Any business activity involves expenses. You have to spend money on diverse processes and purchases: those needed for the production of products, equipment maintenance, the purchase of raw materials, packaging, and transportation. And also on management processes, not to mention wages. This multifactorial nature of costs indicates the need for their classification and separate accounting.

Let’s understand the concept of “overhead costs”, clarify which costs can be attributed to them and how to recognize them in financial accounting.

How are overhead expenses different from core expenses?

What is overhead

Not all costs in production go directly into the product and can be directly planned and taken into account in its cost. Nevertheless, the funds spent turn out to be absolutely necessary for the manufacture of products, their sale, promotion on the market, as well as the management of the organization itself.

The most accurate definition of overhead would be “everything else.” This type of costs is not highlighted in a separate article in the Tax Code of the Russian Federation; naturally, their structure is not spelled out there either. In accounting, it is also impossible to clearly differentiate them.

NOTE! The law establishes a list of overhead costs only in the construction and medical industries. All other enterprises must determine overhead costs themselves, fixing this in their accounting policies.

overhead costs, accepted in business, implies expenses that cannot be attributed directly to technological production processes, accompanying the production process, but not included in the cost of work and raw materials. Another name for overhead costs is indirect costs . They are indicated when planning and drawing up estimates for both the company as a whole and individual structural divisions.

How to calculate the cost of production taking into account overhead costs ?

Why consider overhead costs?

The most obvious goal is planning future profits, which are affected by all the costs incurred by the entrepreneur. But in terms of overhead costs, this poses certain difficulties. If potential direct costs can be fairly accurately calculated for specific types of products, then it is quite difficult to determine how many indirect costs will result and how they will be distributed when, for example, expanding production or signing a certain contract.

IMPORTANT! To adequately determine the cost of a product, it is necessary to take into account and distribute overhead costs in proportion to direct expenses - calculate production costs .

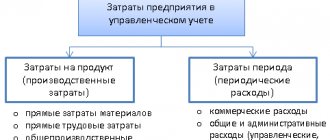

Overhead expenses included in cost

The cost of products manufactured by an enterprise includes 2 types of expenses: direct and overhead.

Direct ones include those that can be unconditionally linked to a specific type of product being created. It is either difficult or impossible to relate overhead costs directly to manufactured products. Based on their connection with the production process, they are divided into:

- for production - ensuring the functioning of production units producing products;

- general economic - not directly related to the creation of products, but necessary to ensure the operation of the enterprise as a whole.

Existing rules (Chart of Accounts, approved by order of the Ministry of Finance of the Russian Federation dated October 31, 2000 No. 94n) do not prevent the possibility of forming accounting costs at 2 levels:

- its incomplete value, including, in addition to direct costs, only those overhead costs that are related to production;

- its full size, which combines, in addition to direct costs, overhead costs generated both in production departments and in general business structures.

What are overhead costs, read in ConsultantPlus. If you do not have access to the K+ system, get a trial online access for free.

What is included in overhead costs

Indirect costs can be roughly divided into 4 main groups:

- Management costs:

- his salary;

- money spent on training, certification and advanced training of management.

- Contents: purchase of computers, office supplies, expenses for office needs, including communication services.

- Expenses associated with the process of organizing production:

- maintenance repairs of structures, buildings, premises, equipment belonging to the organization;

- costs of transport owned by the company;

- payment of rent for warehouse premises and/or office;

- waste of money due to downtime, defects, etc.;

- money that needs to be spent on maintaining fixed assets.

- Personnel costs:

- social tax contributions;

- payments to social security and other funds;

- equipment of household premises, canteens, showers, etc.

- Non-production costs:

- advertising expenses;

- payment for consultations and examinations;

- payment of utility bills, etc.

Direct and indirect costs, basic and overhead

Expenses are divided into basic (directly related to production) and overhead (organization, management and maintenance of production) depending on participation in the production process.

Main expenses: 1. Salaries (main and additional production personnel, including bonuses and types of additional payments according to relevant provisions - vacation, severance pay, etc.). 2. Salary payments (pension insurance part - 28%, social -5.4-6%, medical - 3.6%, employment fund - 1.5%). 3. Materials. 4.Depreciation. 5. Wear. 6. Transport. 7. Other basic expenses (travel expenses, compensation for damage to organizations and individuals).

Overhead expenses (organization of management and maintenance of production): 1. Administrative and economic expenses - maintenance of the management apparatus (basic and additional salaries, all accruals to them). 2. Travel allowances. 3. Rental and maintenance of premises. 4. Depreciation charges for buildings and structures. 5. Current repairs. 6. Transport. 7. Postal and telegraph expenses. 8. Technical safety and labor protection. 9. Recruitment of workers. 10. Advanced training. 11. Other business expenses. On average, overhead costs are up to 20% of basic costs.

There are also direct and indirect costs. The former are related to the volume of production or work, the latter are not. INDIRECT COSTS: 1. Shop costs – costs of organization, management and maintenance at the workshop level. 2. General production (factory) expenses are associated with the maintenance and operation of machinery and equipment, as well as with the organization, management and maintenance of production (shop expenses) and non-productive expenses. 3. General expenses are associated with the maintenance and organization of production and management of the enterprise as a whole. 4. Selling expenses – costs associated with the sale of products. 5. Expenses for preparation and development of production (start-up costs). 6. Rental, renovation of buildings. 7. Personnel training, recruitment of workers. 8. Other expenses - an element of cost, which reflects taxes, fees, contributions to special extra-budgetary funds, payment for communication services, banks, rent, depreciation of intangible assets, and costs not included in other elements.

DIRECT COSTS: 1. Raw materials and supplies. 2. Salaries of main workers and support staff. 2.1 Additional salaries. 2.2 Salary charges (26%, of which 6% are budgetary, 14% are divided into 12% and 2% + medical insurance (2.8%) and social insurance (3.2%). 3. Depreciation. 4. Transport 5. Other.

There is the concept of production and full cost (respectively, without and with commercial and non-production costs). In addition - planned and actual. If an enterprise produces Y units of product per year (or performs a certain amount of work), then Csp = ZplY + MY + Ao t + Rtr t + Pd t + Porg-lik t + Rnakl t Csp = R usl-variable + R usl-post or Ssp = K1U + K2 t with t = Y / Ptr Or Ssp = K Y + K Y / Ptr and then for Ssp ed pr we get Ssp ed = Ssp / Y = L + K / Ptr

According to the degree of expediency of spending, expenses are divided into productive and unproductive (defects, downtime, fines, etc.). Methods for determining cost are methods of grouping and calculating the costs of production and sales of products. There are detail-based (for mass, serial production), detail-operational (for long cycles), custom-made (individual and small-scale production), step-by-step (staged by stages of production, for example, textiles) and normative methods. There is also a weight method (proportional to mass, in petrochemicals) and a cost exclusion method. The most progressive is the normative method, which consists in distributing actual costs in proportion to the normative cost per unit of production. The actual cost is determined by taking into account deviations from current standards and their changes for each costing item.

Design and estimate method. In topographic production, the design and estimate method is used. During the preparation of a technical project, the estimated cost (Cc) is calculated - these are funds received by the enterprise from the customer or from the state, including all basic costs, as well as overhead costs and profit of the enterprise. The cost is calculated according to zonal estimated prices. The entire territory of the country is divided into a number of zones and for each zone the price of a triangulation point, etc. is set. To calculate the total cost, the volume of work must be multiplied by the estimated zonal price. It already contains basic, overhead costs and profit: Rzon = (Rosn, Rnakl and Pr) * Cs = Rzon * Y. The enterprise cannot change the estimated cost - this is the meaning of Rzon.

Overhead distribution options

IMPORTANT! Recommendations for the distribution of overhead costs from ConsultantPlus are available here

Despite the difficulties of planning indirect costs, this is a necessary procedure that can be carried out in several ways:

- The "working wage" method. If the main production employs a large number of workers, especially if manual labor predominates, overhead costs can be calculated in proportion to the wage fund for their labor.

- The “sales volume” method is advisable to use if automated processes predominate in the company. You can distribute income in proportion to machine hours.

- The unit of production method is applicable when direct costs significantly exceed indirect costs. Then we can take as a basis the ratio of direct costs per unit of goods to the total amount of direct costs.

- Direct counting method. Indirect expenses are summed up separately for each expense item.

- Combined methods are applicable in large companies with a complex structure, where several types of products are produced. For example, you can account for manufacturing overhead on the payroll basis, and general business overhead on the basis of unit cost.

EXAMPLE OF CALCULATION. Avtokoleso LLC is engaged in the transportation of goods. The staff wage fund is 8 million rubles per year. The overhead expense ratio in 2021 was 80%, that is, 6 million 400 thousand rubles. The company decided to reduce overhead costs, for which it fired several people. At the same time, the wage fund decreased by 20%, which means that the overhead costs of Avtokoleso LLC for 2021 can be planned in the amount of 5 million 120 thousand rubles.

Is there any provision for rationing of overhead costs ?

Procedure for calculating overhead costs

Planning and accounting of all expenses, including overheads, is carried out in a certain order:

- The total amount of costs for general business activities of the company is calculated.

- The amount of overhead costs that will need to be included in the estimate per unit of each type from the product range is determined.

ATTENTION! It is necessary to take into account the legal limits for overhead costs for specific items and the standards defined by the company's internal regulations.

Legal limits regarding overhead costs

The law determines the composition and limits of overhead costs in the construction and medical industries.

Construction overhead

In this industry, overhead planning is especially important. An estimate is drawn up, which indicates the average costs for the industry, which are included in the cost of construction products or services.

Cost rationing in the construction industry is regulated by the Methodological Guidelines for determining the amount of overhead costs in construction, approved by the Resolution of the State Construction Committee of Russia (separately for regions of the Far North and equivalent regions). These documents define the coefficient that must be applied to determine overhead costs for a particular construction activity, and also clarify the scope of its application. The wage fund for construction workers is taken as the base. The distribution of coefficients is carried out according to the following main types of construction:

- industrial;

- agricultural;

- transport;

- housing;

- energy;

- related to water management;

- in the field of nuclear energy;

- restoration work;

- major repairs;

- other types.

FOR YOUR INFORMATION! Overhead costs according to construction standards must be applied at the stage of drawing up estimates, as well as when paying for work performed.

Medical overhead

The standards and composition of overhead costs in the medical industry are regulated by Order of the Ministry of Health and Medical Industry of Russia No. 60 dated March 14, 1995. According to the provisions of this order, the cost of medical care must include all annual costs of a medical institution:

- salaries of all types of personnel, except medical personnel, with all accruals;

- expenses for the purchase of furniture, stationery, household goods (everything, except medicines and dressings);

- means for repairs.

The basis is the wage fund of medical personnel providing specific medical services, based on a coefficient of 1.5.

IMPORTANT! Typically, overhead costs are significantly higher in medicine than in construction.

Cost of finished products, works, services: criteria for assigning costs to account 109 00

To account for operations to form the cost of finished products, work performed, services provided, account 109 00 is intended (clause 124 of the Instructions, approved by order of the Ministry of Finance of Russia dated December 1, 2010 No. 157n, hereinafter referred to as Instruction No. 157n).

Costs are grouped into the following groups:

- direct costs directly attributable to the cost of finished products, works, services - account 109 60;

- overhead costs for the production of finished products, works, services - account 109 70;

- general business expenses - account 109 80.

1.1. Direct costs are directly included in the cost of manufacturing a unit of finished product, performing work, providing a service (account 109 60). These are expenses directly related to the provision of a specific type of product, work, or service.

Direct costs may include:

- salaries of key personnel;

- accruals for wages of key personnel;

- the cost of inventories completely consumed in the manufacturing process of a unit of finished product, work, or service;

- depreciation of fixed assets used in the process of manufacturing finished products, work, services.

When producing one (single) type of finished product, work, or service, all costs directly related to the production of finished product, performance of work, or services are considered direct costs.

More on the topic: Correcting mistakes of past years using the example of fixed asset accounting (video)

Example. The budgetary institution produces one type of finished product - cottage cheese with a fat content of 9%.

All costs associated with the production of this type of finished product (staff wages, charges for wages, utilities, cost of consumed materials, etc.) are debited to account 109 60.

1.2. Overhead costs are expenses that cannot be directly attributed to specific types of products, works, and services. Overhead costs (account 109 70) are distributed monthly to the cost of finished products sold, work rendered, services (account 109 60) in proportion to the established bases through calculated coefficients.

Overhead costs may include:

- remuneration of general institutional personnel;

- accruals for wages of general institutional (administrative and economic) personnel;

- utility and business expenses (costs of materials and items for current business purposes, office supplies, inventory and payment for services, including costs of current repairs, etc.);

- expenses for business trips and official travel;

- wear and tear of soft equipment in auxiliary departments;

- depreciation (wear and tear) of fixed assets not directly related to the production of products, performance of work, or provision of services.

Example 1. A budgetary institution is engaged in the production of two types of finished products - cottage cheese with a fat content of 9% and cottage cheese with a fat content of 18% (for the production of these types of finished products, one set of inventories is used - milk, sourdough).

All costs associated with the production of these types of finished products (staff wages, accruals for wages, utilities, cost of consumed materials, etc.) are debited to account 109 70.

At the end of the month, account 109 70 indicators are distributed to the cost of each type of product (account 109 60) in proportion to the established base.

Example 2. A budgetary institution is engaged in the production of two types of finished products - bread and sweets (different sets of inventories are used for the production of these types of finished products).

Costs directly related to the production of bread (cost of consumed inventories, bakers' salaries, accruals for bakers' wages) are charged directly to the cost of a specific type of finished product (bread) - to the debit of account 109 60.

Costs directly related to the production of sweets (cost of consumed inventories, confectioners' salaries, accruals for payments for confectioners' wages) are charged directly to the cost of a specific type of finished product (candy) - to the debit of account 109 60.

Costs not associated with the production of a certain type of finished product (utilities, salaries of general institutional personnel, accruals for payments for wages of general institutional personnel) are classified as overhead costs - in the debit of account 109 70. At the end of the month, account indicators 109 70 are distributed to the cost of each type products (account 109 60) in proportion to the installed base.

1.3. General business expenses are expenses for management needs not directly related to the production process (the process of providing services, performing work).

More on the topic: VAT declaration for government agencies

General business expenses are divided into:

- Distributed - subject to distribution to the cost of finished products sold, work rendered, services (account 109 60);

- Not distributed - subject to attribution to the increase in expenses of the current financial year (account 401 20).

Example 1. A budgetary institution is engaged in the production of two types of finished products - cottage cheese with a fat content of 9% and cottage cheese with a fat content of 18%.

Costs not directly related to the production of these types of finished products (salaries of management personnel, accruals for payments for wages of management personnel, utilities for the administrative building, cost of office supplies for management personnel, etc.) are classified as general business expenses - in the debit of the account 109 80.

At the end of the month, account 109 80 indicators are distributed to the cost of each type of product (account 109 60) in proportion to the established base.

The choice of the method for calculating the cost of a unit of production (volume of work, service) and the base for the distribution of overhead costs between the objects of calculation is carried out independently by the institution or founder and is an element of the accounting policy.