Introductory information

The situation when a company is headed by its “founding father” is not uncommon in practice. Moreover, often such a manager is ready to perform his functions without receiving a monthly salary. There can be many reasons for this. There is a banal lack of funds, a desire to save on taxes and contributions, and simply a reluctance to “bother” with additional accounting and personnel issues. Unfortunately, regulatory agencies also play a significant role in this approach; they cannot decide whether the director, the sole founder, needs an employment contract. So such a manager works without a salary and an employment contract. But how safe is this approach for the company?

Registration of a director - the sole founder: a brief history of the issue

The question of whether it is necessary to conclude an employment contract with the director, the sole founder of the organization, has been the subject of constant debate for more than twenty years. Let us briefly recall how the position of officials and legislators changed (for more details, see “Is it possible not to pay a director’s salary: new facts, previous conclusions”).

In 2002, a provision appeared in the Labor Code of the Russian Federation stating that written employment contracts must be concluded with all employees, without exception. It followed from this that if the company’s staff list includes the position of director, then an employment contract must be drawn up with him.

But in a situation where the director was also the sole founder of the company, the conclusion of such an agreement raised questions. As a result, Rostrud issued letter No. 2262-6-1 dated December 28, 2006, in which it indicated that the sole founder cannot be an employee of the organization. The department referred to Article 273 of the Labor Code of the Russian Federation, which states that the features established by the Labor Code for regulating the work of the head of an organization do not apply to the director, who is the sole founder. Therefore, the letter said, there is no need to conclude an employment contract with such a director. A similar point of view was expressed by the Ministry of Health and Social Development in letter dated 08.18.09 No. 22-2-3199.

But this approach soon enough led to the cessation of income to extra-budgetary funds from payments in favor of such managers. Therefore, the Ministry of Health and Social Development, in letter No. 428n dated 06/08/10, stated that in any case an employment contract is concluded with the director, even if he is the only founder. The ministry justified its new approach by the fact that only in this way can the manager be provided with social and labor guarantees.

In 2011, legislators noticed the described problem and tried to solve it by amending the laws on social insurance. They directly indicated that managers who are the only participants (founders) of organizations belong to the category of insured persons (clause 1, part 1 and part 5, article 2, article 13 of the Federal Law of December 29, 2006 No. 255-FZ , paragraph 2, paragraph 1, article 7 of the Federal Law of December 15, 2001 No. 167-FZ, paragraph 1 of Article 10 of the Federal Law of November 29, 2010 No. 326-FZ).

True, these amendments were not very successful, since managers were not mentioned as a separate item, but were included in the general list of insured persons as follows: “those working under an employment contract, including heads of organizations who are the only participants (founders).” That is, instead of solving the problem, the amendments actually gave reason to believe that managers - the only founders - have the opportunity to choose: work under an employment contract and receive social protection, or not draw up a contract and not receive pensions and benefits.

Rostrud made the next move again. In letter dated 03/06/13 No. 177-6-1, officials again indicated that an employment contract with the manager - the sole founder - is not concluded. The rationale is this. An employment contract is an agreement between an employer and an employee, that is, a bilateral act. If one of the parties to the employment contract is absent, it cannot be concluded. The only participant in the organization must, by his decision, assume the functions of a manager, without concluding any contract, including an employment contract.

Rights of the General Director

In addition to representing the interests of an LLC without a power of attorney, the sole executive body has the right to:

- Issue powers of attorney to other persons to represent the interests of the Company;

- Issue various orders, including on the appointment of employees to positions, their transfer to other positions and their removal from positions;

- Issue orders to reward employees or fine (impose disciplinary sanctions);

- Carry out all other functions and powers that are not assigned to the powers of the General Meeting of Participants or the sole participant of the Company, the Board of Directors or the collegial body of the LLC.

The procedure for performing the function of the General Director during the Company’s business activities is established by the Company’s Charter, internal documents of the LLC, as well as an agreement between the Company and the sole executive body.

Position of the Ministry of Finance: there are labor relations, but there is no employment contract

And in 2021, the Russian Ministry of Finance became involved in resolving the issue of whether the director, the sole founder, needs an employment contract. In a letter dated 03/15/16 No. 03-11-11/14234 with reference to a fairly old court decision (determined by the Supreme Arbitration Court of the Russian Federation dated 06/05/09 No. 6362/09), financial department specialists indicated that labor relations with the director - the sole founder - still exist . But they are formalized not by an employment contract, but by the decision of a single participant. This means that the manager is an employee of the organization and he needs to pay a salary. Thus, the issue of insurance premiums from payments to the director was resolved in favor of the budget, and at the same time the Ministry of Finance did not come into conflict with Rostrud (also see “The Ministry of Finance announced how to formalize labor relations with a director who is also the sole founder of the organization”).

But this approach, for all its apparent success, does not answer the main question: will a “manager without a contract” be an insured person? After all, the laws mentioned above clearly state that in order to fall into this category, a manager must have an employment contract. In addition, the conclusion of the Ministry of Finance directly contradicts the article of the Labor Code of the Russian Federation, which states that labor relations arise only on the basis of an employment contract. The only exception to this rule is the actual admission of the employee to work with the knowledge or on behalf of the employer (it is clear that this exception does not apply to the situation under consideration).

Thus, we have to admit that the approach outlined by the Ministry of Finance cannot be applied in practice, since it contradicts the Labor Code. In addition, guided by the position of the Ministry of Finance, it is impossible to answer the question of whether it is necessary to charge insurance premiums on salaries that are paid to the director not on the basis of an employment contract. Finally, this approach calls into question the legality of including payments to a “manager without an employment contract” as expenses under the OSNO, under the simplified tax system or under the unified agricultural tax. Indeed, on the basis of Article 255 of the Tax Code of the Russian Federation, labor costs include accruals provided for in the employment contract.

In passing, we note that the definition of the Supreme Arbitration Court of the Russian Federation, to which the authors of the commented letter refer, was devoted to the question of whether the founder-manager has the right to social benefits. And this judicial act was adopted even before the approval of the above-mentioned amendments to the laws on social insurance. That is, the court’s conclusion, which officials refer to, is actually taken out of context. Therefore, it cannot be said with confidence that at present the arbitrators will support the approach proposed by the Ministry of Finance if a dispute arises about the right not to draw up an employment contract with the director - the sole founder.

Election and appointment of the General Director as the sole executive body

The sole executive body of the LLC, also known as the General Director (President or other job titles), is elected by the General Meeting of Participants or the sole participant of the Company for the period specified in the Charter. By the way, the election of the sole executive body may be within the competence of the Board of Directors, which makes the decision on the election of the General Director to the position.

The election of the General Director must be formalized by the Minutes of the General Meeting or the Decision of the sole participant, indicating for what period he was elected.

The decision to elect the General Director of the LLC must be made by a simple majority of votes of participants in the General Meeting. See also: Cheat sheet on the number of votes for making various decisions at the General Meeting.

Exception method: a contract is needed, but it cannot be civil law

So how do you formalize your relationship with a manager who is also the sole founder of the organization? In our opinion, in the current situation of legal uncertainty, it is possible (and necessary) to resolve this issue using the exclusion method.

Let us recall that relations regarding the management of an LLC are regulated by a special Federal Law dated 02/08/98 No. 14-FZ “On Limited Liability Companies” (hereinafter referred to as the LLC Law). By virtue of paragraphs 1 and 4 of Article 40 of this law, the company’s relations with the sole executive body (that is, the director) are in any case formalized by an agreement. This law does not establish any exceptions for the manager - the sole participant of the LLC.

At the same time, from the analysis of the Law on LLC it follows that this agreement can be civil if it is concluded with a professional manager in the manner prescribed by Article 42 of the Law on LLC. Obviously, in this case, the person claiming to be the manager (that is, in our case, the sole founder) will carry out entrepreneurial activities in managing the LLC. This means that he will have to register as an individual entrepreneur (subclause 2, clause 2.1, article 32 of the LLC Law).

So, a civil contract is not suitable in the situation under consideration. We exclude him. And as a result we get the following. First, you need to conclude an agreement with the manager. Secondly, this agreement cannot be civil law. Thus, there is only one option left for formalizing relations with the director of the LLC - concluding an employment contract with him. The legislation does not yet provide for any other option.

Reason for hiring

According to Article 40 of the Federal Law of 02/08/1998 No. 14-FZ “On Limited Liability Companies”, the directors are elected and appointed by the company’s participants. To do this, at a general meeting they must, by a majority vote, decide to elect a leader. The board of directors (supervisory board) can also do this if it is enshrined in the charter.

Directors are chosen from among the founders or invited from outside.

Attention! Disqualified persons may not be hired as directors. Check in advance that the future manager is not listed in the Register of Disqualified Officials. To do this, you can use the service on the Federal Tax Service website.

The decision on appointment to a position is documented in the minutes of the general meeting. This will be the basis for concluding an employment contract. There is no need to write an application to the director when hiring.

If there is only one owner in the LLC, then he can delegate the powers of the manager to himself or hire an employee. In this case, the director will be hired on the basis of the decision of the sole founder of the company.

What to pay the founder-manager: salary or dividends

So, we have established that it is still necessary to conclude an employment contract with the manager - the sole founder. And if an employment relationship is formalized, then the employer must pay the employee wages (Art., Labor Code of the Russian Federation). The condition of remuneration is a mandatory condition of the employment contract (Article of the Labor Code of the Russian Federation). Thus, the absence of wage accruals in the presence of a concluded employment contract is a violation of labor legislation, which is punishable by at least an administrative fine (Part 1 of Article 5.27 of the Code of Administrative Offenses of the Russian Federation).

At the same time, it would be incorrect to say that the reward for a manager’s work may not be wages, but dividends. The fact is that a participant in an LLC has the right to dividends regardless of whether he manages the company or not (clause 1, article 8, clause 2, article 28 of the LLC Law). This means that dividends cannot be a substitute for wages.

How to draw up a decision or protocol on the appointment of a director

In Art. 40 of the Law “On Limited Liability Companies” dated 02/08/1998 No. 14-FZ, establishes the rules that must be followed when choosing a sole executive body, for example, director, general director, president, etc. The election of the sole executive body is carried out exclusively at the general meeting of participants.

But as always, in every case there are exceptions, namely:

- There is only one participant in the society;

- The right to choose the head of the organization rests with the board of directors.

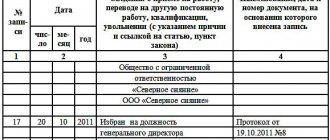

After the meeting is held and decisions are made on the issue raised, everything must be recorded in the minutes. And it is the minutes of the general meeting that are submitted to the Federal Tax Service on the appointment of a director to the position in order to make changes to the Unified State Register of Legal Entities extract.

Important!!! Both a member of the company and a third-party individual can be appointed as a director.

In paragraph 4 of Art. 182.1 of the Civil Code of the Russian Federation clearly states the requirements for the content of the decision on the appointment of a director. The document must contain information such as:

- Place, time and date of document preparation;

- Registration number of the decision (not always);

- Full corporate name of the organization;

- Information about the meeting participants, namely last names, first names and patronymics, passport details and place of registration. If there are more than 15 founders, a separate Appendix is drawn up to the protocol with a complete list of them;

- Information about the appointment of the director, namely the last name, first name, patronymic of the appointed director, passport details, place of registration.

- List of reflected questions;

- Voting data;

- The decision made during voting;

- Signatures of all meeting participants. If there are legal entities among the participants, then in addition to the signature it is also necessary to affix a stamp.

After the decision has been made to appoint a director, an employment contract is concluded with the already appointed director, registration for a new workplace is carried out in accordance with the requirements of the Labor Code of the Russian Federation. The director, like all employees of the organization, must receive a salary, regardless of whether he receives dividends as a member of the company or not.

In order to provide information to the Federal Tax Service about a change in the director of the organization, it is necessary to draw up an application in the established form P14001, which is certified by notaries (in fact, the signature of the new manager is certified, since he will already sign it to the Federal Tax Service). The decision to appoint a director does not need to be certified separately.

Calculation of insurance premiums and reporting: are there any options?

We will separately dwell on the question of whether it is necessary to accrue insurance premiums for payments to the director - the sole founder and to include information about him in the reporting on contributions. Naturally, in the case when the manager is paid a salary on the basis of an employment contract, it is necessary to calculate insurance premiums and provide personalized information. But in practice there are situations when the above question is not so clearly resolved. Let's consider such situations.

The first situation: an employment contract has not been concluded with the director and no payments are made in his favor (except for dividends).

In this case, it is obvious that the obligation to pay insurance premiums does not arise, since there is no taxable base (clause 1 of Article 419 of the Tax Code of the Russian Federation).

As for the presentation of reports, it must be taken into account that, according to the position of the Ministry of Finance of Russia (letter dated June 18, 2018 No. 03-15-05/41578), an organization that during the reporting (settlement) period did not make accruals at all in favor of individuals, all equally obliged to submit zero reports. As officials explained, the policyholder thereby declares the absence of payments and remunerations that are subject to insurance premiums, and, accordingly, the absence of paid contributions (see “The founding director does not receive a salary: is it necessary to indicate this information in the zero DAM?” ).

In addition, officials insist that for a director with whom an employment contract has not been concluded, the SZV-M form must be submitted (letter from the Pension Fund of the Russian Federation dated 03.29.18 No. LCH-08-24/5721 and the Ministry of Labor of Russia dated 03.16.18 No. 17-4/ 10/B-1846; see “SZV-M for directors: the Pension Fund of Russia requires submission of reports even for those founding directors with whom there is no employment contract”). And although in both letters the reasoning used by the departments is not convincing enough, failure to submit reports will most likely lead to a conflict with inspectors. And how the court will look at this situation is almost impossible to predict, since initially the courts proceeded from the position that an employment contract should be concluded with the manager. Thus, in the event of a trial, the possibility cannot be ruled out that the arbitrators will take the side of the inspectors. In addition, the organization may have to pay a fine for the fact that an employment relationship has not been formalized with the director and his salary is not paid.

Therefore, comparing the possible risks, we believe that in the situation under consideration it is safer to submit both a zero calculation for insurance premiums and the SZV-M form in relation to the manager.

Fill out, check and submit the SZV-M for free via the Internet

Second situation: an employment contract has been concluded with the manager, but wages are not accrued to him

All the conclusions made above are also relevant for the situation when an employment contract has been concluded with the manager, but wages are not accrued to him. The difference in this situation will be the even more precarious position of the organization in the event of initiation of legal proceedings. After all, if there is an employment contract, salary calculation is mandatory (Article of the Labor Code of the Russian Federation).

True, in 2021, a ruling by the Supreme Court of the Russian Federation dated 02/17/17 No. 309-KG16-20570 appeared, in which the judges recognized: if there is an employment contract with the director and in the absence of a salary accrued to him, contributions may not be paid (see “Supreme Court: if the organization does not pay the director a salary, she is not obliged to pay insurance premiums").

However, it is possible that inspectors will seek payments in favor of the director. And when they find it, they will try to justify that these payments are in the nature of remuneration for labor. If they succeed, the organization will be assessed additional fees, penalties and fines.

Third situation: the organization does not operate

This situation is a variation of the first or second situation, but with the condition that the organization does not carry out any activities (that is, we are talking about a “sleeping” organization).

Tax officials insist that the Tax Code of the Russian Federation does not relieve payers of insurance premiums from the obligation to submit calculations if they do not conduct financial and economic activities and do not pay remuneration to individuals during a particular settlement (reporting) period. Therefore, a “sleeping” company is obliged to submit the DAM with zero indicators (letter of the Federal Tax Service of Russia dated November 16, 2018 No. BS-4-21 / [email protected] ; see “The LLC does not pay salaries and does not conduct business: is it necessary to submit a zero DAM?” ).

And considering that we are talking about a manager with whom, according to the rules of the Labor Code of the Russian Federation and the Law on LLCs, it is necessary to conclude an employment contract, the chances of the organization defending the right to an “unaccountable” life are extremely small.

Practical conclusions

In conclusion, we present some practical conclusions.

- Current legislation does not provide for any other option for formalizing relations with the director - the sole founder (who is not an individual entrepreneur), other than concluding an employment contract with him. Without an agreement, the activities of such a manager acting on behalf of the organization may be recognized as unlawful upon the claim of one of the company’s counterparties, which could jeopardize the business as a whole. Thus, an employment contract is needed, first of all, to protect the business, that is, the decisions that the manager makes and the documents that he signs.

- Labor relations, by virtue of the direct and repeated instructions of the Labor Code, imply the calculation and payment of wages. Violation of this rule is fraught with at least an administrative fine. Accordingly, if an employment contract has been concluded with the manager, the sole founder, then such employee must be accrued and paid wages in the amount specified in this contract. The law does not allow replacing wages with dividends.

- Concluding an employment contract with the manager, the sole founder, is a step that resolves numerous conflicts with regulatory authorities. Thus, such an agreement removes uncertainty regarding the calculation of insurance premiums (they must be calculated) and the reporting of contributions (they must be provided). In addition, the employment contract allows you to safely pay various social benefits to the manager. Finally, an employment contract makes it possible to include wages in expenses when determining the tax base for income tax, the unified “simplified” tax or the Unified Agricultural Tax, and in the event of claims being made, to successfully defend this right in court.