Financial assistance as a type of income

Such support, unlike other types of income, does not depend on:

- from the employee’s activities;

- from the results of the organization’s activities;

- from the cyclical nature of work periods.

The grounds for receiving financial assistance can be divided into two: general and targeted. It is provided when any circumstances arise in the employee’s life:

- anniversary, special event;

- difficult financial situation;

- illness of an employee or close family member;

- death of an employee or close family member;

- birth of a child;

- emergencies;

- vacation.

A complete list of grounds for calculating financial assistance, as well as their amounts, are established by the regulatory (local) document of the organization. In some cases, for example, due to illness, the amount of financial assistance will be determined by the decision of the manager.

What does size depend on and how is it determined?

The amount accrued as assistance is not affected by the position held by the employee or his salary. The amount of financial assistance is determined solely on the basis of local documents, which not only allow for the calculation of payments of this kind, but also stipulate their amounts.

The employer has the right to independently set any amount, coordinate it with the trade union organization, and fix it in a local regulatory document (for example, in a collective agreement).

That is, in fact, the amount of accruals may be affected by:

- social policy pursued by management at a particular enterprise or organization;

- financial capabilities of an organization or enterprise, namely profit margins.

However, in reality, management needs to focus not only on local documents, but also on current legislation.

According to the order of the Ministry of Finance, issued in 2007, a one-time financial payment due to an emergency situation (this can also include the death of a loved one) should not exceed two months’ salary.

There is also a tax-free limit that must be taken into account. Otherwise, the employer will have to pay insurance and tax amounts.

Taxation of financial assistance

The main question that an accountant asks is whether financial assistance is subject to personal income tax?

Each type has its own distinctive characteristics and accounting features for determining the personal income tax base, as well as insurance premiums. The personal income tax and contribution base depends on the basis for which financial assistance was provided. It is indicated in the employee’s application. Taxation of financial aid follows the same principles. At the same time, monetary support from the employer is either completely tax-free or not taxed up to an amount limit, which depends on the basis.

Tax-free financial assistance (NDFL)

Financial assistance is a social payment from the employer that is not related to the employee’s performance of his official duties. It can be provided to employees or their close relatives. Money is issued at the request of a worker or other person. Documents confirming the reasons for issuing funds are attached to it. Based on the papers, a corresponding order is issued.

Financial assistance is issued to an employee or other person for financial support in special life situations. Such a payment can be made at the birth of a baby, the death of a loved one, in emergency circumstances, etc.

Is it taxable and to what extent?

Personal income tax on material assistance begins to be withheld when its amount per year exceeds 4 thousand rubles. It does not matter what taxation system the company uses. The purpose of the payment also does not play a role in taxation.

Personal income tax is not charged on financial assistance, regardless of its amount, in cases of its payment:

- To the victim of a natural disaster or emergency or to the relatives of a citizen who died as a result of these incidents. The employer must receive a certificate confirming the emergency situation, for example, from the Ministry of Emergency Situations.

- A person who was injured from a terrorist attack that occurred in the Russian Federation or a relative of a person who died from terrorism.

- An employee, members of his family, a retired former worker to pay for medical expenses. Costs must be documented. The amount paid out of the company's net profit is not taxed.

- Relatives of a deceased employee or retired former employee. This payment is a one-time payment, i.e. it is assigned by one order of the director.

- To the worker, in. including an ex who retired due to the death of a family member. The payment must be a one-time payment.

Source:

Is financial assistance subject to personal income tax in 2021?

This is the allocation of funds to solve emergency life situations. In many cases, such payments are not subject to income tax, but this is not always the case. To understand whether material assistance is subject to personal income tax (2016-2017), you need to consider different cases of its provision in detail.

What are the grounds for transferring financial assistance to employees?

Companies that value their employees and do not want to lose them in conditions of high competition for qualified personnel are introducing additional incentive systems. One of them is financial assistance. This is the allocation of money from the organization’s budget, which an employee can use to solve a difficult (force majeure) situation that has arisen in his life.

Reasons for receiving such funds include:

- birth of a child;

- wedding;

- the occurrence of serious health problems;

- death of relatives;

- fire, flood and other disasters.

It would be wrong to assume that financial assistance is subject to personal income tax.

It has a number of essential differences from the salary on which income tax is transferred: it does not depend in any way on economic indicators and the results achieved in the employee’s activities, does not compensate for his costs incurred in the production process, and does not reward him for any achievements. This is not part of the financial incentive; it is not paid regularly, but only in certain emergency cases.

The basis for the transfer is the employee’s statement written in the name of his immediate supervisor. The decision to issue money is exclusively social and emotional in nature.

It is expected that with the use of these tools, the employee will be able to overcome the difficult situation in his life.

Often the possibility of making payments of this kind is enshrined in a collective agreement between the staff and the employer, in a trade union agreement or in employment contracts.

Exemption of most types of financial assistance from personal income tax requires the company's accountant to correctly prepare all related documentation.

Money for these purposes is allocated from the company's budget or from its net profit.

If financial support is allocated to full-time students at a university, the funds for it are drawn from a special fund, which makes up a quarter of the scholarship fund.

How to determine whether financial assistance is subject to personal income tax?

Current legislation defines an exhaustive list of situations in which a particular monetary transfer can be classified as “material assistance.” This is done in order to prevent possible abuses when calculating the tax base.

The main requirements for social benefits include:

- Size. The amount of transfers per employee for the entire reporting period should not exceed 4,000 rubles. It does not matter whether the employee continues to work or was dismissed due to disability or reaching retirement age;

- Documentary confirmation. In order not to pay personal income tax on material assistance in 2021, the organization must confirm that the difficult situation that the transfer is aimed at solving actually took place.

- If an employee is receiving benefits due to the loss of a close relative (child, parent, spouse), a death certificate must be provided;

- If an employee was injured during a terrorist act committed on the territory of Russia, then he must provide a certificate from the police confirming the fact that this crime was committed;

- If the property or health of an employee was damaged as a result of a natural disaster, then documents from the competent authorities are needed that will contain information about this disaster;

- Special life circumstances. A number of events, such as the death of one of the employee’s family members or an emergency, serve as grounds for not accruing personal income tax. However, we repeat, it is necessary to have documents confirming this situation.

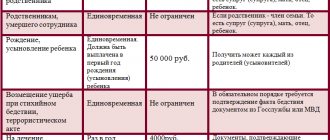

If financial assistance is provided for the birth of a child, its amount cannot exceed 50 thousand rubles. Only this amount is not subject to income tax, and for any excess there is a rate of 13%. The law does not specify who has the right to such encouragement: the father or the mother. It can be received by one of the parents or both.

Regardless of the situation on the basis of which an organization transfers funds to its employee, there must be mandatory documentary evidence.

If the tax inspectorate considers the facts provided to be insufficient, it may disagree with the legality of classifying the payment as “material assistance” and impose a tax on it.

The reason for refusal may be the absence of any documents, including a properly executed application from an employee addressed to the manager.

If a cash payment to an employee is recognized as completely legitimate and is not subject to personal income tax, then there is no need to make contributions to insurance funds.

Source:

Is financial assistance subject to personal income tax and in what cases in 2018

Many employers, wanting to provide additional incentives to their employees, are introducing a system of incentives in the form of financial assistance, which can be issued in the event of certain force majeure circumstances.

Some types of financial assistance are exempt from personal income tax, however, not everything is so simple.

As practice shows, the employer must clearly know whether financial assistance issued for a specific case is subject to personal income tax.

Procedure for paying financial assistance

Most companies that value their employees and want to retain them in the face of fierce competition for highly qualified personnel offer employees financial assistance when difficult life situations arise. Help is usually offered if one of the following situations occurs:

- disaster

- death of a close relative

- wedding

- birth of a child

- serious illness.

Such assistance to an employee is not of an economic nature, does not depend on the employee’s performance indicators, and should not in any way constitute a form of remuneration.

Material assistance cannot be part of the system of financial motivation of employees, is not an incentive for work performed, and is paid as compensation for costs incurred by the employee during the production process. Also, it cannot be issued regularly.

Assistance provided to an employee to help overcome a difficult life situation is exclusively social and emotional in nature. Often, the possibility of receiving such payments is provided for in an employment contract, a trade union agreement, or a collective agreement.

Source: https://lgotaposobie.ru/materialnaya-pomoshh-ne-oblagaemaya-nalogom-ndfl.html

Not taxed

The list of such income is specified in Art. 217 Tax Code of the Russian Federation. In particular, financial assistance, tax-free for 2021, is provided in the following cases:

- death of an employee or a close member of his family;

- natural disaster;

- purchasing sanatorium and resort vouchers on the territory of the Russian Federation (compensation depending on the type of support, for example, for accompanying parents of children with disabilities to a place of recreation and recovery);

- emergency situation (terrorist attack and others).

Financial assistance to family members of a deceased employee

If your internal local regulations provide for financial assistance for a deceased employee, then we will consider this situation in detail. According to paragraph 8 of Art. 217 of the Tax Code of the Russian Federation, financial assistance upon the death of an employee is not subject to personal income tax in full if the following conditions are met:

- the payment is made to family members of a deceased employee or a former employee who has retired;

- payment is made in a lump sum.

On the issue of a one-time payment, there is a letter from the Ministry of Finance dated October 31, 2013 No. 03-04-06/46587. It doesn’t matter how the assistance is paid – in one payment or several. The most important thing is that it is related to one event and paid on the basis of one order.

Accordingly, if the payment is made to non-family members of the deceased employee, then do not forget to withhold personal income tax from the full amount of financial assistance.

You can familiarize yourself with the issues of accounting for financial assistance in the article: “Accounts for accounting for financial assistance.”

Taxed over the limit

This applies to support that is of a general nature by providing:

- birth, adoption, establishment of guardianship rights - in the amount of no more than 50,000 rubles for each child when paid within 1 year after birth;

- the amount of partial compensation for sanatorium and resort vouchers in the Russian Federation in the amount of up to 4,000 rubles (taking into account the type of assistance, for example, to support the health of children due to severe environmental and climatic conditions, etc.);

- anniversary, special event (wedding) - up to 4,000 rubles;

- support for an employee in a difficult life situation, vacation - up to 4,000 rubles.

Let us remind you that the limit of financial assistance for the birth of a child is 50,000 rubles per parent. Such clarifications were given by the Ministry of Finance of the Russian Federation in letter dated 08/07/2017 No. 03-04-06/50382. Previously, officials considered the set amount to be the limit for both parents or guardians.

IMPORTANT!

When calculating personal income tax, a deduction for financial assistance on a general basis up to 4,000 rubles is provided once, regardless of how many times the support is provided.

Categories of workers eligible for assistance

The main problem for employers is often the wording “close relative”. This concept has different interpretations, but by default the definition from the Tax Code (its reference to family law) is used, since the issue concerns finance and its taxation.

Article 217 of the Tax Code provides a direct reference to Article 14 of the Family Code, according to which close relatives include:

- persons who are related by blood in the ascending line (mother, father, grandmother, grandfather);

- persons who are related by blood in a descending line (children, grandchildren, brothers and sisters, including stepsisters).

But, according to an already established tradition, many employers also classify wives or husbands as relatives, although they are not blood relatives.

And according to the order of the Ministry of Finance (letter number 03-05-01-04/234 dated August 2006), relatives also include adoptive parents and the citizens they have adopted.

Accordingly, assistance is accrued in the event of death:

- the employee himself (paid to his family members);

- a former employee who is already retired (money is also paid to his family members);

- his immediate family (the assistance is issued to the employee).

Income codes and material support deduction codes

The personal income tax tax base codes are fixed in the Order of the Federal Tax Service dated September 10, 2015 No. ММВ-7-11/ [email protected] Depending on the basis of financial assistance, the following are determined:

- material assistance income code (Appendix 1 of the Order of the Federal Tax Service);

- deduction code that provides financial assistance (Appendix 2 of the Federal Tax Service Order).

Let's look at an example. As a result of the fire, the employee lost her husband, long-term treatment did not produce results, the employee took leave due to life circumstances. By decision of the head of the organization, the employee was provided with financial support:

- in connection with a natural disaster - 100,000 rubles;

- in connection with the death of a spouse - 80,000 rubles;

- compensation for the cost of treatment - 60,000 rubles;

- in accordance with the collective agreement, when taking annual leave, an employee is entitled to support in the amount of two salaries (salary for the position held is 20,000 rubles), thus, financial assistance for leave amounted to 40,000 rubles.

Below we discuss the taxation of financial assistance to an employee in 2021, as well as financial assistance up to 4000 (2021 taxation).

Design features

To apply for assistance to an employee (or his relatives, if we are talking about the death of a current or former employee), you must submit to the accounting department:

- An application issued to the head of an organization or enterprise, containing a brief request for assistance.

- In this document, the full name of the manager and his position are indicated at the top; the last name, first name and patronymic of the employee, his position and the structural unit in which he works are entered below. The body of the document indicates exactly who died and what amount of payment the employee is claiming (this point can be omitted).

- Then the supporting documents that are attached to the application are listed.

- The date of compilation and the signature of the employee are placed at the bottom.

Applications for financial assistance in connection with the death of a close relative can be found here.

A death certificate (its copy) is also submitted, confirming the fact of this sad event. And documents confirming relationship (for example, marriage certificate).

Based on the documents received and a statement written by the employee or his relative (if the employee himself has died), an appropriate order is prepared, which is then signed by management.

This document does not have a single (unified) form. Therefore, it is drawn up in any form, but the manager must indicate the amount of payment and the circumstances (reasons) according to which the funds will be accrued.

For example: “According to paragraph 21 of the collective agreement, I order one-time financial assistance to accountant E.I. Chumakova. in the amount of 5,000 (five thousand) rubles in connection with the death of the mother. Payment from the cash desk should be made on June 28, 2021. Grounds: statement of E.I. Chumakova, copy of her mother’s death certificate.”

The order must be familiarized with the signature of the person who submitted the application.

In accounting documents, the accrual of assistance and its payment is reflected as account 70. Credit “salaries” (it is also indicated here that the assistance was accrued on the basis of an order from management). The debit “Other expenses” is indicated (account 91). The payment is processed as a debit to account 70 and a credit to account 50 (cash). It must be indicated that the assistance was paid according to a cash receipt order.

How to get maternity leave if you don’t work - a detailed guide! Correct calculation of sick leave is very important. Therefore, our article was written specifically for this topic. How to resolve the issue of sick leave pay after your dismissal - read here.

Calculation of the base for insurance premiums

IMPORTANT!

If payments are reflected in one of the reporting forms, then, based on clause 3 of the inter-document control relationships, prepare explanations for discrepancies in the forms. For example, non-taxable income not indicated in the 2-NDFL certificate and reflection of the dates of transfers for the specified payments in the 6-NDFL form.

Finally, let’s figure out whether financial assistance is subject to insurance contributions or not.

When determining the base of insurance premiums, support amounts are legally excluded on the same grounds as the base for calculating personal income tax.

What is financial assistance?

The generally accepted rewards for employees for fruitful work, for contribution to the development of the company, ideas or the introduction of know-how consists of bonus payments, 13th salary, one-time or quarterly bonuses and other material payments and valuable gifts.

Each such payment relates to employment and is subject to income tax. The list also includes valuable gifts. However, there are situations when serious joyful or tragic events happen in the life of an employee. In such cases, the company management has the right to provide one-time financial assistance to an employee in need.

The amount allocated by the company is determined by the manager himself. Usually in the internal labor regulations, in the form of a decree, there is a procedure for issuing financial assistance to employees. According to this provision, each employee, in connection with a life situation that has arisen, has the right, on the basis of his application, to which the relevant documents are attached, to receive extremely necessary assistance.

In organizations where such a procedure is not provided, material assistance is provided voluntarily by the team itself. Typically, each employee allocates either a fixed or feasible amount. It is often practiced to raise funds monthly for life force majeure of employees.

The initiative in organizing this kind of fund is taken by the team itself. The amount of the illegal fund itself is not taxed - all contributions and payments are made legally upon receipt of wages.

How the position of the Ministry of Finance has changed regarding the imposition of personal income tax on material assistance at the birth of a child - see this video:

The legislative framework

The Ministry of Finance of Russia and the Federal Tax Service in their letters regulate and regulate the procedure for settlements, insurance premiums, filling out 6NDFL, 2NDFL, recording accounting entries and the basis for paying one-time financial assistance. To fully understand your rights, you can read the second part of the Tax Code of the Russian Federation, Articles 23, 217, 422. Changes are published in Letters of the Ministry of Finance and the Federal Tax Service of the Russian Federation.

In July 2021, the Ministry of Finance published a letter on insurance premiums, which amended the conditions and procedure for paying financial assistance to employees. The previous letter has been withdrawn. In turn, the Federal Tax Service also published a letter in July, which explains in more detail the procedure for filling out personal income tax, after amendments made by the tax service.

Financial assistance is considered one-time if issued on the basis of one order. Management may, by one order, assign one single payment or several payments not exceeding the total limit.

If there are several orders regarding one person, then in addition to the amount indicated in the first order, the rest will be subject to tax and insurance contributions.

A large number of orders per employee during the reporting period equates to an attempt to hide true income and leads to an unscheduled audit by the tax inspectorate.

Management, when providing financial assistance to employees, is based on documents confirming such a need. Documents can be provided after the employee receives the amount. For example, a marriage or birth certificate. Financial assistance in such cases is necessary on the eve of the upcoming event.

Conclusion

An organization may pay its employees a one-time cash payment that is not related to the performance of their job duties. Is financial assistance subject to personal income tax? Yes, provided that the payment amount exceeds 4 thousand rubles. The legislation also stipulates certain cases when financial assistance is not subject to taxes. The existence of conditions for payment of financial assistance must be documented. In the absence of a certificate, statement or order from the director, the tax office may consider the payment unlawful and charge additional personal income tax.