Types of car insurance

If an organization or individual entrepreneur that uses the simplified tax system has a car, then, of course, it needs to be insured under the MTPL program. Moreover, the payer of the simplified tax system can purchase a CASCO or DSAGO policy. But what about when calculating the single tax? Can insurance fees paid to an insurance company be expensed?

OSAGO is compulsory motor third party liability insurance. Without a compulsory motor liability insurance policy, your car will not be registered, you will not be allowed to undergo a technical inspection, and a traffic police officer will fine you on the road. OASGO is a mandatory type of car insurance.

DSAGO - additional civil liability insurance on a voluntary basis. In the case of insurance under DSAGO, the amount of payments under OSAGO (for compensation for damage to property, life and health of third parties) increases.

CASCO is a voluntary insurance contract that provides compensation for damage from car damage, theft or loss of a car (at the discretion of the policyholder).

The principle of “income minus expenses”

Having chosen the object of taxation “income reduced by the amount of expenses”, the payer of the simplified tax system in 2021 must keep records of income received and expenses incurred in the book of income and expenses. And based on this book, determine the final amount of tax to be paid.

As part of the “simplified” income, it is necessary to take into account income from sales and non-operating income (Article 346.15 of the Tax Code of the Russian Federation). In this case, income under the simplified tax system is recognized using the “cash” method. That is, the date of receipt of income is the day of receipt of funds, receipt of other property or repayment of debt by other means (clause 1 of Article 346.17 of the Tax Code of the Russian Federation).

The list of expenses that can be taken into account on a simplified basis is given in Article 346.16 of the Tax Code of the Russian Federation and is closed. This means that not any costs can be taken into account, but only justified and documented costs listed in the specified list. This list includes, but is not limited to:

- expenses for the acquisition (construction, production), as well as completion (retrofitting, reconstruction, modernization and technical re-equipment) of fixed assets;

- costs of acquiring or independently creating intangible assets;

- material costs, including costs for the purchase of raw materials and materials;

- labor costs;

- the cost of purchased goods purchased for resale;

- amounts of input VAT paid to suppliers;

- other taxes, fees and insurance premiums paid in accordance with the law. An exception is the single tax, as well as VAT allocated in invoices and paid to the budget in accordance with paragraph 5 of Article 173 of the Tax Code of the Russian Federation. These taxes cannot be included in expenses (subclause 22, clause 1, article 346.16 of the Tax Code of the Russian Federation).

- costs for maintenance of CCP and removal of solid waste;

- expenses for compulsory insurance of employees, property and liability, etc.

The company has the right to terminate the contract with the insurer, for example, when selling a vehicle. In this case, part of the previously transferred premium (minus the amount attributable to the period during which the contract was actually in force) is returned to the policyholder’s account and reflected in the accounting debit of the account. 51 from credit account 76.

| Operation | D/t | K/t | Sum |

| The insurer has decided to pay the balance under compulsory motor liability insurance | 76 | 91/1 | 12945,21 |

| Receipt of insurance compensation | 51 | 76 | 12945,21 |

In the same way, insurance compensation for damage from an accident is recorded in accounting, provided that the driver is innocent.

| Operation | D/t | K/t | Sum |

| The insurance premium for compulsory motor liability insurance has been paid. | 76 | 51 | 12 000 |

| The costs of purchasing the policy are taken into account | 29 | 76 | 12 000 |

| Repair work to restore the vehicle was reflected and paid for | 29 60 | 60 51 | 20 000 20 000 |

| Compensation under MTPL: | |||

| — accrued | 76 | 91/1 | 20 000 |

| - received | 51 | 76 | 20 000 |

The amounts of compensation received upon the occurrence of an insured event under compulsory motor liability insurance are taken into account as part of non-operating income for calculating the base for the single tax (clause 1 of article 346.15 and clause 3 of article 250 of the Tax Code) upon receipt of them to the current account or to the cash desk of the company.

Vehicle repair costs are recognized as expenses in the period in which they were incurred, in the amount of actual expenses (clause 1 of Article 260 of the Tax Code of the Russian Federation), even if the amount of insurance compensation established by the contract exceeds (Letter of the Ministry of Finance of the Russian Federation No. 03-03-06/2 /70 dated 03/31/2009).

How to take into account car insurance premiums under the simplified tax system

Let's see how paying for car insurance affects the reduction of the simplified tax system for different objects of taxation.

Income

If an organization or individual entrepreneur pays a single “simplified” tax on income, then the cost of car insurance does not in any way affect the calculation of tax according to the simplified tax system. After all, almost no expenses with this option are offset and the tax according to the simplified tax system is not reduced. Consequently, insurance for MTPL, DSAGO and CASCO does not reduce the simplified tax system (clause 1 of Article 346.14 of the Tax Code of the Russian Federation).

Income minus expenses

If a company or individual entrepreneur pays a single tax according to the simplified tax system on the difference between income and expenses, then the expenses under the compulsory motor liability insurance agreement (including the costs of technical inspection) reduce the tax base according to the simplified tax system. This is provided for in subparagraphs 7 and 12 of paragraph 1 of Article 346.16 of the Tax Code of the Russian Federation). Take into account payments for expenses as they are paid (clause 2 of Article 346.17 of the Tax Code of the Russian Federation).

As for contributions for voluntary insurance (DSAGO or CASCO), they do not reduce the tax base for the single “simplified” tax. The fact is that the list of expenses that can be taken into account when calculating the single tax is exhaustive (Article 346.16 of the Tax Code of the Russian Federation). And the costs of voluntary insurance are not included (Letter of the Ministry of Finance of Russia dated May 10, 2007 No. 03-11-04/2/119).

Read also

18.01.2017

Accounting for compulsory motor liability insurance under the simplified tax system

In accounting, expenses for compulsory motor liability insurance can be recognized simultaneously in the reporting period when they were incurred, or written off throughout the entire term of the contract, distributed in equal parts (clause PBU 10/99). An acceptable method is fixed in the accounting policies. In tax accounting, such costs are recognized upon payment (Article 346.17 of the Tax Code).

Accounting for compulsory motor liability insurance under the simplified tax system “Income minus expenses” is carried out in the accounts of the relevant industries - 20th account (main), 23rd, 25th, 26th, 29th, 44th (auxiliary, commercial, servicing), corresponding to account 76 on a specially designated sub-account “Insurance settlements”.

The use of account 76 is due to the specifics of settlements with the insurance company: payment for the purchased policy does not mean that the insurance service has been fully provided, since there is always the possibility of returning part of the insurance premium upon early termination of the insurance contract, or upon compensation for damage incurred in an accident.

Leasing payments and redemption value from the lessee under the simplified tax system

To do this, leasing costs must satisfy the requirements that the law sets for expenses taken into account when taxing profits (and the Tax Code of the Russian Federation). Input VAT paid in the amount of leasing payments recognized as expenses is also included in the reduction of the tax base (). Write off expenses in the form of leasing payments when calculating the single tax after leasing services are provided and paid for (). Confirm this fact (as well as the amount of payments), as well as those that indicate payment - acts, payment orders, etc.

d. (, Procedure approved). From the recommendation How can a lessee reflect lease payments in accounting and taxation in relation to the redemption value? Accounting The procedure for reflecting the redemption of property in accounting depends on several conditions: how the redemption value is paid - during the contract (in advance) or at its end; on whose balance sheet the property is recorded during the contract.

Insurance costs under the simplified tax system: accounting and tax accounting

Selections from magazines for an accountant Details Category: Selections from magazines for an accountant Published: 12/07/2014 00:00 Source: Glavbukh magazine Accounting for insurance costs In accounting, you need to take into account absolutely all expenses, and insurance costs under the simplified tax system are no exception. And since the machine is used in business activities, expenses associated with its maintenance and operation are expenses for ordinary activities (clauses 7 and 9 of PBU 10/99 “Expenses of the organization”).

The corresponding account will be account 76 “Settlements with various debtors and creditors” subaccount “Settlements for property and personal insurance”. You can write off insurance costs under the simplified tax system in one of two ways indicated in the table.

Methods for writing off insurance in accounting Method Characteristics What is the convenience of the method One-time attribution of the full amount of insurance to expenses The cost of insurance is included in expenses for ordinary activities at a time on the date the insurance contract comes into force (the date of payment of the policy) (clauses 5, 7 and 18 PBU 10/99). The postings will be as follows: DEBIT 76 subaccount “Calculations for property and personal insurance” CREDIT 51 - payment of the insurance premium is reflected; DEBIT 20 (23, 26, 44) CREDIT 76 subaccount “Calculations for property and personal insurance” - the cost of the insurance premium under insurance contract 1 is expensed.

This accounting procedure is convenient

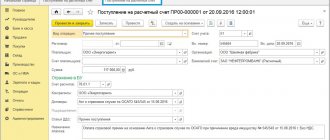

Accounting for transactions under MTPL and CASCO agreements in 1C:Accounting 8

Accounting, taxation, reporting, IFRS, analysis of accounting information, 1C: Accounting

02/13/2013 subscribe to our channel

Organizations that have vehicles must enter into compulsory civil liability insurance contracts.

Additionally, they can enter into voluntary property insurance contracts for motor vehicles.

Doctor of Economics, Professor S.A. talks about accounting and tax accounting of individual transactions under compulsory and voluntary insurance contracts in 1C: Accounting 8. Kharitonov. Enterprises in their economic life can use various vehicles, in particular cars. After purchasing a car, the organization must first enter into a compulsory civil liability insurance agreement (MTPL), since liability insurance for car owners is mandatory (clauses 1, 2 of Art.

4 of the Federal Law of April 25, 2002 No. 40-FZ

“On compulsory civil liability insurance of vehicle owners”

), and the received MTPL policy is necessary for registering the vehicle with the traffic police, its technical inspection and operation (clause

2 tbsp. 19, paragraph 3, art. 16 Federal Law of December 10, 1995 No. 196-FZ “On Road Safety”; paragraphs 1, 3 art. 32 of the Federal Law of April 25, 2002 No. 40-FZ).

The procedure for recognizing insurance expenses under the simplified tax system

If an organization/individual entrepreneur on the simplified tax system has chosen the object of taxation “income minus expenses”, in accordance with clause 2 of Art. 346.18, when calculating the taxable base, you can reduce the income received by the amount of expenses. The list of costs is closed and enshrined in Art. 346.16 Tax Code. In accordance with sub. 7 clause 1 art. 346.16 all compulsory types of insurance are subject to inclusion in expenses, namely:

- For simplified property insurance.

- Employee health and life insurance.

- For insurance of various types of civil liability.

At the same time, according to paragraph 2 of Art. 3 of Law No. 4015-1 of November 27, 1992, insurance can be voluntary or compulsory. In the latter case, the obligation to take out insurance is assigned to the policyholder by the legislation of the Russian Federation, and the amount of risks and minimum insurance amounts are established officially (clause 4 of article 3).

The simplifier has the right to recognize these expenses, subject to their compliance with the criteria named in paragraph 1 of Art. 252 Tax Code - that is, with documentary evidence and economic justification. The procedure for accounting for property insurance costs under the simplified tax system “income minus expenses” is prescribed in Art. 263 and corresponds to the procedure for recognizing such costs when calculating profit tax.

According to paragraph 2 of Art. 263, compulsory property insurance is included in expenses under the simplified tax system “income minus expenses” only within the limits of insurance tariffs approved at the legislative level. If the tariff level is not approved, the entire amount of actual costs may be taken into account in expenses. Voluntary property insurance is not included in the expenses of the simplifier.

For example, Vector LLC uses expensive equipment in its current activities and enters into a voluntary insurance agreement for this property. How to calculate the amount of insurance premiums? Since this type of insurance is not mandatory, a simplifier will not be able to include an insurance premium of 42,000 rubles in expenses under the simplified tax system. even after paying it.

In accordance with Law No. 40-FZ of April 25, 2002, MTPL insurance under the simplified tax system “income minus expenses” can be included in costs, since this type of insurance is mandatory. Therefore, if a simplifier uses cars in his business activities, he has the right to take into account the amount of car insurance in his expenses under the simplified tax system after it has actually been paid. At the same time, voluntary types of insurance, such as CASCO or DSAGO, cannot be taken into account when calculating the simplified tax.

For example, Volgograd-Opt-Trade LLC in April 2021 purchased a car on its balance sheet, for which an OSAGO policy worth 15,000 rubles was paid. and a CASCO policy worth RUB 45,000. Both amounts were transferred to insurance companies in May, but the company’s accountant can only take 15,000 rubles as expenses. for compulsory insurance. Reduce the tax base by 45,000 rubles. when calculating tax using the simplified tax system, it will not work, since this type of insurance is voluntary.

Accounting for the leased asset

If the leased asset is listed under the agreement on the balance sheet of the lessee, recognize it in accounting as a fixed asset. Its price includes:

- all expected payments under the leasing agreement, including the purchase price;

- costs of delivery, setup and completion of the leased item.

Important! In tax accounting, the initial cost of a leasing asset is equal to the amount of the lessor's expenses for the purchase and setup of property (clause 1 of Article 257 of the Tax Code of the Russian Federation). Even if the asset is on the lessee’s balance sheet.

When accounting for the lessee's balance sheet, create the following entries:

- Dt08 Kt76 - reflects the cost of property received under a leasing agreement;

- Dt08 Kt20/23/25/26/60/76 - reflects the costs of installation, commissioning, etc.;

- Dt01 Kt08 - the leasing object was put into operation;

- Dt 20/23/25/26/29/44 Kt02 - depreciation.

If the leased property is listed on the lessor’s balance sheet, reflect the received property on the debit of off-balance sheet account 001.