01.07.2019

0

322

4 min.

Paying taxes is an obligation that applies to every employed member of society. The existing system of collecting fees is a product of gratuitous contributions by individuals and organizations to ensure the functionality of the state, municipalities and the maintenance of disabled categories of citizens. Employees who decide to quit often ask their employer the question: is compensation for vacation subject to an insurance premium or not?

For officially employed people, the employer automatically makes monthly contributions to the inspectorate. Taxable income includes salary, bonuses and vacation payments, work on holidays and overtime, sick leave, compensation for unused vacation upon dismissal.

What payments are due upon dismissal?

The Labor Code of the Russian Federation establishes three ways to terminate employment contracts: at the request of the employee, at the initiative of the employer and by agreement of the parties. For each of them, the manager is obliged to transfer the following payments to the resigning person no later than the last working day:

- compensation for unused vacation;

- salary for the period worked.

If the dismissal is due to staff reduction, severance pay is transferred. It may also be provided for by agreement of the parties.

If the dismissed person was in the position of a manager, his deputy or chief accountant, he is also entitled to compensation payments.

Is compensation for unused vacation upon dismissal subject to personal income tax?

The amounts due to employees upon termination of an employment contract, paid for unused vacation rights, are not considered as compensation not subject to personal income tax (clause 3 of Article 217 of the Tax Code of the Russian Federation). Compensation for unused vacation upon dismissal is subject to personal income tax.

In addition to unused vacations, there are a number of compensation payments, in connection with which questions often arise: should personal income tax be calculated on them?

Art. 217 of the Tax Code of the Russian Federation contains a whole list of compensation payments that are not subject to taxation. However, the provisions of the Tax Code cannot always be interpreted unambiguously. For example, should you be taxed on your employees' compensation for child care expenses?

The answer to this question can be found in the material “Payment for kindergarten - taxable income of an employee .

Read the point of view of officials and experts on this issue in the article “Is compensation for part of the parental payment for the maintenance of a child in kindergarten that the employer paid to its employees subject to compensation?”

To ensure that the inspection authorities do not have any claims regarding the non-accrual of personal income tax on compensation payments, comply with legal requirements and draw up legally competent contracts and agreements with employees.

You can learn more about these nuances from the material “What needs to be done in order not to impose personal income tax on compensation for “official” use of personal property .

The publications posted on our website will introduce you to the nuances of personal income tax assessment of various types of compensation:

- “Travel” compensations are not subject to personal income tax and contributions and reduce profits”;

- “Personal income tax on housing payments - when you don’t need to pay”;

- “An employee has been recalled from vacation: should I pay personal income tax on travel to work and back to the place of rest?”

Other payments to employees, whether compensatory or otherwise in the performance of their official duties, may or may not be subject to taxation, depending on the specific situation.

More details about the opinions of officials on some situations can be found in the following materials:

- “Allowances for work in special climatic conditions are not compensation and are subject to personal income tax”;

- “The Ministry of Finance has named the condition for exemption from personal income tax for financial assistance to an employee in connection with a fire”.

From what payments is personal income tax withheld upon dismissal?

Personal income tax stands for personal income tax. They are subject to most of the payments, including compensation upon dismissal. For residents of the Russian Federation, its value is 13%, for non-residents – 30%.

Compensation for unused vacation is transferred regardless of the reason for the employment contract. Taxation of personal income tax is a priority: only after the tax has been calculated, alimony and other payments are withheld from the amount received.

Personal income tax is also transferred from the following income:

- salary, bonuses, allowances;

- temporary disability benefits.

The employing organization is a tax agent, therefore the obligation to transfer personal income tax rests with it. Violation of this rule is subject to administrative liability in the form of a fine, so it is very important to comply with the deadlines and procedure for calculating the tax.

Answers to common questions

Question No. 1 : Do I need to pay compensation for unused vacation to an external part-time worker?

Answer : All employees, including external part-time workers, must be provided with payment for unused vacation, since guarantees and compensation, according to the Labor Code of the Russian Federation, for any part-time workers are provided in the same amount as for main employees.

Question No. 2 : Is it possible to forgive an employee for overpaid vacation pay and what to do with overpaid personal income tax?

Answer : The organization may not issue a refund of vacation pay, that is, overpayments may not be taken into account in favor of the employee. But at the same time, vacation pay is the employee’s income and no question of any personal income tax refund should arise.

Income not subject to taxation

The list of income from which personal income tax is not withheld is determined by Art. 217 Tax Code of the Russian Federation. This includes the following:

- monthly payments in connection with the birth of children;

- compensation for harm to health;

- payment of allowances in kind;

- severance pay not exceeding three times the average monthly salary, for residents of the North - six times the amount;

- daily allowance up to 700 rubles. while on a business trip.

Expert commentary

Kamensky Yuri

Lawyer

Thus, if on the date of dismissal an employee is due to receive compensation for vacation time and severance pay, these payments will not be taxed. If an employee terminates an employment contract during illness, temporary disability benefits are paid no later than 10 days from the date of receipt of sick leave, while the tax is withheld on the day the benefits are transferred and paid to the Federal Tax Service no later than the last day of the month.

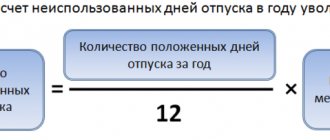

How is compensation for unused vacation calculated?

The minimum duration of annual paid leave for citizens working under employment contracts is 28 calendar days. For some categories of persons, additional days of rest are provided.

How compensation is calculated:

- The number of days of non-vacation is established. To do this, the personnel officer determines the product of the number of days of rest due to the employee for each month worked and subtracts the days already used.

- The resulting number of vacation days is multiplied by the citizen’s average daily earnings.

For example, if a quitter is entitled to 14 days of vacation, and the average daily earnings are 1,500 rubles, the calculation will be carried out as follows: 14 x 1,500 = 21,000 rubles. – the total amount from which personal income tax will be withheld.

21,000 x 13% = 2,730 rub. – personal income tax amount.

21,000 – 2,730 = 18,270 rubles. - the total is in the hands of the employee.

18,270 x 22% = 4,019.4 rubles. – the amount of contribution to the insurance part of the pension paid by the employer.

18,270 x 5.1% = 931.77 rubles. – the amount of payment to the Compulsory Medical Insurance Fund from the employer’s funds.

Compensation code for unused vacation in certificate 2-NDFL

Previously, code 4800 was used to indicate the income of an individual when he received vacation pay compensation upon dismissal.

Such clarifications were given by the Federal Tax Service in its letters dated 08.08.2008 No. 3-5-04/ [email protected] and dated 16.08.2017 No. ZN-4-11/ [email protected]

The Federal Tax Service issued an order dated October 24, 2017 No. ММВ-7-11/ [email protected] , on the basis of which changes are made to Appendix No. 1 of the order dated September 10, 2015 No. ММВ-7-11/ [email protected] From the moment of entry into force By virtue of this order, income code 2013 is used to compensate for unused vacation.

| Before the changes come into force | After the changes come into force (in 2021) |

| Income code for compensation for unused vacation |

Is it necessary to retroactively allocate vacation compensation upon dismissal to a separate income code for personal income tax in 2021?

There is no need to apply the new code retroactively. At the same time, it should be borne in mind that for each certificate with incorrect codes, the tax agent may be fined 500 rubles. This amount of sanctions is established in Art. 126.1 Tax Code of the Russian Federation.

Where is the income code indicated for compensation upon dismissal in the 2-NDFL certificate in 2021?

The procedure for filling out the 2-NDFL certificate, as well as the form itself, has changed since January 1, 2021. The Simplified 24/7 program has a current form where you can see a sample of filling out the income code for compensation.

To compensate for unused vacation upon dismissal in 2019, at what point is the personal income tax code set according to the new rules?

Order No. ММВ-7-11/ [email protected] came into force. New codes are valid when indicated in 2-NDFL certificates for 2021 and beyond.

If vacation compensation is paid without dismissal, what is the income code?

An employee may ask to be paid part of his vacation pay without actually going on vacation and without being fired. The employer has the right (but is not obligated) to satisfy such a request. But compensation for vacation days is allowed only when we are talking about days in excess of 28 standard vacation days. This may be additional leave due to special working conditions, extended main leave, etc.

How to withhold personal income tax from compensation upon dismissal: step-by-step instructions

To understand this issue, you must first study the features of the dismissal procedure:

- The employee submits his resignation. If necessary, the employer has the right to assign mandatory work of 2 weeks.

- The manager issues a dismissal order indicating a specific date. The person leaving gets acquainted with it against signature, then the document is transferred to the personnel department and accounting department. It is the accountant who makes all the deductions, but this can only be done if there is a reason - an order.

- The accountant calculates wages, compensation for unused vacation and other payments minus personal income tax, contributions to the Social Insurance Fund and pension contributions.

- On the last working day, the employee is transferred or given cash. He must also be issued with education documents, a salary certificate, 2-NDFL, and information about the status of his personal account with the Pension Fund.

Important! All charges must be reflected in the documentation. The accountant deals with them, and he also draws up the postings.

Let's sum it up

Compensation for unused vacation is due to employees who have worked for a long time without rest or who quit their current place of work, while many other circumstances are important that make receiving this compensation possible. In both cases, the deduction of personal income tax will be handled by the employing organization, so employees have nothing to worry about. Companies must have accountants on staff who have a decent level of knowledge so that they carry out the transfer operation correctly, making accounting entries in the required sequence.

Some categories of citizens cannot qualify for compensation funds

Transfer deadline

The deadline for transferring tax to the budget depends on the method of receiving compensation:

| Cash in the bank | No later than the day of issue |

| To the employee's bank account (non-cash transfer) | No later than the day of transfer |

| Cash from the company's cash desk | No later than the day following the date of issue |

Important! If compensation is paid not upon dismissal, but during the citizen’s work, it must be transferred on payday. Payment according to the Labor Code of the Russian Federation is made every 15 calendar days. If the payment date falls on a weekend, the money must be transferred on the previous weekday.

For example, when an organization pays salaries on the 15th and the date falls on a Sunday, the money must be issued on Friday.

Transfer of funds on the next business day is not allowed, because this will already be considered a delay in wages, and the employer undertakes to pay a penalty for each day of delay.

Deadline for paying personal income tax on salary upon dismissal

All tax accrued on payments upon termination of an employment contract must be paid no later than the day following the date of their actual transfer to the employee (clause 6 of Article 226 of the Tax Code of the Russian Federation). When the deadline for transferring tax upon dismissal coincides with a day off, settlements with the budget for personal income tax are made on the next working day (Clause 7, Article 6.1 of the Tax Code of the Russian Federation).

Important

Although now almost all companies pay salaries by bank transfer, and making payments on the day of dismissal is not a problem, there are situations when the date of separation and receipt of money do not coincide. For example, small organizations may issue wages through a cash register, but the employee does not show up to collect the money on the last working day. Then the company is obliged to make payments no later than the next day after the date the dismissed person applied for the debt (Article 140 of the Labor Code of the Russian Federation).

Example 1

The company pays employees wages through a cash register. The employee resigns on 08/20/20__. However, he did not show up for the payment and brought a statement demanding its issuance only on 09/02/20__. The company, in compliance with the law, made a full settlement with him on 09/03/20__. When should she remit personal income tax?

Decision: based on the above provisions of paragraph 6 of Art. 226 of the Tax Code of the Russian Federation - no later than 09/04/20__.

Calculation and accounting entries

As mentioned earlier, the tax rate on employment contracts for residents of the Russian Federation is 13%. Non-residents are subject to an increased tax of 30%. If citizens have applied for tax deductions or other social benefits, they must be deducted from their salaries, and personal income tax will be withheld from the final amount.

Let's look at practical examples:

A citizen has been working at the company for 3 years. Previously, he received a tax deduction, according to which 1,000 rubles are deducted from the tax amount every month. In May 2021, he decided to quit. The salary for the period worked was 30,000 rubles, compensation for several days of unused vacation was 15,000 rubles. In total, an amount of 45,000 rubles is used to calculate personal income tax and other contributions. How personal income tax is calculated:

45,000 x 13% = 5,850 rub.

After withholding personal income tax, 39,150 rubles remain. Insurance premiums and payments to the Compulsory Medical Insurance Fund must be paid from this amount. They are transferred by the employer from the enterprise budget.

39,150 x 22% = 8,613 rubles. – the amount of contributions to pension insurance.

39,150 x 5.1% = 1,996.65 rubles. – payment to the Compulsory Medical Insurance Fund.

The second example is the payment of state contributions for a non-resident of the Russian Federation:

A foreign citizen works at the enterprise for 2 months, i.e. less than 183 days. This alone does not give him the right to be considered a resident. The decision to resign was made by him in November 2021. He does not yet have the right to leave, so no compensation will be paid. Only wages for the period worked are subject to transfer. In a month, a citizen earned 50,000 rubles. From this money, the employer must withhold 30% of personal income tax - the tax is paid from the employee’s funds. Also, 22% is withheld for the insurance part of the pension, and 5.1% for the Compulsory Medical Insurance Fund. The last two payments are made from the organization's budget.

50,000 x 30% = 15,000 rub.

50,000 – 15,000 = 35,000 rub. – the foreigner finally received it.

35,000 x 22% = 7,700 rub. – transferred by the company towards pension contributions.

35,000 x 5.1% = 1,785 rubles. – the amount of contributions to the Compulsory Medical Insurance Fund.

Accounting entries

In the postings, the accountant reflects all payments as follows:

| DT 44 Kt 70 “F.I.O. employee" | Payroll |

| DT 70 (full name of the employee) Kt 68 Personal Income Tax | Tax withholding |

| DT 70 (full name of employee) Kt 50 (51) | Issuance of wages |

| DT 68 Personal income tax Kt 51 | Transfer of tax to the budget |

Responsibility for non-payment of personal income tax

The employing organization is a tax agent, and the obligation to remit personal income tax rests entirely with it.

The agent's responsibility for untimely transfer is assigned to Art. 123 Tax Code of the Russian Federation. It all depends on the specific situation:

| The tax was withheld from the employee, but was not transferred to the budget | Arrears of 20% of the unpaid amount will be charged. An additional penalty will be charged for each day of delay. |

| The tax is not transferred to the budget and is not withheld | According to the Tax Code of the Russian Federation, personal income tax is always withheld only from employee salaries. Collection of tax from the employer for personnel is not allowed (clause 9 of Article 226 of the Tax Code of the Russian Federation). If the arrears cannot be recovered, no penalty will be charged. |

When compensation is not taxable

In all cases, compensation for unused vacation is subject to taxation. The exception is when relatives of a deceased employee apply for it: in such a situation, there is no need to withhold personal income tax.

To receive compensation and other salary payments for a deceased relative, you must do the following:

- Guided by Art. 141 of the Labor Code of the Russian Federation, according to which relatives of the deceased employee are entitled to payments, draw up an application and collect the necessary package of documents for the employer. This must be done within 4 months from the date of death of the citizen.

- Submit a package of documentation to the organization. Money must be transferred no later than 1 week from the date of application.

Along with the application, the employer is provided with a death certificate, passport and a document confirming the relationship of the citizen with the deceased employee.

Important! If wages are paid into staff bank accounts, the employer must not transfer funds upon learning of the employee's death, otherwise it will no longer be considered a legal payment. The money must be given to close relatives. If they do not apply within 4 months, the amount is included in the inheritance mass, and only the heirs can apply for it after six months.

In addition to compensation for unpaid vacation, the employer must give relatives the amount of salary for the period worked, as well as other payments due to the employee during his lifetime. There are no taxes or insurance contributions, since a citizen’s tax obligations cease due to death.

Compensation for unused vacation and other payments upon dismissal are subject to personal income tax without fail, with the exception of the death of the employee: in this case, his relatives receive the amount without withholding tax.

If personal income tax is not paid on time, the tax agent may oblige the Federal Tax Service to pay arrears and penalties, so it is very important to comply with the deadlines for the transfer and know the specifics of accounting entries.

When is it held?

An employer faces personal income tax compensation in two cases:

- when replacing additional vacation days with cash payments during work;

- upon dismissal - details of accrual here.

You need to withhold 13% to transfer them to the budget directly when paying compensation to the employee - on the day the cash is issued at the cash desk or on the day it is transferred to the card.

Upon dismissal, this is the employee’s last day of work, when full payment is made to him.

There is no need to impose personal income tax on vacation compensation if it is paid to a relative of a deceased employee.

If an employee dies, the employment contract with him is terminated, and all due payments upon dismissal are transferred to relatives, including compensation for unused vacation.