Concept of distributable income

Distribution of dividends is the prerogative of commercial organizations whose purpose of existence is to make a profit.

A dividend is a profit received for a certain period intended for distribution among the participants of this organization. Profit can be distributed in full or in part. In the Russian Federation, commercial firms are usually created in one of 2 forms:

- in the form of a joint-stock company (JSC), guided by the Federal Law “On Joint-Stock Companies” dated December 26, 1995 No. 208-FZ;

- in the form of an LLC, applying the Federal Law “On Limited Liability Companies” dated 02/08/1998 No. 14-FZ.

In the 1st of these laws, the concept of dividends is used in relation to the payment of income (Chapter V), and in the 2nd law there is no such concept, although the issue of profit distribution is discussed in it (Articles 28, 29 of Law No. 14-FZ) .

Both of these concepts (dividend and profit distribution) are united by Art. 43 of the Tax Code of the Russian Federation, which classifies as dividends any income received by a participant or shareholder as a result of the distribution of net profit in proportion to his share of participation.

Restrictions on dividend payments

In order to distribute dividends, the mere fact of profit is not enough. Both of the above laws contain lists of very similar restrictions (Article 43 of Law No. 208-FZ and Article 29 of Law No. 14-FZ), which apply not only to the date of the decision on payment, but also to the date of payment (if the situation has changed by the time of payment ).

Limitations common to both organizational forms:

- The management company must be paid in full.

- Net assets must exceed the sum of the authorized capital and reserve fund even after payment of dividends. For a joint-stock company, the amount of the excess of the value of preferred shares over their par value is also added to the amount of the authorized capital and reserve fund.

- Signs of bankruptcy must not occur or arise as a consequence of the payment of dividends.

A special restriction for an LLC: a decision on payment is not made until the actual value of the share (or part thereof) has been paid to the retiring participant.

According to the AO, a decision cannot arise:

- until the completion of the repurchase from shareholders of shares in respect of which there is a right to demand their repurchase (Clause 1, Article 75 of Law No. 208-FZ);

- without observing the correct sequence of making a decision on the payment of dividends: first in relation to those preferred shares that have special advantages, then on other preferred shares and only then on ordinary shares.

Both laws contain a clause that under an existing payment decision that has not been implemented due to restrictions that arose at the time of payment, the issuance of dividends is mandatory after the disappearance of these restrictions.

Recommendation for payment of dividends for the 1st half of 2021

The Board of Directors of PJSC Polyus (Moscow and London Exchanges - PLZL) (“Polyus”, the “Company”) recommends paying dividends for the first six months ending June 30, 2021 in the amount of RUB 131.11 per ordinary share.

The dividend is equivalent to approximately $1.91 per common share or $0.96 per depositary share (with two depositary shares equaling one common share).1

The total amount of recommended dividends for the first half of 2021 will be RUB 17,351,049,675.96, which is equivalent to USD 253.2 million and corresponds to 30% of the Company’s EBITDA for the first half of 2021.

In accordance with the Company's current dividend policy, the amount of dividend payments for 2021 should be 30% of the Company's EBITDA for the year, but not less than US$550 million. The recommendation to pay dividends is subject to approval at the extraordinary general meeting of shareholders of the Company, which will be held on September 28, 2021. The date for compiling the list of persons entitled to receive dividends will be October 18, 2021.

Pole

Polyus is the largest gold producer in Russia and one of the top ten gold mining companies in the world in terms of production volume with the lowest costs. According to the report on ore reserves and mineral resources, it ranks second among the largest gold mining companies in the world in terms of reserves and resources.

The Group's main production facilities are located in the Krasnoyarsk Territory, Irkutsk and Magadan regions, as well as the Republic of Sakha (Yakutia).

Contacts

For investors Viktor Drozdov, Director of Investor Relations +7 [email protected]

For the media Victoria Vasilyeva, Director of Public Relations +7 [email protected]

Forward-Looking Statement

This communication may contain “forward-looking statements” regarding Polyus and/or the Polyus Group. In general, the words “will”, “may”, “should”, “should”, “continue”, “possibility”, “believes”, “expects”, “intends”, “plans”, “estimates” and other similar expressions are indicative of forward-looking statements. Forward-looking statements contain elements of risk and uncertainty that could cause actual results to differ materially from those expressed in the forward-looking statements. Forward-looking statements contain statements regarding future capital expenditures, business and management strategies, and the development and expansion of Polyus and/or the Polyus Group. Many of these risks and uncertainties involve factors that cannot be controlled or accurately estimated by Polyus and/or the Polyus Group, and therefore the information contained in these statements should not be relied upon as conclusive and are provided solely as of the date of the relevant statements. . Polyus and/or any Polyus group company undertakes no obligation and does not intend to provide any updates with respect to these forward-looking statements except as required by applicable law.

1 Based on the exchange rate established by the Central Bank of Russia of 67.1783 rubles per 1 US dollar as of August 24, 2018.

Recommendation for the payment of dividends for the 1st half of 2021 134 Kb

Frequency and methods of payment

In both forms (JSC and LLC), it is allowed to make a decision on the payment of dividends with a frequency of 1 time:

- per quarter;

- half year;

- year.

Quarterly and semi-annual distributions will be considered interim. The payment of such dividends is assessed accordingly.

IMPORTANT! Interim dividends remain dividends even if the profit at the end of the year is less than the amounts already paid in the form of dividends. There is no need to reclassify them as other income. This is important for tax purposes. Read more here.

A legal entity is not necessarily required to make a decision on the payment of income. There may also be a decision on non-distribution of profits, usually made at the end of the year.

Law No. 208-FZ directly lists the methods of paying dividends (in money or property), while Law No. 14-FZ does not indicate either the methods of payment or any restrictions on them. Thus, it is possible to pay dividends regardless of the form of the legal entity:

- cash from the cash register.

- by non-cash transfer to the participant’s bank account;

- property.

From the amount of accrued income, personal income tax (for an individual) or income tax (for a legal entity) must be withheld. For the calculation, a rate of 13% is used for residents (clause 1 of Article 224 and subclause 2 of clause 3 of Article 284 of the Tax Code of the Russian Federation) and 15% for non-residents (clause 3 of Article 224 and subclause 3 of clause 3 of Article 284 Tax Code of the Russian Federation). The question of paying tax when paying dividends to a legal entity arises regardless of what taxation regime is applied by the organization that decided to issue them.

To learn how the tax on dividends paid to a legal entity is calculated, read the article “How to correctly calculate the tax on dividends?” .

For information on the taxation of dividends from individuals, see the material “Is personal income tax levied on dividends?”

ConsultantPlus experts explained in detail what tax reporting needs to be submitted on dividends paid. Get trial access to the legal system for free and go to the K+ Guide.

The specified rates are used in relation to dividends paid in 2021, regardless of the year for which they are paid and what rate was in effect in the year for which they were accrued. For an individual, this income is taken into account separately from other income taxed at the same rate. In the case of payment of dividends to a legal entity that owns more than 50% of the capital, the rate may be 0% (subclause 1, clause 3, article 284 of the Tax Code of the Russian Federation).

For information on what needs to be done to apply a 0% rate on dividends, read the article “How to justify a zero tax rate on dividend income”

The situation of issuing dividends with property is regarded as a sale (letter of the Ministry of Finance of Russia dated December 17, 2009 No. 03-11-09/405), entailing the payment of VAT and income tax from the transferring party. At the same time, the obligation to pay tax for the recipient of dividends is not relieved. Taxes are calculated based on the market value of the property. If there is no interdependence, this value is equal to the contractual value of the transfer. The issue of establishing the market value will be significantly complicated in the case of interdependence of persons (participation share of more than 20%) and the presence of constituent entities of the Russian Federation among the participants.

How is the payment decision made?

This decision is made by the general meeting:

- shareholders in the joint-stock company (clause 3 of article 42 of law No. 208-FZ).

- participants in an LLC (Clause 1, Article 28 of Law No. 14-FZ).

The financial statements for the relevant period must be ready for the meeting, their data must be analyzed to ensure compliance with the restrictions established for making a decision on payment, and the amount of profit that can be used to pay dividends must be determined.

The result of the meeting is a protocol, which, when executed by the JSC, must contain (clause 2 of Article 63 of Law No. 208-FZ) the following:

- time and place of the meeting;

- the total number of votes and votes of meeting participants;

- information on the election of the chairman and secretary;

- agenda;

- the results of consideration of each of the issues;

- final decision.

The listed data will not be superfluous in the protocol drawn up by the LLC.

With regard to dividends, the meeting of the joint-stock company must decide on the following points:

- for what period they are paid;

- total payment amount and size for each type of shares;

- the date on which the composition of shareholders will be determined;

- form and time of payment.

For LLCs, the following are excluded from this list:

- the amount of dividends for each type of shares;

- the date on which the composition of shareholders will be determined.

The distribution of the total amount between specific persons is carried out:

- in JSC - according to the algorithm laid down in the charter, depending on the types and number of shares;

- in an LLC - in proportion to shares, unless the charter contains a different order.

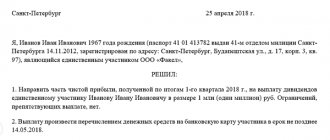

The general meeting is not held by the sole founder. It is enough for him to make a decision on the payment of dividends, formalizing it as any of his decisions, indicating the date of preparation and the essence of the issue on which the decision is being made.

Terms of payment of dividends in LLC

For an LLC, the period for issuing dividends is limited to 60 days from the date of the decision (Clause 3, Article 28 of Law No. 14-FZ). A specific period within these 60 days may be established by the charter or a meeting of participants. If such a period is not recorded in the LLC documents, it is equivalent to 60 days.

Important! “ConsultantPlus” warns that if you violate the deadline for paying dividends, as well as if you do not pay them, the consequences may be different depending on whose fault the violation occurred. Read more about the consequences in K+.

Procedure and terms of payment of dividends

Dividends in 2021 are paid based on the decision of the general meeting of shareholders (participants).

Many business owners are interested in whether it is possible to pay dividends in installments. The law allows you to do this once every quarter, half year or year. Because net profit is finally determined only at the end of the year, then quarterly and semi-annual payments are interim dividends.

The dividend payment date is tied to the date of the decision of the general meeting. For a joint stock company, the “cut-off” day is first determined, i.e. the date on which the list of persons entitled to receive them is recorded. The cutoff for dividends for 2021 should be set no earlier than 10 and no later than 20 days after the decision on payment is made (clause 5 of Article 42 of Law No. 208-FZ). The actual payment of dividends must be made within 10 days from the cut-off date - to nominee holders and trustees, and within 25 days - to all other shareholders.

For an LLC, the period for paying dividends should not exceed 60 days from the date of the decision (Clause 3, Article 28 of Law No. 14-FZ). The charter or minutes of the meeting of participants may provide for a shorter period. If it is not specified, then “by default” dividends must be issued within the 60-day period established by law.

The method of payment of dividends does not depend on the form of the legal entity. This may be the issuance of funds (both cash and non-cash) or the transfer of property.

When paying dividends, the company performs the functions of a tax agent for income tax or personal income tax, depending on the category of the income recipient.

For individuals, the personal income tax rate is 13% for residents (in the 2-NDFL certificate, the dividend income code is 1010) and 15% for non-residents (Article 224 of the Tax Code of the Russian Federation). The same rates (13% and 15%), depending on the resident status, are applied to income tax for legal entities (clause 3 of Article 284 of the Tax Code of the Russian Federation).

If the organization receiving the dividends owns over 50% of the authorized capital of the payer for a year or more, then a preferential rate of 0% is applied.

In this case, taxes are calculated taking into account whether the payer company, in turn, is the recipient of dividends. In this case, for dividend tax, the calculation formula is as follows:

- Н = К x Сн x (Д1 – Д2) К – share of dividends attributable to a specific recipient;

- Сн - tax rate on dividends

- D1 – total amount of dividends

- D2 - dividends received by the organization in the past or previous periods and not previously used to calculate taxes.

The above formula does not apply to payments in favor of non-residents. For them, the tax is calculated based on the total amount of dividends paid by the company (clause 6 of Article 275 of the Tax Code of the Russian Federation)

Consequences of failure to pay dividends on time

Both laws provide the same procedure for situations of non-payment of dividends on time. They can be claimed by the participant within 3 years (or 5 years if this is stated in the charter) from the date:

- making a decision on payment to the JSC (clause 9 of Article 42 of Law No. 208-FZ).

- completion of the 60-day period in the LLC (Clause 4, Article 28 of Law No. 14-FZ).

If dividends are unclaimed at the end of these periods, they are returned to profit and claims for them are no longer accepted.

The legislation does not provide for any sanctions for exceeding the deadline for paying dividends. The consequences may be that the participants go to court demanding the payment of not only dividends, but also interest for the delay in their transfer. If it is proven that the JSC that accrued the dividends opposes their payment, then a fine is possible under Art. 15.20 of the Code of Administrative Offenses of the Russian Federation in the amount of:

- from 20,000 to 30,000 rub. for officials;

- from 500,000 to 700,000 rubles. for legal entities.

For information on the rules for reporting dividends in the 6-NDFL report, read the material “How to correctly reflect dividends in the 6-NDFL form?”

Reflection of dividend payments in accounting

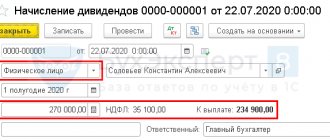

For clarity, we will consider the reflection of payment of income to participants using an example.

Example 3

Olympus LLC decided to distribute profits and pay dividends to participants in the following amounts:

- Petrov P.P. — 35,000 rubles, incl. Personal income tax - 4,550 rubles (resident of the Russian Federation, not an employee of the company);

- Fedorov F.F. — 20,000 rubles, incl. Personal income tax - 2600 rubles (resident of the Russian Federation, is an employee of the company);

- LLC "Meridian" - 45,000 rubles, incl. Income tax - 5850 rubles (resident of the Russian Federation).

The accountant of Olympus LLC must make the following entries:

DEBIT 84 CREDIT 75

— 35,000 rub. – dividends were accrued to Petrov P.P.;

DEBIT 84 CREDIT 75

— 45,000 rub. – dividends accrued to Meridian LLC;

DEBIT 84 CREDIT 70

— 20,000 rub. – dividends were accrued to Fedorov F.F.;

DEBIT 75 CREDIT 68

— 4550 rub. – personal income tax was withheld from the income of Petrov P.P.;

DEBIT 75 CREDIT 68

<- 5850 rub. – income tax was withheld from the income of Meridian LLC.

DEBIT 70 CREDIT 68

— 2600 rub. – personal income tax was withheld from the income of Fedorov F.F.;

DEBIT 70 CREDIT 50 (51)

— 17,400 rub. – dividends were paid (transferred) to Fedorov F.F.;

DEBIT 75 CREDIT 50 (51)

— 30,450 rub. – dividends were paid (transferred) to Petrov P.P.;

DEBIT 75 CREDIT 51

— 39,150 rub. – dividends of Meridian LLC are listed;

DEBIT 68 CREDIT 51

— 7150 rub. – the withheld personal income tax is transferred to the budget;

DEBIT 68 CREDIT 51

— 5850 rub. – the withheld income tax is transferred to the budget.

Olga Fedun

, for the magazine “Practical Accounting”

Help your business grow

Invaluable experience in solving current problems, answers to complex questions, specially selected latest information in the press for accountants and managers. Choose from our catalog >>

If you have a question, ask it here >>

Results

The period for paying dividends in an LLC is 60 days from the date of the decision to pay them, unless a different period is established by the charter or meeting of the company’s participants. In a JSC, the period for paying dividends depends on the recipient: 10 days from the date of the decision for payment to nominee holders and trustees, and 25 days for payment of dividends to other shareholders.

Sources:

- Tax Code of the Russian Federation

- Law of 02/08/1998 N 14-FZ “On Limited Liability Companies”

- Law of December 26, 1995 N 208-FZ “On Joint Stock Companies”

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

When can dividends be paid?

In accordance with the law, a limited liability company can distribute profits quarterly, every six months or every year (Clause 1, Article 28, Law No. 14-FZ dated 02/08/1998). The maximum payment period is 60 days from the date of the decision. Participants can independently determine the payment period by specifying it in the company’s charter or in the decision on the distribution of profits. If information about the timing is not documented, then dividends must be paid within 60 days.

But what to do if the deadline for dividend payments has passed, and the participants still have not seen their money? In this case, the founders have the right, within three years after the end of the payment period, to contact the company with a demand to receive their share of the income. By the way, the period can be extended to five years if this is specified in the company’s charter.