Algorithm for calculating and paying personal income tax for individual entrepreneurs on OSNO

Note!

Since the beginning of 2021, the procedure for calculating personal income tax by entrepreneurs has changed. Previously, advance payments were calculated by specialists from the Federal Tax Service; now individual entrepreneurs must do this themselves.

Below is a step-by-step algorithm for calculating and paying personal income tax for individual entrepreneurs on the OSN, which was relevant until 2021:

- The individual entrepreneur received his first income of the year.

- Calculated the amount of estimated income for the whole year (minus expenses).

- Filled out and submitted the 4-NDFL declaration to the Federal Tax Service (with information about the expected income).

- I received notifications from the Federal Tax Service with the calculated amounts of advances for the payment of personal income tax.

- Paid advance payments on time (specified in notifications).

- At the end of the year, I compiled and submitted the 3-NDFL declaration.

- Paid or returned the tax calculated according to the 3-NDFL declaration.

Are there any penalties for paying taxes early?

Inspectors do not have the right to impose sanctions if personal income tax was transferred in advance. Auditors previously believed that since the amount was transferred in advance, it was not a tax. After all, the transfer is made not from the employee’s income, but from one’s own funds. Such actions are prohibited by clause 9 of Art. 226 NK.

If the company does not pay the debt on time, a fine is imposed. The amount of recovery is twenty percent of the amount of the debt.

When inspectors impose penalties, entrepreneurs protest. Disagreements between the parties are resolved in court. FAS NWZ took the side of the entrepreneur (resolution No. A56-16143/2013). The inspectorate cannot withhold the fine, since the company paid the tax, although it violated the deadlines.

When the personal income tax payment is made earlier than the due date, the company should not make repeated transfers. It is enough to correctly indicate the details in the payment document.

If disputes arise about the meaning of the prepayment made, payment documents will be useful. They will confirm that the company has indeed fulfilled its obligation. Therefore, there is no need to go through bureaucratic procedures to return funds and make payments again.

So, today the fiscal department answers negatively to the question of whether it is necessary to pay personal income tax on an advance payment. However, there are no penalties for early performance of duties.

Payment of personal income tax in 2020-2021

From the beginning of 2021, entrepreneurs must calculate their advance payments themselves. Therefore, you no longer need to file a 4-NDFL declaration.

— it’s cancelled.

At the end of the 1st, 2nd and 3rd quarters, the individual entrepreneur calculates the amount of the advance payment based on the revenue received, tax deductions and the personal income tax rate. He transfers the received amount to the budget.

At the end of the year, the individual entrepreneur calculates the tax for the year, taking into account the listed advances. He pays the amount received to the budget. If the personal income tax amount is less than the listed advances, the difference can be returned.

Deadlines for personal income tax payment

Advance payments are paid to individual entrepreneurs by the 25th day of the month following the end of the quarter. Taking into account the postponement of holidays in 2021, the dates are as follows:

- advance payment for the 1st quarter - until April 26;

- advance payment for half a year - until July 26;

- advance payment for 9 months - until October 25.

At the end of the year, the individual entrepreneur fills out a 3-NDFL declaration, in which he calculates the tax for additional payment (refund). It must be submitted no later than April 30. The additional tax amount must be paid by July 15.

The detailed procedure for calculating advance payments and annual tax can be found below (slider “Example of calculating advance payments and annual tax”

).

Deadlines for transferring personal income tax in the table

| Type of income | Deadline for transfer of personal income tax by tax agent | Based: |

| Salary for part of the month (advance) | Day of transfer of personal income tax from salary for the month (at final settlement) | clause 2 art. 223 Tax Code of the Russian Federation |

| Monthly salary, including incomplete salary upon dismissal (final payment) | No later than the next day after the actual payment of the amount of money | clause 2 art. 223 Tax Code of the Russian Federation; clause 6 art. 226 Tax Code of the Russian Federation |

| Vacation pay and sick pay | No later than the last day of the month in which vacation pay or disability benefits were paid | clause 6 art. 226 Tax Code of the Russian Federation |

| Payment in kind, material benefit, forgiven debt | No later than the next day after payment of income (if paid in kind, personal income tax is withheld from any other cash payments) | pp. 2 paragraph 1 article 223 of the Tax Code of the Russian Federation; clause 4 art. 226 Tax Code of the Russian Federation |

How is PFDL calculated in 2021 for individual entrepreneurs?

The tax for the year is calculated using the following formula:

Personal income tax = (Received income of an individual entrepreneur - Tax deductions) x Tax rate - Advance payments

Individual income received

To determine the personal income tax base, all income of an individual entrepreneur received by him in cash and in kind, in the form of material benefits, as well as when the right to this income arises, is taken into account. Income received both on the territory of the Russian Federation and abroad is subject to accounting.

An individual entrepreneur must determine the tax base separately for each type of income for which different tax rates are provided.

A complete list of income taken into account when calculating income tax is given in Art. 208 Tax Code of the Russian Federation.

Tax deductions

When calculating the amount of tax to be paid, an individual entrepreneur can use all types

tax deductions. The main deduction for individual entrepreneurs is professional and represents the possibility of accounting for all expenses incurred in the process of carrying out business activities.

Professional deductions can be provided in the amount of:

- Actual expenses incurred, if they are economically justified and documented;

- In the amount of 20% of all income received for the year, if there is no documentary evidence of expenses.

The composition of expenses is determined by the individual entrepreneur independently, in the manner prescribed by Chapter. 25 Tax Code of the Russian Federation.

Note

: It is beneficial to use a deduction in the amount of 20% of the income received when the documented amount of expenses incurred is less than the deduction provided in the amount of 20%.

In addition to professional ones, an individual entrepreneur can apply property, social, standard, investment and “loss” deductions. The procedure for their application is similar to that for ordinary citizens (that is, all necessary documents must be attached to the declaration).

Note:

deductions can be used to reduce income taxed at a rate of 13% (except for income from equity participation in an organization). Thus, if an individual entrepreneur is a non-resident, he will not be able to claim deductions (including professional ones).

From the beginning of 2021, an additional personal income tax rate of 15% (Law No. 372-FZ of November 23, 2021). It applies to individual entrepreneurs’ income exceeding 5 million rubles. You must pay tax at a rate of 15% on income exceeding 5 million rubles.

Tax rates

The basic tax rate for personal income tax for individual entrepreneurs is 13%

. It applies to the amount of income of an entrepreneur up to 5 million rubles inclusive.

For income exceeding 5 million rubles, the rate applies 15%

.

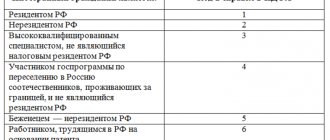

If an individual entrepreneur is a non-resident of the Russian Federation, he pays personal income tax at the rate 30%

.

A 15% rate applies to income over 5 million rubles. For example, if the tax base of an individual entrepreneur for 2021 is 6 million rubles, then in total he must pay: (5 million * 13%) + (1 million * 15%) = 800 thousand rubles.

A working entrepreneur must calculate tax based on his own actual income, without taking into account payments made to him by his employer. The Federal Tax Service will aggregate data from the 3-NDFL declaration (probably its form will change) submitted by the individual entrepreneur and the 2-NDFL certificate submitted by the employer. If the total amount of a citizen’s income exceeds 5 million rubles, the tax authority itself will calculate the additional personal income tax payment taking into account the increased rate and send a notification. This explanation was given by the head of the Department of Taxation of Personal Income and Administration of Insurance Contributions, Mikhail Sergeev, during the All-Russian Winter Online Business Congress “Taxes and Reporting in 2021”.

An example of calculating advances and taxes for the year

IP Ivanov I.I. uses OSNO. Let's calculate his tax for 2020.

For the 1st quarter of 2021, the individual entrepreneur earned income in the amount of 400,000 rubles. His advance payment will be: 400,000 x 13% = 52,000 rubles.

For 6 months, the income of the individual entrepreneur amounted to 700,000 rubles. He must pay: 700,000 x 13% - 52,000 = 39,000 rubles.

The amount of income for 9 months is 1,000,000 rubles. The advance payment will be: 1,000,000 x 13% - (52,000 + 39,000) = 39,000 rubles.

In just one year, IP Ivanov earned 1,200,000 rubles. Until April 30, 2021, he needs to submit a 3-NDFL declaration. His tax for the year will be 1,200,000 x 13% - (52,000 + 39,000 + 39,000) = 26,000 rubles. It must be paid by July 15, 2021.

General rules

The algorithm for withholding and transferring personal income tax from wages is given in Chapter 23 of the Tax Code.

It contains two concepts: “date of actual receipt of income” and “day of payment of income.” At first glance, it may seem that these are different formulations of the same event. But in reality we are talking about completely different things. The date of actual receipt of income, in fact, means the day when the final amount of income became known. It is at this moment that the taxable base can be formed and personal income tax can be calculated. In the case of wages, this moment is the last day of the month for which it was accrued (clause 2 of Article 223 of the Tax Code of the Russian Federation).

The income payment day is the date when money for salary or advance payment is debited from the current account or issued from the cash register. Each employer sets its own payment dates. Sometimes the advance is given on the 25th of the current month, and the salary is given on the 10th of the next month, sometimes the advance is given on the 15th, and the salary is on the 1st, etc.

The moment when the employer is obliged to withhold and transfer income tax to the budget depends on the date of payment of income. Thus, it is necessary to withhold personal income tax upon actual payment of money to an employee (clause 4 of Article 226 of the Tax Code of the Russian Federation). You must transfer money to the budget (with the exception of tax on vacation pay and sick leave) no later than the day following the day of payment (clause 6 of Article 226 of the Tax Code of the Russian Federation). From a literal reading of these norms, we can conclude that personal income tax should be withheld and transferred twice a month: from the advance payment and from the salary.

But officials have repeatedly explained: tax withholding and payment need to be made only once—at the final payment of wages for the month worked. This is explained by the fact that before the end of the month the date of actual receipt of income has not yet arrived. Consequently, the employer is not able to form a personal income tax base and calculate the amount of income tax. This will only be possible on the last day of the month. Therefore, there is no need to withhold and pay personal income tax on the advance payment. Such comments are contained, in particular, in the letter of the Federal Tax Service of Russia dated January 15, 2016 No. BS-4-11/320 (see “The Federal Tax Service reminded that personal income tax is not withheld from advances paid to employees”) and in the letter of the Ministry of Finance of Russia dated July 22, 2015 No. 03-04-06/42063 (see “Ministry of Finance: from an advance paid to an employee, personal income tax is withheld when paying the second part of the salary”).

Personal income tax reporting for individual entrepreneurs in 2021

Declaration 3-NDFL is submitted once a year until April 30. If this day falls on a weekend, it is moved to the next working day.

Declaration 3-NDFL for 2021 must be submitted to the tax authority before April 30, 2021

.

Declaration 3-NDFL for 2021 must be submitted to the tax authority before May 2, 2022

.

Information in the 3-NDFL declaration is entered in accordance with the KUDiR (book of income, expenses and business transactions), which individual entrepreneurs are required to maintain under the general taxation regime.

More details about the 3-NFDL declaration.

And in taxes - “advance”

Moreover, the tax in this situation must be calculated from the entire salary for this month, and not just from the amount of the “advance”, but withheld only in proportion to the “advance” paid (letter of the Ministry of Finance of Russia dated March 13, 1997 No. 04-04-06 ). The tax amount is determined taking into account the rounding rules established by clause 6 of Art. Tax Code of the Russian Federation.

Let's give an example. The company accrued wages in the amount of 32,389 rubles for the first half of September and paid them on September 30, 2017. Salaries for the second half of September were accrued in the amount of 20,611 rubles and paid on 10/14/2017. The employee does not have the right to deductions. As of September 30, 2017, the organization needs to calculate personal income tax on the entire salary for September: (32,389 rubles + 20,611 rubles) × 13% = 6,890 rubles. This amount must be withheld in proportion to payments, rounded according to the general rules (up to 50 kopecks are discarded, 50 or more are rounded up to the full ruble). Therefore, if paid on September 30, 2017, 4,211 rubles will be withheld (with a transfer deadline of 10/02/2017), and if paid on 10/14/2017 - 2,679 rubles with a transfer deadline of 10/16/2017.

Reflection of the advance in form 6-NDFL

In the new form of the 6-NDFL report, reflection of the advance payment is not provided for by the filling rules. Earnings at the end of the month are indicated in section 2 of the form, indicating the date of payment of income to staff. All calculations are entered into the report as a total amount. The personal income tax payment deadline in the report must comply with tax legislation.

If income was paid to employees only in the first part of the month (as an advance), then the amount of payment is recognized as income in terms of wages on the last day of the month for which the calculation is made. The amount of personal income tax, which is calculated from income, but is not withheld because Tax is not withheld from the advance payment; you will need to deduct it from the employee’s next salary payment.

In such a situation, settlements with personnel are reflected in Form 6-NDFL as follows:

- an advance that is recognized as wage income is reflected in the total amount of income received;

- tax withholding date – taking into account the actual personal income tax withheld.

Important! When checking the report, tax officials may recognize untimely withholding of income tax.

An explanatory note to the report on Form 6-NDFL will help protect the company from quibbles and fiscal sanctions from tax authorities. It should indicate the reason for such a discrepancy in the timing of income payment and tax withholding.