What applies to intangible assets

Under certain conditions, intellectual property objects (results of intellectual activity) can be taken into account as part of intangible assets. In particular:

- inventions, industrial designs, utility models;

- computer programs, Internet sites;

- trademarks and service marks;

- production secrets (know-how);

- breeding achievements (for example, for a grown plant variety or a bred animal breed).

In addition, the business reputation of the organization can be taken into account as part of intangible assets.

This is stated in paragraph 4 of PBU 14/2007.

The intangible assets of an enterprise cannot include:

- organizational expenses;

- intellectual and business qualities of personnel, their qualifications and ability to work.

Such rules are established by paragraph 4 of PBU 14/2007.

Conditions for classification as intangible assets

An object of intellectual property can be taken into account as part of intangible assets if the following conditions are simultaneously met:

- the organization is the holder of exclusive rights to the intangible asset. At the same time, the existence of the object itself and the exclusive rights to it must be documented;

- the organization has the right to receive economic benefits from the use of the facility;

- the period of use of the object exceeds 12 months, and the organization does not intend to resell it for at least 12 months;

- the original (actual) cost can be reliably determined.

This is stated in paragraph 3 of PBU 14/2007.

The conditions for recognizing intellectual property objects as intangible assets are presented in more detail in the table.

If the conditions for recognizing an object of intellectual property as an intangible asset are not met (for example, if the organization has not received a patent for an invention or the useful life of the object is less than 12 months), then its value can be taken into account as part of:

- expenses for research, development and technological work (R&D);

- deferred expenses;

- current expenses.

Rules for accounting for intangible assets

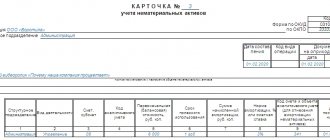

The unit of measurement of intangible assets is an inventory object. This term refers to the totality of all rights associated with the purchase of one asset. An object may include rights to a collection of objects.

Objects are recorded in account 04 “Intangible assets”. The accounting must indicate their original cost. The situation is somewhat more complicated with depreciation. In relation to some assets, it cannot be reflected on account 05 “Depreciation of assets”. Accruals are indicated in the credit column of account 4 “Intangible assets”. The receipt of objects into the enterprise is reflected in the debit of account 04. The correspondence will be account 08 “Investments in non-current assets”.

Rights to the created object

If an organization has created an object of intellectual property on its own, then the exclusive rights to it must be documented. Most intellectual property objects (results of intellectual activity) must be registered with Rospatent or the State Commission for Testing and Protection of Selection Achievements. Documents confirming exclusive rights to the created object are:

- certificate for a trademark (service mark) (Articles 1480 and 1481 of the Civil Code of the Russian Federation);

- certificate of exclusive right to the appellation of origin of goods (clause 2 of Article 1518 and Article 1530 of the Civil Code of the Russian Federation);

- patent for an invention, industrial design, utility model (Articles 1353 and 1354 of the Civil Code of the Russian Federation);

- patent for a selection achievement (Articles 1414 and 1415 of the Civil Code of the Russian Federation).

If the organization has received the necessary security documents, the created intellectual property object can be taken into account as part of intangible assets.

Some intellectual property objects are registered voluntarily, for example, the exclusive right to a computer program (Article 1262 of the Civil Code of the Russian Federation).

Rights to the transferred object

In addition to creating intellectual property on its own, an organization can obtain rights to them:

- under an agreement (license or alienation of an exclusive right) (Article 1233 of the Civil Code of the Russian Federation);

- in a non-contractual manner on the basis of the law (for example, during reorganization, foreclosure on the property of the copyright holder) (Article 1241 of the Civil Code of the Russian Federation).

In each of these cases, the organization acquires the rights to use the intellectual property. These rights may be exclusive or non-exclusive.

Depending on the type of agreement, an organization may receive all exclusive rights to an intellectual property object or only part of them.

To transfer all rights to an object of intellectual property, an agreement on the alienation of exclusive rights is concluded. In this case, the organization becomes the only one who can use the resulting intellectual property. This is stated in Article 1234 of the Civil Code of the Russian Federation.

If part of the exclusive rights to the result of intellectual activity is transferred, a license agreement is concluded. The license agreement can be of two types:

- simple (non-exclusive) license;

- exclusive license.

In the first case, the original owner of the exclusive right (licensor) reserves the right to issue licenses to other parties. That is, other organizations can also use this result of intellectual activity (means of individualization). In the second case, the organization is the only one who uses the object within the framework of the rights transferred to it. Such rules are established in Article 1236 of the Civil Code of the Russian Federation.

For example, a program for management accounting was developed at the request of an organization. According to the agreement, the organization has exclusive rights to use the program in its business activities, and the developer has exclusive rights to modify it. In such a situation, the developer does not have the right to provide the computer program for use by other persons, and the organization does not have the right to enter into agreements for modifying the computer program with other developers.

An object of intellectual property can be included in the intangible assets of a company only if the organization owns all the exclusive rights (for example, if an agreement on the alienation of an exclusive right was concluded or the organization became the copyright holder after reorganization). This follows from the provisions of paragraphs 38 and 39 of PBU 14/2007. To include the received object among intangible assets, you must have documents confirming exclusive rights. For example it could be:

- agreement on alienation of exclusive rights;

- transfer act (in case of reorganization in the form of transformation, merger or accession) or separation balance sheet (in case of division or separation of an organization) (Article 58 of the Civil Code of the Russian Federation).

The agreement must be registered with Rospatent (State Commission for Testing and Protection of Selection Achievements) in cases where the result of intellectual activity itself was registered (clause 2 of Article 1232, clause 7 of Article 1452, clause 5 of Article 1262 of the Civil Code of the Russian Federation) .

If only part of the exclusive rights to an intellectual property object has been received, then such an object is recognized as an intangible asset received for use. Since intellectual property objects received for use are not included in the organization’s balance sheet, it is necessary to maintain off-balance sheet accounting for them. This procedure follows from paragraphs 38 and 39 of PBU 14/2007.

The cost of the enterprise's intangible assets recorded on the balance sheet should be repaid by calculating depreciation (clause 23 of PBU 14/2007).

Inventory of fixed assets and intangible assets

An inventory of fixed assets and intangible assets is carried out based on the order of the head of the company or upon inspection by the tax authorities. A special commission is being created for this purpose. During the inventory the following is checked:

- availability and correct completion of primary documentation for commissioning and operation;

- condition of cards and other analytical accounting registers;

- correct reflection of the primary cost of objects;

- correct reflection of data on the movement of fixed assets and intangible assets on accounts.

When unaccounted for fixed assets are identified, they are classified as non-operating profit received in kind. If a shortage of intangible assets or assets is detected, then it is necessary to identify the guilty employees. When these are not established or the court refuses to compensate for losses, the shortage is written off as production costs or a decrease in funds.

Intangible assets are property that does not have a physical form, but represents for the enterprise. In addition, they, like fixed assets, are aimed at generating profit in the course of financial activities. Accounting for this group of funds is somewhat different from collecting information about the rest of the property. We will get acquainted with the features of its organization and the structure of the assets themselves in this article.

R&D

The costs of acquiring (creating) an object of intellectual property should be reflected as part of R&D if the following conditions are simultaneously met:

- the object was developed in-house by the organization or on its order;

- work to create an object can be classified as research or scientific and technical activities. The criteria for such activities are defined in Article 2 of the Law of August 23, 1996 No. 127-FZ;

- the result of R&D is not subject to legal protection or legal protection is not properly formalized (for example, if the invention does not require a patent or the organization for some reason did not patent its invention).

This follows from paragraph 2 of paragraph 1 and paragraph 2 of PBU 17/02.

Future expenses

If the cost of an intellectual property item cannot be reflected as part of R&D expenses, then the costs of its creation (purchase) should be included either in deferred expenses or in current expenses. The costs of acquiring (creating) an object of intellectual property that will be used in several reporting periods are considered as deferred expenses. For example, do this if, when purchasing the rights to use an object of intellectual property, the organization paid a fixed amount at a time. If this condition is not met, the costs of acquiring (creating) an object of intellectual property should be taken into account as part of current expenses. For example, do this if the organization makes periodic payments for the use of intellectual property. This procedure follows from paragraph 18 of PBU 10/99.

Costs for the acquisition (creation) of an intellectual property item, recorded as deferred expenses, are subject to write-off. The organization independently establishes the procedure for writing off expenses relating to several reporting periods. For example, an organization can write off a one-time one-time payment for the use of an object of intellectual property evenly over the period for which it was received. Fix the applied option for writing off deferred expenses in the accounting policy for accounting purposes. This is stated in paragraph 18 of PBU 10/99 and paragraphs 7 and 8 of PBU 1/2008.

An example of reflecting in accounting the costs of acquiring part of the exclusive rights to use a patented invention. For the use of a patented invention, the organization pays a fixed amount at a time

In January 2021, Alpha LLC entered into a license agreement with Proizvodstvennaya LLC (patent holder). Under the agreement, the organization receives part of the exclusive rights to use the patented invention for 2 years (24 months) - from February 1, 2021 to January 31, 2021.

Under the terms of the agreement, in January 2021, the “Master” is paid a remuneration in the form of a fixed one-time payment in the amount of 169,920 rubles, including VAT - 25,920 rubles.

Alpha's accounting policy states that deferred expenses are written off as current expenses evenly over the period to which they relate. In this case, during the validity period of the license agreement.

In accounting, Alpha's accountant made the following entries.

In January 2021:

Debit 012 – 169,920 rub. – the cost of an intangible asset received for use is taken into account;

Debit 97 Credit 60 – 144,000 rub. (RUB 169,920 – RUB 25,920) – remuneration accrued under the license agreement;

Debit 19 Credit 60 – 25,920 rub. – VAT on remuneration under the license agreement is taken into account;

Debit 68 subaccount “Calculations for VAT” Credit 19 – 25,920 rub. – accepted for deduction of VAT on remuneration under the license agreement;

Debit 60 Credit 51 – 169,920 rub. – remuneration under the license agreement is transferred.

Every month from February 2021, the accountant writes off (in proportion to the number of calendar days) part of the remuneration under the license agreement, taken into account as part of deferred expenses.

In February 2021:

Debit 20 Credit 97 – 5713 rub. (RUB 144,000: 731 days × 29 days) – part of the remuneration under the license agreement, previously taken into account as deferred expenses, was written off.

In March 2021:

Debit 20 Credit 97 – 6107 rub. (RUB 144,000: 731 days × 31 days) – part of the remuneration under the license agreement, previously included in deferred expenses, was written off.

The accountant made similar entries for writing off royalties under the license agreement, included as deferred expenses, until January 2021 (inclusive).

In January 2021, upon expiration of the license agreement, the accountant wrote off the value of the intangible asset acquired for use:

Credit 012 – 169,920 rub. – the value of an intangible asset received for use is written off.

An example of reflecting in accounting the costs of acquiring part of the exclusive rights to use a patented invention. For the use of a patented invention, the organization transfers monthly license payments

In January 2021, Alpha LLC entered into a license agreement with Proizvodstvennaya LLC (patent holder). Under the agreement, the organization receives part of the exclusive rights to use the patented invention for 2 years (24 months) - from February 1, 2021 to January 31, 2021.

According to the agreement, the cost of the intangible asset received for use is 169,920 rubles. Under the terms of the agreement, the “Master” is paid a monthly remuneration in the amount of 7,080 rubles, including VAT – 1,080 rubles.

The following entries were made in Alpha's accounting.

In January 2021:

Debit 012 – 169,920 rub. – the cost of an intangible asset received for use is taken into account.

Every month from February 2021 to January 2021, the accountant makes the following entries:

Debit 20 Credit 60 – 6000 rub. (RUB 7,080 – RUB 1,080) – remuneration accrued under the license agreement;

Debit 19 Credit 60 – 1080 rub. – VAT on remuneration under the license agreement is taken into account;

Debit 68 subaccount “Calculations for VAT” Credit 19 – 1080 rub. – accepted for deduction of VAT on remuneration under the license agreement;

Debit 60 Credit 51 – 7080 rub. – remuneration under the license agreement is transferred.

In January 2021, upon expiration of the license agreement, the cost of the intangible asset acquired for use was written off by the accountant:

Credit 012 – 169,920 rub. – the value of an intangible asset received for use is written off.

1

Accounting for fixed assets and intangible assets. Accounting for inventories, low-value and high-wear items.

Accounting for fixed assets must ensure the following tasks:

- correct execution of documents and timely reflection in accounting;

- reliable determination of the results from the sale and other disposal of fixed assets;

- complete cost determination;

- control over the safety of the OS.

Fixed assets are valued at initial, replacement, residual value, book value, liquidation value. The initial cost of fixed assets acquired for a fee is the amount of the organization's actual costs for the acquisition, construction and production, excluding VAT.

Accounting for fixed assets. Actual costs for the acquisition, construction and production of OS:

- 1. amounts paid by the organization in accordance with the supply, purchase and sale agreement;

- 2. amounts paid to organizations for carrying out work under a construction contract and other contracts;

- 3. amounts for information and consulting services related to the acquisition of fixed assets;

- 4. registration fees, state duties and other similar payments made in connection with the acquisition of rights to an OS object;

- 5. customs duties and other payments, etc.

Replacement cost is the sum of the costs of reproducing the OS at the time of valuation, i.e. how much does it cost to purchase the same or similar ones? Residual value is the real value of an object at a specific time of operation. Book value is the cost at which fixed assets are reflected on the balance sheet. Liquidation value is the value at which a written-off object can be sold, or the value that is attributed to losses upon liquidation of the asset. Depreciation is the process of gradually transferring the cost of fixed assets as they wear out to the product or services produced, in order to reimburse their cost and accumulate funds for subsequent full restoration. Assets costing over 20 thousand rubles are depreciated.

There are 4 ways to calculate depreciation:

- 1. linear;

- 2. reducing balance method;

- 3. method of writing off value by the sum of the numbers of years of useful life;

- 4. method of writing off the cost in proportion to the volume of production.

OS objects leave the organization as a result of:

- sale (sale) of an object to another legal entity or individual;

- write-offs in case of moral and (or) physical wear and tear;

- transfer of fixed assets in the form of a contribution to the authorized capital of other organizations; liquidation in case of accidents, natural disasters and other emergencies;

- transfers under contracts of exchange, donation of fixed assets; write-off of fixed assets previously leased with the right to purchase, etc.

To determine the feasibility and unsuitability of fixed assets for further use, the impossibility or ineffectiveness of its restoration, as well as to draw up documentation for the write-off of these objects, a permanent commission can be created in the organization by order of the head. The results of the decision made by the commission are documented in an act for writing off the asset. The act is approved by the head of the organization. Based on the completed acts for write-off of fixed assets, a note on disposal of the object is made in the inventory card.

Accounting for intangible assets. Intangible assets are the value of objects that do not have a material form, do not have physical properties, but provide the enterprise with the opportunity to receive income for a long time, have properly executed documents confirming the existence of the asset itself and the exclusive right to the results of intellectual activity, and have a long useful life. use, have the ability to be identified, and are not intended for resale. Intangible assets are accepted for accounting at their original cost. Additional expenses increase the initial cost of intangible assets. Depreciation is calculated based on the initial cost of the intangible asset and its useful life. The useful life of intangible assets is determined by the organization when accepting the object for accounting. The useful life of intangible assets is determined based on: the validity period of the patent and the expected period of use of this object. For intangible assets for which it is impossible to determine the useful life, depreciation rates are established for 20 years. The financial statements reflect the initial cost and the amount of accrued depreciation by type of intangible assets at the beginning and end of the reporting year, the cost of write-offs and increases, and other cases of movement of intangible assets.

Inventories. Inventory and equipment are assets used in the production of products, performance of work or provision of services, or for management needs for a period not exceeding 12 months or the normal production cycle, and are also intended for resale. The main objectives of inventory accounting are: 1. Formation of the actual cost of inventories. 2. Correct and timely documentation of operations and provision of reliable data on the procurement, receipt and release of inventories. 3. Control over the safety of stocks in storage areas and at all stages of their movement. 4. Monitoring compliance with inventory standards established by the organization. 5. Timely identification of unnecessary and excess stocks. 6. Conducting an analysis of the efficiency of use of reserves.

All operations involving the movement of inventories must be documented with primary documents, which must be properly executed. Inventory and equipment are accepted for accounting at actual cost. Materials are one of the types of materials. Upon acceptance, materials are thoroughly checked. Materials must be supplied in appropriate units of measurement. Reception acts and receipt orders must be drawn up on the day the relevant materials are received at the warehouse or other storage locations.

Shortages and damage are taken into account in the following order: – The amount of shortages and damage within the limits of natural loss norms is determined by multiplying the number of missing and (or) damaged materials by the contract price of the supplier. – shortages and damage to materials in excess of natural loss norms are accounted for at actual cost.

The spent material is written off on the basis of actual or standard consumption according to the act of writing off materials and is charged to expenses. Accounting for operations on the movement of materials is carried out in “materials accounting cards”. Records are kept by the financially responsible person on the basis of primary receipts and expenditure documents on the day of the business transaction. Accounting for auxiliary materials. For packaging and registration of medicines during their manufacture and dispensing, for in-pharmacy preparation and packaging for processing prescription glassware, maintaining the sanitary regime in pharmacies, the following materials are used: labels, stoppers, capsules and other materials. The posting and accounting of auxiliary materials is carried out in the same way as other materials. The spent VMs are written off according to the “certificate of standard consumption of materials” AP-53.

If the issuance of VM occurs according to the current need, then the financially responsible person must keep records of the issuance of VM by name, quantity, price, amount. At the end of the month, the accountant calculates the total expense and draws up a write-off report. Accounting for medicinal and plant raw materials. Medicinal plant raw materials accepted at the purchase price from the population are issued with an acceptance receipt f. AP-4, which is compiled in triplicate. This receipt is a strict reporting form. One copy of the receipt remains with the person who accepted the raw materials, and at the end of the month is attached to the pharmacy report. The second copy is presented by the person who handed over the raw materials to the cash desk, where he is paid the procurement cost of the raw materials. In this case, the receipt remains at the cash register. The third copy remains with the person who handed over the raw materials.

When selling drugs, an “Act on the transfer of drugs into goods” must be drawn up, on the basis of which drugs from the Raw Materials value group are transferred to Goods. Accounting for sanitary clothing. Sanitary special clothing is issued to employees in the manner established by the collective agreement based on standard industry standards for the free issuance of special clothing. Pharmacy establishments are obliged to provide their employees with gowns, caps, etc. The issuance and return of sanitary clothing to employees must be reflected in personal cards. It records the full name of the employee, what was issued, the basis for the issue, the period of wear, the date of issue and the signature of the recipient. Workwear issued to employees is the property of the organization and must be returned. Workwear can be accounted for either as fixed assets or as part of inventory. It depends on the period of its use. The cost of workwear, recorded as materials, is written off to cost immediately. The cost of workwear accounted for as fixed assets is depreciated if its cost is more than 10 thousand rubles, and if it is less than 10 thousand rubles. it can be written off as an expense immediately upon commissioning.

4. Accounting for goods.

The assortment, quantity and quality, order and terms of shipment and other delivery conditions are determined by supply contracts. To receive goods from a transport organization or supplier, an authorized person is issued a power of attorney of the established form. When selling, all organizations are required to provide the buyer with an invoice, which is issued in two copies. The supplier registers invoices in the Sales Book. After this, invoices are entered into the “Invoice Registration Journal”, filed with it and stored for a full 3 years from the date of issue. The buyer registers the received invoices in the “purchase book”, after which they are also registered and filed in the “Invoice Registration Journal” and are stored for a full three years. The main type of consumption of goods in a pharmacy is sales for cash and non-cash payments. To account for the cost of an extemporaneous recipe, use the recipe journal AP-65 or receipts for custom production of AP-59. When taxing extemporaneous prescriptions, it is necessary to highlight the cost of medicines, purified water, and manufacturing tariffs. It is necessary to separate out from the total sales drugs sold at a discount or free of charge. All these indicators are reflected in the AP-71 recipe log. To summarize data on preferential dispensing, a “Consolidated register of prescriptions for preferential dispensing of drugs”, form No. AP-9, is compiled.

Another type of production activity is laboratory and packaging work. Their records are kept in the “Register of Laboratory and Packaging Works”. Based on the monthly results of this journal, a “Certificate of additional valuation or markdown for laboratory and packaging work, implementation of work and services” is compiled. This data is also reflected in the department's product report. Production activities also include the production of purified water, which is used for the manufacture of drugs. Its cost is reflected as a separate line in the receipt for the ordered medicine and in the “Logbook for accounting for wholesale supply and settlements with customers. At the end of the month, these data are reflected in the AP-12 certificate and the product report. The pharmacy's production costs are covered by charging a tariff, which is taken into account in the same documents that reflect the cost of manufactured drugs. All calculations for the sale of goods to the public are carried out using cash register systems, therefore the main documents confirming the fact of sale of goods to the public are cash documents. When dispensing drugs, it is necessary to highlight sales with VAT of 10% and 18%.

Containers are a type of goods intended for packaging, transportation and storage of products, goods and other material assets. Containers are accepted for accounting at the actual cost, which consists of all expenses for its purchase and delivery or the costs of its production. Acceptance of containers from suppliers and buyers, release of containers to third parties, as well as movement of containers within the organization are documented with the same primary documents as for materials accounting. Containers that have become unusable due to natural wear, breakage or damage are documented with the appropriate document. The act is drawn up by a commission. The movement of containers is recorded in the “Material Warehouse Card” for each item, item number in quantitative terms. At the end of the month, financially responsible persons, drawing up the commodity report TORG-29, also draw up the “Container Report” TORG-30.

Accounting for the movement of fixed assets and intangible assets. Primary documents. Accounting for fixed assets.

Conditions for classification as OS:

- 1. useful life more than 12 months.

- 2. the object is intended for use in the production of products, performance of work and provision of services

- 3. the organization does not intend subsequent resale

- 4. the object is capable of bringing economic benefits in the future

- 5. cost over 40,000 for newly acquired objects, until 2012 – 20,000

Features of fixed assets accounting.

Assets are valued at primary, residual and recovered values. Primary cost is the cost of the equipment originally purchased. Residual value is the difference between the original cost and accumulated depreciation. Recovered value - arises as a result of revaluation of fixed assets, i.e. revaluation.

Features of accounting for the receipt of fixed assets - all actual costs associated with the acquisition of fixed assets minus VAT:

- OS cost

- transport services

- information and advisory services

- fees paid by the intermediary organization through which the asset was acquired.

- customs duties and fees

Costs are accounted for in account 08, subaccount 4. After being accepted for accounting, the total costs for account 08 are written off to account 01 (OS). Accounting for the acquisition of fixed assets under a purchase and sale agreement.

Primary documents for accounting of fixed assets: 1. act of acceptance - transfer of fixed assets, except for buildings and structures: FORM No. OS - 1 2. act of acceptance - delivery of repaired, reconstructed, modernizing fixed assets: FORM No. OS - 3 3. invoice for the internal premises of the OS object: FORM No. OS - 2 4. Inventory card for accounting of the OS object: FORM No. OS - 6 5. Inventory card for group accounting of the OS object: FORM No. OS - 6a 6. Inventory book for accounting of the OS object: FORM No. OS - 6b 7. Certificate of acceptance or receipt of equipment: FORM No. OS – 14

FORM Act No. OS - 1 is used to formalize and record the operation of receiving and transferring fixed assets within organizations or between them. The act, together with the technical documentation, is transferred to the accounting department, which, on the basis of this document, opens the corresponding inventory card. Acceptance of completed work on the reconstruction of equipment is formalized using FORM No. OS - 3. To register fixed assets within the organization, invoice OS-2 and act OS-14 are used. According to the object accounting of OS, accounting is carried out on inventory cards OS - 6, which are opened for a single object or a group of objects. Inventory cards are grouped into cards by sections and subsections.

Algorithm: 1. equipment purchased in the amount of actual costs: debit investment in non-current assets (08.4) credit settlement with suppliers (60.1) 2. reflected VAT on purchased equipment: D – VAT on acquired value (19.1) K – 60.1 3. payment of invoice supplier: D60.1K51 Current accounts 51 4. accepted for accounting OS: D01K08.4 Investments in non-current assets 08 4. Acquisition of fixed assets 5. accepted for deduction from the budget VAT: D68.2K19.1

Accounting for the acquisition of fixed assets under a gift agreement According to the Civil Code of the Russian Federation, Art. 575: donations between commercial organizations are allowed within 5 minimum wages (minimum wage - 4600). Upon receipt of fixed assets under a gift agreement, fixed assets are valued at market value and recognized as deferred income (98.2). As depreciation is calculated, future income is written off as income for the reporting period, from which 20% income tax is paid.

Algorithm: 1. equipment was received under a donation agreement: D08.4K98.2 2. fixed assets were accepted for accounting: D01K08.4 3. depreciation was accrued: D44K02 Selling expenses 44 Depreciation of fixed assets 02 4. as depreciation accrues, future income is written off included in other income of the organization: D98.2K91.1

Accounting for the receipt of fixed assets as a contribution to the authorized capital of the fixed assets is reflected in the assessment agreed with the founders, i.e. at a negotiated price. Investment-related transactions are not subject to VAT.

Algorithm: 1. organization created: D75.1K80 Settlements with founders 75 1. Settlements on contributions to the authorized (share) capital Authorized capital 80 2. contributed by OS founders to pay off debt: D08.4K75.1 3. acceptance for accounting: D01K08 .4

Accounting for depreciation of fixed assets Depreciation is accrued from the first day of the month following the month of acceptance for accounting. Termination of accrual - from the first day of the month following the month of disposal of the fixed assets. Depreciation is not accrued: 1. for fixed assets of non-profit organizations. Based on them, information on the amount of depreciation accrued in a straight-line manner is compiled on an off-balance sheet account 2. for objects received for rent 3. for environmental management objects Suspended for objects that are in the stage of repair and reconstruction for more than 12 months; if the equipment is sent for storage.

Methods of calculating depreciation: 1. linear - straight-line write-off method 2. reducing balance - accelerated depreciation 3. method of writing off value by the sum of numbers, years, useful life 4. method of writing off value in proportion to the volume of products or work

The use of one of the methods is carried out throughout the entire useful life of OS objects. Annual depreciation amount (ASA) - what amount of the original cost is depreciation charges for the year: ASR = cost of fixed assets * AGR Annual depreciation rate (ARR) - determines how much% per year depreciation should be accrued from the useful life: ACR = 100% / number of years or SPI in years

Methods for calculating depreciation: 1. linear GSA is determined based on the original cost and on the determined and SPI. Initial cost = 150 tr. SPI = 5 years

| Period | GSA | Accumulated depreciation amount | Residual value |

| 1 | 30 | 30 | 120 = 150-30 |

| 2 | 30 | 60 | 90 |

| 3 | 30 | 90 | 60 |

| 4 | 30 | 120 | 30 |

| 5 | 30 | 150 | 0 |

GSA = 100% / 5 =20% GSA = 150*20% / 100% 2. the reducing balance of GSA is determined based on the original cost at the beginning of the reporting period; GNA based on SPI and acceleration coefficient (by law: maximum value = 3) Initial cost = 150 tr. SPI = 5 years Acceleration factor: 2

| Period | GSA | Accumulated depreciation amount | Residual value |

| 1 | 60 | 60 | 90 |

| 2 | 36 | 96 | 54 = 150-96 |

| 3 | 21,6 | 117,6 | 32,4 |

| 4 | 12,96 | 130,56 | 19,44 |

| 5 | 19,44 | 150 | 0 |

1-4 years – first interval 2 = 90*20%*2 3 = 54*20%*2 4 = 32.4*20%*2 GSA = 100% / 5 =20% GSA = 150*20%*2 (acceleration coefficient) / 100% With t.z. Tax legislation in this method allows combining methods of calculating depreciation: Entire SPI / 2 time intervals: 1 = 80% of SPI, and 2 = 20% During the first interval, accelerated depreciation is used. At the beginning of 2, the residual value from 1 is taken as the primary value and written off in proportion to the number of months remaining until the end of the joint venture. Year 5: 19.44 * 12 months / 12 months = 19.44 This method is necessarily used for cars purchased by the organization with a cost of over 450,000.

3. The method of writing off the cost by the sum of numbers, years, useful life of the GSA is determined based on the primary cost and the ratio: Number of years remaining in operation until the end of the SPI / sum of the numbers of years of the SPI Initial cost = 150 tr. SPI = 5 years

| Period | GSA | Accumulated depreciation amount | Residual value |

| 1 | 50 | 50 | 100 |

| 2 | 40 | 90 | 60 |

| 3 | 30 | 120 | 30 |

| 4 | 20 | 140 | 10 |

| 5 | 10 | 150 | 0 |

1 = 150 * 5 years / 15 years 2 = 50 * 4 / 15 3 = 60 * 3 / 15 4 = 30 * 2 / 15 5 = 20 * 1 / 15 4. The method of writing off the cost in proportion to the volume of products or work of the State Automated Service is determined based on from the physical indicator of the volume of products or work in the reporting period and the ratio: Initial cost of fixed assets / total quantity of P or P that is expected to be produced for the entire SPI Initial cost = 150 tr. 1 = 250 units P 2 = 300 3 = 200 4 = 150 5 = 100 Zavest SPI = 1000 units P.

| Period | GSA | Accumulated depreciation amount | Residual value |

| 1 | 37,5 | 37,5 | 112,5 |

| 2 | 45 | 82,5 | 67,5 |

| 3 | 30 | 112,5 | 37,5 |

| 4 | 22,5 | 135 | 15 |

| 5 | 15 | 150 | 0 |

1 = 250*150 / 1000 2 = 300*150 / 1000 3 = 200*150 / 1000 4 = 150*150 / 1000 5 = 100*150 /1000 Organizations with seasonal work, cargo transportation.

Accounting for the disposal of fixed assets When disposing of fixed assets, account 91 is used. Other income and expenses 91 1. Other income 2. Other expenses 9. Balance of other income and expenses According to D91.2, all costs associated with the sale of fixed assets are reflected: residual value of fixed assets transportation costs expenses for dismantling equipment information and advisory services VAT on sales K 91.1 - income from sales is reflected. The difference between income and expenses is account 91.1. Account 91.1 corresponds only with the profit and loss account - 99. Income > expenses - D 91.9K99 Income < expenses - D99K91.9 01.1 reflects the initial cost of fixed assets remaining on the balance sheet 01.2 - retired from the balance sheet 01.3 - leased

Accounting for intangible assets

Conditions for classification as intangible assets: 1. absence of material structures 2. the object is capable of bringing economic benefits in the future 3. the organization has the right to receive economic benefits, i.e. has properly executed documents confirming the existence of the asset itself + the right of this organization to the results of intellectual activity 4. possibility of identification, i.e. separation of the object from others 5. the object is intended for use for a long time 6. the organization does not intend to sell the objects 12 months. 7. The original cost can be reliably determined. Personal qualities are not intangible.

Accounting for the acquisition of intangible assets. D 08.5 takes into account all actual costs associated with the acquisition of intangible assets. Algorithm: 1. intangible assets received in the amount of actual costs: D08.5K60.1 Investments in non-current assets 08 5. Acquisition of intangible assets Settlements with suppliers and contractors 60 2. VAT reflected: D19.2K60.1 Value added tax on acquired assets 19.2 . Value added tax on acquired intangible assets 3. supplier invoice paid: D60.1K51 4. state registration for transfer of ownership of intangible assets is reflected: D08.5K76 Settlements with various debtors and creditors 76 5. state registration of intangible assets is listed: D76K51 6. accepted for accounting of intangible assets: D04K08 Intangible assets 04 7. accepted for VAT deduction: D68.2K19.1 Calculations for taxes and fees 68 Value added tax on acquired assets 19.1. Value added tax on the acquisition of fixed assets

IMA: the exclusive right of the patent holder to an invention, industrial design, utility model - objects of intellectual property.

Conditions for classification as an invention: 1. absolute novelty 2. industrial applicability 3. high technical level 4. patentability Protective document – patent (20 years).

Industrial design: 1. level of technical development below 2. design implementation Security document - certificate (5 years, but can be extended for 3 years). Utility model: 1. object design

Protective document – patent (10 years, but can be extended for 5 years). the exclusive right of the author to use the computer program and database. Account 97 Deferred expenses 97 exclusive right of the author to a trademark, service mark, company name, appellation of origin of goods (these are means of individualization of legal entities or individuals) Protective document - patent, re-registration every 10 years. exclusive right of the patent holder to a selection achievement Protective document – patent (30 – 40 years). works of science, art, literature. Exclusive copyright is not transferred. Real ones are the opposite. possession of know-how - a secret formula or process or information regarding industrial, commercial and scientific experience.

The following do not apply to intangible assets: 1. intellectual, business qualities of personnel and their qualifications and ability to work 2. expenses associated with the formation of a legal entity (organizational expenses)

Accounting for depreciation of intangible assets 2 methods of calculation: 1. account 05 – for any intangible assets. D44.20K05 Amortization of intangible assets 05

Selling expenses 44 2. not using account 05 – mandatory when calculating depreciation on “+” business reputation for 20 years in a straight-line manner + intangible assets for which exclusive rights must be extended. D44.20K04 Intangible assets 04

Methods of calculating depreciation: 1. linear - straight-line write-off method 2. reducing balance - accelerated depreciation 3. method of writing off cost in proportion to the volume of products or work

Accounting for “+” and “-” business reputation. “+” and “-” business reputation arises as a result of the acquisition of the entire organization. “+” business reputation is the excess of the market value of the purchased object over the balance sheet.

!!! A company was acquired - 2 million 360 rubles. Property received under the transfer deed: Equipment = 1 million Goods = 400 tr. Materials = 160 tr. Short-term financial investments = 200 tr. Total = 1760 1. property received under a transfer deed: book value: D01K76 – 1 Settlements with various debtors and creditors 76 goods: D41K76 – 400 materials: D10K76 – 160 short-term financial investments: D58.3K76 – 200 Financial investments 58 3. Loans provided D01,41,10,58.3K76 – 1760 2. transferred from the current account: D76K51 – 2360 3. VAT on acquired property is reflected: D19K76 – 360 4. a “+” result was identified from the excess of the market value over the balance sheet 2360-1760-360 = 240 D08.5K76 – 240 Investments in non-current assets 08. 5. Acquisition of intangible assets Over 20 years, in a straight-line manner, “+” business reputation is written off as the cost of services: D44.20K04 – 1 (240/240 months = 1000) “-” business reputation goodwill – arises as a result of purchasing an organization below book value. Part of the property received free of charge is taken into account as deferred income.

!! A company was acquired – 1777 + VAT. Property received under the transfer deed: Equipment - 1 million Goods - 300 Raw materials and supplies - 120 Construction in progress (08.3) - 200 1. property received under the transfer deed: D 01.41, 10, 08.3 K 76 - 1620 2. invoice paid: D76K51 – 1777 3. VAT reflected: 1777*18 / 118 = 270. D19K76 – 270 4. “-” business reputation was identified, which is not intangible assets, but income for the future period: D76K98.1 – (120) Writes off to income of the reporting period monthly for 20 years deferred income: D98.1K91.1 – 500