Base

In accordance with the Labor Code of the Russian Federation (Article 183), as well as Federal Law No. 255 “On Compulsory Social Insurance” (Article 13), in the event of an employee’s illness, the employer is obliged to provide him with the opportunity to receive benefits for the entire period of his disability. Wherein:

- the first 3 days of illness are paid at the expense of the employer;

- the rest of the period is at the expense of the Social Insurance Fund.

The basis for receiving payments is sick leave.

Is sick leave subject to personal income tax?

Today, there are many reasons for applying for sick leave, for example, injury, illness, pregnancy and childbirth, as well as caring for a baby under 1.5 years old. In this case, the tax deduction is made depending on the cause of disability.

In fact, the cash payment for the employee’s illness period is his income. Based on this, existing tax rules, including personal income tax, should be applied to it. Despite this, such compensation does not apply to payroll, and therefore should not be taxed. However, they are still subject to income tax.

Judging by the Tax Code of the Russian Federation, monetary compensation for the time spent on sick leave is taxed in accordance with the general procedure. Personal income tax is deducted for the period of incapacity for work, based on a document that was issued due to:

- worker illnesses;

- illnesses of his children or dependents;

- quarantine for infections;

- industrial or domestic injury;

- the employee is in a hospital setting.

All cash payments for sick leave are accrued immediately after the accounting department receives the corresponding supporting document. According to Article 217 of the Tax Code of the Russian Federation, such payments are classified as income, in this regard:

- if sick leave is issued to a worker due to any illness, illness of children or dependents, then the employer pays all necessary tax fees by law from the monetary compensation received;

- if sick leave was received for pregnancy and childbirth, then taxes are not withheld from the funds accrued for it. When going on maternity leave, the employee is transferred 100% of her earnings for the entire time she will be waiting for the birth of the child;

- if sick leave is issued due to a worker being injured at work, then in this situation, payment for the period of absence from work will also not be subject to personal income tax and Social Security contributions. This is explained by the fact that the employee lost his ability to work due to the fault of the employer.

In addition, the accounting department must know that the amount of sick leave payments depends on the employee’s length of service. In this regard, the worker can be paid 60-100% of earnings for each day missed due to illness.

Sick leave issued during maternity leave is paid at 100%, regardless of the length of service of the pregnant woman.

Possible benefit reduction

The law defines 2 possible grounds for reducing the amount of disability benefits:

- If the insured person violates the regime assigned to him in a medical institution.

- If the patient avoids carrying out the medical social examination assigned to him or does not appear for mandatory medical examinations.

The benefit can also be greatly reduced if it is proven that the employee’s illness or injury was the result of alcohol abuse, the use of narcotic, toxic, or other illegal drugs.

Features of calculation and tariffs of insurance premiums for sick leave payments

Insurance contributions for sick leave payments recognized as the employee’s income are calculated in the usual manner for the employer. Article 426 of the Tax Code of the Russian Federation establishes the following rates for 2021:

- for compulsory pension insurance - 22% within the established limit and 10% if it is exceeded;

- for compulsory social insurance - 2.9% within the established limit (for foreign citizens and stateless persons - 1.8%);

- for compulsory health insurance – 5,1%.

The maximum values for calculating contributions are approved annually by the government of the Russian Federation. According to Decree No. 1378 dated November 15, 2017, in 2021 they are:

- for social insurance – 815 thousand rubles;

- for pension insurance – 1,021 thousand rubles.

Individual organizations, in accordance with the procedure provided for in Article 427 of the Tax Code of the Russian Federation, may apply reduced tariffs. The insurance premium rates applied by a particular employer may depend on the organizational and legal form, type of main activity, taxation system, and whether the organization or entrepreneur has licenses, permits or special status.

Insurance premiums are charged only on the amount recognized as income. For example, during the period of incapacity, the employer had to pay the employee 10 thousand rubles, but as a result of an error, 15 thousand were actually paid. Additionally, on his own initiative, the employer transferred another 3 thousand rubles to him.

In this case, insurance premiums must be calculated in the following amount: (15,000 + 3,000) – 10,000 = 8,000 rubles.

And the amount of contributions payable will be:

- for compulsory pension insurance – 8,000 rubles. * 0.22 = 1,769 rubles;

- for compulsory social insurance – 8,000 rubles. * 0.029 = 232 rubles;

- for compulsory health insurance – 8,000 rubles. * 0.051 = 41 rub.

Complete waiver of benefits

An employee may be denied benefits altogether if he has lost his ability to work intentionally. That is:

- independently caused harm to his health;

- there was a suicide attempt.

Also, a person will be deprived of payment if he received an injury/illness or injury while committing an illegal act or an intentional crime.

In the first and second cases, the basis for refusal or reduction of the payment amount is the establishment of a cause-and-effect relationship between:

- impartial actions of the patient;

- his actions, his intake of substances;

- the onset of illness or injury.

Deadline for granting benefits

After the employee submits sick leave to the accounting department of the enterprise where he is registered, disability benefits should be assigned to him no longer than 10 days.

The transfer of funds for this obligation is carried out on the nearest day when the enterprise usually pays wages to employees. An employee can receive the money due (at his choice, at the request of the recipient):

- through the post office;

- banking or credit organization;

- at the company's cash desk.

If the insured person does not apply for the payments assigned to him, then he can receive them in full upon subsequent application, but no more than 3 years after the date of the last assigned transaction. If the funds are not received by an individual due to the fault of third parties or, for example, an employer, then the statute of limitations in this case is not established by law.

Contributions levied by the employer

Taxation on sick leave in 2017-2018 is determined by the provisions of the Tax Code of the Russian Federation. Due to the fact that payments based on a document confirming incapacity for work are made by the employer, he must withhold income tax. Accordingly, the employee receives compensation, from which personal income tax has already been deducted.

Payment of sick leave to a part-time worker. Registration, calculation and amount of benefits

The organization pays only for the first 3 days of sick leave. The remaining days until recovery will be compensated by the Social Insurance Fund. This means that the tax is collected from the amount that is accrued to the employee for the first 3 days of his being on sick leave.

Taxes on sick leave compensation are calculated in the same way as they are levied on accrued wages.

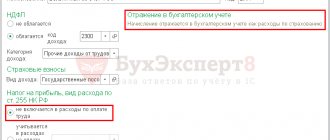

Personal income tax on sick leave is calculated at a rate that is 13%.

Attention! The employee can receive compensation under the document within 6 months. from the date of return to work after recovery, since the duration of sick leave is limited to the above period.

Term and date of withholding personal income tax from sick leave

From the beginning of 2021, the transfer of personal income tax from sick leave and vacation pay must be made no later than the last day of the month in which they were paid.

Personal income tax on temporary disability benefits

At the moment - in 2021 - funds received by the insured person as temporary disability benefits are not included in the list of income not subject to personal income tax. This provision is reflected in Article 217 of the Tax Code of the Russian Federation. This means that an employee on sick leave will receive a benefit amount already reduced by the amount of tax (personal income tax is usually 13%).

The employer - being a tax agent - is obliged to transfer the personal income tax withheld from the employee to the treasury no later than the end of the month in which the sickness benefit was issued. It doesn’t matter how the benefit was received – to a current account/in cash from the company’s cash register/to a salary card.

Cases when tax is not charged

According to the current legislation of the country, personal income tax is not taken from sick leave if it is issued to an employee in connection with pregnancy and childbirth . After submitting such a document and several certificates attached to it to the employer, the employee must receive full compensation within ten days, since these payments are not taxable.

There is also a special case when taxes are not levied on sick leave in 2021 - this is the adoption of a child. A certificate of temporary incapacity for work is issued upon adoption of a child under 3 months of age. for 70 days. The date of birth of the child will be considered the one indicated in the court decision. Personal income tax is not deducted from sick leave issued for such an occasion.

FSS pilot project

A special project has been launched in several corners of the Russian Federation since 2011. Its essence is that the tax agent of employees may not be the employer, but directly the Social Insurance Fund. Employers throughout the country are looking forward to its widespread implementation. After all, for them such an innovation means a reduction in responsibility and workload, and getting rid of the lion's share of routine reporting. In fact, their role in this matter is exclusively intermediary.

If this pilot project were adopted in all regions, employers would no longer have to worry about paying benefits or whether income tax is charged on certain payments.

At the beginning of 2021, 33 regions of Russia are already participating in the project. A complete list with the start dates of the FSS pilot project can be seen by reading the Decree of the Government of the Russian Federation No. 294 of 04/21/2011. Also see “Participants in the pilot project”

Deadlines for paying personal income tax on sick leave in 2021

The deadline for paying personal income tax when paying for an employee’s temporary disability will be the last day of the month during which sick leave was paid.

If, for example, sick leave was paid on April 10, then the deadline for paying personal income tax will be April 30 (adjusted for the production calendar in a given month, it is better to pay the tax on the last working day of the 28th). Moreover, even if you pay sick leave for an employee on the last day of the month, you will have to pay tax on the same day. But if you make a payment on the first day of the month, then you will have almost a full month ahead to pay personal income tax for this payment.

Naturally, since in most organizations sick leave is paid along with the payment of wages at the beginning of the month, it is not difficult for the accounting department and does not require excessive haste to pay the tax on time.

Where can I view data on accrued sickness benefits for an employee?

Certificate 2-NDFL contains the most complete information about all income of an individual and the tax paid on it. The amount of amounts paid to employees as disability benefits must also be reflected when filling out this certificate.

In 2021, the digital code for the type of income such as disability benefits in the 2-NDFL certificate remained the same - “2300”.

Also see “The Federal Tax Service of Russia has approved 5 new income codes and 1 deduction for the 2-NDFL certificate.”

Read also

24.04.2018

Insurance premiums from sick leave

When calculating disability benefits, the question arises: are insurance premiums paid on sick leave?

If the company pays benefits in the amount established by law, then this type of mandatory payment is not subject to payment (clause 1, clause 1, article 422 of the Tax Code of the Russian Federation). At the same time, benefits paid at the expense of the Social Insurance Fund and benefits paid for the first three days of illness at the expense of the enterprise are not taxed.

In addition, by the amount paid from the Social Insurance Fund, you can reduce the amount of contributions transferred to the budget for social insurance in connection with temporary disability and maternity.

If the company has established an additional payment for sick leave up to average earnings, then insurance premiums must be calculated from the amount of the additional payment and transferred to the budget.