Reflection of revenue in accounting

Amounts of revenue that bring profit to the organization, regardless of the type of economic activity, are taken into account in account 90 “Sales”.

Account 90 “Sales” collects all information about the organization’s income and expenses, which is accompanied by the production and sales process. Account 90 in accounting is active-passive, therefore, credit turnover reflects the total amount of income, and debit turnover reflects the total amount of expenses.

Account 90 reflects revenue accounting entries for the following types:

- Sales of finished products, goods, semi-finished products of own production;

- Performance of work and provision of services;

- Sales of purchased goods;

- Providing for a fee the temporary use of your property (lease agreement), etc.

Account 84 - accounting entries and examples

Accounting account 84 is used to reflect and analyze generalized information about retained earnings (uncovered loss), the amount of which is determined based on the results of the reporting financial year. Using standard postings and illustrative examples, we will help you understand the specifics of using account 84 and the features of recording transactions with retained earnings.

The amount of net profit (loss) is determined based on the results of the reporting year when reforming the balance sheet. When determining profit, its amount is recorded according to Kt 84 in correspondence with Dt 99. If a loss is identified in the reporting year, then its indicator is reflected according to Dt 84.

The amount of net profit on account 84 can be distributed:

The loss, the amount of which is formed on accounting account 84, can be covered from the shareholders’ own funds, as well as from reserve capital:

| Dt | CT | Description |

| 82 | 84 | The loss is covered by the reserve fund |

| 84 | 83 | Profit is used to form additional capital |

At the end of 2015, JSC Fantasia received a profit of 184,200 rubles. By decision of the board of JSC Fantasia it was established that profits will be distributed as follows:

The accountant of Fantasia JSC made the following entries:

| Dt | CT | Description | Sum | Document |

| 99 | 84.01 Retained earnings | The amount of net profit received by JSC Fantasia is reflected | 184,200 rub. | Profit and Loss Statement |

| 84.01 Retained earnings | 82 | Part of the funds from the amount of retained earnings was used to replenish the reserve fund (RUB 184,200 * 12%) | RUR 22,104 | Minutes of the board's decision |

| 84.01 Retained earnings | 75 | Part of the funds from the amount of retained earnings was used to pay dividends to the shareholders of JSC Fantasia (RUB 184,200 * 65%) | 119.730 rub. | Minutes of the board's decision |

| 84.01 Retained earnings | 84.02 Profits subject to distribution | The balance of funds in the form of retained earnings is reflected in the accounts (184,200 rubles - 22,104 rubles - 119,730 rubles) | RUB 42,366 | Minutes of the board's decision |

According to the accounting policy of Megapolis JSC, one of the sources of capital investment is retained earnings. In January 2016, Megapolis JSC purchased a conveyor machine worth 175,300 rubles, VAT 26,741 rubles.

The following entries were made in the accounting of Megapolis JSC:

| Dt | CT | Description | Sum | Document |

| 08 | 60 | Purchased a conveyor machine (RUB 175,300 - RUB 26,741) | RUR 148,559 | Packing list |

| 19.1 | 60 | The amount of input VAT on the purchased machine is taken into account | RUR 26,741 | Invoice |

| 01 | 08 | The purchased conveyor machine was accepted for accounting | RUR 148,559 | OS commissioning certificate |

| 68 VAT | 19.1 | The amount of input VAT accepted for deduction | RUR 26,741 | Invoice |

| 84.02 | 84.03 | Targeted financing of the cost of the purchased machine has been taken into account (through the use of net profit) | RUR 148,559 | Consignment note, Asset entry certificate, Profit and loss report |

At the end of 2015, JSC Fiesta received losses in the amount of 841,800 rubles. The founders of JSC “Fiesta” are Savelyev R.N. (58% share in the authorized capital) and Markov K.L. (42% share in the authorized capital). By decision of the board it was established that the losses of 2015 would be covered at the expense of the founders:

- at the expense of Savelyev - 488,244 rubles. (RUB 841,800 * 58%);

- at Markov’s expense - 353,556 rubles. (RUB 841,800 * 42%).

The protocol of the board’s decision was signed in February 2021. In the same month, funds were received from Savelyev and Markov into the current account of JSC Fiesta.

To reflect operations to cover losses at the expense of the founders’ own funds, the following sub-accounts were opened in the balance sheet of JSC Fiesta:

- 75.1 - Savelyev’s funds aimed at repaying the loss;

- 75.2 — Markov’s funds used to repay the loss.

The following entries were made in the accounting of JSC Fiesta:

| Dt | CT | Description | Sum | Document |

| 75.1 | 84 | Savelyev's debt to repay the loss with his own funds is reflected | RUR 488,244 | Minutes of the board's decision |

| 75.2 | 84 | Markov's debt to repay the loss with his own funds is reflected | RUR 353,556 | Minutes of the board's decision |

| 51 | 75.1 | Funds from Savelyev were credited to repay the 2015 loss | RUR 488,244 | Bank statement |

| 51 | 75.2 | Funds from Savelyev were credited to repay the 2015 loss | RUR 353,556 | Bank statement |

| 99 PNO | 68 Income tax | The amount of permanent tax liability is taken into account (RUB 488,244 * 20%) | RUR 97,649 | Minutes of the board's decision |

Net profit and financial statements

The balance of account 84 is reflected in the balance sheet in section. III “Capital and reserves” on line 1370 “Retained earnings (uncovered loss)”.

Retained earnings (credit balance of account 84) are indicated without parentheses, and uncovered losses (debit balance of account 84) are indicated in parentheses.

In the income statement, line 2400 “Net profit (loss)” reflects the amount of the organization’s net profit for the reporting period.

The indicator for line 2400 of the Report should be equal to the final balance in account 99 “Profits and losses”, which, when closing the annual balance sheet, is written off to account 84 “Retained earnings (uncovered loss)”.

An example of calculating the difference in income tax

For example, an enterprise accepted for accounting a transformer substation worth 124,000 rubles. According to the OKOF classifier, the accountant classified it as depreciation group 7 (over 15 years to 20 years). The useful life was assigned a minimum, that is, 15 years: 15 years * 12 months = 180 months.

Accordingly, you can calculate monthly depreciation in accounting, calculated using the linear method: 124,000.00 / 180 = 688.89 rubles.

In tax accounting, an organization uses a non-linear method of calculating depreciation.

The Tax Code defines the standard for calculation using coefficients. For group 7, 1.3% was assigned. You can calculate what the depreciation will be for the 1st quarter. Table 1. Nonlinear calculation of depreciation

| Period | Calculation of the base in NU | Base for calculating depreciation in NU | Coefficient | Depreciation in NU |

| January | 124 000 | 124 000 | 1,3% | 1 612 |

| February | 124 000-1 612 | 122 388 | 1,3% | 1 591,04 |

| March | 122 388-1 591,04 | 120 796,96 | 1,3% | 1 570,36 |

To include the temporary difference in postings, you need to multiply it by the rate of 20%: 2706.73 * 20% = 541.35 rubles.

Table 2. Calculation of temporary differences

| Period | Depreciation in used | Depreciation in NU | VR calculation | Time difference (TD) |

| January | 688,89 | 1 612 | 688,89-1 612 | -923,11 |

| February | 688,89 | 1 591,04 | 688,89-1 591,04 | -902,15 |

| March | 688,89 | 1 570,36 | 688,89-1 570,36 | -881,47 |

| TOTAL | -2706,73 |

The accountant reflected the amount received by writing:

Debit 09 “Deferred tax assets” Credit 68.04 “Income tax” - the deductible difference in the amount of 541.35 rubles is taken into account.

Note from the author! We must remember that in the balance sheet account 09 will be taken into account in thousands of rubles.

Construction materials exceeding standards

When signing a contract, construction and repair organizations provide an act KS-2, which is actually an estimate. KS-2 indicates the cost of materials that are used for the construction of a specific facility. All consumption standards for building materials are known, they are approved by state regulatory authorities and published in open sources. Let’s say that during the work, the builders exceeded the amount of materials approved by the KS-2 document. The reasons for the overexpenditure could be theft, damage, destruction of materials, or the supply of low-quality materials or the correction of defects made by employees. Can an accountant for a construction organization write off materials spent in excess of norms as expenses? That is, if written-off materials are not included in KS-2, how does such overexpenditure affect income tax? In this case, builders should properly document the write-off of materials in excess of the norms. Tax consequences in the form of refusal to accept additional expenses will follow if the contractor does not provide inspectors with confirmation of the consumption of these materials. How does the tax office check write-offs of materials? Requires the tax authorities to provide papers confirming the purchase of materials, internal consumable invoices or invoices for the movement of materials from the warehouse to the site, as well as a certificate of completion of work signed by the customer. If the listed papers are correctly filled out, the taxpayer can count on the right to write off materials in excess of the norms and reduce income tax. Income tax is reduced by writing off materials in excess of norms during construction.

How is the financial result of an enterprise formed?

Within a month, all transactions are reflected in the organization’s accounts.

At the end of the month, the total profit or loss from ordinary activities, as well as from other income and expenses, is written off by posting to account 99:

- D90.9 K99 – profit from ordinary activities for the month is reflected;

- D99 K90.9 – loss from ordinary activities for the month is reflected;

- D91.9 K99 – profit from other income and expenses is reflected;

- D99 K91.9 – loss from other income and expenses is reflected.

When calculating income tax, it is accrued for payment to the budget by posting D99 K68. Income tax.

If emergency expenses arise, they are written off D99 K01 (04, 10, 43, 50, 70, etc.).

Closing account 99 at the end of the year

At the end of the year, the debit and credit turnover of account 99 are compared, and the final balance is displayed. If the balance is debit, then the financial result for the year is a loss, if the balance is credit, it is profit.

The loss or profit received during the year of activity must be written off at the end of the year, and account 99 is closed so that its final balance is equal to zero.

At the beginning of next year, accounting account 99 is reopened.

Postings for closing account 99 at the end of the year:

- D84 K99 – final financial result for the year – loss;

- D99 K84 – final financial result for the year – profit.

Balance Sheet Reformation

Balance sheet reformation is the closure of accounts related to the formation of the company’s financial result. Closing accounts means resetting their final balance to zero.

The reform concerns the following accounts: 90 “Sales”, 91 “Other income and expenses”, 99 “Profits and losses”.

Based on the results of the reformation of the balance sheet on account 99, the final profit or loss is identified and transferred to account 84 by the transactions indicated above.

The Reformation allows you to end the year, reset your accounts and start accounting in the new year with a “clean slate.”

The balance sheet is reformed on December 31 of the year after all business transactions related to that year have been reflected.

How to write off the shortfall amount at the expense of net profit

The only option is to write off the shortfall on the financial results of the organization. To identify shortages, conduct an inventory.

If the guilty persons are not found, then losses from the shortage of property and its damage are written off to the financial results of the organization (clause 28 of the Regulations, approved by Order of the Ministry of Finance of Russia dated July 29, 1998

N 34n). Determine the amount of the loss based on the value of the missing property according to accounting data and assign it to other expenses: Debit 91-2 Credit 94 - the loss from the shortage of property is written off due to the absence of the guilty party (refusal to recover damages). This procedure follows from paragraph 11 of PBU 10/99 and the Instructions for the chart of accounts. In tax accounting, take into account the shortfall within the limits of natural loss norms when calculating income tax as part of material expenses (subclause

Distribution directions

The directions for distribution of net profit can be mandatory and voluntary (i.e., by decision of the founders).

Mandatory contributions are made only by joint stock companies. Using net profit, they must create a reserve fund (capital). Every year, at least 5 percent of net profit must be allocated to the reserve fund (capital). Contributions may be terminated when the reserve fund (capital) reaches the amount provided for by the charter of the joint-stock company. The minimum size of the reserve fund (capital) is 5 percent of the authorized capital. This is stated in paragraph 1 of Article 35 of the Law of December 26, 1995 No. 208-FZ.

An LLC can also create a reserve fund (capital), but it is not obligated to do so. The size of the reserve fund (capital) and the procedure for its formation are determined by the company independently. This follows from Article 30 of the Law of February 8, 1998 No. 14-FZ.

By decision of the founders, the organization can direct its net profit:

– for the payment of dividends;

– to increase the authorized capital.

Enter the site

RSS Print

Category : Accounting Replies : 11

You can add a topic to your favorites list and subscribe to email notifications.

« First ← Prev.1 Next → Last (2) »

| boa.84 |

| Hello, to which account in accordance with the new chart of accounts should I now write off materials at the expense of net profit 90.8 or 91? Thank you |

| I want to draw the moderator's attention to this message because: Notification is being sent... |

| Tatiana [e-mail hidden] Republic of Belarus, Minsk, Molodechno Wrote 3221 messages Write a private message Reputation: 671 | #2[532023] August 20, 2012, 15:40 |

Notification is being sent...

If the result does not depend on the method of solution, it is mathematics, and if it does, it is accounting.| Tananda// [email hidden] Wrote 13011 messages Write a private message Reputation: 2383 | #3[557479] November 28, 2012, 11:07 |

Notification is being sent...

all women are angels, but when their wings are clipped, they have to fly on a broom| Victoria [email protected] Belarus Wrote 904 messages Write a private message Reputation: | #4[557510] November 28, 2012, 11:42 |

Tata // wrote:

Tell me, if I want to write off envelopes at the expense of profit (there is no accounting of outgoing correspondence), then I don’t charge VAT?

no no need to charge

I want to draw the moderator's attention to this message because:Notification is being sent...

| Tananda// [email hidden] Wrote 13011 messages Write a private message Reputation: 2383 | #5[557512] November 28, 2012, 11:45 |

Notification is being sent...

all women are angels, but when their wings are clipped, they have to fly on a broom| Volmerka [email protected] Wrote 4538 messages Write a private message Reputation: 723 | #6[557517] November 28, 2012, 11:49 |

Tata // wrote:

Tell me, if I want to write off envelopes at the expense of profit (there is no accounting of outgoing correspondence), then I don’t charge VAT?

Why at the expense of profit?

I want to draw the moderator's attention to this message because:Notification is being sent...

If you've been scammed, spread your wings...| Tananda// [email hidden] Wrote 13011 messages Write a private message Reputation: 2383 | #7[557519] November 28, 2012, 11:53 |

Notification is being sent...

all women are angels, but when their wings are clipped, they have to fly on a broom| Volmerka [email protected] Wrote 4538 messages Write a private message Reputation: 723 | #8[557522] November 28, 2012, 11:58 |

Tata // wrote:

I don’t have time to make lists where I sent them, I have the right to write them off at the expense of profit, the employer doesn’t mind

The fact that you have the right is undeniable. All clear

I want to draw the moderator's attention to this message because:Notification is being sent...

If you've been scammed, spread your wings...| Tasenka [email hidden] Belarus, Minsk Wrote 1092 messages Write a private message Reputation: 163 | #9[557525] November 28, 2012, 12:00 |

Notification is being sent...

| Volmerka [email protected] Wrote 4538 messages Write a private message Reputation: 723 | #10[557534] November 28, 2012, 12:07 |

Tasenka wrote:

Listen, where can I read about the fact that you can write off expenses only if you have mailing lists???

And I would too...

I want to draw the moderator's attention to this message because:Notification is being sent...

If you've been scammed, spread your wings...« First ← Prev.1 Next → Last (2) »

In order to reply to this topic, you must log in or register.

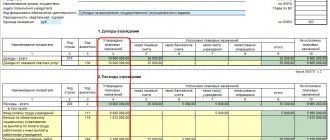

Formation of financial results for the year

To reflect the final financial result of an organization’s activities for a month or a year, account 99 “Profits and Losses” is used, the debit of which reflects losses, and the credit – profits.

The final profit or loss is formed by income and expenses from ordinary activities of the organization (sale of goods, products, provision of services, performance of work) and other income and expenses (which include operating and non-operating).

Income and expenses from ordinary activities are reflected in account 90 “Sales”, which is discussed in detail in this article.

Other income and expenses are reflected in account 91, which is described in detail here.

Plus, the financial result is affected by taxes, in particular, income tax, which reduces the organization’s final profit.

Also, account 99 may reflect other losses and profits received by the organization during the reporting period that are not accounted for in other accounts. For example, expenses received in emergency situations are written off directly to account 99.

New in accounting for expenses and net profit

Write-off against net profit*. ___________ * The term “net profit” is synonymous with the term “profit remaining at the disposal of the organization,” i.e.

This is the profit remaining after paying income tax and financial sanctions for settlements with the budget and extra-budgetary funds. We use the term “net profit” as the most concise one. __________ The first method was to reflect the costs of acquiring and creating assets (fixed assets, intangible assets, materials, goods, etc.)

P.). For non-current assets, these expenses were initially reflected in the debit of account 08 with their subsequent write-off from this account to the debit of accounts 01 and/or 04.

For current assets, expenses were reflected either directly on the debit of the accounts for their accounting (10, 41, etc.), or were first collected on the debit of account 15, and then written off from it to the accounts for asset accounting. The second method involves two accounting options:

What are accounting entries?

Every day millions of payments are made around the world. They are made by both ordinary people and businesses. Any business must take into account its own payments to keep them under control. Therefore, any payment is accounted for through accounting entries.

Accounting entries are accounts drawn up on actual papers, reflecting the amount of a business transaction that is subject to accounting.

Any information about actions performed on accounts is marked with a double entry, i.e. in the debit of one account and in the credit of another, for an identical amount. With its help, all accounts assume a single interconnected structure.

To understand the concept of accounting for debit and credit accounts, the following features of account accounting were introduced into accounting:

- asset – reflects the values owned by the organization;

- liability – displays the organization’s debt to creditors;

- active-passive account – displays one-time debit and credit debt.

This is interesting: How to celebrate a wedding outdoors - let’s take a closer look

Accounting entries for disposal of materials using examples

Let's consider the theoretical foundations that need to be relied upon when organizing the accounting of materials at the stage of their disposal.

We will also get acquainted with the accounting records of the facts of the economic life of the enterprise, that is, with the postings as a result of solving situational problems.

Let's study how accounting records are kept for the disposal of materials under account 10. Contents Materials received by the enterprise are acquired for some purpose: either for use in the production process directly, or for organizing the management process.

Therefore, there comes a time when materials are deregistered.

Upon disposal, their value must be assessed. Let's say an employee came to the warehouse for a certain name of material, and a release was made according to the request-invoice. At what cost should the accountant write off this item of inventory in accounting?

After all, in a warehouse it may turn out that units of the same material have different actual costs due to inflation, for different suppliers.

Accounting entries for net profit

Net profit - the posting of its reflection will be discussed in the article - includes the amount of turnover according to the company's current chart of accounts, accumulating all incoming and outgoing transactions for a certain period of time. It is calculated by any company and individual entrepreneur, since it is the result of entrepreneurial activity.

What is net profit?

Net profit in form 2

Postings to net profit

How to take advantage of net profit?

Results

How to take advantage of net profit?

Having completed the year, the company can decide to distribute profits. Options for this procedure are varied, for example:

- reduction in the amount of losses of previous periods (Kt 84);

- transfer of dividends (Kt 75);

- staff bonuses or material payments (Kt 70);

- replenishment of the Criminal Code (Kt 80);

- formation of various types of funds (Kt 82).

For options for using state of emergency, see the material “Art. 270 of the Tax Code of the Russian Federation (2015): questions and answers.”

Results

Net profit is the most important indicator that reflects the real state of affairs in the company. Its meaning is expressed in form 2 and has great practical content in the economic analysis of activity.

You can find more complete information on the topic in ConsultantPlus. Full and free access to the system for 2 days.

Disposal of retained earnings from previous years

The profit received by the company can be distributed exclusively by order of the owners of the company. This norm is provided for by the laws “On Limited Liability Companies” dated 02/08/1998 No. 14-FZ and “On Joint-Stock Companies” dated 12/26/1995 No. 208-FZ.

But there are also certain distribution frameworks that establish that when an NP is formed at the end of the year, the company is allowed to use it for the following purposes:

- issuance of dividends;

- repayment of previously incurred losses;

- to account 84 to accumulate profits for the purpose of its further use;

- formation of reserve capital;

- increase the authorized capital;

- other purposes established by laws No. 14-FZ and No. 208-FZ.

The direction of NP for the above purposes is accompanied by the corresponding entries in accounting:

| This year's NP is aimed at: | Dt | CT |

| For accrual of dividends | ||

| Formation of reserve capital | ||

| Increase the authorized capital |

In circumstances where the company decides to use retained earnings in account 84 to compensate for losses from previous years, it is necessary to make a posting between internal subaccounts. In other words, do internal wiring.

When a company receives a loss at the end of the year, it is allowed to repay it from the following resources:

- reserve capital;

- NP of previous years;

- authorized capital (after changes in the charter);

- target funds belonging to the founders.

In this case, the following wiring is required:

| If the loss is covered by: | Dt | CT |

| Reserve capital | ||

| Founders' target funds | ||

| Authorized capital |

In addition, the company has the opportunity to significantly reduce the loss incurred in the current period due to retained earnings from previous years. In a company that decides to do this, the accountant will make an internal entry to account 84.

Distribution of profits in LLC accounting entries

In accounting, this operation can be displayed in two accounts:

- 75-2 – these founders are not full-time employees;

- 70 – these founders are full-time employees of the enterprise.

Get 267 video lessons on 1C for free:

- Free video tutorial on 1C Accounting 8.3 and 8.2;

- Tutorial on the new version of 1C ZUP 3.0;

- Good course on 1C Trade Management 11.

Accrual and payment of dividends in accounting entries Account Dr Account Kt Entry amount, rub. Description of the entry Document-basis Payment of dividends in cash entry 84 70 (75-2) 175,000 Accrual of dividends to a resident shareholder in proportion to the equity participation of each founder (RUB 500,000.

Important: But the charter can change this order, that is, it can specify a disproportionate distribution of profits. However, it must be taken into account that for tax purposes, the tax authorities do not recognize the distribution of profits, which is disproportionate to the share, as dividends (Letter of the Federal Tax Service of Russia dated August 16, 2012 N ED-4-3/)

The basis for the distribution of profit is the data of the financial statements. Attention: Difficulty may arise if the company applies one of the special taxation regimes - the simplified regime (especially with the object of income), tax on imputed income. In this case, there are no restrictions, especially since organizations applying special regimes must also prepare financial statements

The absence of the need to take into account expenses for tax purposes does not mean that these expenses are not accepted in accounting.

List of transactions for write-off of materials

| Account Dt | Kt account | Transaction amount, rub. | Wiring Description | A document base |

| Write-off of materials for production | ||||

| 20 (23) | 10 | 12 000 | Write-off of materials to main (auxiliary) production | Limit collection card, movement invoice, write-off invoice |

| 25 (26) | 10 | 145 000 | Materials written off for general production (general business needs) | Invoice for movement, invoice for write-off |

| 44 | 10 | 12 300 | Written off materials that were used in the sale of goods and finished products | Invoice for movement |

| 10 | 10 | 108 000 | Transfer of materials from the main warehouse to the warehouses of workshop departments | Invoice for movement |

| Other reasons for write-off and gratuitous transfer | ||||

| Shortage (damage) in the presence of a culprit | ||||

| 94 | 10 | 21 390 | Write-off of the book value of materials | Write-off act |

| 20, 23, 25, 26, 29 | 94 | 8 500 | Write-off of materials within the limits of natural loss that were previously approved | Write-off act, book. reference-calculation |

| 73-2 | 94 | 12 890 | Write-off of the identified shortage of materials to the guilty party in an amount that exceeds the norm of natural loss | Write-off act, book. reference-calculation |

| 91-2 | 68-2 | 2 320,20 | The amount of VAT charged on the cost of materials exceeds the rate of natural loss | Account, account. reference-calculation |

| 50-01 | 73-2 | 12 890 | The culprit repaid the shortfall in cash | PKO |

| 70 | 73-2 | 12 890 | The amount of the shortfall was repaid from wages | Buh. reference-calculation |

| Shortage (damage) in the absence of the culprit | ||||

| 91-2 | 94 | 12 890 | Write-off of identified shortages of materials that exceed the norm of natural loss (the culprit has not been identified) | Write-off act, book. reference-calculation |

| Free transfer of materials | ||||

| 91-2 | 10 | 178 000 | Write-off of materials donated free of charge | Invoice, invoice |

| 91-2 | 68 | 32 040 | Charging VAT on the cost of donated materials | Invoice, invoice |

| Write-off of materials lost as a result of a natural disaster (accident) | ||||

| 99 | 10 | 127 500 | Materials that were damaged during a natural disaster were written off | Write-off act |

| 99 | 68 | 22 950 | VAT charged on the amount of damage | Check |

Use of net profit

The net profit is managed by the participants of the organization (shareholders) (clause 1, article 28 of Law N 14-FZ, clause 11.1, clause 1, article 48 of Law N 208-FZ).

They can use it, for example, for dividends, increasing the authorized capital or creating reserve capital.

In addition, losses from previous years are repaid using net profit.

In this case, an internal entry is made to the debit of subaccount 84-retained profit and the credit of subaccount 84-uncovered loss.

When distributing net profit, the following entries are made:

In addition, adjustment entries for account 84 correct significant errors of previous years that affected the financial result.

Write-off of the shortage at the expense of the net profit of the posting

If damage is detected in excess of the norms of natural loss, then the employee responsible for ensuring the safety of these valuables bears responsibility. Remember that all transactions reflected in accounting are supported by documents.

If a shortage of goods and materials is detected, an internal inspection is mandatory, based on the results of which the head of the company issues an order to compensate for damage or write off the shortage within the limits of natural loss norms.

When the shortage is written off within the limits of the standards, the order should also indicate the details of the regulatory act by which these standards were approved. The official audit also determines the circle of persons responsible for the shortage, because there is a high probability that the property was stolen not by an employee of the organization, but by a third party.

In this case, law enforcement agencies will look for the culprit of the shortage based on the organization’s statement of theft of property.

We recommend reading: Tax deduction for paid distance learning is applied

Income tax entries

If the profit calculated in tax accounting exceeds the “accounting” profit, then the temporary difference is deductible.

In this case, a deferred tax asset (DTA) appears. It is calculated like this:

- Amount of temporary difference x 20% (tax rate) = IT

- IT is reflected in accounting by the following correspondence:

- Dt 09 Kt 68

If the “tax” profit does not exceed the amount of “accounting” profit, then a deferred tax liability (DTL) appears.

This indicator is reflected in accounting by the following entry:

Dt 68 Kt 77 accrued IT.

When a constant difference appears, it is necessary to establish the nature of this value, whether the difference is positive or negative

If the profit for tax accounting exceeds the “accounting” indicator, then the constant difference is positive. In this case, a permanent tax liability (PNO) arises.

It is calculated like this:

- Positive constant difference x 20% = PNA

- This is reflected in the accounting by the following entry:

- Dt 99 Kt 68 – PNO accrued

If the profit in tax accounting does not exceed the value in accounting, then the constant difference is negative.

- In this case, a permanent tax asset (PTA) arises: Dt 68 Kt 99 – PTA accrued

- “Accounting” profit multiplied by 20% is called a conditional income tax expense, it is reflected in the following entry: Dt 99 Kt 68

- The resulting loss, multiplied by 20%, is a conditional income tax income, it is accounted for as follows: Dt 68 Kt 99

Profit calculated according to tax accounting data, multiplied by the tax rate, is called the current income tax; to carry it out, you do not need to write a separate entry in accounting.

Thus, the conditional income tax expense (income) approaches the amount of the current income tax.

When reducing or completely writing off temporary differences in accounting, you need to make the following entries:

- Dt 68 Kt 09 – ONA decommissioned

- Dt 77 Kt 68 – written off by ONO.

But it is possible that the difference will remain outstanding. Then the remainder of the difference must be attributed to other income and expenses using the following entry:

- Dt 91 Kt 09 – ONA decommissioned

- Dt 77 Kt 91 – written off by ON

Companies that do not use PBU 18/02 show the accrual of income tax with the following posting

Dt 99 Kt 68

Write-off of materials due to net profit posting

rub. Kt, thousand rub. 90/B 500 90/C 350 90/VAT 76 91/PD 150 91/PR 80 Postings: Dt 90/V – Kt 90/Z — 500,000 rub.; Dt 90/Z - Kt 90/S - 350,000 rubles; Dt 90/Z - Kt 90/VAT - 76,000 rub.

; Dt 91/PD - Kt 91/Z - 150,000 rubles; Dt 91/Z - Kt 91/PR - 80,000 rubles; Dt 90/Z - Kt 99 - 74,000 rubles; Dt 91/Z – Kt 99 — 70,000 rub. ; Also, entries were made in accounting for the accrual of permanent and temporary differences due to the difference between accounting and tax accounting: Accounting cost item, thousand rubles. If the organization decides to calculate personal income tax and insurance contributions, then additional entries will be made in the accounting: Dt73 Kt 68.01 - personal income tax has been calculated; Dt91 Kt 69 (according to the corresponding subaccounts) - insurance premiums have been calculated.

By virtue of paragraph 1 of Art. 210 of the Tax Code of the Russian Federation, when determining the tax base, all income of the taxpayer received by him, both in cash and in kind, or the right to dispose of which he has acquired, as well as income in the form of material benefits, determined in accordance with Art.