After the repeal of Law No. 212-FZ dated July 24, 2009, most policyholders have questions about how to transfer insurance premiums in 2021. Now the procedure for calculation, payment, terms and rates is regulated by the new 34th chapter of the Tax Code. The changes affected compulsory pension and medical coverage (CPS, compulsory medical insurance), as well as contributions in case of temporary disability and in connection with maternity (VNiM).

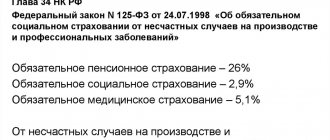

Insurance against accidents and occupational diseases should be paid according to the old rules (Law No. 125-FZ of July 24, 1998), that is, funds should be transferred to the Social Insurance Fund. Moreover, payments must be transferred to the Social Insurance Fund in pennies. Rounding to whole numbers is not required.

What changed

In 2017, the administration of insurance premiums from wages was transferred to the Federal Tax Service. This means that tax authorities:

- control the timeliness and completeness of insurance transfers;

- accept and verify reports on insurance premiums for employees in 2021;

- collect arrears and penalties, issue fines.

Payment of contributions in 2021 goes to the territorial offices of the Federal Tax Service. Read more in the article about who should now pay insurance premiums.

The Pension Fund and the Social Insurance Fund have the right to check past periods (until December 31, 2016), but last year’s debt on insurance contributions to the Pension Fund in 2021 does not need to be transferred. We pay debts using the new KBK.

It's time to pay your dues for 2021: a few tips

Good afternoon, dear individual entrepreneurs!

A traditional note that I write at the end of every year.

After the New Year, questions constantly appear in the comments from those who remembered about contributions only after the holidays were over =)

Therefore, just in case, I remind you once again in the form of a summary article with references to materials that I published earlier.

So, the most important thing:

By what date are dues due for 2021 due?

Fixed contributions of individual entrepreneurs “for themselves” for 2021 must be paid by December 31, 2021. But taking into account the fact that December 31 is a day off, the payment deadline is postponed to January 9, 2019.

But I strongly recommend not to delay payment until the very last day of December (and especially until January 9, 2021). It is better to pay now, without waiting for the deadline.

For example, if an individual entrepreneur using the simplified tax system pays contributions for 2021 in January 2019, then he will only be able to deduct them from the tax under the simplified tax system for 2019. Please take this into account.

How much do you need to pay for 2021?

- Contributions to the Pension Fund for oneself (for pension insurance): 26,545 rubles

- Contributions to the FFOMS for yourself (for health insurance): 5840 rubles

- Total for the full year 2021 = 32,385 rubles

- Also, do not forget about 1% of the amount exceeding 300,000 rubles of annual income

I remind you that you can subscribe to my video channel on Youtube using this link:

https://www.youtube.com/c/DmitryRobionek

I’ll immediately answer a very common question from newbies.

If you work as an individual entrepreneur for less than a full year, then contributions are recalculated taking into account the date of registration as an individual entrepreneur. That is, you will have to pay less for the full year 2021.

But I’ll tell you more about this below.

The full article + scheme about contributions for 2018 is here. Everything is told and shown in it; I see no point in repeating it.

Until what date do you need to pay 1% of the amount exceeding 300,000 rubles of annual income for 2021?

Individual entrepreneurs who have an annual income of more than 300,000 rubles know that they need to pay 1% of the amount that exceeds 300,000 rubles.

This 1% must be paid for compulsory pension insurance.

In 2021, a new law was adopted, according to which the date for payment of 1% of the amount exceeding 300 thousand rubles of annual income is postponed from April 1 to July 1. More details here.

It is clear that many individual entrepreneurs pay 1% throughout the year. But the deadline for paying 1% for 2021 is July 1, 2021.

If your income for 2021 is less than 300,000 rubles, then you do not need to pay 1% for pension insurance.

Yes, another important point for individual entrepreneurs using the simplified tax system “income minus expenses”.

I know that there are several decisions of the Supreme Court, when specific individual entrepreneurs on the simplified tax system “income minus expenses” were allowed to take into account expenses when calculating the 1% contribution to pension insurance.

But no changes were made to the Tax Code (let me remind you that we pay insurance premiums “for ourselves” to the Federal Tax Service, and not to the Pension Fund of the Russian Federation, as was previously the case). There were also many letters from the Ministry of Finance and the Federal Tax Service, in which these departments adhered to the previous position: an individual entrepreneur using the simplified tax system cannot take into account expenses when calculating the 1% additional contribution to the Pension Fund.

Read more in the letters:

- Letter of the Ministry of Finance dated 06/09/2017 No. 03-15-05/36277

- Letter of the Ministry of Finance dated March 17, 2021 N 03-15-06/15590

- Letter of the Ministry of Finance No. 03-15-03/69372 dated 10/23/2017

- Letter of the Ministry of Finance No. 03-15-07/8369

- Letter of the Ministry of Finance dated May 3, 2021 N 03-15-05/29955

- Letter of the Federal Tax Service dated July 25, 2018 No. BS-3-11/ [email protected]

All these letters are easy to find through Yandex or Google.

How to pay if there is no accounting program? Where can I get receipts or payment orders?

Just don’t download forms “from the Internet”, as is often the case =)

Use the official Federal Tax Service “Pay Taxes” service using this link:

https://service.nalog.ru/payment/index.html

If you use it, then KBK must be entered WITHOUT spaces. It’s even better to use accounting programs and services, which I constantly write about on my blog.

Now is not the time to keep records completely manually. Changes happen too often and are easy to miss.

How to calculate contributions if an individual entrepreneur has worked for less than a full year?

A very common situation is when an individual entrepreneur has been working for the first year, but opened, say, in the summer. How to calculate contributions “for yourself”?

The most reasonable option is to use accounting programs and services that calculate contributions taking into account the date of registration as an individual entrepreneur.

Or read this article, where I talked about the algorithm for calculating contributions in such cases:

A frequent question from individual entrepreneurs: how to calculate mandatory contributions “for yourself” if you have only worked for less than a year?

Just keep in mind that in this article I spoke using the example of 2017.

You can estimate your contributions in my “for yourself” contribution calculator for 2018:

Calculator of fixed contributions for individual entrepreneurs “for themselves” for 2021

And for 2021 there is already a calculator, by the way:

Calculator of fixed contributions for individual entrepreneurs “for themselves” for 2019

Which KBK should I pay for?

- For pension insurance “for yourself” 182 1 02 02140 06 1110 160

- For medical insurance “for yourself” 182 1 02 02103 08 1013 160

- At the end of 2021, for 1% of the amount exceeding 300,000, a separate BCC is not provided and it coincides with the BCC for pension insurance contributions.

PS By the way, it is possible that in 2021 there will finally be a separate KBK for the 1%. They already tried to introduce it in February 2021, but quickly abandoned this idea, since many individual entrepreneurs paid fees for the “old” BCC. Follow the news, update your accounting programs.

That's all for today.

Pay on time, don't look for trouble out of the blue =)

Important. Please note that starting from February 4, 2021, the details for paying taxes and contributions in 26 regions of the Russian Federation will change. Please read here: I recommend checking your details with your tax office after this date, as well as updating your accounting programs.

Dear entrepreneurs!

A new e-book on taxes and insurance contributions for individual entrepreneurs on the simplified tax system of 6% without employees is ready for 2021:

“What taxes and insurance premiums does an individual entrepreneur pay under the simplified tax system of 6% without employees in 2021?”

The book covers:

- Questions about how, how much and when to pay taxes and insurance premiums in 2021?

- Examples for calculating taxes and insurance premiums “for yourself”

- A calendar of payments for taxes and insurance premiums is provided

- Frequent mistakes and answers to many other questions!

Find out the details!

Dear readers, a new e-book for individual entrepreneurs is ready for 2021:

“Individual Entrepreneurs on the simplified tax system 6% WITHOUT Income and Employees: What Taxes and Insurance Contributions must be paid in 2021?”

This is an e-book for individual entrepreneurs on the simplified tax system of 6% without employees who have NO income in 2021. Written based on numerous questions from individual entrepreneurs who have zero income and do not know how, where and how much to pay taxes and insurance premiums.

Find out the details!

How to pay insurance premiums in 2021: changes

The calculation procedure has not been changed (Article 52 of the Tax Code of the Russian Federation): as in the previous calendar period, the tax base is multiplied by the established tariff. The procedure for determining the taxable base is now established by Art. 420 - 421 Tax Code of the Russian Federation. Insurance payments, which should not be included in the base for calculating SV, are enshrined in Art. 422 of the Tax Code of the Russian Federation. In comparison with the norms of Law No. 212-FZ, the list of insurance payments has been modified in terms of daily allowances, payments to guardians and employer payments for voluntary social security.

The rate or tariff is set in accordance with Art. 425 - 429 Tax Code of the Russian Federation. A number of preferential categories of policyholders have been established who have the right to make payments on insurance premiums in 2021 at reduced rates.

The procedure for paying insurance premiums in 2021 is enshrined in Article 431 of the Tax Code of the Russian Federation. Key points:

- The policyholder is obliged to settle payments by the 15th day of the month following the reporting month. That is, for August the SV should be transferred by September 15th.

- Transfers are made by type of insurance coverage (compulsory insurance, compulsory medical insurance, VNIM).

- When paying VNIM, a new procedure for offsetting employer expenses applies (Part 2 of Letter of the Federal Tax Service of Russia dated 02/01/2017 No. BS-4-11/2748). Participants in the pilot project do not offset expenses when paying for VNIM.

Overpayment of accident insurance premiums

Currently the Social Insurance Fund rate is 2.9%. But, in addition to the regular transfer of this amount, a Pension Fund contribution of 22% is also deducted from each employee’s income. A regular payment to the Compulsory Medical Insurance Fund is added to these contributions. The amount transferred to it should be 5.1% of the employee’s total income. When calculating all fees, it turns out that the organization is obliged to transfer 30% of the income paid to the employee.

The percentage calculated by the Social Insurance Fund must be transferred to the fund not by the employee himself, but by the organization where he works.

Depending on the situation, the amount accrued by the fund will have a specific value.

Reimbursement of expenses received from Social Insurance is necessarily reflected in the calculation of insurance premiums, which is submitted to the tax office.

The amounts should fall into line 080 of Appendix No. 2 of the report form. The data is filled in monthly and on a cumulative basis.

We discussed the nuances of filling out the report in the article New reasons why tax authorities will stop calculating contributions in 2018.

When filling out the ERSV report, you can pay attention to line 001 of Appendix No. 2 of the reporting form. This line implies an indication of which method is used to reimburse social security expenses - direct payments or an offset system.

Most policyholders use an offset system. Direct payments can only be used by those legal entities or entrepreneurs that are registered in the regions where the FSS pilot project operates. In this case, benefits are paid directly to employees based on documents submitted by the employer to Social Security.

In 2021, the list of participants in the Social Insurance pilot project includes 33 regions of Russia.

Since with direct payments, accrued insurance premiums cannot be reduced by the amount of benefits paid, they are not reflected in the ERSV report.

Clause 1.1 art. 78 of the Tax Code of the Russian Federation indicates that it is impossible to offset the overpayment of one contribution (that is, one BCC) against the payment of other contributions or taxes (that is, other BCCs).

One of the previous sections already contains an application form for the return of overpayments on disability insurance premiums as of 01/01/2017.

There is no need to attach any documents to the application.

The specific list depends on the type of benefit being reimbursed.

But the period for transferring funds by Social Insurance is strictly limited by law. The FSS is obliged to return the money before the expiration of 10 days from the date of receipt of the application. However, if an inspection is ordered, the period is extended.

Contributions for accidents are paid directly to Social Security, so there are no difficulties in this case. An application for the return of overpaid contributions is submitted to its branch of the Fund, and the Fund transfers the payment within 10 days.

The return of funds from the Social Insurance Fund for any reason (overpayment or reimbursement of expenses) is not considered income under any tax regime.

But you should pay attention to whether payments for social benefits were accidentally included earlier in expenses for tax purposes and whether they reduced the single tax under the simplified tax system of 6% or under other taxation systems.

Transfer of insurance premiums in 2021: with or without kopecks

Any innovations provoke a large number of questions from accounting workers. Thus, the debate over how to round up insurance premiums in 2021 continues to this day.

To eliminate errors in calculations and prevent penalties from regulatory authorities, we will determine the answer to the pressing question: how to pay insurance premiums: with or without pennies in 2021.

So, based on Art. 431 of the Tax Code of the Russian Federation, we can affirmatively state that disputes about how insurance premiums are paid (with or without kopecks in 2020) are absolutely groundless. Paragraph 5 of this article gives a comprehensive answer: we pay in rubles if the amount is “round”, and in rubles and kopecks if the amount is a fraction.

Consequently, the payment of insurance premiums (with or without kopecks in 2020) depends on the specific value of the payment. To make it clearer, let's look at a specific example.

Examples: pay insurance premiums with or without kopecks 2021

Example No. 1.

For the month of July, employees of the State Budgetary Educational Institution DoD SDYUSSHOR "ALLUR" were accrued wages and vacation pay in the amount of 1,500,000 rubles. There are no non-taxable income in the accrued amount. Electricity taxation is carried out according to generally established tariffs. Let's calculate the amount of payments to the budget:

- OPS: 1,500,000 × 22% = 330,000.00 rubles;

- Compulsory medical insurance: 1,500,000 × 5.1% = 76,500.00 rubles;

- VNiM: 1,500,000 × 2.9% = 43,500.00 rubles;

- FSS NS and PZ = 1,500,000 × 0.2% = 3,000.00 rubles.

Consequently, in July, GBOU DOD SDUSSHOR ALLYUR makes payments without kopecks. But this payment format is not associated with rounding!

Example No. 2. Accrued wages for August at the State Budgetary Educational Institution of Children's and Youth Sports School "ALLUR" amounted to 102,653 rubles due to the majority of employees being on vacation. CA calculations for August will be as follows:

- OPS: 102,653 × 22% = 22,583.66 rubles;

- Compulsory medical insurance: 102,653 × 5.1% = 5235.30 rubles;

- VNiM: 102,653 × 2.9% = 2976.94 rubles;

- NS and PZ: 102,653 × 0.2% = 205.31 rubles.

As a result, for August, a budgetary institution is obliged to pay the budget in rubles and kopecks. There are no exceptions in this case.

Can payments to the Pension Fund of Russia be rounded in 2021? It is possible, but only in a big way. For example, when calculating for August, a budgetary institution will transfer not 22,583 rubles and 66 kopecks, but exactly 22,584 rubles. The result is an overpayment of 34 kopecks. This method of payment is not prohibited, but it is not necessary to round payments up.

IMPORTANT!

You cannot round down the amount according to the SV! This will lead to the formation of debts, penalties and fines.

Summarize. The company, deciding how to pay insurance premiums to the Pension Fund of Russia - with or without kopecks in 2021, or in favor of other types of insurance coverage, can make calculations without kopecks, rounding up payments. However, representatives of the Federal Tax Service do not encourage this method of payment.

Limit value of the base for calculation

Specific rates of insurance premiums in 2021 are established for the entire calendar period. Changes occur when the limit established by law is exceeded (GD of the Russian Federation dated November 29, 2016 No. 1255):

- for compulsory health insurance, a limit of 755,000 rubles per insured person is set;

- for VNiM - 876,000 rubles;

- not established for compulsory medical insurance.

The size of the limit is set in full thousands. For example, in August 754,400 rubles were accrued, round up to exactly 754,000. If the amount is 875,550 rubles, then 876,000.

Let's look at a specific example.

| Month | Amount of charges (rubles) |

| January | 100 000,00 |

| February | 100 000,00 |

| March | 100 000,00 |

| April | 100 000,00 |

| May | 200 000,00 |

| June | 10 000,00 |

| July | 150 000,00 |

| August | 150 000,00 |

| TOTAL | 910 000,00 |

Exceeding the limit for OPS occurs in July (760,000.00 rubles), and for VNiM - in August (910,000.00 rubles). From this moment, reduced rates for insurance premiums for compulsory health insurance are established in 2020. The rate is reduced from 22% to 10%, and for VNiM - from 2.9% to 0%.

How to pay dues in 2021

We will fill out the payment order according to the new rules. First of all, we establish the number and date of the payment. We fill out the fields in chronological order, otherwise the Treasury or the bank will cancel the operation.

Go to field 101. For transfers of insurance coverage to the Federal Tax Service, set the value to “01”, since the legal entity pays.

We fill in information about the payer (name, tax identification number, checkpoint, bank, settlement and correspondent accounts of a budget organization).

We enter similar information about the recipient of the funds. Please note that you must first indicate the branch of the Federal Treasury, and in brackets - the Federal Tax Service number. These rules do not apply to FSS NS and PZ payment cards. The recipient in this case is the FSS. We provide Social Security details so that the payment is not returned.

Let's move on to filling out the "Codes" block. The order of payment for monthly payments is “05”, for payments at the request of the inspection – “03”. Type of operation – value “01”, code – “0”.

We will consider the features of filling out the tax line and the purpose of payment in the form of a table.

| Field name and number | Details for compulsory medical insurance, compulsory medical insurance and VniM | Details for FSS NS and PZ |

| 104 "KBK" | For monthly payments we indicate:

| 393 1 0200 160 |

| 105 "OKTMO" | We indicate the code of the territory of the municipality for the recipient of the money transfer. | |

| 106 “Basis of payment” | The value of “TP” is for the current period, in case of voluntary repayment of debt - “ZD”. | 0 |

| 107 “Tax period” | We put a code of 8 characters: the first 2 characters are the abbreviated name of the period (MS, HF, GD), the second 2 characters are the designation of the month, quarter, the last 4 characters are the designation of the calendar year. For example, payment for August 2021 is MS.08.2018. | 0 |

| 108 “Basic document” | For monthly payment - “0”. When paying debts on demand - “TR”, if there is a decision on installment plans - “RS”. | |

| 109 “Date of foundation document” | “0” – for periodic payments. If requested, the date of the document (request, audit report, etc.). | |

| 110 "Inform" | Do not fill out. | |

| 24 “Purpose of payment” | We write down the name and period for which we pay. | “Insurance premiums against industrial accidents and occupational diseases for employees for August 2021. Registration number - 1234567890.” We must indicate the registration number. |

Details for paying FSS insurance premiums in 2021

The purpose of the Social Security Fund is to support employers and their employees in the event of incapacity for work. These include maternity leave, parental leave and workplace accidents. The employer is obliged to make monthly cash contributions to the Social Insurance Fund for its employees.

This is done according to two types of insurance: in case of pregnancy, childbirth and care of a newborn, and in connection with temporary disability caused by the place of work.

In turn, the social insurance fund supports workers, acting as a guarantor of cash income in case of illness or maternity leave. In some cases, sick leave may also be paid.

Employers' insurance premiums go to help those injured at work, for their treatment and rehabilitation.

Payments should be made to the local tax authority. For 2018, transfers and payments of funds for insurance are controlled by the Federal Tax Service .

Budget classification codes and rules for filling out payment orders have also changed. However, separate payments “for injuries” should be submitted to the Social Security Fund.

Insurance payments are made thanks to settlement documents that are sent to the tax service.

The Tax Code of the Russian Federation instructs taxpayers to maintain accurate records of contributions made and other cash transfers.

To do this, it is proposed to use the form of the Russian Pension Fund - an individual registration card.

The employer is obliged to transfer funds for insurance no later than the fifteenth day of the month following the month of accrual. The monetary amount of the contribution is calculated in rubles.

Basic

The tax office was responsible for the transfer of insurance payments. Thanks to this, the insurer should now find out local tax information and transfer funds using new details.

The address and TIN of the local tax authority can be found on the Internet. Please note that all Budget Classification Codes that were controlled by the Social Insurance Fund have been changed.

Thanks to them, contributions and payments to employees are now under the control of the Tax Code. The codes have changed both for transfers to compulsory health insurance and for funds allocated to the Pension Fund. The only thing that remained unchanged was the form for filling out transfers “for injuries”: neither the CBC, nor the recipient, nor other columns have changed.

KBK

The abbreviation KBK stands for “Budget Classification Codes”; they are needed to record income and expenditures at all levels of the Russian budget.

They are indicated when processing payment orders for paying taxes, government contributions, fees and fines.

The twenty-digit number is the correct place of arrival of money transfers, a kind of state account of a particular organization.

Each digit in the code is a carrier of information : the first digits indicate the code of the organization to which the transfers are received, followed by the income code, after that the payment code, then the income item and subitem, numbers indicating the place of transfer of the state budget, numbers deciphering the reason for the payment and numbers explaining the type of income.

Knowing the correct transfer codes is very important to avoid making mistakes when transferring money.

KBK table for 2021:

| Insurance payments for compulsory social insurance for those injured at work or who have received an illness related to professional activity. | 393 1 0200 160 |

| Insurance premiums in case of temporary disability (illness confirmed by sick leave) or in connection with pregnancy and childbirth. | 393 1 0200 160 |

Registration numbers

In order for the transfer of the amount to occur successfully, it is necessary to take into account all the above factors and correctly draw up the payment document.

Previously, the process of obtaining a registration code occurred as follows : the tax service itself transmitted all the data necessary to the employer.

Now neither the registration numbers of the Pension Fund nor the Social Insurance Fund will be indicated in the updated form for filling out the unified Calculation of Insurance Contributions. Previously, documentation with an error in the form of the specified Pension Fund code did not play a role.

However, payments for “injury” - for workers who were injured in connection with work activities - have not changed for 2021 and remain the same. The budget classification code for these transfers also remains the same. The entire process of paying contributions is carried out in the same way as before.

Contributions for injuries

Previously, contributions for injuries were combined with contributions for compulsory health insurance. For 2021 they are paid separately.

Payments for workers who may be injured at work are made to the Social Insurance Fund, as happened before, all assigned tariffs and special benefits remain in place.

Due to the division of labor between the fund and the tax office, the reporting form has changed.

The employer is obliged to pay insurance payments for the employee if the employee is employed officially, through a work book. The percentage of contributions to the fund depends on the possible risk for the worker.

Money transfers are calculated monthly, and the reporting itself is submitted at the end of the quarter. Due dates vary from the twentieth of the month following the reporting quarter to the twenty-fifth.

The number of workers affects the method of reporting - on paper it is submitted in the case of a headquarters of up to 25 people, and electronically if their number is larger.

Table for transferring funds “for injuries”:

Reporting periodForm on paperForm in electronic version

| First quarter | 20 April | 25th of April |

| Second quarter | July 20 | July 25 |

| Third quarter | The 20th of October | the 25th of October |

| Fourth quarter | January 22 | The 25th of January |

Important details regarding payments

During any operations with documents and papers, you need to take into account all the subtleties and nuances in order to avoid mistakes: wasted effort and money. It is also useful to know how, in case of an error, you can return your own spent funds. features when it comes to insurance payments:

- The updated form of the report on the Unified Social Insurance Tax cannot provide for the indication of information on the registration numbers of the insurer in the local branch of the Social Insurance Fund or the Pension Fund, which were previously mandatory. For 2021, registration numbers are not indicated when transferring funds.

- At the end of the year, it is necessary to reconcile all data with the funds. If debts are discovered, they must be repaid by the end of the current year.

- If you discover that funds have been paid to the fund in excess, you must submit a statement explaining the situation and supporting documents to the branch of the Social Insurance Fund. There, it is possible to arrange a transfer of funds back to the account of the insurer and the premium payer - after the validity of the expenses has been verified.

Penalty amount

The amount of penalties will increase in case of delay in insurance payments:

- in case of 30 days of delay - by 1/300 of the rate;

- in case of 31 or more days - 1/150 of the rate.

Anyone can use an online calculator of penalties for insurance payments - right from the comfort of their home. To do this, on the website you like, you should select the tax or contribution in the required box, the established payment date and the date of actual payment. Next, the calculator will calculate the amount of debt you are interested in.

Since the tax service has taken over responsibilities not only for insurance, but also for pension payments by the employer, you can practically not remember about the details of the Russian Pension Fund. For 2021, payments are sent to the address of the local tax authority. In this regard, changes in the documentation occur in the following columns :

- the recipient changes;

- the TIN column is changed;

- The Taxpayer Identification Number column is changed;

- The budget classification code is changing.

Now pension transfers for employees of your own enterprise are made according to a new scheme - through the Federal Tax Service.

As for the FFOMS, for correct transfer you need to know the Budget Classification Codes.

| Transfer to the employee budget | 392 1 0211 160 |

| Transfer to the FFOMS for potential payments to an individual entrepreneur | 392 1 0211 160 |

This data is sufficient to transfer funds.

We recommend other articles on the topic

Source: https://znaybiz.ru/fondy/fss-ffoms/vznosy/rekvizity-dlya-uplaty.html