Cancel the round seal

The abolition of the seal for legal entities has caused a lot of unrest and misunderstanding in the business industry. First of all, managers and representatives of the economic sector of the organization asked the question: “Has the use of seals been canceled for all procedures, or are there documents that are not valid without certification?” The answers were provided by the law on the abolition of seals No. 82-FZ of 04/06/2015. It describes in detail how an organization should operate from the moment the law is adopted, whether it is necessary to put a stamp on the contract, as well as on tax, accounting and primary reporting documents. Also, the law on the abolition of seals explains the procedure for placing such marks on powers of attorney, allowing the interests of a legal entity to be represented in court.

Should a society have a seal?

The need for the company to use such requisites is prescribed in its charter. Organizations such as LLCs and JSCs are not required to have a round seal based on Federal Law No. 82-FZ of 04/06/2015. Also, from April 7, 2015, enterprises have an obligation to indicate in the charter the fact of having a stamp. If it is absent, it is considered that the legal entity is not obliged to certify documents in this way. Therefore, after the law has come into force, companies that have a mark in their charter indicating the presence of a round seal do not need to make any amendments. As for organizations that were created before April 7, 2015 and do not have the corresponding mark in their documentation, they are recommended to supplement the charter with the required information. The need for this addition is justified by the possible need to put a mark on the papers required by law. As for companies formed after April 7, 2015, they have the right to have a stamp, but this is not obligatory for them.

The concept and purpose of printing for documents

From April 7, 2015, business companies are not required to have a round seal. In accordance with paragraph 5 of Art. 2 of the Federal Law of 02/08/1998 N 14-FZ “On Limited Liability Companies” (hereinafter referred to as the LLC Law), the presence of a seal for an LLC is a right, not an obligation. Similar rules are contained in the Federal Law of December 26, 1995 N 208-FZ “On Joint-Stock Companies” (hereinafter referred to as the JSC Law).

At the same time, seals are currently actively used in modern business activities; without them, it is perhaps difficult to imagine the document flow of a legal entity or individual entrepreneur. Moreover, in addition to the main seal, other seals are used in business practice, which differ in their purpose; they are conventionally called “additional” or “auxiliary”. These also include stamps “for documents”. How justified is its use? What documents can be certified with this seal? Let's try to answer these questions.

In general, in civil legislation the concept of “seal for documents” is absent, and the legislator does not define the term “seal” itself.

We find the legal definition of a seal in clause 2.1 of GOST R 51511-2001, approved by Decree of the State Standard of Russia dated December 25, 2001 N 573-st (hereinafter referred to as GOST R 51511-2001), according to which a seal is understood as a device containing a printing cliche, for making impressions on paper.

According to clause 5.24 of GOST R 7.0.97-2016 “National Standard of the Russian Federation. System of standards on information, librarianship and publishing. Organizational and administrative documentation. Requirements for the preparation of documents" (approved by Order of Rosstandart dated December 8, 2016 N 2004-st) the seal certifies the authenticity of an official’s signature on documents certifying the rights of persons recording facts related to financial assets, as well as on other documents that require certification of a signature with a seal in accordance with the legislation of the Russian Federation.

Thus, the concept and legal status of any seal, including the seal “for documents”, is defined: it is a tool that allows you to certify the signature of an authorized person on a document.

This conclusion is enshrined in clause 71 of GOST R 7.0.8-2013, approved by Order of Rosstandart dated October 17, 2013 N 1185-st, according to which a seal is a device used to certify the authenticity of an official’s signature by applying his imprint to a document.

On the one hand, having such a seal is very convenient for an accountant, HR officer, or lawyer of an organization, since it is always at hand and can be used to certify a signature on a document when there is no access to the main seal (for example, the manager took it with him to negotiations in another city) .

On the other hand, the question arises whether such an assurance is legitimate and whether it will cause the organization’s counterparty to doubt the integrity of its actions. Firstly, doubts arise from the analysis of the norms of the Laws on LLCs and JSCs, from the literal interpretation of which it follows that an organization has the right to have only one seal (clause 5 of Article 2 of the Law on LLCs, clause 7 of Article 2 of the Law on JSCs). At the same time, the seal “for documents” is quite widely used in the field of entrepreneurship. This is undoubtedly facilitated by the well-established judicial practice in relation to this category of seals (Resolutions of the Twelfth Arbitration Court of Appeal dated June 14, 2018 N 12AP-3901/2018 in case No. A12-33980/2017, the Fifteenth Arbitration Court of Appeal dated December 11, 2017 N 15AP- 18702/2017 in case No. A53-14906/2017).

Thus, the appellant’s argument that the “document stamp” with which the certificates of completed work were certified was unreasonably recognized by the court of first instance as the “seal of the organization”, was also rejected by the arbitration court of appeal, since, as the court pointed out, “the presence of a seal imprint ( stamp with the defendant’s data) on the act of completed work gives rise to a legal fact, the presence of which gives rise to certain rights and obligations for a person, since a seal and stamp are a means of individualizing a legal entity and are at the disposal of the company itself, only authorized persons have access to it. Accordingly, the seal certifies the authenticity of the signature, as well as the fact that the corresponding document comes from an individually determined organization" (Resolution of the Seventh Arbitration Court of Appeal dated June 22, 2016 in case No. A45-22782/2015 (Resolution of the Arbitration Court of the West Siberian District dated 11.10 .2016 N F04-4272/2016 in case N A45-22782/2015 this Resolution was left unchanged)).

This Resolution contains very important conclusions that make it possible to determine the status of a seal “for documents”: this kind of seal (or it can also be called a “stamp”, thereby distinguishing it from the main seal) can also serve as evidence of the authenticity of the signature of officials on documents, since , being under the jurisdiction of a specific legal entity, with limited access, is also a means of its individualization.

Speaking about the appearance of the seal “for documents”, it should be noted that the legislator has not established imperative requirements for how it should look. GOST R 51511-2001 introduces standards only for printing with the reproduction of the state emblem of the Russian Federation. And yet, the mandatory requirements for this type of seal can be determined if we are guided by the purpose of any seal as a means of identifying a specific legal entity.

As already written above, the seal certifies the signature of the manager or other authorized person on the document. It is doubtful that all counterparties of a legal entity thoroughly know the signature of its head. In this case, any seal serves as a guarantee that the document comes from this organization. In this regard, the seal “for documents”, like other seals, must contain the following details: the full name of the organization in Russian indicating the organizational and legal form, location, OGRN, INN. The seal “for documents” will necessarily include an additional inscription “for documents”. Moreover, the shape and size of such a seal can be any.

Thus, we can draw the following conclusions regarding the concept and purpose of the seal “for documents”:

- Since 04/07/2015, organizations have the right to have a seal or refuse it. If a legal entity has a seal, then this must be recorded in the charter.

- An organization can have only one main seal. It is more correct to call all other seals stamps, since, despite the similarity of concepts, differences between them certainly exist. Controversial conclusion - see above.

- The seal “for documents” also belongs to the category of stamps. The external difference between this seal and the main one is the additional inscription “for documents”; the stamp may also contain all other attributes, for example, details of the organization. Since the legislator has abolished the requirements for the shape of the main seal (now it does not have to be round), it follows that the shape of these two seals can be any.

The legal status of the main seal and the seal “for documents” is also similar: both are used to certify the signature of a manager or other authorized person on documents. The choice of seal depends on the status of the document, since the law may require its certification only with the main seal. This raises the question of what other types of documents can be certified with this seal so that the court does not subsequently recognize them as inadequate evidence. To answer, one should proceed from the opposite, that is, determine the list of documents on which the main seal is required.

When is printing necessary and when is it not?

The company is obliged to affix a seal in the following cases:

- if there is a need to leave the pledge with the pledgor under the protection of the lock and seal of the pledgee,

- when an educational organization certifies education documents,

— if documents are submitted for registration under a lease agreement for a structure or building for a period of more than a year, then they must be certified with a seal, but only on the condition that this method is prescribed in the charter,

— an information message is submitted to the customs authority in a package with other documents on the payment of excise taxes on goods marked by the Customs Union and imported into the territory of Russia from the territory of the union state.

The abolition of the seal for legal entities forced corresponding amendments to be made to a number of laws. Some of the by-laws still presuppose the need for its presence. Cases where by-laws require this mark to be placed on documents should be perceived by a legal entity as optional. But government agencies, banks and other structures may still require stamping on documents.

More about seals in office work

The manager must issue a separate order in order to practically approve a list of documents that require printing. A separate order or instruction requires a list of officials who have the right to sign documents.

For legal entities, printing also becomes mandatory. Acts on industrial accidents, magazines and books, powers of attorney - this is just a small list of papers that require the use of this material. The use of seals in office work simplifies doing business. Moreover, the lack of printing makes it difficult to solve many problems.

Some legal entities are required by law to have this tool, regardless of whether they plan to use it in practice. For public organizations and cooperatives, for example, this is not a mandatory requirement. In work books, stamps are placed only in three situations:

- When the document is issued for the first time.

- If an employee's personal information changes.

- If there is a dismissal.

The only serious problem at present is the lack of rules for canceling erroneously placed seals.

It is permitted to use trademarks and trade names on seals as long as this does not violate the rights of others. Thanks to this, management has an additional tool for individualization. This helps you stand out from your competitors. The right to use a trademark arises immediately after its registration is completed. You can make a seal for an organization at any company that provides the relevant services. It is acceptable to use additional protection against counterfeiting. To do this, drawings are applied that remain visible or invisible.

Each leader decides for himself whether to use the seal or refuse it. Some regulations do not provide for the mandatory use of a seal at all.

Top

Write your question in the form below

Registration of work books

In accordance with the rules for maintaining a work record book, upon dismissal of an employee, all entries that were made during his work must be certified by a seal. The abolition of the mandatory seal introduced adjustments to this procedure. Now the employee’s information is certified with a stamp belonging to the personnel department. Rostrud believes that replacing a round seal with another is not a violation of the Labor Code and does not infringe on the rights of the employee, since the latter receives confirmation of the fact of working in this organization. It is important to understand that only the mark that contains information about the name and location of the employer is confirmatory.

To bet or not to bet? That is the question!

When preparing documents confirming the involvement of foreign employees, the employer certifies them only if this is provided for in the charter. As for the staffing table, the abolition of the mandatory seal of business companies entailed a complete absence of the need to certify this document. The changes also affected the principle of drawing up an employment contract. The abolition of the organization's seal now implies that there is no need to certify the employment contract with a stamp.

Is a stamp required on the contract?

Even before the seal ceased to be mandatory, judges came to the conclusion that the legislation does not contain the mandatory presence of a seal of the parties to the agreement (Resolution of the Federal Antimonopoly Service of the Moscow District dated March 22, 2012 No. A40-62363/11-71-291).

It turns out that affixing a seal to contracts was not mandatory before (unless, of course, the contract itself required it).

Without a seal, it is also possible to conclude employment contracts, since the article of the Labor Code of the Russian Federation does not provide for a seal as a mandatory requisite. Thus, for the purpose of concluding contracts, the abolition of the seal, in principle, did not change anything.

Draw up contracts for free in Kontur.Elbe using ready-made templates

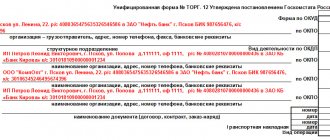

Printing on primary documents

The Tax Code and the Accounting Law do not contain any information about the need to affix a stamp to the organization’s primary documents, even those that indicate income tax expenses. But there are cases when the mandatory certification is established by the procedure for filling out a specific form, or the form itself, or the format for submitting the primary document, developed by the taxpayer. In connection with this subtlety, taxpayers are recommended to warn their counterparties about the need to certify the document, if this is provided for in the form of this document. Also, the abolition of seals for legal entities forces taxpayers to make sure in advance that the counterparty also needs a seal.

Is a stamp required on the order?

Thus, from the point of view of the rules for preparing such documentation, a stamp on the order is not required. But in most organizations they still put an imprint. Why?

The first reason is that it adds weight to the document. Although in this case the need is rather purely psychological.

The second reason is to verify the authenticity of the official’s signature. This is not particularly necessary, but in the event of a conflict situation (violation of labor or legal standards in an order, violation of the order itself by subordinates), the presence of a seal on the internal orders of the organization is an additional argument in the dispute.

Submitting reports to the Federal Tax Service

It is the responsibility of each taxpayer to timely submit a declaration in accordance with the form approved by the Federal Tax Service of Russia and agreed upon with the Ministry of Finance of Russia. If an organization submits reports in paper format, then affixing a stamp is mandatory. This rule is regulated by the instructions of the tax department, which include standards for filling out declarations. The abolition of stamps misled many legal entities, which led to the frequent absence of important details on the submitted declaration and, as a consequence, to its rejection.

In connection with the existence of a rule stating that cases requiring the affixing of a seal must be prescribed in federal laws and the provision of this requirement in by-laws, a paradoxical contradiction arises. Legal force is on the side of the law, that is, conflicting by-laws are not taken into account. However, in order not to risk thinking that the abolition of the seal of business entities also applies to this situation, it is recommended to certify the document with a wet seal until clarifications appear from the competent authorities or changes are made to the orders relevant to this situation. At the same time, as a recommendation, a wish is put forward to include information about the presence of a stamp in the organization’s charter.

Mandatory stamp on the service provision certificate

To answer the question, the following documents and regulations were used:

- Tax Code of the Russian Federation.

- Resolution of the Federal Antimonopoly Service of the Ural District dated March 2, 2011 No. F09-765/11-S3 in case No. A76-10969/2010-37-370.

- Resolution of the Federal Antimonopoly Service of the Moscow District dated July 15, 2011 No. KA-A40/7114-11 in case No. A40-122922-10-76-711.

- Resolution of the Federal Antimonopoly Service of the North-Western District dated 08/03/2009 in case No. A56-51039/2008.

- Resolution of the Federal Antimonopoly Service of the Volga District dated 04/06/2009 in case No. A65-19581/2008.

- Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated January 20, 2009 No. 2236/07 in case No. A40-11992/06-143-75.

- Letter of the Ministry of Finance of the Russian Federation dated November 12, 2007 No. 03-03-06/1/800.

- Letter of the Ministry of Finance of Russia dated July 31, 2012 No. 03-03-06/2/85.

Based on the information provided by you, we consider it necessary to report the following.

Service agreements concluded to meet the needs of the parties in the field of information, advertising, medicine, consulting, law, audit, etc. are widespread nowadays. In this regard, it is important to know what documents are used to document service contracts so that the parties do not have problems, both with the tax authorities and among themselves, when executing the contract. After all, a service does not have a material expression, and therefore the fact and scope of service provision can be confirmed only with documents, primarily an act on services rendered.

As practice shows, tax inspectors, when carrying out tax audits, pay close attention to the execution of acts on the provision of services. There is no unified form of such an act, and the organization must develop it independently. An act on the provision of services, drawn up with violations and not meeting the requirements of the law, may lead to the fact that, based on the results of tax audits, the expenses will be recognized as unlawful, and the deduction of “input” VAT will be denied. This situation, unfortunately, has a high probability.

Despite the fact that a standard form of such an act, its unified form, does not exist, tax authorities are very demanding about its form and content. Thus, although the taxpayer’s expenses and their content can be confirmed by any documents, including contracts, acts, invoices and payment documents, from the position of the tax authorities, expenses can only be reliably confirmed by documents drawn up in accordance with the requirements established by current legislation. This position has been confirmed in judicial practice, in particular in the Resolution of the Federal Antimonopoly Service of the Ural District dated 03/02/2011 No. F09-765/11-S3 in case No. A76-10969/2010-37-370.

What are these requirements and what must the certificate of services provided necessarily contain? To understand this issue, let us dwell on the main provisions for which the tax authorities put forward requirements.

First of all, tax authorities, in order to establish a connection between the expenses incurred and the commercial activities of the organization, require in the acts a detailed description of the services provided with their decoding. In the absence of detail in the acts, they can exclude expenses from the composition of expenses that reduce the taxable base for profit, as not confirmed. At the same time, both the Ministry of Finance of the Russian Federation and the arbitration courts stand in this matter to protect the interests of the taxpayer, based on the fact that neither tax nor other authorities have the right to establish mandatory forms of tax accounting documents for taxpayers (Letter of the Ministry of Finance of the Russian Federation dated November 12, 2007 No. 03-03-06/1/800, Resolution of the Federal Antimonopoly Service of the Moscow District dated July 15, 2011 No. KA-A40/7114-11 in case No. A40-122922-10-76-711). Due to the existing discrepancies in this matter, we recommend that the author of the letter describe in detail in the act the content and scope of the services provided.

As for the issue of precisely drawing up an act of services rendered, then, because the act is a primary document, then the general requirements for the preparation of primary documents apply to it. The act must indicate the date the document was drawn up, the name of the organization on whose behalf the document was drawn up, the content of the services provided, the cost of the services, the names of the positions of the persons responsible for the business transaction and the personal signatures of these persons. Moreover, special attention must be paid to the signatures on the act of provision of services - the act must contain their transcripts, as well as the names of the positions of the persons who signed this act. The need for the above elements to be present in acts was also indicated in its Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated January 20, 2009 No. 2236/07 in case No. A40-11992/06-143-75.

But the organization’s seal is not mentioned in the list of mandatory details of the primary document. This position is confirmed, for example, in the Letter of the Ministry of Finance of Russia dated July 31, 2012 No. 03-03-06/2/85. However, we believe that putting a stamp on the certificate of services rendered would be useful. In addition, this may turn out to be an additional argument if the customer refuses to pay, citing the fact that the document contains the signature of an unauthorized person.

Judicial practice in this matter also justifies the absence of the need to affix a seal on acts of services rendered. For example, the Federal Antimonopoly Service of the Ural District, in its Resolution No. Ф09-9195/07-С2 dated January 29, 2008, noted that the absence of a seal of the counterparty organization on the acceptance certificate for services provided to the taxpayer does not deprive the latter of the right to take into account the costs of their payment when calculating tax for profit, since the presence of the affixed seal of the person from whom such a document comes is not provided as a mandatory requirement for the execution of the act. It is worth noting that many judicial acts indicate a judicial practice that allows for the absence of the act of services rendered as such, because civil legislation does not establish the obligation of the parties to formalize the relationship for accepting the result of services by a bilateral act (Resolution of the Federal Antimonopoly Service of the North-Western District dated 08/03/2009 in case No. A56-51039/2008, Resolution of the FAS Volga District dated 04/06/2009 in case No. A65-19581/2008 ).

And yet, if the organization considers it necessary to affix a seal on the certificates of services rendered, we recommend that in the service agreement itself it is mandatory to indicate that the services provided are drawn up in an acceptance certificate, signed and certified by the seals of both parties. This will help in the future to avoid possible disputes regarding the execution of the act and refusal of one of the parties to affix a seal on it. The existing law enforcement and judicial practice on this issue still does not provide a clear unambiguous interpretation of the “for” or “against” of the seal, while the tax authorities will most likely not miss the opportunity to refuse to attribute expenses to expenses for acts of services rendered that do not have side print.

Summary.

Service agreements are one of the most common types of agreements in the business sector. Based on their accounting, the tax authorities have developed a very definite position, which is that an act on the provision of services, drawn up with violations, does not meet the requirements of the law and does not have the necessary details, will not be accepted by the tax authorities, and the expenses will be recognized as unlawful, and in acceptance to VAT deduction will be denied.

At the same time, today (and this position is actively supported by the courts) civil legislation does not establish the obligation of the parties to formalize the relationship for accepting the result of services in a bilateral act, and there are no unified requirements for drawing up such an act. Since the act of services is a primary document, general content requirements apply to it: the date the document was drawn up, the name of the organization on whose behalf the document was drawn up, the content of the services provided, the cost of services, the names of the positions of the persons responsible for the business transaction and the personal signatures of those persons As you can see, there is no requirement to have a seal on certificates of services rendered. This position is supported by the Ministry of Finance of the Russian Federation, the Federal Tax Service and, in many respects, the courts. However, as the norms of civil law state, the parties, when concluding contracts and, accordingly, accompanying documents, are free to express their will and can include in their text any provisions that do not contradict the law. This includes the requirement to affix seals of the parties to certificates of services rendered. In this regard, we recommend that the author of the question, in order to avoid claims from the tax authorities and dishonest behavior of the counterparty - the contractor, affix stamps on the certificates of services rendered.

Would you like to receive legal advice on your matter? Call now!

Reporting for the Pension Fund of Russia

According to the law on insurance contributions, certification of reports submitted to the Pension Fund of the Russian Federation is not required. This provision also applies to filling out forms such as RSV-1 Pension Fund. But, despite this, in the form itself there is a field that requires a stamp. In this regard, the lack of certification on the RSV-1 Pension Fund leads to a refusal by the receiving authority. Also, making corrections during the process of filling out the calculation requires mandatory certification of the corrections with a seal.

How to submit reports to the Social Insurance Fund and not get rejected

If you study the procedure for filling out reports for submission to the social insurance fund in Form 4-FSS, you will understand that there is a need to confirm the correctness of the data with a seal. In the same way as in the case of data that have undergone changes in the RSV-1 form of the Pension Fund of the Russian Federation, mandatory certification requires the corrected information in the document containing calculations for contributions sent to the social insurance fund. As for the documents requested by the Federal Tax Service, according to the form describing the requirements for the provision of documentation, the organization must submit copies of those papers that are required by the inspection, certified by the signature of the head and the corresponding seal, unless otherwise provided by the legislation of the Russian Federation.

The abolition of round seals - what has changed in the work of a lawyer, personnel officer and accountant.

1. To the lawyer: PJSC and LLC will decide independently whether to have a seal

1.1. You can find out whether a company has a seal from its charter.

1.2. Whether there will be a seal on the contract still depends on the decision of the parties

1.3. Is it possible not to put a stamp on the power of attorney?

1.4. In what cases is it possible not to put a stamp, and in what cases is it obligatory?

2. For the HR officer: should I put a stamp when preparing documents?

2.1. The accident report may not contain the employer's seal.

2.2. How to certify entries in work books if there is no seal?

2.3. You can conclude an employment contract without a stamp

2.4. It is up to the employer to decide whether to put the organization’s seal on the certificate of incapacity for work.

2.5. Documents on attracting foreign workers are certified by a seal, if any.

2.6. To approve the staffing table, no stamp is needed

3. To the accountant: will the absence of a seal affect the work?

3.1. For organizations that have a seal, information about which is in the charter

3.1.1. What will happen to the costs if the counterparty does not have a seal?

3.2. For organizations that have a seal, information about which is not in the charter, as well as for newly created companies

3.2.1. What if the inspectorate does not accept reports without a seal?

3.2.2. What to do with reporting insurance premiums?

3.2.3. Is it necessary to certify with a seal copies of documents requested by the inspectorate during the inspection?

3.2.4. Is it necessary to put a stamp on the power of attorney of a representative of the organization?

3.2.5. Should an organization using CCP use a seal?

3.2.6. The obligation to affix a stamp when paying excise tax established in the Tax Code of the Russian Federation remains unchanged.

1. To the lawyer: PJSC and LLC will decide independently whether to have a seal

1.1. You can find out whether a company has a seal from its charter.

From April 7, 2015, LLCs and PJSCs are not required to have a round seal (Federal Law dated April 6, 2015 N 82-FZ, hereinafter referred to as the Law). Corresponding changes have been made, including to the Law on LLCs and the Law on JSCs.

From the same date, information about the presence of a seal must be contained in the company's charter. The absence of such information indicates that the legal entity does not have a seal. At the same time, the obligation to destroy the seal if these changes are not made to the charter is not established.

If a seal is required by federal law, a seal impression, information about the presence of which is not in the charter, cannot be affixed to fulfill this requirement. However, there is no prohibition on the use of such a seal or liability for it.

Summary

Companies whose charter already contains information about the presence of a seal do not need to do anything. We recommend that other organizations include relevant information in their charter, since often the need to stamp documents is provided for by law or in an agreement between the parties. As for companies that are created from April 7, 2015, they have the right, but are not required, to have a seal.

1.2. Whether there will be a seal on the contract still depends on the decision of the parties

The sealing of contracts, both previously and now, is considered an additional requirement for their form.

Therefore, a seal on a contract is needed only if there is a corresponding indication in the law, other legal act or contract. This is confirmed by judicial practice. At the same time, a company’s refusal to use a seal may lead to difficulties in relations with counterparties for whom such execution of a transaction is decisive.

No less important is the question of whether it is necessary to put a stamp on acts confirming the execution of the contract by the parties (for example, on an act on the provision of services or on the completion of work), as well as on a receipt confirming the transfer of funds under a loan agreement. If the parties already have a seal and this is reflected in the charter, they can continue to use it when drawing up the listed documents.

Summary

You may not put a stamp on the contract unless the counterparty objects and the law does not provide otherwise. Since the use of a seal when concluding a contract is an established practice for many companies, we recommend that you do not refuse to use the seal at least for the first time after the innovations come into force.

The online service “Contract Designer” will help you draw up an agreement taking into account the described innovations. A warning has already been added to the questionnaires (section “Final provisions”) and templates (section “Addresses and details of the parties”) for contracts for supply, contract, paid services, rental of non-residential premises, loans, as well as purchase and sale of vehicles, according to which the bonding the seal of the contract is not necessary, unless it is provided for by agreement of the parties, law or other regulatory legal acts. In addition, relevant judicial practice is provided.

1.3. Is it possible not to put a stamp on the power of attorney?

As of September 1, 2013, a seal ceased to be a necessary requisite of a legal entity’s power of attorney, as provided for by the Civil Code of the Russian Federation. A power of attorney on behalf of a legal entity is issued signed by its director (clause 4 of article 185.1 of the Civil Code of the Russian Federation). Previously, the obligation to put the organization’s seal on a power of attorney issued on behalf of a legal entity was established in clause 5 of Art. 185 of the Civil Code of the Russian Federation. The requirement for a seal remained for some types of powers of attorney, for example, for powers of attorney of procedural representatives.

With the adoption of the Law, even procedural powers of attorney in most cases can be issued without a seal, if the organization does not have one.

At the same time, in paragraph 6 of Art. 57 of the Code of Administrative Proceedings of the Russian Federation establishes that a power of attorney on behalf of an organization must be sealed with the seal of that organization. A legal entity that decides not to use a seal will not be able to issue such a power of attorney.

Summary

The absence of a seal of an organization will not prevent it from issuing a power of attorney to carry out a transaction or to represent it in an arbitration court. However, for representation in some cases heard in courts of general jurisdiction (for example, in cases of challenging regulatory and non-regulatory acts), a seal will be required.

We recommend that you do not abandon the seal, so as not to complicate the involvement of a representative in such processes.

1.4. In what cases is it possible not to put a stamp, and in what cases is it obligatory?

Before the Law came into force, the requirement for a seal on documents was contained in a number of federal laws, as well as in many by-laws. According to the changes, only the requirement for a seal imprint established in federal law is mandatory. In this regard, two main questions arise for societies: which laws retain the obligation to affix a seal and what to do with similar provisions of by-laws?

In a number of laws, amendments have been made to the provisions on the need to affix a seal, according to which a seal is affixed only if it is available. For example, now, when submitting a package of documents for registration of a lease agreement for buildings or structures concluded for a period of at least a year, only those business companies whose charter contains an indication of the presence of a seal must certify copies of the constituent documents with a seal. For other companies, certification of the above-mentioned documents with a seal is not necessary.

At the same time, a seal is still needed, for example, in order to leave the subject of pledge with the pledgor under lock and key and the seal of the pledgee, as well as for certification of education documents by educational organizations.

In addition, until May 18, 2015, the obligation of organizations participating in customs legal relations to affix a seal in cases specified by the Law on Customs Regulation remains.

The situation is more complicated with by-laws, which still require legal entities to have a seal. For example, to open a current account, a legal entity must provide the relevant bank with a card with sample signatures and a seal.

Since the Law does not indicate that the obligation to use a seal can be enshrined in by-laws, formally such instructions are not mandatory from April 7, 2015.

Summary

If the requirement for a seal on documents is established by by-law, it should be perceived as optional. However, you need to be prepared for the fact that government agencies, banks and other persons may continue to require a seal on documents.

Organizations that participate in customs legal relations and whose charter does not contain information about the presence of a seal must include the relevant information in the charter. Otherwise, from April 7 to May 17, 2015, they will not be able, in particular, to issue a power of attorney on their behalf for representation when appealing actions and decisions of the customs authority or its official.

2. For the HR officer: should I put a stamp when preparing documents?

2.1. The accident report may not contain the employer's seal.

When drawing up a report on an industrial accident, it is now necessary to affix the organization’s seal only if it is available (Part 5 of Article 230 of the Labor Code of the Russian Federation).

Previously, in all cases it was required to certify this act with a seal. In this case, the individual employer who did not have it had to certify his signature in the prescribed manner.

Summary

The procedure for drawing up a report on an industrial accident has been simplified for both individual employers and organizational employers. Now business companies that do not have a seal are not required to put one on this document.

2.2. How to certify entries in work books if there is no seal?

In connection with the abolition of the mandatory seals, an important question arises about how to draw up work books. According to the rules for their maintenance, when an employee is dismissed, the entries made in the work book during his work are certified by the employer’s seal.

To certify information about the employee on the first page of the work book or changes made to this data (for example, last names), you can use the seal of the personnel service.

Previously, such an alternative was provided for certification of entries made in the employee’s work book upon employment and during the period of his work in the organization. Currently, this possibility is not legally established. At the same time, the explanations of Rostrud allow us to conclude that certification of entries in the work book with an employer’s seal other than a round one does not entail a violation of the employee’s rights, since it confirms the fact of his work for this employer. The seal must contain information about the name of the employer (legal entity) and its location.

Summary

Since the obligation to use a seal is established only by federal legislation, and the requirements for certification of information in work books with a seal are enshrined at the by-law level, compliance with such requirements is not mandatory.

However, in order to avoid risks, we recommend that employers (HR officers) continue to certify the information in employees’ work books with a seal. If there is no round seal, the organization can use another seal containing the necessary data.

2.3. You can conclude an employment contract without a stamp

As a general rule, an employment contract is concluded in writing and signed by the parties. In practice, it is also customary to put the organization’s seal on employment contracts. Meanwhile, the legislation does not provide for the requirement to certify this act with a seal.

Summary

The organization’s lack of a seal, and therefore the inability to put it on the employment contract, will not affect its validity.

2.4. It is up to the employer to decide whether to put the organization’s seal on the certificate of incapacity for work.

The form of the certificate of incapacity for work has a separate field for the employer's seal. However, there are no special rules regarding the form of such a seal or the information it must contain.

Individual employers put a stamp if available (see Procedure for issuing certificates of incapacity for work).

Similar rules will likely apply to business companies in connection with the abolition of the rules on the need to have a round seal. This seems justified, since in this case the federal law does not establish the obligation to put the employer’s stamp on the sick leave.

Summary

Until the document forms and the procedure for filling them out are brought into compliance with the changed legislation, the decision on whether to put a stamp on such documents remains at the discretion of the employer. From a legal point of view, the requirements of by-laws regarding the presence of seals on documents can be considered optional. If the employer is ready to defend his position in court, he may not use the seal in such a case.

2.5. Documents on attracting foreign workers are certified by a seal, if any.

The requirement to certify with a seal the documents necessary to obtain permission to attract and use foreign workers, at the by-law level, contained the clause “if any” even before the abolition of the mandatory seals.

Summary

Now PJSC and LLC may not certify such documents with a seal, regardless of whether the seal is used in the conduct of the company’s activities.

2.6. To approve the staffing table, no stamp is needed

The absence of a seal will not prevent the organization from approving the staffing table. The uniform form of this document does not provide space for printing.

Summary

The staffing table still does not need to be certified with the company’s seal.

3. To the accountant: will the absence of a seal affect the work?

From April 7, 2015, companies are no longer required to have a seal. For organizations whose charter contains information about a seal, it is advisable to keep it, since there is a high probability that an accountant will be faced with the need to certify documents with a seal (for more details on such cases, see below). Moreover, even its use does not guarantee that the organization’s accountant will not have difficulties, since the counterparty may refuse to print.

In addition, there are organizations that have a seal, but there is no information about it in the charter. They, like newly created companies, should pay attention to the possible consequences

3.1. For organizations that have a seal, information about which is in the charter

3.1.1. What will happen to the costs if the counterparty does not have a seal?

Neither the Tax Code of the Russian Federation nor the Accounting Law stipulates that the organization’s seal must be affixed to primary accounting documents confirming, in particular, expenses for profit tax purposes. However, the requirement to certify a primary document with a seal may follow, for example, from the procedure for filling out the form of such a document, either the unified form itself, or the form of the primary document developed by the taxpayer.

Summary

If the counterparty does not certify the source documents with a seal in cases where this is necessary due to the form used, then the tax authority will likely assess additional taxes more often, believing that the company did not exercise due diligence or received an unjustified tax benefit. If the primary documents contain certain shortcomings (for example, the lack of decoding of a signature or the document being signed by an unidentified person), without the organization’s seal it may be more difficult to defend its position.

In this regard, in order to avoid risks, it can be recommended that taxpayers ask counterparties to put a stamp on documents, if such certification is provided in accordance with the forms. Otherwise, you should make sure that the forms approved by the counterparty do not necessarily require a seal. To do this, we recommend sending the counterparty a corresponding request. Even if he does not respond, such a request may, among other things, demonstrate due diligence.

3.2. For organizations that have a seal, information about which is not in the charter, as well as for newly created companies

In addition to difficulties in relations with counterparties who have refused the seal, the organization's accountant may face a number of additional difficulties if the company decides not to use the seal.

3.2.1. What if the inspectorate does not accept reports without a seal?

The taxpayer is obliged to submit a declaration to the inspectorate in a form approved by the Federal Tax Service of Russia in agreement with the Ministry of Finance of Russia. In the case when an organization submits reports on paper, it is necessary to affix a stamp. This rule is contained in the instructions approved by the tax department for filling out declaration forms (for example, reporting on income tax or corporate property tax). It should be borne in mind that now the absence of a stamp on a declaration submitted by an organization is one of the grounds for the inspection to refuse to accept it.

Summary

Since it is now stipulated that mandatory cases of use of the seal must be established in federal laws, and the said requirement is provided for by regulations, a contradiction arises. From a legal point of view, it is resolved in favor of the law, i.e. norms of by-laws that contradict it should not be applied. However, in order to avoid risks, we recommend that organizations, before clarifications from the competent authorities or changes are made to the relevant orders, put a stamp when submitting tax reports on paper to the inspectorate. In this case, it is advisable to include the relevant information about the seal in the charter (see section 1.1).

3.2.2. What to do with reporting insurance premiums?

The Law on Insurance Contributions does not contain a requirement to certify reporting on contributions with a seal. There is no such requirement in the procedure for filling out the RSV-1 Pension Fund form. At the same time, the form itself indicates a stamp field, and its absence in the calculation submitted by the organization to the Pension Fund of the Russian Federation is grounds for refusal to accept documents. In addition, corrections made when filling out the calculation must be certified by a seal.

In order to fill out reports in Form 4-FSS, it is directly indicated that the organization must be stamped. Similar to the PFR form RSV-1, corrections in the calculation of social insurance contributions should also be certified with a seal.

Summary

Since it is now stipulated that cases of mandatory use of the seal must be established by federal laws, and the said requirement is provided for by regulations, a conflict arises. From a legal point of view, it is resolved in favor of the law, i.e. norms of the by-laws that contradict it are not applied. However, in order to avoid risks, we recommend that organizations certify the reporting on insurance premiums with a seal until clarifications from regulatory authorities appear or appropriate changes are made. In this case, it is advisable to include the relevant information about the seal in the charter (see section 1.1).

3.2.3. Is it necessary to certify with a seal copies of documents requested by the inspectorate during the inspection?

According to the form of the request for the submission of documents (information), the organization submits copies of the documents requested by the inspection, which are certified by the signature of the head and seal, unless otherwise provided by the legislation of the Russian Federation.

From the clarifications of the Ministry of Finance of Russia, we can conclude that when submitting copies of the requested documents to the tax authority, the taxpayer should be guided by GOST R 6.30-2003. In accordance with it, documents are certified with the seal of the organization, however, on copies the company can put a seal chosen at its discretion.

Summary

The provisions established by the tax department contain a reservation, which means that now the organization has the right not to put a stamp on documents submitted at the request of the inspectorate if the company has refused to use the seal. However, in order to avoid risks, we recommend that companies, before making changes to the provisions of GOST or until clarifications from the competent authorities appear, certify with a seal copies of documents submitted to the inspection upon request in accordance with Art. Art. 93, 93.1 Tax Code of the Russian Federation. It should be borne in mind that in this case the company can use a seal other than a round one at its discretion.

3.2.4. Is it necessary to put a stamp on the power of attorney of a representative of the organization?

As a general rule, an authorized representative can participate in tax legal relations on behalf of an organization on the basis of a power of attorney issued in accordance with civil law. Currently in Art. 185 of the Civil Code of the Russian Federation there is no requirement for a seal on such a power of attorney.

Summary

In order, for example, to submit reports or accept a document (demand) from the inspection, a representative of the organization may have a power of attorney that is not certified by a seal. It should be noted, however, that the presence of a seal will serve as additional evidence for counterparties and tax authorities that the power of attorney was signed by an authorized person.

For more details, see Federal Law No. 100-FZ dated 05/07/2013.

3.2.5. Should an organization using CCP use a seal?

Several cases of using the seal are established by the Instructions for the use and completion of forms of primary accounting documentation for recording cash settlements with the population when carrying out trade operations using cash registers (for example, when preparing a cashier-operator's journal). Based on the wording of the new provision, these situations do not fall under mandatory cases of using the seal, since they are provided for by by-laws and not by federal law.

Summary

From a legal point of view, the conflict that arises is resolved in favor of the law, i.e. norms of by-laws that contradict it should not be applied. However, in order to avoid risks, we recommend that organizations, before official clarifications appear or changes are made to the mentioned Instructions, put a stamp on the forms of primary accounting documentation when performing transactions using cash registers, if such a stamp is necessary. In this case, it is advisable to include the relevant information about the seal in the charter (see section 1.1).

3.2.6. The obligation to affix a stamp when paying excise tax established in the Tax Code of the Russian Federation remains unchanged.

The Tax Code of the Russian Federation provides for the only case when a document must be certified with a seal. The organization's seal must be affixed to the information message, which is submitted to the customs authority, among other documents, for paying excise duty on marked goods of the Customs Union imported into Russia from the territory of a member state of the said union.

Summary

For excise tax payers, nothing changes in this situation. In this case, the obligation to certify a document with a seal is established directly in the Tax Code of the Russian Federation, which is consistent with the requirements now provided, i.e. You can't do without a seal. In this case, it is advisable to include the relevant information about the seal in the charter (see section 1.1).

https://www.consultant.ru/law/review/fed/nw2015-04-22.html#p37

Is a stamp required on the information message required to pay excise duty?

As for information messages aimed at paying excise duty on labeled goods included in the Customs Union and imported into the territory of the Russian Federation from the territory of the union state, no changes are introduced here (specifically for payers). In this case, the need to certify the information letter with a seal is established by the Tax Code of the Russian Federation. This fact is consistent with the new requirements, which necessitates the mandatory use of a stamp.

What did the abolition of stamps lead to, and for whom is it relevant?

The abolition of the organization's seal applies exclusively to companies with the form of ownership of JSC or LLC. It must be available to non-profit and government organizations. As for legal entities that have the opportunity not to use a seal, if they wish, they can carry out their activities using it. To do this, you just need to state this fact in the charter, and then the abolition of the company’s seal will not raise any questions. Until various departments and ministries give official clarifications, it is not recommended to destroy this document certification instrument. It is best to constantly certify a certain group of documents with a stamp to avoid the possibility of their rejection by the receiving service.