In the practice of entrepreneurship, one has to be both in the role of a lender and in the role of a borrower. In the first case, situations occur when partners, for one reason or another, do not repay the debt on time or do not fulfill their financial obligations at all. However, such financial situations must still be reliably reflected in the organization's accounting and financial records. A special reserve is created for this purpose.

Is it necessary to create a reserve for doubtful debts on advances issued ?

Let's consider the principles of forming this type of reserve, methods of accounting for it, accounting entries accompanying this process, as well as the nuances of write-off.

Doubtful debts and provisions for them

For a reliable financial reflection of the organization’s receivables in the accounting documents, a so-called reserve for doubtful debts is created. To define this concept, you first need to understand what doubtful debt is.

doubtful if they are unlikely to be repaid in full, as evidenced by the following factors:

- violation by a partner of deadlines for paying off debt;

- obtaining information about serious financial difficulties of the debtor partner;

- absence of any additional guarantees (collateral, deposit, surety, bank guarantee, retention of any property of the counterparty, etc.)

FOR YOUR INFORMATION! Debt reflected in the debit of any accounting accounts, including 60, 62, 72, as well as issued as a loan under subaccount 58-3, may become doubtful.

Doubtful debts are identified based on the results of the inventory of current accounts:

- on loans;

- for goods and/or services sold;

- payment for work performed;

- in some cases - for advances issued to suppliers.

How to use the reserve for doubtful debts ?

In order to correctly reflect this type of debt on the balance sheet, a special type of reserve is created, which is intended to serve as an estimate for accounting. This means that the amount of debt must be reflected in the balance sheet by subtracting from it the funds allocated to the reserve. The content of expenses or income must necessarily display:

- creation of such a reserve;

- its increase;

- reduction of funds.

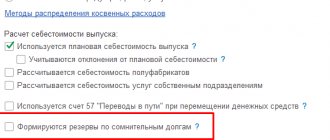

NOTE! The reserve created for doubtful debts is included in the expenses that are deducted for taxation, therefore, it is financially beneficial for organizations from the point of view of tax accounting to form and take into account the reserve.

Postings for using the reserve

As of 04/01/2016, the accounting records of Artemis JSC include the amount of unused reserve in the amount of 43,120 rubles. The list of doubtful and bad debts of Artemis JSC as of 04/01/2016 looks like this:

| Contractor's name | Operation description | Debt amount | Maturity | Overdue period | Debt classification |

| JSC “Hercules” | a batch of agricultural implements was shipped in favor of the counterparty under a supply agreement | RUR 168,410 | 09.04.2016 | 83 days | dubious |

| JSC “Minotaur” | the counterparty was provided with services for setting up agricultural equipment and machinery under the contract | RUR 41,960 | 08.02.2016 | 371 days | hopeless (JSC “Minotaur” was liquidated) |

A reserve has been created for the amount of doubtful debts of “Hercules”.

Due to the liquidation of Minotaur and the classification of the debt as bad, the amount of debt was written off from the previously formed reserve.

Based on the operations performed, the amount of the reserve as of 04/01/2016 amounted to 169,570 rubles. (43,120 rubles + 168,410 rubles – 41,960 rubles).

Let's look at the entries made by Artemis's accountant:

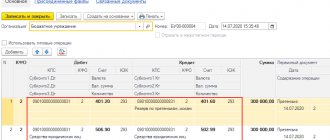

| Debit | Credit | Operation description | Sum | A document base |

| 91.2 | 63 | The amount of the reserve formed as of 04/01/2016 is reflected in other expenses | RUR 169,570 | Accounting statement, accounts receivable statement |

| 63 | 62 | The debts of “Minotaur”, recognized as uncollectible due to its liquidation, were written off from reserve amounts | RUR 41,960 | Accounting statement, accounts receivable statement |

| 63 | 91.1 | The restoration of the amount of the reserve unused at the end of 2021 is reflected | RUR 169,570 | Accounting statement, accounts receivable statement |

Legislative documents

State regulation of issues related to the reserve for doubtful debts is regulated by the following legislative acts:

- Tax Code of the Russian Federation (Part 2) dated August 5, 2000 No. 117-FZ, as amended, entered into force on March 1, 2015;

- Regulations on maintaining accounting and financial statements in the Russian Federation, approved by Order of the Ministry of Finance of the Russian Federation dated July 29, 1998 No. 34n;

- Accounting Regulations PBU 4/99 “Accounting Statements of an Organization”, approved by Order of the Ministry of Finance of the Russian Federation dated July 6, 1999 No. 43n;

- Order of the Ministry of Finance dated June 13, 1995 No. 49 (as amended on November 8, 2010) “On approval of the Methodological Guidelines for the Inventory of Property and Financial Liabilities”;

- Accounting Regulation 21/2008 “Changes in estimated values”, approved by Order of the Ministry of Finance of the Russian Federation dated October 6, 2008 No. 106n.

In what cases is it necessary to restore the provision for doubtful debts in accounting?

How to create a reserve for doubtful debts

The specifics of creating and disposing of a reserve for doubtful debts are not clearly regulated by law. Organizations must independently develop appropriate provisions and consolidate them in internal regulations. In this case, it is necessary to take into account the generally accepted features of the regulation of a company’s financial reserves.

- Basis for creation - for this type of reserve they will be the results of the inventory of receivables carried out on the last reporting day.

- The amount of reserve contributions is determined separately for each defaulter (analytical accounting of doubtful debts). At the same time, the solvency of each partner is taken into account (real financial prospects and opportunities for full or partial repayment of debt).

- Method for creating a reserve can be chosen by the organization independently based on the specifics of its activities and the nuances of the debt itself. There are three possible ways to create a reserve fund for doubtful debts:

- interval - the amount of reserve contributions is calculated every billing period (month, quarter) by calculating a percentage of the debt amount, which may vary depending on the degree of delay in payment;

- expert - the amount of debt that will not be paid on time is assessed separately for each debtor, this will be the amount of reserve contributions;

- statistical – data on bad debts is taken into account for several reporting periods for different types of debt.

IMPORTANT INFORMATION! The organization must record the chosen method and features of calculation in its accounting policies. For each type, you need to specify the appropriate conditions. For example, for the interval method, the accounting period and the percentage of deductions must be indicated (not necessarily the same as that used in tax accounting); for an expert – criteria for the debtor’s solvency, etc.

Accounting for reserves – accounting or tax?

The features of creating a reserve for doubtful debts in accounting and tax accounting differ significantly, since these types of accounting have different purposes. Let's compare the rules specific to accounting and tax accounting regarding the reserve.

- Mandatory creation. In accounting, such a reserve is required, since it is required by paragraph. 1 clause 7 of the Accounting Regulations. If an organization uses the accrual method for tax accounting, then the accountant himself decides whether to create such a reserve for tax accounting or not (this right is reflected in clause 3 of Article 266 of the Tax Code of the Russian Federation).

- Characteristics of deductions. Accounting defines reserve contributions as “other expenses,” and for tax accounting they must be taken into account among non-operating expenses.

- Interpretation of the doubtfulness of debt. For accounting purposes, any debt that is not repaid on time or in full is eligible for compensation as a reserve, but for tax purposes, only late payment for goods, services, and work can be recognized as such.

- Determining the amount of deductions . For accounting, the priority of establishing the size remains with the accountant (taking into account the characteristics of the debt), and for tax accounting the sizes are clearly defined by the Tax Code of the Russian Federation.

- The total size of the reserve fund . In accounting it is not limited, and in tax accounting it cannot be more than one tenth of revenue.

Do provisions for doubtful debts count as estimated liabilities ?

Results

The formation of a reserve for doubtful debts in accounting and tax accounting occurs according to different rules.

This circumstance makes it necessary not only to follow these significantly different rules in each of the accounts, but also to take into account temporary differences in such a reserve that arise both when creating and not creating a reserve in tax accounting. You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Conditions for the formation of the reserve

The decrees, orders and letters of the Ministry of Finance of the Russian Federation define a number of conditions necessary to comply with when creating a reserve fund for doubtful debts.

- This fund can be created as a result of settlements with legal entities and individuals - buyers for purchased goods, services or paid work. Advances paid to suppliers are not included in reserve amounts.

- After creating a reserve, the management and/or accounting department of the organization must constantly monitor the dynamics of debts, since their status may change, and the reserve fund must reflect the actual state of affairs (analytical approach).

- In accounting, a debt can be recognized as uncollectible according to the regulations of Art. 266 of the Tax Code of the Russian Federation (as for tax accounting). Otherwise, there is no limit on the timing and size of the reserve fund for debts.

- If the question arises about which accounting procedure to apply for reserve assets, accounting or tax, you should be guided by the following factors:

- if the discrepancies relate to a temporary difference in the correlation of debt terms (for accounting this is a complete non-repayment within 45 days after the expiration of time restrictions), then the difference will lead to the deposition of tax assets, that is, deductible time intervals for certain amounts of funds (clause 8, 11, 14 PBU 18/02, approved by Order of the Ministry of Finance of the Russian Federation dated November 19, 2002 No. 114n);

- if the amount of deductions to the reserve fund for accounting exceeds the 10% barrier established by tax accounting, then the company will operate with permanent financial differences (clauses 4, 7 of PBU 18/02, approved by Order of the Ministry of Finance of the Russian Federation dated November 19, 2002 No. 114n).

How is the inventory of the reserve for doubtful debts ?

Account 63

Account 63 reflects the turnover and balances of transactions related to the formed reserves for doubtful debts of counterparties. This account may reflect the amounts of reserves formed in connection with:

- violation by suppliers of the terms and conditions of shipment of goods;

- non-compliance by customers with terms and conditions of payment for services (work) received.

The account also reflects the write-off of amounts of debts recognized as bad (by a court decision, in connection with liquidation, bankruptcy of the counterparty, expiration of the statute of limitations, under other conditions).

| ★ Best-selling book “Accounting from scratch” for dummies (understand how to do accounting in 72 hours) > 8000 books purchased |

Operations to form a reserve are carried out according to Kt 63; for their write-off and downward adjustment, Dt 63 is used.

Let's look at typical wiring:

| Debit | Credit | Operation description | A document base |

| 91.2 | 63 | The amount of the reserve for doubtful debts was formed at the expense of other expenses | Minutes of the board's decision, accounts receivable statement, accounting certificate-calculation |

| 63 | 62 | The amount of debt recognized as uncollectible was written off from the reserve previously formed on account 63 | Minutes of the board's decision, accounts receivable statement, accounting statement, court decision, liquidation (bankruptcy) document, etc. |

| 63 | 91.1 | The amount of unused reserve that was restored was taken into account | Accounting certificate-calculation |

| 63 | 76.2 | Write-off of the reserve amount in connection with satisfaction of the claim | Letter of claim, accounting certificate-calculation |

Reflection of the provision for doubtful debts in accounting

Since contributions to this reserve are the dynamics of the estimated value, they must be reflected on the balance sheet at a certain frequency. They are included in the expenses of the period in which changes in the movement of assets in this reserve were observed. Therefore, data on the state of the reserve must be contained in each accounting report (Article 15 of the Federal Law of December 6, 2011 No. 402).

We carry out accounting

Provisions for doubtful debts should be reflected in debit 91 “Other income and expenses” and credit 63 “Provisions for doubtful debts”.

We carry out bad debt

If a debt that was previously listed as doubtful is recognized as uncollectible, its reserve will be written off in debit 63 “Provisions for doubtful debts,” which corresponds with account 62 “Settlements with buyers and customers” or 76 “settlements with various debtors and creditors.” If the amount of bad debt is greater than the reserve for it, it will have to be written off as debit 91 “Other expenses and income.” If a debt has been written off for which the statute of limitations has expired, it must be kept for 5 years in off-balance sheet account 007 “Debt of insolvent creditors written off at a loss” in case the debtor’s solvency returns and the possibility of repayment becomes available.

We make partial payment

If payment is received from the debtor for doubtful debts with the formed reserve, at least partially, this affects the dynamics of funds in the reserve in a positive direction, which must be reflected as a recovery in debit 63 “Provisions for doubtful debts”, correspondence with account 91 “Other income and expenses."

We carry out the unused reserve

If the reserve could not be used before the end of the accounting year that follows the one in which the reserve was created, then this amount on the balance sheet should be added to the financial results for this year under debit 63 “Provisions for doubtful debts”, credit 91 “Other” income and expenses".

Posted as tax obligations

If only mandatory accounting of reserves is carried out, and tax accounting is not carried out, then permanent taxable differences must be recognized as tax liabilities, reflecting them in debit 99 “Profits and losses” and credit 68 “Calculations for taxes and fees”.

Examples

EXAMPLE 1 . Based on the results of the quarterly inventory, the organization revealed doubtful debts in the amount of 12 thousand rubles. according to payments for goods sold. A reserve of 100% was created for this debt. On the date the reserve is created, the accounting records will contain the following entry:

- debit 91-2, credit 63 – 12,000 rub. – a reserve for doubtful debt has been created.

After some time, the debtor company repaid part of this receivable in the amount of 7 thousand rubles. The posting on the date of deposit will be as follows:

- debit 63, credit 91-1 – 7,000 rubles. – the provision for repaid receivables was restored.

EXAMPLE 2 . The organization previously recognized a doubtful debt in the amount of 10,000 rubles. A reserve of 7 thousand rubles was created for it, which was then replenished to 100% of the debt amount. After the expiration of the statute of limitations, this debt was recognized as uncollectible and written off at a loss. Let's look at the transactions (each for its own date of a particular operation):

- debit 91-2, credit 63 – 7,000 rub. – a reserve for doubtful debt has been created;

- debit 91-2, credit 63 – 3,000 rub. – additional provision for doubtful debt has been accrued;

- debit 63, credit 76 – 10,000 rub. – bad debts are written off against the reserve.

Reflected in the balance sheet

To reflect doubtful debts in the balance sheet, line 1230 is intended. It reflects the amount of debts minus the reserve created for them.

Creation or additional accruals to the reserve take place on line 2350 of the financial report (“Other expenses”).

Separately, the balance on account 63 “Provisions for doubtful debts” is not displayed in the balance sheet; the total amount of accounts receivable is simply reduced accordingly.

Accounting: creating a reserve

The provision for doubtful debts in accounting is an estimated value. When it is created, increased or decreased, expenses or income are recognized in accounting, respectively. This is stated in paragraph 4 of PBU 21/2008.

Deductions to the reserve for doubtful debts are taken into account as part of other expenses (clause 11 of PBU 10/99). Transactions related to the creation and use of a reserve for doubtful debts are reflected in account 63 “Provisions for doubtful debts”:

Debit 91-2 Credit 63

– a reserve for doubtful debts was created (increased).

The counterparty can repay the debt for which a reserve was previously created, in whole or in part. Then restore the portion of the reserve that relates to this debt:

Debit 51 (50) Credit 62 (71, 73, 76…)

– the counterparty’s debt is repaid;

Debit 63 Credit 91-1

– the provision for repaid receivables was restored.

Organize analytical accounting of accounts receivable for account 62 (58-3, 71, 73, 76...) in such a way that it is possible to obtain all the necessary information about debt that is not paid on time. Such requirements are established by the Instructions for the chart of accounts.

Situation: how to reflect the difference between accounting and tax accounting if a reserve for doubtful debts was not created in tax accounting?

Record the difference as temporary.

Deductions to the reserve for doubtful debts are reflected as part of other expenses using account 91 “Other income and expenses.” In accounting, the created reserve reduces the accounting profit of the reporting period.

If a reserve is not created in tax accounting, then, accordingly, no expenses arise in the reporting tax period. Therefore, a difference arises between accounting profit (loss) and taxable profit (clause 3 of PBU 18/02).

Expenses associated with the creation of a reserve in the current reporting period affect profit (loss) in the future, when the debt is repaid or written off as uncollectible. Consequently, a temporary difference arises (clause 8 of PBU 18/02).

The temporary difference leads to the formation of a deferred tax asset, which will reduce income tax in subsequent periods (clause 11 of PBU 18/02).

In accounting, reflect the deferred tax asset by posting:

Debit 09 Credit 68 subaccount “Calculations for income tax”

– a deferred tax asset is reflected.

In the future, the created reserve can be:

- restored if the debt is repaid. Then include the restored reserve in other income in account 91 “Other income and expenses”;

- restored if the debtor still does not repay the obligation by the end of the year, but the debt cannot yet be recognized as bad (paragraph 4, paragraph 70 of the Regulations on Accounting and Reporting). Include the amount of the restored reserve in other income in account 91 “Other income and expenses”;

- used when you write off bad receivables using the reserve (clause 77 of the Accounting and Reporting Regulations).

Simultaneously with the recovery, the previously arising temporary difference will be reduced or completely eliminated. Consequently, the deferred tax asset will be reduced or completely eliminated. This procedure follows from paragraph 17 of PBU 18/02 and paragraph 18 of PBU 10/99.

Reflect the repayment (reduction) of the deferred tax asset in accounting by posting:

Debit 68 subaccount “Calculations for income tax” Credit 09

– the deferred tax asset is repaid (reduced).

An example of creating a reserve for doubtful debts in accounting. No reserve is created in tax accounting

According to the supply agreement, Proizvodstvennaya LLC must make payment to Alpha LLC for the delivered goods within 30 days from the date of shipment. On May 15, Alpha shipped goods to Master in the amount of 1,200,000 rubles. As of June 15, payment from “Master” to “Alpha” had not been received. Based on the assessment of the probability of repayment of the debt, Alpha decides that the Master’s debt, which is not secured by a guarantee and has not been paid under the contract on time, is doubtful and a reserve must be created for it in the full amount. Tax accounting does not provide for the creation of a reserve for doubtful debts.

When preparing financial statements for the half-year, Master's debt was recognized as doubtful, so Alpha's accountant made the following entries:

Debit 91-2 Credit 63 – 1,200,000 rub. – a reserve for doubtful debts has been created in accordance with the order;

Debit 09 Credit 68 subaccount “Calculations for income tax” – 240,000 rubles. (RUB 1,200,000 × 20%) – a deferred tax asset is reflected.

On September 25, “Master” partially repaid the debt in the amount of 600,000 rubles. On the same date, Alpha’s accountant made the following entries:

Debit 51 Credit 62 subaccount “Settlements for shipped goods” – 600,000 rubles. – the buyer’s debt is partially repaid;

Debit 63 Credit 91-1 – 600,000 rubles. – the reserve for repaid receivables was restored;

Debit 68 subaccount “Calculations for income tax” Credit 09 – 120,000 rub. (RUB 600,000 × 20%) – the deferred tax asset in terms of the restored reserve was reduced.

Neither this nor next year, as of December 31 of the year, “Master” has not repaid the debt. Therefore, the previously created reserve must be restored. On December 31 of the following year, the following transactions will be reflected in Alpha’s accounting:

Debit 63 Credit 91-1 – 600,000 rubles. – the reserve for outstanding accounts receivable was restored;

Debit 68 subaccount “Calculations for income tax” Credit 09 – 120,000 rub. (RUB 600,000 × 20%) – the deferred tax asset is repaid in part of the restored reserve.

At the same time, on the same date, Alpha assesses the Master’s debt as doubtful, since there is no reason to recognize it as unrealistic for collection. Therefore, the organization created a reserve for doubtful debts regarding this outstanding debt:

Debit 91-2 Credit 63 – 600,000 rub. – a reserve for doubtful debts has been created;

Debit 09 Credit 68 subaccount “Calculations for income tax” – 120,000 rubles. (RUB 600,000 × 20%) – a deferred tax asset is reflected.

An example of creating a reserve for doubtful debts in accounting and tax accounting

According to the supply agreement, Proizvodstvennaya LLC must make payment to Alpha LLC for the delivered goods within 30 days from the date of shipment. On April 13, Alpha shipped goods to Master in the amount of 1,200,000 rubles. As of May 14, payment from “Master” to “Alpha” had not been received. Based on the assessment of the probability of repayment of the debt, Alpha decides that the Master’s debt, which is not secured by a guarantee and has not been paid under the contract on time, is doubtful and a reserve must be created for it in the full amount. Alpha pays income tax quarterly and uses the accrual method. The organization's accounting policy provides for the creation of a reserve for doubtful debts in tax accounting.

The cumulative revenue amounted to:

- at the end of the second quarter - 18,000,000 rubles;

- at the end of the third quarter - 25,000,000 rubles.

At the end of the second quarter, Master’s debt was recognized as doubtful, therefore, when preparing financial statements for the half-year, Alpha’s accountant made the following entries:

Debit 91-2 Credit 63 – 1,200,000 rub. – a reserve for doubtful debts was created in accordance with the order.

As of the end of the second quarter, the organization has the right to create a reserve for doubtful debts in tax accounting in the amount of 50 percent of the debt amount (debt period is more than 45 days, but less than 90). The maximum amount of the reserve at the end of the second quarter should not exceed RUB 1,800,000. (RUB 18,000,000 × 10%).

At the end of the second quarter, in tax accounting, the accountant, based on the order, reflected the creation of a reserve for doubtful debts in the amount of 600,000 rubles. (RUB 1,200,000 × 50%).

The following entry was made in the accounting records:

Debit 09 Credit 68 subaccount “Calculations for income tax” – 120,000 rubles. ((RUB 1,200,000 – RUB 600,000) × 20%) – deferred tax asset is reflected.

As of the end of the third quarter, the organization has the right to increase the amount of the reserve for doubtful debts in tax accounting to 100 percent of the debt amount (debt period is more than 90 days). The maximum amount of the reserve at the end of the third quarter should not exceed RUB 2,500,000. (RUB 25,000,000 × 10%). The reserve amount was RUB 1,200,000. (600,000 rub. + 600,000 rub.).

When preparing financial statements for nine months, Alpha’s accountant made the following entries:

Debit 68 subaccount “Calculations for income tax” Credit 09 – 120,000 rub. (RUB 600,000 × 20%) – the deferred tax asset in terms of the created reserve for doubtful debts is repaid.

In December, Alfa received information that Master had been liquidated, so the debt was recognized as unrecoverable.

The amount of the accumulated reserve in accounting is 1,200,000 rubles, in tax accounting – 1,200,000 rubles.

When preparing financial statements for the year, the accountant made the following entry:

Debit 63 Credit 62 subaccount “Settlements for shipped goods” – 1,200,000 rubles. – bad receivables are written off against the reserve.

In tax accounting, the reserve for doubtful debts was used by the organization to cover losses from bad debts in the amount of RUB 1,200,000.

Situation: how to reflect in accounting the creation of a reserve for doubtful debts if the buyer’s debt is denominated in foreign currency?

Determine the amount of the reserve based on the amount of receivables at the exchange rate of the corresponding currency on the date the reserve was created (reporting date).

Accounting for assets, liabilities and business transactions in Russia is carried out in rubles. Therefore, you should also create and change the amount of the reserve for doubtful debts in rubles. There are no exceptions here (clause 2 of article 12 of the Law of December 6, 2011 No. 402-FZ).

Based on the results of the inventory, the organization has the right to adjust the reserve in connection with the recalculation of accounts receivable at the official exchange rate of the Bank of Russia as of the reporting date. This follows from paragraph 3.54 of the Methodological Guidelines, approved by Order of the Ministry of Finance of Russia dated June 13, 1995 No. 49. If the organization does not adjust the amount of the reserve for debt denominated in foreign currency, the amount of real receivables will be distorted. Indeed, in the financial statements, accounts receivable are reflected minus the provision for doubtful debts. This ensures the reliability of information about the activities of the organization and its property status (clause 1 of article 13 of the Law of December 6, 2011 No. 402-FZ, clause 35 of PBU 4/99).

The right to tax accounting of reserves for doubtful debts

It is not necessary to reflect doubtful debts and provisions for them in tax accounting. But if the accounting department deems it necessary to do this, this right is ensured and regulated by Art. 266 Tax Code of the Russian Federation.

For tax purposes, the definition of doubtful and bad debt is no different from accounting purposes. We discussed the difference in detail above. The procedure for creating and changing the reserve for the following debts differs:

- if the debt period exceeds 3 months, then the amount of the reserve will be fully equivalent to the amount of the debt;

- if the debt payment is overdue for a period of 45 to 90 days, only half of the amount can be deposited into the reserve;

- Before the debt is 45 days overdue, changes to the reserve are not permitted.

For each doubtful debt, analytical records must be constantly maintained for a prompt response in the event of a change in the financial situation of the debtor.

NOTE! In tax accounting, the reserve for doubtful debts can be used exclusively to cover losses on written-off bad debts.

Tax reserve formation operations

In January 2021, a contract for the supply of porcelain tableware was concluded between Sovremennik JSC and Smena LLC. According to the agreement, “Sovremennik” ships “Smena” a batch of dishes in the amount of 1,341,740 rubles, payment for which must be received within 20 days after shipment. The dishes were shipped to the Smena warehouse on April 12, 2016, but payment was not received from Smena by May 3, 2016.

To reflect the operation of creating a reserve in tax accounting, the Sovremennik accountant determined the revenue, which on an accrual basis amounted to:

- as of June 30, 2016 – RUB 17,410,000;

- as of September 30, 2016 – 21,520,000 rubles.

In the tax accounting of Sovremennik, on June 30, 2016, a reserve was created for the debt “Smena:

RUB 1,341,740 * 50% = 670.870 rub.

Due to the fact that as of September 30, 2016, the payment for “Smena” was overdue for more than 90 days, Sovremennik JSC has the right to create a reserve in tax accounting in the amount of up to 100% of the debt amount. In this case, the amount of the reserve should not exceed 10% of the amount of revenue as of September 30, 2016 – RUB 2,152,000. (RUB 21,520,000 * 10%).

In the tax accounting of Sovremennik, on September 30, 2016, a reserve was created for the debt “Smena:

(RUB 1,341,740 * 50%) * 2 = RUB 1,341,740

Due to Smena being declared bankrupt, the amount of debt was written off from the reserve.

The accounting records reflect the following:

| Debit | Credit | Operation description | Sum | A document base |

| 91.2 | 63 | A reserve has been formed for the debt of “Smena” | RUB 1,341,740 | Minutes of the board's decision, accounting certificate-calculation |

| 09 | 68 “Income tax” | The amount of IT is taken into account ((RUB 1,341,740 – RUB 670,870) * 20%) | RUR 134,174 | Accounting certificate-calculation |

| 68 “Income tax” | 09 | ONA extinguished | RUR 134,174 | accounting certificate-calculation |

| 63 | 62 “Goods shipped” | The write-off of the amount of bad debt “Smenya” is reflected | RUB 1,341,740 | Minutes of the board's decision, accounting certificate-calculation |