In this article, we will look at the procedure for conducting an inventory of intangible assets, briefly understand the legal provisions governing this area, take a look at the rules of procedure and find out how the results are recorded. We will also touch on all related issues, one way or another, related to these concepts.

The essence of the object

So, intangible assets are the commercial values of the company. Accordingly, they are aimed purely at obtaining benefits. Otherwise, they are not recognized as such; they also do not have a material form, they are immaterial. But they belong to the company legally. This can be either full copyright, which in fact should be equated to ownership, or use by proxy for a temporary period with restrictions. This category refers to that part of the property that is not involved in turnover. After all, their sale occurs not just once, but constantly during the period that they are owned. Receiving benefits multiple times is the main goal. Therefore, accounting is carried out as an inventory of the non-current assets of the enterprise.

But even though they do not have a material form, they are still subject to accounting, the results of which are stored in special documents. Of course, it is impossible to verify the actual availability by regular reconciliation. After all, they don’t exist in the physical world. But it is permissible to identify the documentary basis for their use, the correctness of execution, the correctness of reception or transmission, the possibility of implementation within a certain period of time and in a specific geographical area.

Moreover, often the number of such objects can even exceed the rest; accordingly, verification becomes a lengthy procedure. And it is extremely difficult to carry out it without the appropriate knowledge, as well as suitable software.

Objects that do not meet the criteria for recognition as assets.

These include objects that do not bring economic benefits to the institution, do not have useful potential, and for which it is not planned to receive economic benefits in the future (clause 8 of the GHS “Fixed Assets”).

In other words, these are fixed assets for which a decision has been made to write off (cessation of operation), including due to physical or moral wear and tear and the impossibility (inexpediency) of further use.

If such objects are identified during the inventory, the commission makes a decision to write them off the balance sheet and reflect them on off-balance sheet account 02 “Material assets in storage” until dismantling (disposal, destruction). In cases provided for by law, this decision is agreed upon with the owner of the property (see above).

Accounting for objects that do not meet the criteria for recognizing them as assets in off-balance sheet account 02 is carried out in the conditional valuation “one object - one ruble” (clause 335 of Instruction No. 157n).

Business Solutions

- shops clothing, shoes, groceries, toys, cosmetics, appliances Read more

- warehouses

material, in-production, sales and transport organizations Read more

- marking

tobacco, shoes, consumer goods, medicines Read more

- production

meat, procurement, machining, assembly and installation Read more

- rfid

radio frequency identification of inventory items More details

- egais

automation of accounting operations with alcoholic beverages Read more

Inventory procedure for intangible assets

When checking the availability of intangible assets, the commission should determine the actual presence of the intangible asset itself, as well as monitor the correctness of their reflection in analytical and synthetic accounting, check the presence of inventory cards and the correctness of their execution. Memorial orders No. 10, 13, 17 are also subject to verification. Also, the commission’s tasks during the audit of intangible assets include checking the accounting for depreciation of the corresponding intangible assets.

After the audit, the inventory committee determines whether accounting is being kept legally, whether the information specified in the accounting is reliable and whether there are inventory cards for each of the intangible assets. After the inspection, it is necessary to document the inventory of intangible assets.

Inventory list of intangible assets

In order to begin the process, it is first necessary to understand what falls into our field of vision.

And this:

- Copyright. It is generally accepted that these include only various achievements in the field of culture and art. Works of art, paintings, illustrations, musical fragments or video sequences. But the list turns out to be much wider. This should include programs, various models, plans, strategies, algorithms and much more. And the specificity from cultural easily develops into scientific.

- Patents. These rights relate to inventions. That is, some kind of device, mechanism, form, graphical shell and much more. The key difference is that in this case it is not the specific result itself, for example, a scientific article. But only a principle that is further used only by those whose action is permitted by law.

- Slogans, names, trademarks, brands and similar. The main value is in the commercial component. And also in associations that people assign to a certain name.

- The reputation of the project, infringement of which is punishable under the current legislation of the Russian Federation.

And these are just simple objects. These include those whose use is permitted on the basis of a separate document. But if one paper makes it possible to implement a mass of patents at once, these are already complex. Which also fall under the inventory.

In addition to those listed, the verified documents also include certificates of state registration and licenses. It all depends on what needs to be legalized.

Purpose and rules

In fact, the inventory of fixed assets and intangible assets is an audit, but it has its own personal characteristics and rules. Which it is better to adhere to in order to carry out the procedure as correctly as possible.

As you know, this method is the best way to control the safety of property. Constantly examine whether all title documents are in order. Enter them into the database, note their presence, and record that their service life has not yet expired. But all actions are performed according to the following rules.

- A certain frequency is established. The number of inventories is the competence of the founders and management; arbitrary is acceptable. But this is if we talk about optional events. But the audit should definitely be carried out at least once a year, before closing the annual reporting. And also in cases where the employees responsible for security left their positions and other persons took their place. The same principle works when changing the organizational structure of a company: reorganization, merger or even liquidation. Especially if the cessation of activity occurs against the backdrop of accumulated debts, not to mention bankruptcy. When detecting theft, it is also necessary to carry out an event for reliability.

- The implementation falls on the shoulders of a special commission. It must include certain links, representatives of accounting, management, experts and other employees. The appointment of the composition is carried out by the director or his authorized deputy. This is the only way to take inventory of non-financial intangible assets; for example, an assistant manager, an accountant, an appraiser, a loader and, inevitably, a storekeeper. Or another person who bears personal responsibility for the safety of the values being studied.

- Even before the start of the action, the commission receives all the papers that record the acceptance, distribution or transfer of objects. To be aware of the state of affairs, to know what to compare with.

- The final result is strictly recorded in duplicate. And this does not happen at the end of the entire event, but at the end of the working day. Even if everything resumes in the morning. The reporting is certified by all those present. The storekeeper also signs, as a supervisory authority that verified the legality and absence of criminal intent during the event. After all, he has financial obligations in case of loss.

- If there are discrepancies in any plan, a special statement is drawn up. It, like the title order, the results of the inventory of intangible assets for each working day, constitutes a complete reporting package.

Regulatory regulation

From the point of view of the law, the main regulator is the order of the Russian Ministry of Finance. It was established back in 1995 at number 49. It reflects the very fact of the need for reconciliation and puts forward basic definitions of key concepts. But the specific procedure and conditions are not regulated. They were changed already in 2007. Again, by the Ministry of Finance, but in PBU (accounting regulations).

Any deviations from the norms specified in the law indicate a violation. And the results obtained are not considered true, and it is unacceptable to refer to them. If a violation of an essential condition has been identified, the procedure must be repeated.

How is it carried out?

The procedure for conducting the inventory is important; intangible assets identified as a result will have to be checked again if there is a violation of the regulations. Therefore, we will pay close attention to it.

Initiation occurs by implementing an order in a special form. This is INV-22. But it does not work in all cases. It, in fact, forms a new commission that will solve the task. But if all the required members already exist as usual and are constantly engaged in this matter, then another order is activated. This is INV-23.

The procedure also applies to storekeepers or other responsible persons. In addition to direct supervision, they also create their own small reports. Or rather, they fill out receipts. The fact that a specific object was registered was revealed during the inspection. Or written off at the end of its operational life. And besides this, they enter all the details of the papers that were handed over to the members of the commission for review. And they strictly note their return to storage.

By the way, if previously the responsible persons were given funds for the purchase of certain goods, both tangible and intangible, and reporting on sales was not carried out, this is also noted.

It is noteworthy that the commission also has an additional goal: deciding whether the things being checked are these intangible assets. Do they meet all the requirements, categories, and conditions specified in the order of the Ministry of Finance? And if something does not fit the description, a corresponding entry is made about it. And he himself is excluded from view during the procedure.

Measures taken based on the results of the inspection

Upon completion of the inspection, the materials are transferred to the manager for approval. The end date of the inspection is the day the documents are signed by the head of the enterprise. The data obtained serves as the basis for making decisions based on the results of the inventory.

| Data identified during the audit | Measures taken |

| Indicators of full compliance of the audit results with the records were obtained | No action taken |

| An asset created or acquired after 2001 does not meet the exclusivity requirement | Attribute costs to current expenses or account 97 “Deferred expenses” if the asset is expected to be used for a long time |

| An asset not included in the accounting data was identified | Information from the inventory and statement serves as the basis for registering an intangible asset |

| An object received on temporary basis with an expired contract was identified | A write-off act is issued |

| An intangible asset with obsolescence has been identified | |

| A shortage of intangible assets resulting from the actions or inactions of the guilty parties has been identified | After documentary confirmation of those responsible for the shortage, the loss is written off at the expense of the responsible persons. |

| A shortage of intangible assets has been identified, the perpetrators of which have not been identified | The shortfall is written off to financial results |

Inventory of intangible assets, documentation of intangible assets

The main final document is the statement. It is formed strictly according to the INV-1A model. And although it is often led by only one person, all members of the commission must confirm the fact of their participation and agreement with the indicated results. And the responsible persons, of course, including.

But, as we have already clarified, there is also a second statement, a comparison statement. It is not always initiated, but only in cases where there are discrepancies. Unaccounted for values or, on the contrary, the absence of such when they are noted on papers. Its form sounds like INV-18.

All results obtained are sent to the accounting department. What is noteworthy is that now, or rather, since 2013, the requirement for strict compliance with the form has been abolished. Of course, in many companies the surplus of intangible assets (INA) identified during the inventory and their reflection is also shown in the matching statement INV-18. But with amendments, companies have the right to develop their own personal form. And act on it, marking documents in your own way. Of course, if the variation does not in any way contradict the legal norms established by the Ministry of Finance. Otherwise, such a form will be excluded and not taken into account.

It’s easier to adapt your own form to automated verification. Which is ten times superior to manual in both speed and quality. , offers various software solutions. They will make the procedure an easy task. With the help of mobile applications adapted to all amendments of the Ministry of Finance, reconciliation is much easier, and recording a report does not require a lot of fiddling with papers and studying reports.

What data is checked?

During the verification process, it will be necessary to check whether the asset corresponds to the concept of intangible asset. Intangible assets must have documentary evidence of the intangible asset itself and exclusive rights to it. The inventory process confirms the presence of a patent, a certificate of copyright or trademark, an agreement for the acquisition of an exclusive right and other documents.

One of the main criteria for classifying an asset as an intangible asset is its exclusivity, when determining which it is necessary to take into account:

- In the absence of exclusive rights, the object does not belong to intangible assets and the costs of its acquisition or creation are expensed.

- The requirement applies to intangible assets created after 2001.

- Previously, the condition for classifying an asset as an intangible asset was the right arising from other types of contracts.

Contracts for intangible assets identified during the inspection before 2001 with expired contracts for the transfer of non-exclusive objects, their description is included in the inventory. Based on the compiled materials, objects are written off from the off-balance sheet account.

Business Solutions

- the shops

clothes, shoes, products, toys, cosmetics, appliances Read more

- warehouses

material, in-production, sales and transport organizations Read more

- marking

tobacco, shoes, consumer goods, medicines Read more

- production

meat, procurement, machining, assembly and installation Read more

- rfid

radio frequency identification of inventory items More details

- egais

automation of accounting operations with alcoholic beverages Read more

Accounting entries

Based on the results of the audit, surpluses or shortages of assets may be identified. Therefore, if they are available, after a complete inventory of intangible assets has been carried out, synthetic accounting entries are reflected accordingly.

Table. Postings for reflecting surpluses and shortages of intangible assets.

| Business transaction | Debit | Credit |

| Capitalization of surplus into other income | 04 | 91 |

| Write-off of shortfalls for other expenses | 91 | 04 |

According to legislative norms, the head of the enterprise has the right to independently establish the period and frequency with which the inventory of intangible assets will be carried out; entries, accordingly, will also be reflected with the same frequency. For example, management has decided to conduct an inventory every quarter before reporting, so the identified discrepancies must be reflected in the quarterly reports.

In addition to the inventory carried out for the purpose of generating accounting documentation for the reporting period, checking the availability of intangible assets is carried out when revaluing assets, when identifying theft, when changing the MOL, as well as in the event of force majeure situations that lead to damage or liquidation of assets.

Similar articles

- Inventory tasks

- Inventory of intangible assets

- Inventory list of intangible assets (sample)

- How to take an inventory and document it

- Inventory list of intangible assets (sample)

Surpluses and disadvantages

For clarity, we will show what the final table looks like. After all, checking the accounting of the results of the inventory of intangible assets is an important part, which is mandatory before the commission members add their signatures.

| Action | D-t | Kit |

| Accounting for surplus | 05 | 92 |

| Written off depreciation due to surplus valuables | 06 | 05 |

| Write-off with value terms | 93 | 05 |

| Transferred to the repayment account at the expense of the financial responsible person | 70 | 93 |

| Difference from the market price and the potential balance when written off at the expense of the financial responsible person | 72 | 73 |

| The amount of potential income after the compensation is realized | 70 | 72 |

| Total losses based on findings | 98 | 95 |

“1C: Accounting 8” (rev. 3.0): how to take into account intangible assets identified during the inventory (+ video)?

How to take into account property rights to the results of intellectual activity identified during the inventory from January 1, 2021 in “1C: Accounting 8” edition 3.0?

The video was made in the program “1C: Accounting 8” version 3.0.75.100.

In a letter dated December 18, 2019 No. 03-03-06/1/99180, the Russian Ministry of Finance recalls that subclause 3.6 of clause 1 of Article 251 of the Tax Code of the Russian Federation allows income in the form of property rights to the results of intellectual activity identified in the course of inventory.

At the same time, paragraph 2 of Article 2 of the Federal Law of July 18, 2017 No. 166-FZ establishes that the provisions of subparagraph 3.6 of paragraph 1 of Article 251 of the Tax Code of the Russian Federation apply in relation to property rights identified from 01.01.2018 to 31.12.2019 inclusive during the course of the taxpayer’s inventory period.

From 01/01/2020, income tax must be paid on such income.

At the same time, the Tax Code of the Russian Federation does not provide for a procedure for determining the initial value of intangible assets (intangible assets) identified as a result of inventory, as well as the possibility of their depreciation (clause 3 of Article 257 of the Tax Code of the Russian Federation, letter of the Ministry of Finance of Russia dated December 18, 2019 No. 03-03-06 /1/99180, Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated March 4, 2008 No. 13106/07).

Receipt of Goods is used to register surplus property

(

Warehouse

).

The tabular part of the document indicates the product, product, material or other property, which is selected from the Nomenclature

.

For information on how to take into account income in the form of the value of surplus inventories and other property that are identified as a result of the inventory, see here.

When registering property rights to the results of intellectual activity, use the Intangible Assets

, therefore the document

Receipt of goods

is not suitable for this purpose.

To take into account property rights to the results of intellectual activity identified during the inventory, you should use the document Operation

(section

Operations – Operations entered manually

).

In the accounting register, you need to enter an entry for the debit of account 08.05 “Acquisition of intangible assets” with the corresponding analytics in correspondence with account 91.01 “Other income” with the type of other income item: Surplus goods identified as a result of inventory

.

In the Amount

field, you should indicate the documented market value of intangible assets (clause “a”, clause 28 of the Regulations on accounting and financial reporting in the Russian Federation, approved by order of the Ministry of Finance of Russia dated July 29, 1998 No. 34n; Instructions for the use of the Chart of Accounts for Financial Accounting - economic activities of organizations, approved by order of the Ministry of Finance of Russia dated October 31, 2000 No. 94n; paragraphs 5, 6, Article 274, Article 105.3 of the Tax Code of the Russian Federation).

Acceptance of intangible assets for accounting is reflected in the document of the same name (section OS and intangible assets

).

On the Tax Accounting

, in

the Procedure for including costs in expenses field

, select the value

Inclusion in expenses upon acceptance for accounting

and indicate the cost item (or other income and expense item) not taken into account for profit tax purposes.

If the organization records calculations according to PBU 18/02 (approved by order of the Ministry of Finance of Russia dated November 19, 2002 No. 114n) in the program using the balance sheet method (method based on the recommendation of BMC No. R-102/2019-KpR “Procedure for accounting for income taxes”) , then the resulting difference between the book value and tax value of the intangible assets will be considered temporary.

In the month of registration of intangible assets when performing a regulatory operation Calculation of deferred tax according to PBU 18

included in the

month-end

, a deferred tax liability (DTL) is recognized for the type of asset

Intangible assets

.

At the same time, a permanent tax expense (PTR) is recognized, which is reflected in the certificate-calculation Income tax expense

generated for the specified period.

Thus, the value of intangible assets identified as a result of inventory and not taken into account in tax expenses generates both temporary and permanent (“complex”) differences.

As intangible assets are depreciated in accounting, they will be repaid.

What is checked during the process, inventory object of intangible assets

As we have already clarified above, the main task is the reconciliation of documents. But at the same time, it is not just the availability of the necessary paper that is calculated. There are a lot of factors that the commission pays attention to.

First of all, the place of application is studied. Everything is permissible for use only in a certain area. Of course, sometimes the entire Russian Federation is a territory. But often this location is much narrower.

Attention is also drawn to the correctness of the design. If an error was made in the preliminary records, for example, about capitalization, then now the assessment is not made as such. After all, there was no receipt. First you need to correct the mistake.

Next, each object is checked for compliance with the definition of intangible assets, focusing on legal norms in the form of orders of the Ministry of Finance. And only if the value, in principle, fits the given definition, the title documentation is checked.

The depreciation period is determined, as well as the permissible maximum period of use.

Conditions for recognition of intangible assets

According to the Methodological Guidelines approved by Order No. 49, intangible assets are those that meet the following conditions:

- intangible assets are confirmed by the presence of documents for the right to be recognized as intangible assets;

- correct and reliable reflection of information on intangible assets;

- registration within the appropriate time frame.

Like all property assets of an enterprise, intangible assets must be registered and accounted for on the balance sheet accordingly. Maintaining accounting records, as well as the procedure for inventorying intangible assets, is regulated by the provisions of PBU 19/02.

How often to initiate the procedure

As we have already clarified, it is necessary to carry out this once a year, when changing the organizational structure or when replacing the person responsible for storage. The rest depends specifically on the organization and the amount of valuables in the property. For small volumes and constant use, it is, in principle, permissible not to carry out additional measures. But if the quantitative factor goes off scale, then it is better to issue a corresponding order at least once every 3 months. And if there is an opportunity and free employees, then even more often.

What is inventory of intangible assets and their revaluation

According to these accounting rules, intangible assets subject to inventory may be:

- Programs developed for computer technology.

- Scientific developments.

- Literary opuses and everything related to art, creativity and music.

- Collected databases.

- Inventions.

In this case, there must be papers confirming the possibility of using copyrights for one or more inventory items.

Concept and relationship with inventory of fixed assets

Such an inventory is carried out when:

- Any transactions with assets (sale, rental, purchase).

- Preparation of an annual accounting report.

- Change of company management.

- Liquidation of the company.

- In the event of precedents arising with the unlawful use of intangible assets.

But not more than once a year. The purpose of this event is:

- Identification of the presence of an asset owned by the company.

- His condition.

- Documentary confirmation of his affiliation with the company’s intangible assets.

- The state of its accounting.

Intangible assets do not belong to the company's fixed assets, but to simplify the procedure, their inventory can be carried out jointly. Moreover, in some high-tech companies they are closely intertwined.

Inventory of fixed assets and intangible assets - topic of the video below:

Features and Requirements

Also, when conducting an inventory, they check whether the controlled objects correspond to their status. That is, they should be:

- Intangible.

- Separated from other types of company property.

- Used when creating a company's commercial product.

- With correctly executed documents confirming the exclusive ownership of the company.

- Not for resale.

Revaluation

Intangible assets are accepted for accounting at the original price, which corresponds to the actual costs incurred. Revaluation is carried out no more than once a year for groups of assets of the same type, according to current market valuation. It can be either positive - an increase in value, or negative - a decrease in value.

Find out how to solve your specific problem. Ask a question right now using the form (below), and within an hour a specialist in the field will call you back to provide a free consultation.

conclusions

To summarize, this process is extremely important for almost any commercial project. After all, there is not a single person who does not use such intangible assets to at least some extent.

The main thing is to understand that not only knowing how to conduct an inventory of intangible assets will allow you to obtain effective results. But also the appropriate software, which will also simplify the task. And for exclusive offers developed specifically for the needs of a specific company, you should contact us. Cleverence software will always help you solve a problem faster, easier and more productively.

Here you can download the necessary documentation layouts.

Number of impressions: 3213

Checking intangible assets for impairment. Example

Enterprises often initiate an inventory count before revaluing intangible assets or a group of assets. The basis for revaluation is the discrepancy between the valuation of assets and the real market value. After revaluation, assets are carried at fair value. The initial cost and accrued depreciation of intangible assets are subject to revaluation. As a result of revaluation, assets are revalued or devalued.

The possibility of revaluation is approved in the accounting policy. Enterprises conducting revaluations are required to carry them out regularly in the future. The change in value and depreciation accrued as of the date is made using a coefficient derived from a comparison of prices. Intangible assets of a unique nature (patents, trademarks and analogues) are not subject to revaluation due to the lack of comparative samples.

Example of asset revaluation after inventory

Let's consider an example of revaluation of an asset after an inventory, during which an expert assessment of the market value of the asset was considered.

The organization Concord LLC carried out an inventory of intangible assets, based on the results of which a decision was made to re-evaluate the value of the Iskra object - registered software. The revaluation was carried out for the first time; there are no other objects on the balance sheet. The residual value of the object at the time of revaluation is 50,000 rubles with accrued depreciation of 5,000 rubles. The market value is estimated at 60,000 rubles (coefficient 1.2).

| Action | Calculation | Wiring |

| Revaluation of original cost | 55,000 x 1.2 = 66,000 rubles | |

| Revaluation of cost | 66,000 – 55,000 = 11,000 rubles | Dt 04 Kt 83 – 11 000 |

| Revaluation of depreciation | 5,000 x 1.2 = 6,000 rubles | |

| Overestimation of depreciation | 6,000 – 5,000 = 1,000 rubles | Dt 83 Kt 05 – 1 000 |

| Calculation of residual value | 66,000 – 6,000 = 60,000 rubles |

The revalued residual value is reflected in the balance sheet. Read also: → account 04 in accounting (postings, example)

Frequency and procedure for conducting an inventory of intangible assets, recording the results

Intangible assets (intangible assets) of an enterprise are considered to be property objects operated by the copyright holder for a long time (more than a year), contributing to the generation of profit (economic benefit), which do not have a physical embodiment (material expression).

Intangible assets of an organization belong to the category of non-current assets and, as is known, require proper accounting.

Such objects are often products of intellectual activity or, alternatively, means of unambiguous individualization of their copyright holder.

Such assets appear in a company as a result of purposeful actions of an interested party to create, transfer/receive or acquire them.

The main feature of all these activities is that the enterprise has an exclusive right to the beneficial use of the corresponding intangible asset.

In order to reliably determine (clarify) the presence of intangible assets, their condition and the degree of obsolescence, it is necessary to regularly conduct an inventory (audit, verification) of the relevant assets in the company.

It is important for specialized specialists to know what such an inventory is, how often it should be carried out, in what order it is carried out, what documents are used to document its results, and how its accounting is carried out.

The specifics of appropriate accounting actions based on the results of an inventory carried out for certain intangible assets are determined by the result that was obtained - full compliance with accounting information or identification of a shortage/surplus.

It should be noted, however, that some aspects of the conduct and execution of such an audit are specifically regulated by regulatory requirements that are generally binding.

What is a concept

The accounting information for intangible assets, verified and confirmed by the corresponding inventory, is used by the accountants of the copyright holder enterprise.

Based on the information, annual financial statements and all interim balance sheets are compiled.

Periodic checking of the presence and condition of such assets helps to monitor their safety and increase the efficiency (profitability) of their practical use.

The inventory of certain intangible assets may result in one of the following results:

- The results of the audit performed completely coincide with the accounting data.

- Identification of assets not recorded in accounting at the start date of the audit. The detected intangible material is included in the inventory list and registered.

- Damage, loss, and other force majeure circumstances determined the absence of intangible assets, which, however, were registered by the copyright holder enterprise. The fact that there is no documentary justification for the intangible asset is recorded in the inventory act indicating the guilty party.

As a rule, an inventory of existing intangible assets is assigned for individual situations (cases), prompting the company's management to check the actual status of these assets on a certain date.

How often is it carried out for NMA?

In principle, the management of the copyright holder organization usually independently regulates the frequency, frequency and specific timing of the inventory of intangible objects.

However, it must be carried out in the fourth quarter of the reporting year - immediately before the preparation and preparation of annual financial statements.

In all other situations (cases), the feasibility and necessity of such an event are determined at the discretion of management.

Thus, in order to collect the necessary information for the preparation of annual financial statements, it will be enough to audit intangible assets once during the year.

To check the presence of intangible assets at the enterprise, assess their actual condition, and also clarify the reliability of the relevant accounting documents, you can perform an inventory of these assets no more than once per six-month period.

Except for those cases when inventory activities are carried out at the enterprise without fail, inventory of intangible assets can be carried out more often, that is, as necessary/expedient, in the following situations:

- the occurrence of force majeure circumstances that led to partial/complete loss of assets (flooding, fire, etc.);

- establishing facts of damage, theft, and other malicious actions committed in relation to the organization’s assets;

- the assets of the enterprise are revalued by specialists at current market prices;

- the structure of the organization is modified (the owner changes, the company is liquidated, it is merged);

- more than 50% of the group of responsible entities of the copyright holder enterprise is subject to release (dismissal);

- a materially responsible entity is replaced at the enterprise, whose competence includes ensuring the safety and accounting of objects;

- other circumstances.

Order of conduct

Inventory of intangible assets at an enterprise is usually carried out by special commissions - one-time or regularly operating.

As a rule, such a commission includes at least three people - the chairman and ordinary participants.

The start of the inventory procedure is formalized by an appropriate order from management (form INV-22).

If the inventory commission operates at the enterprise permanently, the execution of an administrative act of management is not in this case a necessary condition for starting a mandatory inventory.

If such an order is nevertheless issued, it is registered in the accounting book compiled according to the INV-23 standard.

A mandatory requirement when performing the next audit of intangible assets is the direct participation in this procedure of entities that are personally responsible for the safety and proper accounting of the relevant assets.

Responsible entities draw up the necessary receipts, which are included by the commission in the inventory documentation package.

Such papers (receipts) clearly confirm the following facts:

- Intangible assets are written off by the enterprise according to the time limits regulated for disposal;

- 24114899objects at the disposal of responsible entities are accounted for and registered;

- documents recording the receipt, movement, movement and disposal of intangible assets are transferred to authorized persons for the purpose of performing checks.

If responsible entities were previously issued accountable funds for the acquisition (purchase) of an intangible asset, and a documentary report on these amounts was never transferred to the accounting department, a receipt must be drawn up indicating the existence of such circumstances.

An asset inventory, first of all, should clarify whether a specific property item is an intangible asset.

In other words, does this asset meet the regulatory requirements for intangible assets?

In addition, it is necessary to check the availability of documentary evidence of the intangible asset, and also find out whether the owner of the company has an exclusive right to it.

You should check whether the organization that owns the right has patent documentation, copyright certificates, registration paper for a trademark, an agreement on obtaining an exclusive right, and other documents.

Accounting for results: surplus, shortage

The results of the audit of intangible assets are reflected in accounting as follows:

| Operation (description) | Debit | Credit |

| Detected surplus intangible assets are recorded and taken into account | 04 | 91 (according to the subaccount of other income) |

| Write-off of accumulated depreciation for identified shortages of intangible assets | 05 | 04 |

| Write-off of detected shortages of intangible assets at the residual value | 94 | 04 |

| Attribution of the residual value of the shortage to the account of the guilty entity | 73 (according to subaccount) | 94 |

| Attribution of the difference between the market price and the book value of the shortage to the account of the guilty entity while simultaneously reflecting it in future income | 73 (according to subaccount) | 98 (according to subaccount) |

| Payment of monetary compensation to the enterprise by the entity responsible for the shortage | 70,51,50 | 73 (according to subaccount) |

| The amount of future income upon compensation of the shortfall by the guilty entity is transferred to other income | 98 (according to subaccount) | 91 (according to subaccount) |

| Attribution of the detected shortage to non-operating costs if the culprit is absent | 91 (for subaccount of other expenses) | 94 |

| Damage caused to an enterprise by a detected shortage of intangible assets is classified as losses | 99 | 91 (according to the subaccount of the balance of other income/expenses) |

| If the culprit reimburses the company for the amount of the detected shortage, it is taken into account as non-operating income | 91 (according to the subaccount of the balance of other income/expenses) | 99 |

conclusions

Inventory (audit, condition check) of intangible assets is of great importance for increasing efficiency and improving the quality of accounting in an enterprise.

When implementing it, it is necessary to follow generally binding regulatory requirements affecting the frequency, procedure, documentation and accounting of this aspect.

Deviations, inconsistencies, discrepancies discovered by the authorized commission based on the results of such an inspection are subject to correct documentation and proper accounting.

Source: https://praktibuh.ru/buhuchet/vneoborotnye/nma/inventarizatsiya-nematerialnyh-aktivov.html

Lecture. Inventory of fixed assets and intangible assets

The accounting unit for fixed assets is an inventory item. An inventory item of fixed assets is an object with all its fixtures and accessories, or a separate structurally isolated item intended to perform certain independent functions, or a separate complex of structurally articulated items that constitute a single whole and are intended to perform a specific job. When accepted for accounting, each fixed asset item is assigned its own inventory number.

Fixed assets can come to the organization as a result of their acquisition for a fee, under an exchange agreement, on a gratuitous basis, as a contribution of the founders to the authorized capital, as a result of construction and in other ways that do not contradict current legislation. Fixed assets are accepted for accounting at their original cost.

From the moment the fixed asset is received and until it is put into operation, accounting for the fixed asset will be carried out on account 08 “Investments in non-current assets”, the following entry is made in the accounting records:

Debit 08 “Investments in non-current assets” Credit 60 “Settlements with suppliers and contractors” - reflects the receipt of fixed assets into the organization.

When putting a fixed asset object into operation, the following posting is made:

Debit 01 “Fixed assets” Credit 08 “Investments in non-current assets” - fixed assets were put into operation.

After the fixed asset is put into operation from the 1st day of the next month, it will be necessary to calculate depreciation in accordance with the chosen method.

A fixed asset object can be put into operation only on the basis of an order from the manager. The accounting service of the enterprise prepares the Certificate of acceptance and transfer of fixed assets according to forms No. OS-1 “Act on acceptance of transfer of fixed assets (except for buildings, structures)”, No. OS-1a “Act on acceptance and transfer of a building (structure), No. OS-2 “Invoice for the internal movement of fixed assets,” but if several objects are put into operation at the same time, then use form No. OS-1b “Act on the acceptance and transfer of groups of fixed assets (except for buildings, structures).”

Commissioned fixed assets are recorded in inventory cards according to forms No. OS-6,

No. OS-6a.

In small enterprises, an inventory book in form No. OS-6b can be used .

The write-off of fixed assets is documented by the following primary documents: “Act on the write-off of fixed assets” (form OS-4), “Act on the write-off of motor vehicles” (form OS-4a), “Act on the write-off of groups of fixed assets (except for motor vehicles) )" (form OS-4b).

After the order of the head of the enterprise is approved to conduct an inventory of fixed assets:

— checking the availability and correctness of filling out primary documents for accounting, commissioning and disposal of fixed assets;

— the condition of inventory cards, inventory books, inventories and other analytical accounting registers is checked,

— checking the availability and condition of technical passports or other technical documentation for each fixed asset, the availability of documents for fixed assets leased or accepted by the organization for storage.

If, in the course of monitoring the availability of primary documentation for the inspected fixed asset objects, it is revealed that there are no documents for any of the inspected fixed asset objects, it is necessary to find out the reasons for their absence, as well as ensure their receipt or registration.

If, at the stage of preparation for the inventory, any inaccuracies and discrepancies in the accounting registers or technical documentation are revealed, it is necessary to make appropriate corrections and clarifications.

In the course of checking the actual availability of fixed assets, members of the commission, led by the chairman, must inspect all objects; their full name, purpose, inventory number and main technical or operational indicators are entered into the inventory list.

If such objects of fixed assets as land plots, reservoirs and other natural resource objects are subject to inspection, in this case it is also necessary to check the documents confirming the presence of these objects in the ownership of the organization, establish their quality condition, identify unused or not used objects for their intended purpose natural resources, establish the reasons.

If during the inventory the commission identifies objects of fixed assets that have not been accepted for accounting, as well as objects for which there will be no data in the accounting registers, or the specified information characterizing the fixed assets will be incorrect, the commission must include correct information and technical information in the inventory indicators for these objects. The assessment of such unaccounted for objects must be made taking into account market prices, and depreciation is determined based on the actual technical condition of the objects, with information about the assessment and depreciation recorded in the relevant acts.

Fixed assets are included in the inventory by name in accordance with the direct purpose of the object. If an object has undergone restoration, reconstruction, expansion or re-equipment and, as a result, its main purpose has changed, then it is entered into the inventory under the name corresponding to the new purpose.

If the commission established that the work carried out of a capital nature (adding floors, adding new premises, etc.) or partial liquidation of buildings and structures (destruction of individual structural elements) were not reflected in the accounting records and led to a change in the book value of the object, it is necessary to use the relevant documents determine the amount of increase or decrease in the book value of the object and provide data on the changes made in the inventory.

If any machines, equipment and vehicles are listed on the balance sheet of the enterprise, each of them is entered into the inventory individually, indicating the factory inventory number according to the technical passport of the manufacturer, year of manufacture, purpose, capacity, etc.

If there are similar items of household equipment, tools, machines, etc. of the same value, received simultaneously in one of the structural divisions of the organization and taken into account on a standard group accounting inventory card, the inventories are carried out by name, indicating the quantity of these items. Fixed assets that, at the time of inventory, are located outside the location of the organization (on long-distance voyages, sea and river vessels, railway rolling stock, vehicles; machinery and equipment sent for major repairs, etc.) are inventoried until their temporary disposal.

For fixed assets that are not suitable for use and cannot be restored, the inventory commission draws up a separate inventory indicating the time of commissioning and the reasons that led these objects to be unusable (damage, complete wear and tear, etc.).

Simultaneously with the inventory of own fixed assets, fixed assets in custody and leased are checked. For these objects, a separate inventory is drawn up, which provides a link to documents confirming the acceptance of these objects for safekeeping or rental.

For leased fixed assets, you need to check:

— availability of a lease agreement concluded in accordance with current legislation;

— if the contract is valid for more than one year, it is necessary to check the availability of a certificate of state registration of the lease;

— intended use of leased fixed assets, if provided for in the contract;

— the procedure for calculating depreciation.

In the course of summing up the results of the inventory of fixed assets, when comparing accounting data and actual data obtained during the audit, both a surplus of fixed assets and their shortage can be identified, and if the results of the audit reveal a shortage, it is necessary to identify the perpetrators.

If, as a result of the inventory, a surplus of fixed assets was identified, then to establish the value of the object, it is necessary to refer to clause 36 of the Guidelines for accounting of fixed assets, approved by Order of the Ministry of Finance of Russia dated October 13, 2003 No. 91n. According to this paragraph, unaccounted for fixed assets identified during the inventory are accepted for accounting at their current market value and are reflected as non-operating income.

The following entries are made in accounting:

Debit 01 “Fixed Assets” Credit 91 “Other Income and Expenses” sub-account “Other Income” - fixed assets recognized as surplus based on inventory results are taken into account.

Fixed assets identified during the inventory are classified as non-operating income received in kind.

If the inventory commission during the inspection reveals a shortage of fixed assets, it must be attributed to the perpetrators. In cases where the perpetrators are not identified or the court refuses to recover from the perpetrators, losses from shortages and damage are written off as production and distribution costs from the organization or a decrease in funding (funds) from the budget organization.

It must be remembered that in order to bring a financially responsible person to justice, his guilt must be proven in court. Therefore, upon completion of the inventory of fixed assets, members of the commission must draw up an act in which the damage caused to the organization by identified deficiencies will be recorded, the alleged causes of occurrence, an assessment of the damage at market value, the perpetrators are indicated, and recommendations are given to the administration of the organization on bringing the perpetrators to justice to limited or full financial liability, to file a claim with the judicial authorities, and, if necessary, to transfer the materials of the commission’s work to investigative or other authorized bodies.

If the perpetrators have not been identified, the following entries must be made in accounting:

Debit 01 subaccount “Retirement of fixed assets” Credit 01 subaccount “Fixed assets in operation” - reflection at the original cost of a fixed asset, the shortage of which was identified based on the results of the inventory;

Debit 02 Credit 01 subaccount “Disposal of fixed assets” - accrued depreciation is written off;

Debit 94 “Shortages and losses from damage to valuables” Credit 01 subaccount “Disposal of fixed assets” - reflects the residual value of the object;

Debit 94 “Shortages and losses from damage to valuables” Credit 68 subaccount “VAT” - displays the amount of VAT attributable to the residual value of the fixed asset;

Debit 91 subaccount “Other expenses” Credit 94 “Shortages and losses from damage to valuables” - the amount of the shortfall is reflected as part of other expenses.

Expenses for the liquidation of fixed assets, in accordance with the Tax Code of the Russian Federation, should be classified as non-operating expenses, income from spare parts and materials received during the liquidation - to non-operating income.

If, nevertheless, the guilty persons have been identified, and the obligation to compensate for damage will be assigned to them, then the amount of damage to be compensated, according to Art. 250 of the Tax Code of the Russian Federation will be classified as non-operating income, and the date of recognition of such income will be the date of recognition by the debtor, or the date of entry into legal force of a court decision - for income in the form of fines, penalties and (or) other sanctions for violation of contractual or debt obligations, as well as in the form of amounts of compensation for losses (damage).

In accounting, the identified shortage of property will be written off at the expense of the guilty parties and the following entries must be made:

Debit 94 “Shortages and losses from damage to valuables” Credit 01 “Fixed assets” - writing off the cost of the missing fixed asset;

Debit 73 subaccount “Calculations for compensation of material damage” Credit 94 “Shortages and losses from damage to valuables” - compensation for identified shortfalls at the expense of the guilty party.

In accordance with Art. 138 of the Labor Code of the Russian Federation, the amount of all deductions for each payment of wages cannot exceed 20 percent, and in cases provided for by federal laws - 50 percent of wages. If wages are withheld according to several executive documents, the employee, in any case, must retain 50 percent of the wages. If the requirements of the Labor Code of the Russian Federation regarding the procedure for collecting damages are not met, the employee of the organization has the right to appeal the employer’s actions in court.

When conducting an inventory of fixed assets, before starting the inventory, according to the Order, it is recommended to check:

— the presence and condition of inventory cards, inventory books, inventories and other analytical accounting registers for fixed assets;

— availability and condition of technical passports and other technical documentation;

— availability of necessary and correctly completed documentation for fixed assets leased or accepted by the taxpayer or for safekeeping.

Members of the commission inspect the objects being inspected; the inventory includes the full name of the object, its purpose, the inventory number assigned upon acceptance for accounting, as well as the main technical or operational indicators. A check is carried out of documents confirming the location of the inspected fixed assets in the ownership of the organization. The availability of relevant documents for land plots, reservoirs and other natural resources owned by the organization is checked.

If fixed assets are identified that were not accepted for accounting, or were accepted with incorrect data, they must indicate the correct information and technical indicators for these objects in the inventory. At the same time, the assessment of the value of unaccounted for fixed assets identified during the inventory will be made by experts.

In accordance with paragraph 3 of Art. 257 of the Tax Code of the Russian Federation, intangible assets are recognized as acquired and (or) created by the taxpayer results of intellectual activity and other objects of intellectual property (exclusive rights to them), used in the production of products (performance of work, provision of services) or for the management needs of the organization for a long time (duration over 12 months).

In order to recognize an object as an intangible asset, it is necessary to have the ability to bring economic benefits (income) to the taxpayer, as well as the availability of properly executed documents confirming the existence of the intangible asset itself and (or) the taxpayer’s exclusive right to the results of intellectual activity (including patents, certificates, other documents of protection, agreement of assignment (acquisition) of a patent, trademark).

The formation of information in accounting about the intangible assets of an enterprise occurs on the basis of the Accounting Regulations “Accounting for Intangible Assets” PBU 14/2007, approved by Order of the Ministry of Finance of the Russian Federation dated December 27, 2007 No. 153n.

In accordance with this provision, in order to accept an object for accounting as an intangible asset, the following conditions must be simultaneously met:

— the organization is able to exercise control over the object;

— documents are available confirming both the existence of the asset itself and the organization’s rights to it (for example, a patent, certificate, etc.);

— the asset is capable of bringing economic benefits to the organization in the future;

— this asset can be isolated or separated from other objects;

— subsequent resale of the asset is not expected;

— the asset is expected to be used for more than 12 months;

— the initial cost of the object can be reliably determined;

— the asset does not have a tangible form.

Intangible assets include rights to works of science, art and literature, various programs for electronic computers, inventions, and trademarks.

Intangible assets, in accordance with the Tax Code of the Russian Federation, in particular, include:

1) the exclusive right of the patent holder to an invention, industrial design, utility model;

2) the exclusive right of the author and other copyright holder to use a computer program, database;

3) the exclusive right of the author or other copyright holder to use the topology of integrated circuits;

4) exclusive right to a trademark, service mark, appellation of origin of goods and company name;

5) the exclusive right of the patent holder to selection achievements;

6) possession of know-how, a secret formula or process, information regarding industrial, commercial or scientific experience.

The business reputation of the organization that arose in connection with the acquisition of another organization as a property complex as a whole is also taken into account as part of intangible assets.

Intangible assets do not include research, development and technological work that did not produce a positive result, as well as the intellectual and business qualities of the organization’s employees, their qualifications and ability to work.

The accounting unit for intangible assets is an inventory item. The inventory object of intangible assets is recognized as a set of rights arising from one patent, certificate, agreement on the alienation of the exclusive right to the result of intellectual activity or to a means of individualization, etc., intended to perform certain independent functions. A complex object that includes several protected results of intellectual activity (a movie, another audiovisual work, a theatrical performance, a multimedia product, a single technology) can also be recognized as an inventory item of intangible assets.

To summarize information on the presence and movement of intangible assets owned by the organization, as well as on expenses for research, development and technological work for accounting purposes, account 04 “Intangible assets” is used.

Analytical accounting for account 04 “Intangible assets” is carried out for individual objects of intangible assets, as well as for types of expenses for research, development and technological work. The main task of setting up analytical accounting of intangible assets should be to ensure the possibility of obtaining data on the presence and movement of intangible assets, as well as the amounts of expenses for research, development and technological work.

If organizations use intangible assets under licensing agreements, these objects are recorded in off-balance sheet accounts.

Intangible assets are accepted for accounting at their historical cost.

The initial cost of amortizable intangible assets is determined as the sum of the costs of their acquisition (creation) and bringing them to the state in which they are suitable for use, with the exception of value added tax and excise taxes. The value of intangible assets created by the organization itself is determined as the amount of actual expenses for their creation, production (including material expenses, labor costs, expenses for services of third-party organizations, patent fees associated with obtaining patents, certificates), excluding amounts taxes taken into account as expenses in accordance with current tax legislation.

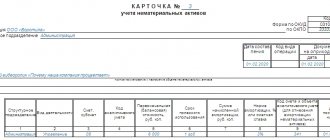

The main primary document for accounting for all types of intangible assets received for use by the organization is the Intangible Assets Accounting Card in the form of Intangible Assets-1. This card is compiled in the accounting department for each object in one copy on the basis of documents for capitalization, acceptance and transfer (movement) of intangible assets and other documentation.

The cost of intangible asset objects accepted for accounting in organizations is repaid by accruing depreciation over the established period of use of the object. If an intangible asset is used by a non-profit organization, then depreciation is not charged. Amortization is also not charged on intangible assets for which, in accordance with the established procedure, the cost is not repaid (trademarks, service marks, etc.).

To summarize information about the depreciation accumulated during the use of intangible assets, account 05 “Depreciation of intangible assets” is used, however, in some cases, depreciation can be written off directly - to the credit of account 04 “Intangible assets”. Analytical accounting for account 05 “Amortization of intangible assets” is carried out for individual objects of intangible assets. At the same time, the construction of analytical accounting should provide the ability to obtain data on the depreciation of intangible assets necessary for managing the organization and drawing up financial statements.

An inventory of intangible assets can be carried out either on the basis of an order from the head of the organization, or on the basis of an order from the head of the state tax service or his deputy.

When conducting an inventory of intangible assets, it is first necessary to check the availability of documents that would confirm the organization’s right to use it, because if the organization does not have such documents, the very acceptance of the object as an intangible asset was not legal. It is also necessary to check the correctness and timeliness of reflection in accounting.

When comparing accounting data and data obtained during the inventory of intangible assets, both their surplus and shortage can be identified, and, as in the case of fixed assets, it is necessary to identify the guilty parties.

In the accounting records of an enterprise, if a surplus of intangible assets is identified, the following entry must be made:

Debit 04 “Intangible assets” Credit 91 “Other income and expenses” subaccount “Other income” - previously unaccounted for intangible assets were capitalized based on inventory results.

If, as a result of the inventory, the absence of documents for an intangible asset is revealed (i.e., there are no grounds for accepting the object for accounting as an intangible asset), the following entries must be made in accounting:

Debit 05 “Amortization of intangible assets” Credit 04 “Intangible assets” - the amount of accrued amortization accrued from the moment the intangible asset was taken into account is written off.

Debit 94 “Shortages and losses from damage to valuables” Credit 04 “Intangible assets” - the residual value of an intangible asset is written off.

As a rule, when conducting an inventory, members of the inventory commission may identify the following types of violations:

— incorrect completion of primary documentation for the acceptance of intangible assets for accounting;

— unlawful acceptance of an object for accounting as an intangible asset;

— errors resulting from the formation of the initial cost of intangible assets;

— incorrect reflection of information on the movement of intangible assets in the accounting accounts.

Conducting an inventory of intangible assets in 2020

> intangible assets > Conducting an inventory of intangible assets in 2021

Inventory is a measure to verify the material and financial assets of the company. With the help of such a check, the safety of the company’s property and reserves is monitored. During the inventory, an inventory of property is carried out, which is subsequently subject to reconciliation with the data of previous inspections.

The rules for conducting inventory are regulated by the legislation of the Russian Federation and methodological materials of the Ministry of Finance. In order to carry out the inventory, a special commission is assembled, the composition of which is approved by the head of the company. It includes company employees. Warehouses, production areas, cash registers and retail areas are subject to inspection.

In this article we will look at how an inventory of intangible assets is carried out.

The legislative framework

According to the order of the Ministry of Finance of the Russian Federation No. 49 (clause 3.8), the object of the inventory is determined. Before conducting it, you will need to check the company’s right to use intangible assets, as well as the accuracy of the data reflected on the company’s balance sheet. The procedure for accounting and reporting is prescribed in PBU 14/2007.

The exact timing of the inventory, as well as the procedure for its implementation, is determined by the head of the organization independently. The exception is those cases that require mandatory verification. This process is also regulated by method guidelines, approved. Resolution of the State Statistics Committee No. 88 of 1998.

Documents used during the inventory of intangible assets

All data that the commission receives during the inventory process is recorded in a special statement INV-1a. Authorized persons responsible for the safety of documents regarding the state of intangible assets put their signature in the header of the statement.

If unaccounted for assets are discovered, they must be included in the inventory compiled during the audit. Such a document is drawn up in two copies, one of which will be kept by the person responsible for storing the documents, and the second is transferred to the accounting department.

All members of the inventory commission sign the inventory.

During the inspection, a matching statement is also drawn up in the INV-18 form. Such a statement is required in order to record the differences between the information obtained during the audit and the data specified in the accounting documents. The statement is also drawn up in two copies.

All results obtained during the inventory of intangible assets are reflected in accounting documents. If, as a result of the audit, surpluses are identified, they are indicated at the market price and entered in the financial result line. Identified deficiencies are subject to recovery from the guilty parties, and their accounting occurs in the same way.

Important! Since 2013, companies have the right not to use unified forms of documents. Therefore, in order to carry out verification, they have the right to independently develop forms of documents, as well as approve them in their internal policies. The main requirement when drawing up document forms is to indicate all the details regulated by law.

Carrying out an inventory of intangible assets

The following are the grounds for conducting an inventory of intangible assets:

- Transfer of ownership of an object to another person. The basis in this case may be a purchase and sale or rental agreement.

- Preparation of annual reports in accordance with legal requirements.

- Taking on the position of a new financially responsible person, an authorized employee.

- The emergence of suspicions of theft of property, abuse of property, or any other violation.

- Disaster.

- Process of liquidation and reorganization.

The inventory of intellectual property in temporary possession is carried out in the presence of its owner.

During the inventory, documents confirming the right to operate, the relationship with the conditions of use and the timeliness and correctness of accounting are subject to verification..

The NMA does not include scientific, literary and other works located on any kind of tangible media.

Before conducting an inventory, responsible persons must provide a receipt. The result of the check is indicated in the comparison sheet, which is filled out on the basis of the inventory. The result of the check is recorded in the month in which the inventory was completed. The annual inventory is recorded in the annual report.

Important! After the inventory process is completed, the act is transferred to the head of the company or to the central commission. The date of the final inventory result is determined by the date of approval of the documents by the manager.

How often is an inventory of intangible assets carried out?

Source: https://buhland.ru/provedenie-inventarizacii-nematerialnyx-aktivov/