What an exporter of goods to Belarus needs to know: legal acts and VAT rate

Belarus is a member of the Customs Union (CU) and is subject to the rules in force on the territory of the CU member countries. When exporting goods by Russian suppliers to the territory of this republic, it is necessary to comply with the norms of the relevant legal regulations:

- Clause 1 Art. 72 of the Treaty on the Eurasian Economic Union (signed on May 29, 2014) - this clause determines that in mutual trade between the member countries of the Customs Union, indirect taxes are collected according to the principle of the country of destination, which provides for the application of a zero VAT rate and (or) exemption from excise taxes when exporting goods .

- Appendix No. 18 to the Treaty on the Eurasian Economic Union (EAEU) - it describes the procedure for collecting indirect taxes when exporting goods and the mechanism for monitoring their payment.

The following figure will help you become more familiar with this procedure in relation to the export of goods from Russia to Belarus:

The moment of determining the tax base: according to the Protocol, but with an eye to the Tax Code of the Russian Federation

For the first time we exported goods to Belarus. In July, we collected a package of supporting documents and took it to the tax office. But they were not accepted, they said, bring them in October, when the third quarter ends. But 180 days from the date of shipment of goods will expire in September. If we submit documents in October, will we be required to pay VAT due to late export confirmation?

No, if, of course, all the documents are in order. The Protocol on Goods states that documents confirming the zero VAT rate must be submitted, on the one hand, within 180 calendar days from the date of shipment (transfer) of goods, and on the other hand, simultaneously with the tax return (Clause 2 of Article 1 of the Protocol on Goods ). Considering that the VAT return is submitted no later than the 20th day of the month following the expired quarter (Article 163, paragraph 5 of Article 174 of the Tax Code of the Russian Federation), tax authorities do not see anything reprehensible in the fact that a timely prepared package of documents will be submitted along with declaration for the quarter in which you collected it. After all, the Federal Tax Service believes that if the full package of export documents is collected, then the moment of determining the tax base for exports to the Customs Union countries is the last day of the quarter in which this happened (Letter of the Federal Tax Service of Russia dated May 13, 2011 N KE-4-3 / [email protected] ). As with regular exports (Clause 9 of Article 167 of the Tax Code of the Russian Federation; Letter of the Ministry of Finance of Russia dated 04/01/2008 N 03-07-08/81). Experts from the Ministry of Finance agree with this.

From authoritative sources Lozovaya A.N., Ministry of Finance of Russia “Since the moment of determining the tax base for VAT when exporting goods to Belarus and Kazakhstan is not established by the Protocol on Goods, this issue is regulated by the norms of the Tax Code of the Russian Federation. Thus, with confirmed exports to CU member states, the moment of determining the tax base is the last day of the quarter in which the full package of documents is collected (Clause 9 of Article 167 of the Tax Code of the Russian Federation). This means that if the deadline for collecting documents when selling goods for export to Belarus (Kazakhstan) expires, for example, in September, and the documents are collected already in July, then the VAT declaration along with the documents is submitted within the period from October 1 to October 20.”

Features of reflecting deductions in the VAT return depending on the type of goods exported

The procedure for filling out a VAT return depends on which group the exported goods belong to.

Note! The VAT declaration was updated by order of the Federal Tax Service dated August 19, 2020 No. ED-7-3/ [email protected] The form is used from the reporting campaign for the 4th quarter of 2021.

You will find a line-by-line algorithm with examples of filling out all twelve sections of the report in ConsultantPlus. Trial full access to the system can be obtained for free.

We are talking about dividing exported goods into raw materials and non-raw materials. The main criterion for such classification is the degree of human participation in the formation of the main characteristics of the product.

Enlarged groups of raw materials are listed in clause 10 of Art. 165 Tax Code of the Russian Federation:

Commodity codes were approved by Decree of the Government of the Russian Federation dated April 18, 2018 No. 466.

Goods not listed in clause 10 of Art. 165 of the Tax Code of the Russian Federation, relate to non-raw materials (letter of the Federal Tax Service of Russia dated August 3, 2016 No. 1-4-05/0021).

For these groups of goods, the following procedure for applying VAT tax deductions is established:

- Input VAT on the value of non-commodity goods intended for export is accepted for deduction in the quarter when the goods are registered and the other mandatory conditions for deduction are met.

Find out about the conditions for applying deductions from the material “What is the procedure for applying (accepting) tax deductions for VAT: conditions”.

- Input VAT on the cost of raw materials purchased for export is accepted for deduction in the quarter when the zero tax rate is justified (clause 1, clause 10 of Article 165, clause 3 of Article 172 of the Tax Code of the Russian Federation).

How to apply a VAT deduction if the product is a raw material, but it is not on the government list, find out in this publication.

Non-taxable goods are exported to Belarus with zero VAT

We trade goods that are not subject to VAT. We would like to conclude a foreign trade contract with a buyer from the Republic of Belarus. Will this export supply also not be subject to VAT at all?

No, you will have to include the export of goods to Belarus in transactions subject to VAT, but you will only apply a 0% rate. The fact that, according to Russian tax legislation, the sale of goods is not subject to VAT (Article 149 of the Tax Code of the Russian Federation) does not play a role. After all, the CU Agreement has priority over the Tax Code of the Russian Federation (Article 7 of the Tax Code of the Russian Federation). And neither the CU Agreement nor the Protocol on Goods provides for the possibility of exemption from VAT when exporting certain goods to Belarus (Articles 1, 2 of the CU Agreement; clause 1, article 1 of the Protocol on Goods; Letter of the Ministry of Finance of Russia dated 05.10.2010 N 03- 07-08/277; clause 4 of Letter of the Ministry of Finance of Russia dated 06.10.2010 N 03-07-15/131). True, in addition to the obligation to apply a zero rate, you also have the right to tax deductions (Clause 1, Article 1 of the Protocol on Goods; clause 2, Article 171, clause 3, Article 172 of the Tax Code of the Russian Federation). Moreover, despite the fact that according to the Tax Code of the Russian Federation the sale of your goods is not subject to VAT, the Ministry of Finance believes that if you do not submit documents in time to justify the zero rate, you will have to pay VAT for the period of shipment of goods (Clause 3 of Article 1 of the Protocol on Goods ).

From authoritative sources Anna Nikolaevna Lozovaya, Advisor to the Indirect Taxes Department of the Department of Tax and Customs Tariff Policy of the Ministry of Finance of Russia “When exporting goods, the sale of which is not subject to VAT on the basis of Art. 149 of the Tax Code of the Russian Federation, a 0% VAT rate must be applied to the territory of the member countries of the Customs Union (Article 7 of the Tax Code of the Russian Federation; clause 1 of Article 1 of the Protocol on Goods). If the exporter does not confirm this rate, he will have to charge VAT on the date of shipment at a rate of 18% (Clause 3 of Article 164 of the Tax Code of the Russian Federation). In this case, input tax can be deducted (Clause 2 of Article 171, paragraph 3 of Article 172 of the Tax Code of the Russian Federation). Such an operation will need to be reflected in Section. 6 of the VAT return, and not in section. 7".

VAT declaration for export to Belarus

Sales of goods to Belarus are reflected in the VAT return according to the following scheme:

What to do if documents confirming the zero rate are not collected in a timely manner? The answer to this question is in the ready-made solution from ConsultantPlus. If you do not have access to the K+ system, get a trial online access for free.

Find out which transaction codes to use to fill out a VAT return from the diagram below:

If goods are sold to a related party or a resident of an offshore zone, special codes from the specified application are applied.

The procedure for filling out individual lines of Section 4 depends on the type of product (commodity or non-commodity):

For a sample of filling out the updated VAT declaration form when exporting goods to Belarus, see ConsultantPlus, having received trial demo access to the K+ system. It's free:

The remaining sections of the declaration are completed in the usual manner.

Step-by-step instructions for accounting for VAT when exporting goods to the countries of the Customs Union.

dollars. A copy certified by the seal of the exporting company.

Documents were not collected on time: what to do with VAT reporting

Exports that are not confirmed on time require the submission of an updated declaration. Such a declaration has three important nuances:

- it is rented out per quarter of export shipment;

- must contain completed section 6;

- The composition of the information in section 6 depends on the type of goods exported (raw materials, non-raw materials).

Ipc-zvezda.ru

Attention

The starting date is considered to be the moment the product is placed under the customs procedure. This means that the papers along with the declaration must be sent to the government agency no later than the 20th day of the month following the expired tax period.

If the documentation could not be collected on time, the tax base is calculated on the day of shipment of the exported goods.

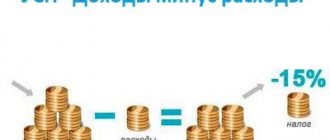

Moreover, the rate in this case is 10 or 18%. The main points of VAT calculations for exports According to Article 164 of the Tax Code of the Russian Federation, if goods exported to the territory of countries that are members of the Commonwealth of Independent States are sold, VAT is charged at a rate of 0%. Based on the statement, we can conclude that the tax is not actually levied if the requirements are met. However, there are differences between these operations.

What can prevent you from confirming your export on time?

Even if the exporter conscientiously approaches the procedure for collecting documents, there is no complete confidence that he will meet the deadline allotted by the Tax Code of the Russian Federation to confirm the validity of applying the zero VAT rate. This is due to the fact that the set of supporting documents includes an application for the import of goods, which the buyer must hand over to the supplier. And it is difficult to influence the actions of a buyer (especially one located abroad). At the same time, the absence of an application for the import of goods deprives the seller of a tax preference in the form of a zero VAT rate (if the buyer has not paid the tax).

The main difficulty in obtaining such a document is that the Belarusian buyer must pay the tax, put a stamp on the application with his tax authorities about payment and, with such a mark, transfer the application to the supplier.

It happens that the export seller was unable to receive an application because the buyer:

- for some reason I did not send the application, although I paid the tax;

- did not pay the tax and did not send anything to the seller;

- I sent the application, but without a tax payment mark.

There are two possible scenarios here:

- If the Belarusian buyer has paid the tax, the situation is not hopeless - Russian tax authorities can check the fact of tax payment in their database (within the framework of electronic information exchange), and the supplier himself can check in a special electronic service on the Federal Tax Service website.

- If the tax is still not paid, the Russian export seller will not be able to confirm the zero rate.

We will tell you in the next section what a supplier can do to protect itself from possible material losses due to unscrupulous buyers.

Simplified does not apply a zero VAT rate and does not issue an invoice

We are simplistic. We entered into an export agreement with a Belarusian company. The buyer wants us to issue him an invoice, with a 0% VAT rate. He refers to the fact that he needs the invoice to submit to the tax office. Should I issue him an invoice?

No. The zero VAT rate when exporting to Belarus should be applied only by VAT payers (Clause 1, Article 1 of the Protocol on Goods; Article 1 of the Customs Union Agreement). You are not one (with the exception of VAT paid upon import and under a simple partnership agreement or trust management of property) (Clause 2 of Article 346.11 of the Tax Code of the Russian Federation). Accordingly, there is no obligation to issue an invoice to the Belarusian buyer (Clause 3 of Article 169 of the Tax Code of the Russian Federation). This is also confirmed by the Ministry of Finance (Letter of the Ministry of Finance of Russia dated July 22, 2010 N 03-07-13/1/04). The interests of your Belarusian partner should not suffer from this. After all, the Protocol on Goods requires that when importing goods, tax invoices must be submitted only if their registration is provided for by law (Subclause 4, Clause 8, Article 2 of the Protocol on Goods). If an invoice is not issued, you can submit to the tax office and indicate in the import application any other document that indicates the cost of goods (Clause 1 of the Letter of the Federal Tax Service of Russia dated May 10, 2011 N AS-4-2 / [email protected] ). To resolve all issues, notify the Belarusian buyer in writing that your company applies a simplified taxation system. Your letter will have more weight if you attach to it a copy of a document from the tax office confirming that you are a simplifier. You can obtain such a document by sending a request to the inspection in any form. Tax authorities must respond to it within 30 calendar days from the date of its receipt (Letter of the Federal Tax Service of Russia dated 04.12.2009 N ШС-22-3 / [email protected] ; clauses 39, 44 of the Administrative Regulations of the Federal Tax Service of Russia on the performance of the state function of free information, approved by Order of the Ministry of Finance of Russia dated January 18, 2008 N 9n).

Contractual insurance against unscrupulous buyers

In order to somehow protect yourself from careless buyers from the EAEU, provide special conditions in your contracts with them. For example:

- The buyer's obligation to pay a fine (compensating for the seller's losses from paying VAT and penalties on it) if the import application is not received from him within the agreed period (for example, no later than 160 days from the date of shipment).

- An indication of the judicial authority (Russian or Belarusian) in which the dispute will be heard if the buyer refuses to pay penalties. It is no secret that it is better to protect your interests on your own territory with the participation of competent lawyers.

The “penalty” element of the contract may look like this:

Confirmation of the validity of applying the zero VAT rate

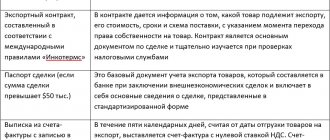

In accordance with paragraph 2 of Art. 1 of the Protocol on Goods, to confirm the validity of the application of the zero VAT rate by the taxpayer of the CU member state from whose territory the goods were exported, the following documents (copies thereof) are submitted to the tax authority simultaneously with the tax return:

- agreements (contracts) with amendments (additions and annexes) to them, on the basis of which the export of goods is carried out;

- application for the import of goods and payment of indirect taxes, drawn up in the form established by the Protocol on the exchange of information in electronic form between the tax authorities of the member states of the Customs Union on the paid amounts of indirect taxes dated December 11, 2009 (Appendix 1), with a mark from the tax authority of the state — a member of the Customs Union into whose territory goods are imported, on the payment of indirect taxes (exemption or other procedure for fulfilling tax obligations). It should be noted that by Order of the Federal Tax Service of Russia dated August 30, 2012 N ММВ-7-6/ [email protected] , the electronic format of the application for the import of goods and payment of indirect taxes by Russian taxpayers was approved;

- transport (shipping) documents provided for by the legislation of the CU member state, confirming the movement of goods from the territory of one CU member state to the territory of another CU member state.

- other documents provided for by the legislation of the CU member state from whose territory the goods were exported. Such documents may be required, for example, in the case of selling goods through an intermediary (Clause 2 of Article 165 of the Tax Code of the Russian Federation). They can be a commission agreement, a commission agreement or an agency agreement, reports from the intermediary on the performance of his duties, etc.

The exporter must provide the above documents to the tax authority within 180 calendar days from the date of shipment (transfer) of goods.

According to paragraph 3 of Art. 1 of the Protocol on Goods, the date of shipment is the date of the first drawing up of the primary accounting document issued to the buyer of goods or the first carrier, or the date of issuance of another mandatory document provided for by the legislation of the CU member state for VAT payers.

REGISTRATION AT CUSTOMS

If documents are not submitted within the prescribed period, VAT is payable to the budget for the tax (reporting) period in which the date of shipment of the goods falls. Further, if the taxpayer collects and submits the appropriate package of documents confirming the fact of export to Belarus, the paid VAT amounts are subject to deduction (offset) or refund.

In accordance with paragraph 6 of Art. 166 of the Tax Code of the Russian Federation, taxpayers are required to keep separate records of transactions for the sale of goods to Belarus, subject to VAT at a rate of 0%, and other transactions.

It should be noted that in addition to the above documents, tax authorities, in order to confirm the validity of VAT refunds on export transactions, require taxpayers to fill out the “VAT Refund: Taxpayer” program (version 3.0.8.2.).

Results

Exports of goods from Russia to Belarusian buyers are taxed at a rate of 0% if the supplier submits a set of supporting documents to the tax authorities along with the VAT return. If the documents cannot be collected on time, the supplier must submit an updated VAT return for the period in which the export shipment occurred.

Sources:

- Tax Code of the Russian Federation

- Treaty on the Eurasian Economic Union (signed on May 29, 2014)

- Decree of the Government of the Russian Federation dated April 18, 2018 No. 466

- Order of the Federal Tax Service of Russia dated October 29, 2014 No. ММВ-7-3/ [email protected]

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

How is zero VAT applied on exports to Belarus?

The export procedure in the direction of Russia - the Republic of Belarus is carried out in stages.

- Shipment. An invoice and invoice with a zero rate are generated.

- Drawing up and submitting a package of documents to confirm the export procedure. The foreign trade participant is given 180 calendar days for this. The starting point is the date of execution of the first document on the transfer of ownership of the goods from the seller to the buyer.

- Declaration of delivery. The number of the section of the VAT declaration to be filled out is determined by the fact of confirmation of export. Having selected a section, you must mark the export procedure code.

If the export documents were collected and sent to the tax authority on time, the shipment of the goods and all deductions are displayed in Section 4 of the VAT return for the quarter in which all documents were collected.

If it is impossible to collect documentation within a period of up to 180 days, the declarant enters the data in Section 6. It is included in the updated declaration for the quarter of shipment of products for export.

How to properly register the export of goods and products to Belarus

Their list is given in subparagraph 1 of paragraph 1 of Article 165 of the Tax Code of the Russian Federation. Article 164. Tax rates Article 165. Procedure for confirming the right to receive a refund when taxed at a tax rate of 0 percent If a company exporting goods uses the services of carriers who are not citizens and taxpayers of the Russian Federation, it must be guided by the provisions of Article 161 of the Tax Code of the Russian Federation. According to the provisions of the regulatory legal act, taxpayers of the Russian Federation using the services of foreign taxpayers must calculate, withhold and pay a certain amount of tax to the budget of the Russian Federation. In this situation, the company that exports goods will act as a tax agent for VAT. Article 161. Features of determining the tax base by tax agents The tax rate for a foreign person is 20%. Table of contents:

- The main nuances of VAT on exports

- Export to Belarus VAT

- VAT in 2021 on exports: changes and new rules

- VAT refund when exporting from Russia

- What documents are required for export to Belarus?

- VAT on export of goods

The main nuances of VAT for exports If a copy of the customs declaration is presented when importing goods, the customs officer carrying out the inspection must make a note on paper “The goods have been imported in full.” Now fill out the sixth section as follows:

- In column 1, in the same way as when filling out sections 4 and 5, reflect the transaction codes.

Fill in all other columns according to each code for which you had transactions.

- In column 2, indicate the tax bases for the relevant transactions separately for each VAT rate.

- In column 3, reflect the amount of tax, separately in accordance with the VAT rate, the validity of applying a zero rate for which has not been documented. Calculate the tax amount for each transaction code as follows: multiply the amount reflected in column 2 by the tax rate (10 or 18) and divide by 100.

- In column 4, reflect tax deductions for those transactions for which the validity of applying the zero rate has not been confirmed, i.e.

Accounting for exports to Belarus in 2021 from the supplier

Afterwards we concluded an agreement, helped find a new buyer for the lamps and continued to work together. Now this is our regular client, we refund export VAT immediately and complete all the paperwork. Export to Belarus in 2021 - the benefits of working with us are significant, here are some of them:

- We will get rid of paperwork;

- We will refund up to 50% VAT immediately;

- We will eliminate risks and downtime as much as possible;

- Personal manager who promptly resolves emerging problems;

In fact, we will conduct a turnkey transaction. Are you a manufacturer? Do you want to increase your profits? — we are ready to offer you to expand the markets for your products. We have the resources to promote your products abroad; with us it’s easier and faster. Contact our specialist and find out more details.