doubtful accounts receivable - the simplest method, which is quite close to reality.

Doubtful debts

Doubtful accounts receivable is an amount that the company may never receive back. In order for it to be considered doubtful, it must meet the following conditions:

- The debt arose in the process of operating activities, that is, those that are the immediate purpose of the company’s existence.

- The debt was not returned within the period specified in the contract. If there is no term in it, then to determine it it is necessary to refer to laws, regulations and other official sources of law.

- There should be no pledge or guarantee in relation to the debt, since otherwise it can be claimed from another person who is the guarantor, or obtained by selling the subject of pledge.

You may be interested in: Payment for fuel and lubricants: drawing up an agreement, payment procedure, rules and features of registration, charges and payments

It is important to remember that PD is questionable if it meets all three specified conditions. Accounting for doubtful accounts receivable is characterized by the presence of certain features that distinguish it from simple accounting.

The presence of such a problem does not mean that the funds are lost forever. Doubtful accounts receivable is an amount that is still recoverable. True, this happens extremely rarely, but if you act quickly and within the law, then everything can turn out very well. Accounts receivable are written off for doubtful debts when they are fully repaid.

Differences in the formation of reserves in accounting and tax accounting

The rules for creating a reserve for doubtful debts in tax accounting differ significantly from the procedure for creating the same funds in accounting.

1. The need for creation.

- In accounting, a reserve is required if there are doubts about the “receivable” - these are the requirements of clause 70 of the Accounting Regulations.

- In tax accounting, everything is left to the chief accountant - it is he who decides whether or not to include the created reserve in the tax base to reduce profits, and with it the amount of taxes (clause 3 of Article 266 of the Tax Code of the Russian Federation).

2. Different concepts of doubtful debt.

- For an enterprise, these are any types of overdue receivables, as well as, importantly, debts that can be overdue with a high degree of probability.

- For the tax service, the amount of the reserve is determined only for overdue debts for payment for goods, works and services (clause 1 of Article 266 of the Tax Code of the Russian Federation).

3. Timing of indebtedness.

- Accounting accrues reserves not only for overdue debts, but also for those that may be overdue.

- Tax accounting takes into account only amounts of debts for which the payment period has expired.

4. Place of reflection.

- In accounting - other expenses.

- In tax accounting - non-operating expenses.

5. Reserve amount.

- In accounting in an organization and an enterprise, the amount of the reserve is not limited by anything.

- Tax authorities allow increasing the cost part by only 10% of the revenue in the reporting period.

What debt should be included in the reserve?

Let us say right away that the definition of doubtful debt has not changed.

As before, it includes any debts to the taxpayer arising in connection with the sale of goods, performance of work, provision of services and not repaid within the time period established by the agreement. An additional condition has also been preserved: debt is recognized as doubtful only if it is not secured by a pledge, surety or bank guarantee (clause 1 of Article 266 of the Tax Code of the Russian Federation). The rule still applies according to which doubtful debts with a period of occurrence from 45 to 90 calendar days are included in the reserve in the amount of 50%, and with a period of occurrence of more than 90 calendar days - in full (Clause 4 of Article 266 of the Tax Code of the Russian Federation).

But there is also an innovation. It is provided for a situation where the debt of the taxpayer and his debtor is of a reciprocal nature. That is, when not only the debtor owes the taxpayer, but the taxpayer himself owes the debtor. The “old” version of paragraph 1 of Article 266 of the Tax Code of the Russian Federation did not prohibit including the full amount of “receivables” in the reserve despite the presence of counter-debts. And although the tax authorities insisted that this could not be done, the judges did not support them (see Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated March 19, 2013 No. 13598/12; “The Presidium of the Supreme Arbitration Court of the Russian Federation: the company has the right to form a reserve for doubtful “receivables”, even if there are counter-accounts payable ").

Since January 2021, the situation has changed. From now on, paragraph 1 of Article 266 of the Tax Code of the Russian Federation clearly states: if a company has a counter obligation to a debtor, then doubtful debt is recognized as the part of the debt that exceeds this obligation (amendments were made by Federal Law No. 401-FZ of November 30, 2016). Please note: the innovation should be applied for the first time when forming a reserve based on the results of the first quarter of 2021 (hereinafter it is assumed that the reporting periods for the organization are quarter, half-year and 9 months). As for the reserve based on the results of 2016, one must be guided by the previous edition of the Code.

Example 1

As of December 31, 2021, Supplier LLC conducted an inventory of receivables and payables. It was revealed that Buyer LLC has accounts receivable of 800,000 rubles. with a period of occurrence of 65 days. A counter-account payable of the “Supplier” to the “Buyer” in the amount of RUB 500,000 was also revealed.

At the end of 2021, the Supplier's accountant formed a reserve for doubtful debts, including 400,000 rubles. (RUB 800,000 x 50%). At the same time, the maximum permissible reserve amount (we will discuss it in detail below) is not exceeded.

As of March 31, 2021, the Buyer’s receivables to the Supplier have not been repaid and have not been classified as uncollectible, and their period of occurrence exceeded 90 days. The counter payables of the “Seller” to the “Buyer” were also not repaid in the first quarter.

Based on the results of the first quarter, the Supplier's accountant created a reserve in the amount of 300,000 rubles (800,000 - 500,000), the maximum allowable amount of the reserve was not exceeded.

If the previous rules were still in effect, the Supplier would be able to include in the reserve the full amount of receivables in the amount of RUB 800,000. (subject to the limit).

Reflection of reserve formation in accounting

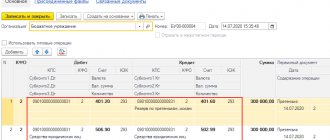

The amounts of the provision for doubtful debts reflected in the accounting records are estimates. Their inventory makes it possible to more or less reliably predict income in the reporting and coming periods. Debt amounts are reflected in “other expenses” in the account. 63 “Provisions for doubtful debts”. To do this, the following wiring is performed:

Debit 91-2 Credit 63 - an existing reserve has been created or increased.

When payment is received from the counterparty, the reserve by the amount received must be reduced. Then the restoration is carried out using the following accounts: Debit 51 (50) Credit 62 (71, 73, 76...) - funds were received from the debtor and Debit 63 Credit 91-1 - the reserve was reduced by the amount of the repaid debt.

Doubtful accounts receivable on balance sheet

Let's consider some accounting features of this phenomenon. The share of doubtful accounts receivable affects its total value. So, if the company failed to recognize the fact of doubtfulness, then the entire debt is reflected as a receivable. If everything fully complies with the conditions specified earlier in the article, then the reserve for doubtful debts of receivables is calculated as a liability. This reserve reduces the total amount presented in section No. 2 of the company’s balance sheet.

The write-off of doubtful accounts receivable occurs at the expense of the amount of the reserve, if, of course, it was created within the framework of the accounting policy. If the amount of the liability is greater than the amount of the reserve, then the difference is written off as company expenses, reduces the amount of income tax and, therefore, increases the amount of net profit.

Transfer, use and restoration of reserve

The created reserve enterprise (organization) has the right:

- postpone;

- use;

- restore.

Transfer

The created reserve is not always used in the reporting period for which taxes are paid to the budget (quarter or year). In this case, the balance can be carried forward to the next reporting period. To do this you need:

- at the end of the new reporting period, conduct an inventory of doubtful debts;

- calculate the volume of the reserve for the reporting quarter;

- check the accrued amount for compliance with the requirement for a limit of 10% of revenue;

- compare the resulting reserve amount with the balance on the first day of the reporting period.

There are two possible situations here:

- the amount of the new reserve is less than the transferred balance. In this case, the difference is included in non-operating income of the tax period;

- the balance is less than the accrued reserve, then the reserve is replenished from non-operating expenses.

If in the first quarter of next year a decision is made to abandon the accounting for the provision for doubtful debts, when calculating taxes you need to:

- make changes to the previously approved tax policy;

- show the balance of the reserve as of December 31 of the reporting year in non-operating income, increasing the capital of the organization;

- the operation should be reflected in the declaration on line 100 of Appendix No. 1 to sheet 02 and on line 020 of sheet 02 as part of general non-operating income.

Usage

The purpose of creating a reserve for doubtful debts is to reduce the amount of budget contributions in the form of income tax. Write-off of bad receivables is carried out in the following order.

- Documents are being collected. Some of them must show how the debt arose: supply or purchase and sale agreements, shipping documents or certificates of work performed, letters of claim to the debtor. The second part is required to confirm the fact of the impossibility of collecting: extracts from the State Register of Legal Entities or the tax inspectorate on the liquidation of the debtor, court decisions, etc.

- A certificate signed by an accountant is being prepared justifying the need to write off the debt.

- An order from the manager is issued to write off the debt at the expense of the reserve.

Recovery

After the debt is written off, an inventory of doubtful debts is again carried out at the end of the reporting period. If it is greater than the balance, the reserve is restored at the expense of non-operating expenses.

Features of creation

How to create a reserve for doubtful debts of accounts receivable? Its amount depends on how long the debt is overdue. Establishing these deadlines is a fairly reasonable decision of the state, since doubtful receivables are debts that are not returned on time, and, of course, the likelihood that a liability that is overdue for 10-15 days will be returned is much higher than if this time was six months or a year. Accordingly, due to differences in the likelihood of debt repayment, there is also a difference in the volume of recognized reserves.

So, if the counterparty does not repay the debt within a period of one to 45 days, this receivable cannot be considered doubtful, since this period is too short. Doing business is not always predictable; perhaps the counterparty does not repay the debt due to an unexpected cash gap; therefore, for this reason, such types of debts are not recognized as doubtful, do not increase the amount of the reserve and do not reduce the amount of income tax paid

If the debt period is from 45 to 90 days, then it is recognized in the amount of 50% of the total amount, increasing the amount of the reserve by this amount.

Accounts receivable with a maturity exceeding 90 days are recognized in full.

Provision for debts in tax accounting

In tax accounting, a reserve for doubtful debts is created and used according to the provisions of Art. 266 Tax Code of the Russian Federation. He can:

- created by a written order of the manager;

- formed by legal entities that keep accounting on an accrual basis;

- include only late payments for goods, works and services.

In addition, the reserve is accrued in fixed amounts related to the duration of the delay:

- up to 45 days - 0%;

- from 45 to 90 days - 50%;

- over 90 days - 100%.

Analytical accounting is maintained for each debt. The total amount of the reserve should not exceed 10% of revenue for the reporting period excluding VAT.

Instead of a conclusion. Properly organized accounting of doubtful debts helps mitigate financial problems that arise when payments are missed. When the moment comes when the debt becomes a bad debt, the legal entity repays it from the reserve, reducing the tax base (profit).

General procedure for creating a reserve for doubtful debts

The general procedure for creating a reserve for doubtful debts has not changed. Let's remember the main points.

To form a reserve, an inventory of receivables must be carried out on the last day of the reporting (tax) period (clause 4 of Article 266 of the Tax Code of the Russian Federation).

The amount of the provision depends on the period of occurrence of the obligation. A reserve for the full amount is created only for those debts that are overdue by more than 90 calendar days. If the delay is from 45 to 90 calendar days, only 50 percent of the debt amount is included in the reserve. For debts with a maturity of no more than 45 days, a reserve cannot be created.

The reserve is formed for the entire amount of the debt, including VAT, not transferred by the buyer (letter of the Ministry of Finance of Russia dated August 3, 2010 No. 03-03-06/1/517).

Revenue is determined according to the rules of Article 249 of the Tax Code. This means that the maximum reserve amount is calculated from “net” (excluding VAT) revenue.

The total amount of the provision for doubtful debts is limited.

Read also: “Any bad debt can be written off using the reserve for doubtful debts”