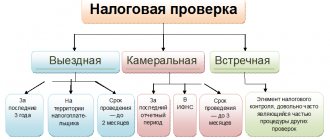

Desk audit results

Since tax authorities have the right to conduct audits of payers, in accordance with current legislation, payers must be notified of the decision made and the results of this audit. However, this is not always the case under tax law. The requirements for drawing up a tax audit report are prescribed by the Order of the Federal Tax Service.

A desk audit is a check regarding the accuracy of the data provided by the payer, which is carried out independently of the payer. That is, the tax authorities check the documents and, if necessary, request additional information, but do not draw up an inspection report if no violations are found with the payer. This measure is not provided for by law - the desk audit ends automatically without notifying the payer.

In cases where violations are detected, the tax authority, within 10 days (meaning working days, not calendar days), draws up a tax audit report, which specifies all violations, requirements for elimination and deadlines. After drawing up the act, the tax authority is obliged to deliver the document to the payer in respect of whom the audit was carried out within 5 working days.

The tax audit report is drawn up within the framework of current legislation and includes three parts: introductory, descriptive, and final.

Each part should contain not only requirements for eliminating the violations found, but also references to legislative acts regulating tax issues. If a tax audit report is drawn up in violation of the norms, the payer has the right to challenge it first to the tax authority, and, if necessary, to the judicial authorities.

Registration of the results of a desk tax audit is not required if the tax authorities have no comments on the payer. In the event that an organization, individual entrepreneur, or individual has violations in matters of compliance with tax legislation, an act is drawn up and submitted within the period established by law.

Checking act

As a general rule, the inspector draws up an inspection report in two copies immediately after completing the inspection (Parts 1 and 4 of Article 16 of the Law of December 26, 2008 No. 294-FZ). In exceptional cases, three working days are allotted for drawing up the act. This is possible if, in order to draw up a document, it is necessary to obtain conclusions based on the results of studies, tests or examinations. This is stated in Part 5 of Article 16 of the Law of December 26, 2008 No. 294-FZ.

The form of the act was approved by order of the Ministry of Economic Development of Russia dated April 30, 2009 No. 141.

The report must contain detailed information about the inspection carried out, namely:

- date, time and place of drawing up the act;

- the name of the territorial labor inspectorate whose employees carried out the inspection;

- date and number of the order (order) of the head of the labor inspectorate (his deputy) to conduct the inspection;

- last name, first name, patronymic and position of the labor inspector who conducted the inspection;

- name of the organization being inspected (individual entrepreneur);

- date, time, duration and place of the inspection;

- information about the results of the inspection, about the violations identified, about their nature and about the persons who committed these violations;

- information about familiarization or refusal to familiarize with the act of a representative of the organization being inspected (individual entrepreneur);

- information about making an entry about the inspection in the inspection log or about the impossibility of making such an entry due to the lack of an inspection log;

- signature of the labor inspector who conducted the inspection.

Such requirements for the content of the act are established in Part 2 of Article 16 of the Law of December 26, 2008 No. 294-FZ.

On-site inspection results

An on-site inspection means a direct inspection by the tax authorities either on the territory of the payer in respect of whom the inspection is being carried out, or, if the payer cannot provide premises for the inspection, on the territory of the tax authority. At the same time, an on-site audit is more thorough than a desk audit, since the tax authorities thoroughly study all the payer’s documentation related to expenses and income. The tax audit report is drawn up strictly within two months after the audit certificate is drawn up. Moreover, if an entire consolidated group was checked, the period is increased by another month.

The tax audit report is drawn up in accordance with all the rules, has an introductory, descriptive and final part, where all aspects of the audit are prescribed. At the legislative level, it has been established that, regardless of the presence of violations, an on-site tax audit report is drawn up and handed over to the payer. Even if there were no violations, the document is drawn up by the tax authority, signed by its head, as well as by the payer in respect of whom the audit was carried out.

It is noteworthy that if the payer refuses to sign the on-site tax audit report, the document is still valid. The tax authority is obliged to make an appropriate mark in it, where the payer’s refusal to sign is recorded.

If the payer avoids receiving the report by all possible means, the tax authority makes an appropriate entry and then sends the documents with attachments by mail. At the same time, the sending format is in the format of a registered letter, since this makes it possible to track whether the payer received the documents and on what date this happened.

Dispatch is carried out exclusively to the payer's address. For example, to the address of an organization or its separate division, but not to the address of a representative or head of the organization.

The law establishes that the day of receipt of documents is considered to be the sixth day from the date of sending. Therefore, all calculation periods for appealing an act or expressing claims on it begin to be calculated precisely from the sixth day after sending the document (meaning the sixth working day). For other cases, the period for transferring the act is 5 working days.

Provided that the payer in respect of whom the audit was carried out is an individual entrepreneur, an individual or a Russian organization.

If the payer is a consolidated group of payers, then the completed on-site tax audit report is transferred within 10 working days to the responsible participant or his representative.

If the payer is a foreign organization, then the act is sent by mail, and the day of delivery is considered to be the 20th working day. The sending format is a registered letter to the address of the organization, as well as to the address of a separate division through which activities are carried out on the territory of the Russian Federation.

The procedure for drawing up an on-site tax audit report is regulated by both Article 100 of the Tax Code and the Order of the Federal Tax Service.

Article 16. Procedure for recording inspection results

⇐ PreviousPage 488 of 968Next ⇒1. Based on the results of the inspection, officials of the state control (supervision) body, municipal control body conducting the inspection draw up an act in the prescribed form in two copies. The standard form of the inspection report is established by the federal executive body authorized by the Government of the Russian Federation.

2. The inspection report shall indicate:

1) date, time and place of drawing up the inspection report;

2) name of the state control (supervision) body or municipal control body;

3) date and number of the order or order of the head, deputy head of the state control (supervision) body, municipal control body;

4) last names, first names, patronymics and positions of the official or officials who conducted the inspection;

5) the name of the legal entity being inspected or the last name, first name and patronymic of the individual entrepreneur, as well as the last name, first name, patronymic and position of the manager, other official or authorized representative of the legal entity, authorized representative of the individual entrepreneur who were present during the inspection;

6) date, time, duration and place of the inspection;

7) information on the results of the inspection, including on identified violations of mandatory requirements and requirements established by municipal legal acts, on their nature and on the persons who committed these violations;

information about familiarization or refusal to familiarize with the inspection report of the manager, other official or authorized representative of a legal entity, individual entrepreneur, his authorized representative present during the inspection, the presence of their signatures or refusal to sign, as well as information about entering into an inspection log of a record of an inspection performed or of the impossibility of making such an entry due to the lack of a specified log at a legal entity or individual entrepreneur;

information about familiarization or refusal to familiarize with the inspection report of the manager, other official or authorized representative of a legal entity, individual entrepreneur, his authorized representative present during the inspection, the presence of their signatures or refusal to sign, as well as information about entering into an inspection log of a record of an inspection performed or of the impossibility of making such an entry due to the lack of a specified log at a legal entity or individual entrepreneur;

9) signatures of the official or officials who conducted the inspection.

3. Attached to the inspection report are protocols for the selection of product samples, inspection samples of environmental objects and industrial environment objects, protocols or conclusions of studies, tests and examinations, explanations from employees of a legal entity, employees of an individual entrepreneur who are held responsible for violation of mandatory requirements or requirements established by municipal legal acts, orders to eliminate identified violations and other documents or copies thereof related to the results of the inspection.

4. The inspection report is drawn up immediately after its completion in two copies, one of which with copies of the attachments is handed over to the manager, other official or authorized representative of the legal entity, individual entrepreneur, his authorized representative against a receipt for familiarization or refusal to familiarize himself with the inspection report. In the absence of the head, other official or authorized representative of a legal entity, individual entrepreneur, his authorized representative, as well as in the event of the refusal of the person being inspected to give a receipt for familiarization or refusal to familiarize himself with the inspection report, the act is sent by registered mail with return receipt requested, which is attached to a copy of the inspection report kept in the file of the state control (supervision) body or municipal control body.

5. If in order to draw up an inspection report it is necessary to obtain conclusions based on the results of studies, tests, special investigations, examinations, the inspection report is drawn up within a period not exceeding three working days after the completion of control measures and is handed over to the manager, other official or to an authorized representative of a legal entity, an individual entrepreneur, his authorized representative against receipt, or sent by registered mail with a return receipt, which is attached to a copy of the inspection report kept on file with the state control (supervision) body or municipal control body.

6. If an unscheduled on-site inspection requires coordination with the prosecutor's office, a copy of the inspection report is sent to the prosecutor's office, which decided to approve the inspection, within five working days from the date of drawing up the inspection report.

7. The results of the inspection, containing information constituting state, commercial, official or other secrets, are formalized in compliance with the requirements stipulated by the legislation of the Russian Federation.

8. Legal entities and individual entrepreneurs are required to keep a log of inspections in a standard form established by the federal executive body authorized by the Government of the Russian Federation.

9. In the log book of inspections by officials of the state control (supervision) body, municipal control body, a record is made of the inspection carried out, containing information about the name of the state control (supervision) body, the name of the municipal control body, the start and end dates of the inspection, the time of its conduct , legal grounds, goals, objectives and subject of the inspection, violations identified and orders issued, as well as the surnames, first names, patronymics and positions of the official or officials conducting the inspection, his or their signatures.

10. The audit log must be stitched, numbered and certified with the seal of a legal entity or individual entrepreneur.

11. If there is no inspection log, a corresponding entry is made in the inspection report.

12. A legal entity, individual entrepreneur, whose inspection was carried out, in case of disagreement with the facts, conclusions, proposals set out in the inspection report, or with the issued order to eliminate the identified violations, within fifteen days from the date of receipt of the inspection report, has the right to submit to the relevant government body control (supervision), the municipal control body, in writing, objects to the inspection report and (or) the issued order to eliminate the identified violations in general or its individual provisions. In this case, a legal entity or individual entrepreneur has the right to attach to such objections documents confirming the validity of such objections, or their certified copies, or, within the agreed period, transfer them to the state control (supervision) body, municipal control body.

Article 17. Measures taken by officials of the state control (supervision) body, municipal control body in relation to violations identified during the inspection

1. If, during an inspection, violations by a legal entity or individual entrepreneur of mandatory requirements or requirements established by municipal legal acts are revealed, the officials of the state control (supervision) body, municipal control body who conducted the inspection, within the powers provided for by the legislation of the Russian Federation, are obliged :

1) issue an order to a legal entity, individual entrepreneur to eliminate identified violations, indicating the time frame for their elimination and (or) to take measures to prevent harm to life, health of people, harm to animals, plants, the environment, cultural heritage sites (historical and cultural monuments ) the peoples of the Russian Federation, state security, property of individuals and legal entities, state or municipal property, prevention of emergencies of a natural and man-made nature, as well as other measures provided for by federal laws;

2) take measures to monitor the elimination of identified violations, prevent them, prevent possible harm to life, health of citizens, harm to animals, plants, the environment, cultural heritage sites (historical and cultural monuments) of the peoples of the Russian Federation, ensure state security, prevent the occurrence of emergency situations of natural and man-made nature, as well as measures to bring persons who committed identified violations to justice.

2. If during an inspection it is established that the activities of a legal entity, its branch, representative office, structural unit, individual entrepreneur, their operation of buildings, structures, structures, premises, equipment, similar facilities, vehicles, goods produced and sold by them (work performed, services provided) pose a direct threat of harm to life, health of citizens, harm to animals, plants, the environment, cultural heritage sites (historical and cultural monuments) of the peoples of the Russian Federation, state security, the occurrence of natural and man-made emergencies, or such harm has been caused, the state control (supervision) body, municipal control body are obliged to immediately take measures to prevent harm or stop it from being caused, up to a temporary ban on the activities of a legal entity, its branch, representative office, structural unit, individual entrepreneur in the manner established by the Code of the Russian Federation on administrative offenses, recall of products that pose a danger to the life, health of citizens and the environment from circulation and bring to the attention of citizens, as well as other legal entities, individual entrepreneurs in any available way information about the presence of a threat of harm and ways to prevent it.

Article 18. Responsibilities of officials of the state control (supervision) body, municipal control body when conducting an inspection

When conducting an inspection, officials of the state control (supervision) body and municipal control body are obliged to:

1) timely and fully fulfill the powers granted in accordance with the legislation of the Russian Federation to prevent, identify and suppress violations of mandatory requirements and requirements established by municipal legal acts;

2) comply with the legislation of the Russian Federation, the rights and legitimate interests of a legal entity, individual entrepreneur, the inspection of which is carried out;

3) conduct an inspection on the basis of an order or order from the head, deputy head of the state control (supervision) body, municipal control body on its conduct in accordance with its purpose;

4) conduct an inspection only during the performance of official duties, an on-site inspection only upon presentation of official identification, a copy of the order or order of the head, deputy head of the state control (supervision) body, municipal control body and in the case provided for by Part 5 of Article 10 of this Federal Law, copies of the document confirming the approval of the inspection;

5) not prevent the manager, other official or authorized representative of a legal entity, individual entrepreneur, or his authorized representative from being present during the inspection and giving explanations on issues related to the subject of the inspection;

6) provide the manager, other official or authorized representative of a legal entity, individual entrepreneur, his authorized representative present during the inspection with information and documents related to the subject of the inspection;

7) acquaint the manager, other official or authorized representative of a legal entity, individual entrepreneur, his authorized representative with the results of the inspection;

take into account, when determining the measures taken in response to detected violations, the compliance of these measures with the severity of the violations, their potential danger to life, human health, animals, plants, the environment, cultural heritage sites (historical and cultural monuments) of the peoples of the Russian Federation, state security, for the occurrence of emergencies of a natural and man-made nature, and also to prevent unreasonable restrictions on the rights and legitimate interests of citizens, including individual entrepreneurs and legal entities;

9) prove the validity of their actions when appealing them by legal entities and individual entrepreneurs in the manner established by the legislation of the Russian Federation;

10) comply with the deadlines for conducting the inspection established by this Federal Law;

11) not demand from a legal entity or individual entrepreneur documents and other information, the presentation of which is not provided for by the legislation of the Russian Federation;

12) before the start of an on-site inspection, at the request of the manager, other official or authorized representative of a legal entity, individual entrepreneur, or his authorized representative, familiarize them with the provisions of the administrative regulations (if any) in accordance with which the inspection is carried out;

13) record the inspection performed in the inspection log.

Article 19. Responsibility of the state control (supervision) body, municipal control body, and their officials when conducting an inspection

1. The state control (supervision) body, the municipal control body, their officials in case of improper performance of functions, official duties, or commission of illegal actions (inaction) during an inspection are liable in accordance with the legislation of the Russian Federation.

2. State control (supervision) bodies, municipal control bodies exercise control over the performance of official duties by officials of the relevant bodies, keep records of cases of improper performance of official duties by officials, conduct relevant official investigations and take measures in accordance with the legislation of the Russian Federation in relation to such officials persons

3. Within ten days from the date of taking such measures, the state control (supervision) body, municipal control body are obliged to inform in writing the legal entity, individual entrepreneur, rights and ( or) whose legitimate interests are violated.

Article 20. Invalidity of the results of an inspection carried out in gross violation of the requirements of this Federal Law

1. The results of an inspection conducted by a state control (supervision) body, a municipal control body in gross violation of the requirements established by this Federal Law for the organization and conduct of inspections cannot be evidence of a violation by a legal entity or individual entrepreneur of the mandatory requirements and requirements established by municipal legal acts, and are subject to cancellation by a higher state control (supervision) body or a court on the basis of an application from a legal entity or individual entrepreneur.

2. Gross violations include violation of the requirements provided for:

1) parts 2, 3 (regarding the absence of grounds for conducting a scheduled inspection), part 12 of Article 9 and part 16 (regarding the period of notification of an inspection) of Article 10 of this Federal Law;

1.1) paragraphs 7 and 9 of Article 2 of this Federal Law (in terms of involving legal entities, individual entrepreneurs and citizens not certified in the established procedure in carrying out control measures);

2) paragraph 2 of part 2, part 3 (in terms of the grounds for conducting an unscheduled on-site inspection), part 5 (in terms of coordination with the prosecutor's office of an unscheduled on-site inspection in relation to a legal entity, individual entrepreneur) of Article 10 of this Federal Law;

3) Part 2 of Article 13 of this Federal Law (in terms of violation of the terms and time of scheduled on-site inspections in relation to small businesses);

4) Part 1 of Article 14 of this Federal Law (in terms of conducting an inspection without an order or order from the head, deputy head of the state control (supervision) body, municipal control body);

5) paragraph 3 (in terms of the requirement for documents not related to the subject of the inspection), paragraph 6 (in terms of exceeding the established deadlines for conducting inspections) of Article 15 of this Federal Law;

6) Part 4 of Article 16 of this Federal Law (regarding failure to submit an inspection report);

7) Part 3 of Article 9 of this Federal Law (in terms of conducting a scheduled inspection not included in the annual plan for conducting scheduled inspections);

Part 6 of Article 12 of this Federal Law (in terms of participation in inspections of experts, expert organizations that have civil and labor relations with legal entities and individual entrepreneurs in respect of whom inspections are carried out).

Chapter 3. Rights of legal entities, individual entrepreneurs in the exercise of state control (supervision), municipal control and protection of their rights

⇐ Previous481482483484485486487488489490491492493494495496Next ⇒

Site search:

What is stated in the act

The introductory part of the act indicates the following information:

- date of drawing up (should be understood as the date of signing the act, and not direct drawing up);

- name of the payer (in the case of organizations - the name of the organization, individual entrepreneur - the name of the individual entrepreneur, individual - full name);

- documents that were checked during the audit;

- a list of taxes and fees that are prescribed to the payer;

- data on the activities that were carried out as part of the inspection;

- the period during which the inspection was carried out;

- period of the beginning and end of the inspection.

If necessary, the introductory part additionally indicates the details of the payer or the tax authority that conducted the audit, as well as any other details necessary for the audit.

The descriptive part of the act describes all aspects of the violations that were found during the inspection, as well as links to the regulatory documents on which the inspection was carried out and inconsistencies were found.

In addition, it is in the descriptive part that possible aggravating circumstances for the payer or, conversely, mitigating circumstances are indicated. If no violations were found during the on-site inspection, this is indicated in the descriptive part.

In the final part of the act, the tax authority states who exactly carried out the audit (should be understood as the full names of specific officials), methods and deadlines for eliminating violations, links to regulatory documents providing for liability for violations, the possibility of objecting to the act, a list of attached documents .

The form and requirements for drawing up a tax audit report imply drawing up the document both in paper format and in electronic format. Moreover, if the act is sent to the payer via telecommunications, this does not negate its preparation on paper, which is also sent to the payer in one of the legal ways.

The act may additionally be accompanied by documents that confirm the fact of the violation.

The legislation establishes the impossibility of attaching documents provided personally by the payer to the act on which the inspection was carried out.

If the documents attached to the act contain deliberately incorrect information, then such documents cannot be considered as evidence of a tax offense. All documents that relate to hidden information or personal data can be presented exclusively in the form of extracts certified by the tax authorities.

Objections

A payer who disagrees with the drawn up inspection report has the right to challenge this report. The legislation provides a period of one month for challenging. The payer has the right to object both directly to the tax authority that conducted the audit, with the provision of evidence documents, and to the judicial authorities.

The tax authority is obliged to consider the written objection, study the submitted documents, check their authenticity, and then make a new decision regarding the payer, which is confirmed by a written document.

Author of the article

Procedure for appealing the results of a tax audit

A taxpayer who disagrees with the facts, conclusions and proposals set out in the on-site tax audit report has the right to submit his written objections to the Federal Tax Service. This can be done within 1 month from the date of receipt of the act. Objections are possible both to the act as a whole and to its individual provisions; in this case, you can attach, or submit later within a specified period of time, documents confirming the correctness of the taxpayer (clause 6 of Article 100 of the Tax Code of the Russian Federation).

The head of the Federal Tax Service considers the taxpayer’s objections along with the act itself and the audit materials. The result of the consideration will be one of the decisions:

- hold the taxpayer accountable,

- refuse to bring to tax liability,

- carry out additional control measures (clause 1 of article 101 of the Tax Code of the Russian Federation).