Normative base

Letter of the Federal Tax Service of the Russian Federation dated 08/18/2011 N AS-4-3/

Letter of the Ministry of Finance of Russia dated 08/27/2012 N 03-04-05/6-1006

Order of the Federal Tax Service of Russia dated September 10, 2015 N ММВ-7-11/ “On approval of codes for types of income and deductions”

Letter of the Ministry of Finance of Russia dated February 17, 2016 N 03-04-05/8718

Letter of the Ministry of Finance of Russia dated December 16, 2014 N 03-04-05/64847

Letter of the Ministry of Finance of Russia dated December 2, 2016 N 03-04-05/71785

Letter of the Ministry of Finance of Russia dated January 20, 2017 N 03-04-06/2414

Ruling of the Supreme Court of the Russian Federation dated August 20, 2015 N 304-KG15-9468 in case N A45-16187/2014

Letter of the Ministry of Finance of Russia dated 02.09.2014 N 03-03-06/1/43912

Letter of the Federal Tax Service of Russia dated December 15, 2016 N BS-4-11/

How to charge in 1C

Many accountants often ask the question: how to reflect in 1C:Enterprise financial assistance to an employee in connection with the death of a relative? The answer depends on the version of the special 1C software product.

So, for example, in 1C: Salary and HR management, accrual is carried out using a special document “One-time benefit”. You can find it by pressing the F1 button and calling up the search window. In the search bar that appears, enter the letter query “burial.”

Or select the “Salary” section, then the “All documents” item, click the “Create” button. Select “One-time benefit” from the list provided.

Legal documents

- Federal Law No. 8 of January 12, 1996

- Art. 2 of the Family Code of the Russian Federation

- Decree of the Government of the Russian Federation dated January 26, 2018 No. 74

- Art. 217 Tax Code of the Russian Federation

- No. 125-FZ

- Art. 422 Tax Code of the Russian Federation

- Order of the Federal Tax Service of the Russian Federation dated September 10, 2015 No. ММВ-7-11/ [email protected]

Tax-free financial assistance 2021

Who can receive financial assistance at work? To give financial assistance or not to give is the right of the employer. Financial assistance may also be paid selectively. During a calendar year, an employee has a non-taxable limit of financial assistance of 4,000 rubles for various purposes. The limit of 4,000 rubles does not depend on the connection in which the money was issued. It could be:

- wedding;

- birthday;

- financial assistance for the anniversary (taxation 2020);

- acquisitions;

- treatment, etc.

Taxation of financial assistance in 2021 and insurance premiums from it vary depending on whether payments exceed 4,000 rubles.

The only exceptions are:

- death of an employee or his relative;

- birth of a child;

- natural disasters and terrorist attacks.

When a subordinate becomes a parent, he can be paid up to 50,000 rubles without calculating insurance premiums. Financial assistance in connection with the death of a family member, compensation for damage due to injury, terrorist attack, emergency or accident are not included in the base for calculating insurance premiums and personal income tax. Thus, taxes on financial assistance and the maximum amount in 2021 remain unchanged for now.

Please note that one-time financial assistance is considered a payment for certain purposes, accrued no more than once a year on one basis, that is, on one order (Letter of the Federal Tax Service of Russia No. AS-4-3/13508). How a person receives the money - all at once or in parts throughout the year - does not matter (Letter of the Ministry of Finance of Russia No. 03-04-05/6-1006).

Financial assistance at the birth of a child

Insurance premiums are not charged on one-time financial assistance for the birth of a child, paid to an employee who has become a parent, guardian or adoptive parent, if the following conditions are met (Tax Code of the Russian Federation):

- the payment was made within a year from the date of birth (adoption) of the child or the beginning of guardianship;

- the amount of payment does not exceed 50,000 rubles. for each child.

If both parents work for the same employer, and assistance is provided to both, payments to each of them up to 50,000 rubles are not subject to contributions.

In the part exceeding this amount, one-time financial assistance at birth (adoption, establishment of guardianship) is subject to insurance contributions according to the general rules.

Financial assistance: taxation 2021, insurance premiums

Is financial assistance subject to insurance premiums in 2020? Since financial assistance does not relate to income related to the employee’s performance of his work duties, it cannot be subject to contributions. However, this provision has a number of limitations. That is, the manager cannot pay his employees any amount as financial assistance. Since 2021, issues related to fees for employee insurance are explained in Chapter 34 of the Tax Code of the Russian Federation. Situations when you do not have to pay are contained in Art. 422 codes. Amounts from one-time financial assistance paid under the following circumstances are not calculated:

- the employee received money to compensate for damage caused by a natural disaster or emergency;

- the victim of a terrorist attack on the territory of the Russian Federation was compensated for damage to health;

- the employer helped with money in the event of the death of a member of his family;

- an amount of up to 50,000 rubles was paid as support for the birth of a child. Not only each parent, but also the adoptive parent and guardian have the right to it;

- the amount of financial assistance does not exceed 4,000 rubles during the year.

We remind you that 4000 rub. - this is tax-free financial assistance (2020). If payments are higher, they are subject to insurance premiums. In this case, the goals may be different, for example, for partial compensation of expenses for additional education, to cover the costs of purchasing medicines, for vacation. Note that the situations listed apply to all existing types of compulsory insurance: pension, medical, social, as well as injuries. In addition, they apply to assistance in both in-kind and cash forms. So, 4000 rubles for financial assistance. (taxation 2020) insurance premiums are not charged

Is financial assistance subject to insurance premiums?

Article 422 of the Tax Code of the Russian Federation contains a list of cases when financial assistance is not subject to insurance contributions.

Depending on this, the entire amount of financial assistance or only some part of it is not subject to contributions. So, according to sub. 3 p. 1 art. 422 of the Tax Code of the Russian Federation, regardless of the amount of payment, certain types of financial assistance are completely exempt

Here is financial assistance that is not subject to insurance contributions:

- issued to an employee one-time in connection with the death of a family member ;

- issued to individuals to compensate for damage caused to them by a natural disaster or other emergency ;

- issued to people who suffered from terrorist attacks on the territory of the Russian Federation.

In addition, individuals receiving financial assistance who are not employees of the person who pays this assistance are not insured persons for this payer. Therefore, such payments cannot be subject to insurance premiums .

Financial assistance up to 4000 (taxation 2020)

Let's consider the taxation of financial assistance to an employee in 2021. Is financial assistance subject to personal income tax (2020)? The withholding of personal income tax is indicated in Chapter 23 of the Tax Code of the Russian Federation, and Article 217 of the Tax Code of the Russian Federation specifies whether financial assistance is subject to personal income tax. If you carefully read this article, it will become clear that income tax for individuals is not withheld in the same cases when insurance premiums are not collected. We are talking about the payment of money upon the birth of a child or the death of a family member, amounts up to 4,000 rubles (for any purpose). At the same time, we must remember that the 2-NDFL certificate will have different income codes and deduction codes each time - depending on the type of financial assistance provided and taxation or collection of insurance premiums (Order of the Federal Tax Service of Russia dated September 10, 2015 No. ММВ-7-11/).

Here are some more interesting points:

- According to the Ministry of Finance, monthly financial assistance to a person on maternity leave can be subject to personal income tax, taking into account standard tax deductions, the amounts of which are contained in paragraphs. 4 clause 1 of Article 218 of the Tax Code of the Russian Federation (Letter dated 02/17/2016 No. 03-04-05/8718). In other words, if an employer pays extra every month to a woman on maternity leave, he can reduce the amount of the extra payment by the so-called child deduction. Since this form of support may be a general type of financial assistance, and not a one-time payment in connection with the birth, although one reason is the birth of a baby;

- financial assistance, tax-free in 2021, is provided by the employer to family members of a deceased employee or former employee who previously retired due to disability, age or old age, or to the employee (pensioner) himself if one of his family members has died (Letters from the Ministry of Finance dated 16.12 .2014 No. 03-04-05/64847, dated 12/02/2016 No. 03-04-05/71785);

- if the fact of an emergency or terrorist act is not confirmed, the employer takes personal income tax from compensation (Letter of the Ministry of Finance dated January 20, 2017 No. 03-04-06/2414).

Conditions and procedure for receiving financial assistance

The provision of financial assistance to an employee and personal income tax is not related to entrepreneurial or other activities. To receive financial assistance from regional or federal authorities, as well as an employer, grounds are required.

The main role is played by obtaining the status of a low-income family, in which:

- The family member is not employed.

- A close relative retired. According to the new rules of pension reform, the return for women is 60 years, for men - 65.

- The citizen has the status of “pensioner” and lives alone from his family.

- The person has a disability group, i.e. with limited capabilities.

- The family has several young children.

Read also: Extension of maternity leave

Thus, only truly needy citizens have the right to receive financial assistance. To complete the procedure, social protection authorities are involved, and the level of income and living conditions are checked.

Applicants send a package of documentation and an application to the relevant departments. Based on the results of the review, the institution announces a verdict on the provision or refusal to receive financial assistance payments. In a situation where the application is not satisfied, the agency is obliged to provide legitimate reasons for the refusal in writing.

Tax on financial assistance

Please note: funds for one-time support are transferred when appropriate circumstances arise. At the same time, assistance has no connection with the person’s performance of any functions or actions and does not entail the imposition of obligations.

Support for quitting employees

An interesting question: what to do with insurance deductions from payments to ex-employees. Article 420 of the Tax Code of the Russian Federation will help answer this, which states that contributions are accrued for remuneration under employment agreements or GPC agreements. Since there are no such relationships with those who quit, there is no need to retain anything. At the same time, inspectors may have questions on what basis financial support was provided. Organizations need to keep this point in mind when discussing financial assistance (taxation 2021, insurance premiums).

Exemption of financial assistance from insurance premiums

Taxation of material assistance through insurance premiums is regulated by the provisions of Chapter 34 of the Tax Code of the Russian Federation.

As a general rule, financial assistance accrued to an employee in accordance with the employment contract and local regulations of the company is exempt from the calculation of insurance premiums. This provision is contained in paragraph 3 of paragraph 1 of Art. 422 of the Tax Code of the Russian Federation and provides for exemption from the calculation of contributions to the Pension Fund, Social Insurance Fund, and Compulsory Medical Insurance Fund.

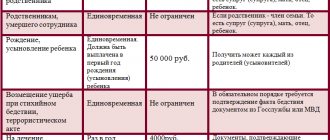

The list of payments accrued to an employee as financial assistance and exempt from insurance contributions is presented in the table below:

| No. | Basis for payment of financial assistance | Basis according to the Tax Code of the Russian Federation | Amount limit | Description |

| 1 | Birth of a child | Clause 3, clause 1, art. 422 Tax Code of the Russian Federation | Up to 50,000 rub. for each parent (adoptive parent) | If a local regulatory act of an organization provides for a one-time payment of financial assistance at the birth (adoption) of a child, then the amount of such payment is exempt from the calculation of insurance premiums, provided that the amount of financial assistance does not exceed 50,000 rubles. (for each parent/adoptive parent). |

| 2 | Death of a relative | Clause 3, clause 1, art. 422 Tax Code of the Russian Federation | No limits | Payment of financial assistance to an employee in connection with the death of a relative is not subject to contributions subject to death:

|

| 3 | Emergency | Clause 3, clause 1, art. 422 Tax Code of the Russian Federation | No limits | Some companies provide a one-time payment of financial assistance to employees affected by an emergency (fire, flood, accident, flooding, natural disaster). The amount of such payment is exempt from taxation by insurance premiums, regardless of the size. |

| 4 | Other grounds | Clause 11 clause 1 art. 422 Tax Code of the Russian Federation | Up to 4,000 rub. in year | When paying financial assistance for other reasons (for health improvement, in connection with vacation, wedding, etc.), an amount not exceeding 4,000 rubles is exempt from taxation with insurance contributions. during a year. |

The procedure for obtaining financial assistance in an organization

To receive money, the employee writes a free-form application. In some cases, he will have to prove his right to financial assistance of 4,000 rubles. (taxation 2021, insurance premiums) and provide relevant documents, such as a birth or death certificate, a certificate of accident, etc. Based on the application, the manager issues an order. Below are samples of documents that can be used when applying to an employer for financial assistance at the birth of a child.

Sample application for financial assistance

Sample order for financial assistance

Financial assistance in connection with the death of a relative

Insurance contributions for compulsory pension, medical insurance and VNIM are not charged for one-time financial assistance paid in connection with the death of an employee’s relative, if the deceased is a member of the employee’s family (spouse, parents, children, including adoptive parents and adopted children) (clause 3 clause 1 article 422 of the Tax Code of the Russian Federation). There are no restrictions on the amount of such financial assistance. The employee must provide a death certificate and documents confirming relationship with the deceased.

Financial assistance paid due to the death of other relatives should be subject to insurance premiums in accordance with the general procedure. But exceptions are possible here, provided that they actually lived with the employee and ran a joint household, that is, they can be classified as family members.

Financial assistance in tax accounting

In tax accounting, financial assistance is not reflected (clause 1 of article 252, clause 23 of article 270 of the Tax Code of the Russian Federation). The Ministry of Finance made only one exception. Material assistance can be taken into account in labor costs if it is provided for in the company’s internal personnel documents and is related to the performance of job duties (Letter No. 03-03-06/1/43912 dated 09/02/2014). An example is financial assistance for vacation.

Financial assistance accounting

Art. 129 of the Labor Code of the Russian Federation clearly distinguishes the payment of material assistance from labor costs, therefore financial assistance has no relation to the income tax base. It must be taken into account under other balance sheet items.

PBU 10/99 recommends using a credit to account 73 “Settlements with personnel for other operations” and a debit to account 91 “Other income and expenses” with the subaccount “Other expenses”.

If the payment of financial assistance is not subject to personal income tax, then both in the current and in future reporting periods in accounting for income tax expenses it will be recognized as a permanent difference, and in the debit of account 99 “Profits and losses” in correspondence with account 68 “Calculations for taxes and fees" will be taken into account as a permanent tax liability.

When making payments in favor of the employee’s relatives or other persons who are not subjects of labor relations, account 76 “Settlements with other debtors and creditors” is used in correspondence with account 91 “Other income and expenses”.

Financial assistance to low-income families in 2021

Financial assistance to low-income citizens of the Russian Federation is currently provided in several forms. The most common option is cash payments that the state makes monthly. In addition, there is one-time monetary assistance in the form of a grant for training, a scholarship, assistance for the purchase of basic necessities, assistance in kind (food, medicine, etc.). A low-income family may be exempt from paying all taxes and fees when calculating material assistance in the form of benefits and subsidies.

Children who are raised in a family with low-income status have the right to receive education in higher and secondary educational institutions, taking part in a general competition for applicants. They can also count on help from the state, but for this at least one of the following conditions must be met:

- if the child is raised by only one parent who is recognized as a disabled person of the second or first group;

- if a child from a low-income family has scored the minimum number of points based on the exam results, which allows him to take part in the competition, since the exams are considered to have been passed successfully;

- the age of the child who wishes to enter a higher education institution does not exceed 20 years.

There are a number of innovations specifically for children raised in low-income families:

- out of turn children must be admitted to educational preschool institutions;

- in schools, children must have two meals a day, which are paid for by the state;

- Children should receive both a uniform for school and clothing for sports free of charge;

- Children under 6 years of age can receive the necessary medications for free, but only with a doctor’s prescription.

Parents who are part of a low-income family can count on the following benefits:

- preferential employment;

- lowering the retirement age;

- exemption from paying registration fees;

- obtaining a garden or summer cottage plot out of turn;

- obtaining a mortgage loan on preferential terms.

Personal income tax

The subject of personal income tax taxation is the taxpayer’s income received both in cash and in kind (Article 209 and paragraph 1 of Article 210 of the Tax Code of the Russian Federation). The amount of financial assistance that is paid to a non-employee will be fully subject to personal income tax.

However, there are exceptions that are prescribed in Article 217 of the Tax Code of the Russian Federation, namely:

- Amounts of one-time financial assistance by employers to family members of a deceased former employee, a retired employee, or an employee, a retired former employee, in connection with the death of a member (members) of his family (clause 8 of Article 217 of the Tax Code of the Russian Federation)

- Amounts of financial assistance to former employees who resigned due to retirement due to disability or age in an amount that does not exceed 4,000 rubles (clause 28 of Article 217 of the Tax Code of the Russian Federation)

- Amounts of financial assistance paid to victims and members of their families from terrorist attacks on the territory of the Russian Federation, natural disasters or other emergency circumstances (clause 46 of Article 217 of the Tax Code of the Russian Federation)

Financial assistance for pensioners in 2021

Many pensioners are interested in the question of whether the government will repeat the one-time payment of 5,000 rubles, as it did in 2017. No, no such payment is planned. This was a single measure taken by the government in order to compensate for losses from rising prices.

From January 1, 2018, insurance pensions were indexed; the increase was 3.7 percent. In monetary terms, this is approximately 300-500 rubles.

Social pensions, received by those who do not have a single day of work experience (disabled people, disabled children, those who have lost their breadwinner, etc.), have increased by 4.1 percent since 04/01/2018. Depending on the disability group, this ranges from 175 to 500 rubles. Pensioners who are officially employed may not count on indexation in 2021.

Financial assistance: insurance premiums 2021

In 2021, the procedure for receiving financial assistance remains the same: the employee writes an application to the employer with a request to provide him with financial assistance, and also indicates the reasons why such a need arose. Documents confirming the circumstances that have arisen are attached to the application - these can be certificates from the relevant government services, birth certificates of children, death certificates, etc. Having decided to provide assistance, the employer must issue an order about this and indicate in it the amount due, as well as the payment period.

The list of types and amounts of financial assistance provided to employees must be contained in the collective agreement or other local document of the employer. An employer may provide for the possibility of financial support for its former employees, as well as employees who have retired due to age or disability.

To find out whether financial assistance is subject to insurance premiums, let’s turn to the legislative framework. There are only a few days left until the end of 2021, which means that Chapter 34 of the Tax Code of the Russian Federation on insurance premiums will begin to take effect very soon. At the same time, from January 1, 2017, Law No. 212-FZ of July 24, 2009 will cease to apply. Chapter 34 will bring virtually nothing new in terms of taxation of financial assistance contributions. Further in the text, references will be made to articles of both the current Law No. 212-FZ and the provisions of the Tax Code of the Russian Federation, which will regulate insurance premiums starting in 2021. With regard to insurance premiums for “injury”, the law of July 24, 1998 No. 125-FZ will continue to apply in 2021.

Financial assistance to large families in 2021

Today the state provides large families with:

- material support for the construction of a house;

- benefits for obtaining housing using social rent;

- land;

- subsidies for payment of utility bills;

- targeted benefits.

In the coming year, 2021, benefits will be provided as before. Assistance will be provided to each family subject to the same conditions:

- presentation of a certificate of large families issued by social security authorities;

- age of children (set separately by regions);

- if parents do not shirk their responsibilities.

Financial assistance to military personnel in 2021

Financial assistance to military personnel is accrued in the amount of their salary after submitting a report to the superior. If assistance is not received, it is accrued at the end of the year along with wages. The payment is issued based on the signing of the order by the commander. Financial assistance to military personnel is paid:

- when going on vacation;

- at the birth of a child;

- in case of wedding;

- in the event of the death of a relative;

- when the employee’s financial situation is difficult.

Financial assistance is calculated based on the following components on the 1st day of the last month of the year: monthly salary, taking into account military rank; monthly salary based on position.

Accounting for financial assistance

The reflection of financial assistance in accounting depends on whether it is stated in local documents.

If, for example, the payment of financial assistance is provided for by the Regulations on remuneration, then it should be accrued on the credit of account 70 “Settlements with personnel for remuneration”.

If financial assistance is paid at the request of the employee and is not provided for by the organization’s local regulations, then it must be accrued as a credit to account 73 “Settlements with personnel for other operations.”

When providing financial assistance to former employees or relatives of an employee, settlements with them are reflected in account 76 “Settlements with various debtors and creditors.”

The order for the provision of financial assistance must indicate the source of payment. If this is the profit of previous years, then the debit of account 84 “Retained profit (uncovered loss)” is used, if the current profit is the debit of account 91 “Other income and expenses” (sub-account “Other expenses”) or the debit of cost accounting accounts - 20, 26, 44 (if financial assistance is recognized as part of wages).

FAQ

Financial assistance 4000 rub. - income code in certificate 2-NDFL

Financial assistance paid in connection with the death of an employee or a member of his family is not subject to personal income tax, therefore, it does not need to be reflected in the 2-NDFL certificate.

Financial assistance paid for other reasons is reflected in 2-NDFL in full amount according to the codes:

- 2762 - at the birth of a child;

- 2760 - for treatment, anniversary, for other reasons.

At the same time, a deduction for financial assistance is indicated with the following codes:

- 508 - at the birth of a child (maximum 50,000 rubles);

- 503 - for other reasons (RUB 4,000).

Financial assistance 4000 rub. and income tax

Material assistance is not included in the enterprise’s expenses when calculating profit tax (clause 23, article 270 of the Tax Code of the Russian Federation). But insurance premiums calculated on the amount of financial assistance exceeding 4,000 rubles can be included in other expenses associated with production and sales (clauses 1, 45, clause 1, article 264 of the Tax Code of the Russian Federation)

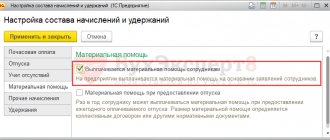

How to make postings in 1C 8.3

Financial assistance is reflected by the posting: Debit 91 Credit 73 (76). To reflect it in 1C 8.3 you need to:

1. Set up the additional accrual “Financial Assistance” in the “Salaries and Personnel Management” section.

2. Then, in the “Methods of reflecting wages in accounting” section, create a method for reflecting financial assistance and write down the corresponding entries.

3. Select the correct method of reflecting the previously created additional accrual on the “Accounting and UTII” tab.

Income code and deduction code in 2021

| Index | Code |

| Financial assistance at the birth of a child | 2762 |

| Financial assistance for treatment, anniversary, etc. | 2760 |

| Deduction for payment of financial aid at the birth of a child (RUB 50,000) | 508 |

| Deduction for payment of other financial assistance | 503 |

Financial assistance 4000 under the simplified tax system “Income minus expenses”

When applying the simplified tax system, financial assistance cannot be taken into account in expenses (clause 2 of article 346.16 of the Tax Code of the Russian Federation).

How many times a year can financial assistance be given in 4000

The number of financial assistance payments to one employee is not limited in any way. But you need to keep in mind that the deduction is only provided in the amount of 4,000 per year for all payments. For example: Ivanov I.I. financial assistance paid:

- in March - 2000 rubles;

- in June - 5,000 rubles;

- in August - 1000 rubles.

Material assistance paid in March will not be subject to personal income tax; in June, 3,000 rubles will need to be taxed. (that is, the balance of the annual deduction in the amount of 2000 rubles has been provided), and financial assistance in August will be taxed in full.

Financial assistance 4000 rub. in 6-personal income tax from 2021, tax-free

Financial assistance is reflected in 6-NDFL as follows:

| Basis for payment of financial assistance | The order of reflection in the report |

| Due to death | Not included in the report in full. |

| In connection with the birth of a child | In the non-taxable limit (up to 50,000 rubles), the Federal Tax Service allows it not to be reflected in the report (Letter dated December 15, 2016 No. BS-4-11/). But if you don’t want discrepancies with 2-NDFL certificates, then you can reflect it by analogy with other financial aid (see below). |

| Other financial assistance | In section 1: line 020 reflects all financial assistance (both taxable and non-taxable parts), line 030 - only the non-taxable part (deduction); in line 040 - the amount of calculated personal income tax. In section 2: in lines 100 and 110 - the date of payment; in line 120 - the next business day after payment; 130 - the amount of financial assistance together with personal income tax; in line 140 - the amount of tax withheld. If the entire amount of financial assistance is not subject to personal income tax, enter “0” in line 140. |

Financial assistance 4000 rub. when calculating sick leave

When calculating average earnings, only material assistance for which insurance premiums were calculated is taken into account. The following are not included in the calculation of the amount of financial assistance:

- in connection with death;

- in connection with the birth of a child in the amount of 50,000 rubles;

- financial assistance for other reasons in the amount of 4,000 rubles. for every year.

How to reflect receipt of financial assistance in tax reporting?

To understand how and when material assistance is reflected and whether it is subject to personal income tax, an example should be given.

Semenov Yu. G. officially contacted the employer on June 1, 19 with an application for payment of financial assistance in the amount of 50,000 rubles. The manager made a decision on June 4, 19 to transfer funds to the applicant in full. The accounting department made the appropriate accrual, transferred the money to the account and reflected the posting in the tax reporting.

Note: starting from 2021, a new form of certificate for personal income taxes (2-NDFL) is in effect. Using the old format is unacceptable.

Form 2-NDFL

To reflect financial assistance, personal income tax and insurance contributions, it is necessary to take into account that the amount of up to 4,000 rubles transferred to the employee’s account must have code 2760, and the deduction is shown as 503 (Article No. 217, paragraph No. 28 of the Tax Code of Russia). For financial assistance provided at the birth of a child, the income code will be 2762, the deduction will be 504 - order of the Federal Tax Service No. ММВ-7-11/387.

Non-taxable support, regardless of the volume, is not indicated in form 2-NDFL. For example, the amount does not need to be shown in the certificate issued to the employee if there is a fire in his house. However, the causes of the emergency should not relate to the actions of the employee. The payment is quoted as assistance in connection with the occurrence of emergency circumstances. In this situation, the payment is not subject to reflection, and therefore is not subject to tax.

Form 6-NDFL

Funds transferred as financial assistance are not subject to reflection if the grounds are specified in Appendix No. 2 to the Order of the Federal Tax Service No. ММВ-7-11/387. This is due to the fact that the bet size (line 040) is the difference between lines 020 and 030, multiplied by line 010 (bet). This equality is the main one and is established by the Control ratios during the analysis and conducting a desk audit.

Please note: submitting documents to receive a refund on previously paid personal income tax is allowed within 3 years.

Calculations should reflect the following types of support:

- Assistance that is completely free of mandatory fees. The payment is reflected in line 020.

- Full or partially tax-free assistance is indicated in line No. 020, and non-taxable funds are transferred to line 030 of form 6-NDFL.

In a situation where support is provided to an employee not with money, but with materials and products, then instead of accounts 70, 73 property will be indicated. In addition, due to the transfer of rights to goods free of charge, they are recognized as a sale. Therefore, VAT should be established on the position in accordance with Articles No. 146 (clause No. 1, paragraph 1), No. 154 (clause No. 2) of the Tax Code of the Russian Federation.

Read also:How to get an apartment for an orphan