On the basis of what documents is a bank guarantee reflected in accounting?

According to accounting standards, all transactions reflected in the accounts must be supported by documents. It does not matter whether balance sheet accounts are involved or off-balance sheet accounts.

Based on the norms of Ch. 23 of the Civil Code of the Russian Federation, the principal and the guarantor are not required to draw up a bank guarantee in a separate agreement. However, bankers do not trust the oral form of agreements and describe the nuances of relations with the principal in a separate document - an agreement on the issuance of a bank guarantee.

Such an agreement usually contains all the necessary data for which the beneficiary can make entries in his accounting (guarantee amount, validity period, etc.).

The guarantee can also be issued in electronic form. It is drawn up in the form of an electronic document, which has the same legal force as its paper counterpart. Documents are signed with an electronic signature, which gives the electronic document legal force. If necessary, a paper version of the electronic guarantee can be requested from the bank.

“Not every bank can act as a guarantor to the tax office” will introduce you to the tax nuances of accounting for a bank guarantee .

We will describe below how a bank guarantee is reflected in accounting.

Accounting

Let's consider the rules for reflecting in accounting the amounts provided by procurement participants as security for the execution of the contract.

The amount of funds contributed by the procurement participant. As we noted above, on the basis of Art. 96 of Law No. 44-FZ, funds provided by procurement participants as security for participation in the execution of the contract are credited to the account specified by the customer in the procurement documentation and which, in accordance with the legislation of the Russian Federation, accounts for transactions with funds received by the customer. When the supplier (performer) fulfills the obligations stipulated by the contract, the funds contributed as security for the execution of the contract must be returned to the procurement participant with whom the contract was concluded. In other words, the said funds are at the customer’s disposal temporarily.

Funds that, upon the occurrence of certain conditions, are subject to return to the owner, refer to funds at the temporary disposal of the customer (institution) (Letter of the Ministry of Finance of the Russian Federation dated October 8, 2014 No. 02‑07‑07/50609). According to section V of Instructions 65n, transactions leading to an increase (decrease) in funds and not related to the income (expenses) of institutions, including the receipt (disposal) of funds at the temporary disposal of an autonomous (budgetary) institution, are reflected using Article 510 “Receipts to accounts budgets" (Article 610 "Disposal from budget accounts") of KOSGU.

Thus, funds received as security for the execution of a contract are accounted for in accounting as funds received for temporary disposal, indicating in the 19th – 23rd digits the account number of code 3 “Funds in temporary disposal” (clause 21 of the Instructions No. 157n).

In accordance with paragraph 267 of the said instructions, account 304 01 000 “Settlements for funds received at temporary disposal” is intended to account for amounts received at the temporary disposal of the institution and upon the occurrence of certain conditions subject to return. Accounting for transactions on this account is kept in the journal of transactions with non-cash funds (clause 269 of Instruction No. 157n).

The Letter of the Ministry of Finance of the Russian Federation dated June 27, 2014 No. 02‑07‑07/31342 clarifies that funds received as security for the execution of a contract cannot be accounted for in off-balance sheet account 10 “Security for the fulfillment of obligations.”

The sports school (budgetary institution) established a requirement in the procurement documentation to ensure the execution of the contract. As such security, the contractor with whom it is planned to conclude a contract transferred funds in the amount of 200,000 rubles to the customer’s account. After completing the work and signing the relevant act, the customer returned the security amount to the contractor.

In the accounting records of a budgetary institution, transactions will be reflected as follows:

| Debit | Credit | Amount, rub. | |

| The funds received as security for the execution of the contract have been transferred to the personal account of the institution | 3 201 11 510 | 3 304 01 730 | 200 000 |

| The funds received as security for the execution of the contract were returned to the contractor | 3 304 01 830 | 3 201 11 610 | 200 000 |

The amount of the bank guarantee provided. Bank guarantees provided to secure participation in a competition (closed auction), as well as to secure the execution of a contract, by virtue of clause 351 of Instruction 157n, are subject to accounting in off-balance sheet account 10 “Security for the fulfillment of obligations.”

According to Letter of the Ministry of Finance of the Russian Federation dated June 27, 2014 No. 02-07-07/31342, security for an obligation in the form of a bank guarantee is reflected in this account on the date of provision of this guarantee. The disposal of a bank guarantee from accounting on off-balance sheet account 10 (reflected in the account with a minus sign) is reflected by the date of termination of the obligation to secure the said guarantee (the date of fulfillment by the supplier (performer) of the obligations secured by the guarantee, or the date of fulfillment by the bank of the customer’s demands for payment of a sum of money in connection with the violation by the supplier (performer) of the obligation to secure which the guarantee was issued).

The autonomous sports institution (customer) has established in the procurement documentation a requirement to ensure the execution of the contract. The supplier with whom it is planned to conclude a contract has chosen to provide a bank guarantee as security. The amount of the bank guarantee is RUB 170,000. The contract period is two months. The bank guarantee was issued by the supplier's bank for three months.

In the accounting records of an autonomous institution, the amount of the bank guarantee will be reflected as follows:

| Debit | Credit | Amount, rub. | |

| The amount of the bank guarantee accepted by the customer as security for the execution of the contract has been received | 10 | – | 170 000 |

| The amount of the bank guarantee was written off as of the date the supplier fulfilled the contractual obligations to secure which such a guarantee was issued | – | 10 | 170 000 |

Withholding the security amount against the unreturned advance. Ensuring the execution of a contract in its meaning is a guarantee of the fulfillment by the supplier (performer) of obligations under the contract. In addition, the specified security guarantees the customer the return of the previously transferred advance, for example, in the event of termination of the contract.

The question arises: can the customer withhold the amount of security provided by the supplier (performer) against the unreturned advance payment?

Explanations on this matter are given in the Letter of the Ministry of Finance of the Russian Federation dated December 25, 2014 No. 02-02-04/67438 and the Federal Treasury No. 42-7.4-05/5.1-805 “On the use of contract performance security provided by the supplier (contractor, performer) in connection with failure to fulfill obligations related to the return of the advance payment" (hereinafter referred to as the Letter dated December 25, 2014). It states that if, upon termination of the contract, the contractor (supplier) violates the obligations to return the advance payment, to secure the fulfillment of which funds or a bank guarantee are provided, the said security may be retained by the customer under the terms of the contract or a demand for payment of funds is sent in relation to the specified security according to the Civil Code of the Russian Federation.

If the customer under the contract is a budgetary (autonomous) institution, the amounts of the retained collateral are subject to transfer to the appropriate account in which transactions with the institution’s funds are recorded and from which the obligations under the contract were paid (advance transfer), and used to fulfill the obligation with clarification of the financial plan. economic activity of a state (municipal) institution. In this case, the amounts of retained collateral received:

- during the financial year in which the obligations under the contract were paid - are recorded in the corresponding personal account of the state (municipal) institution as a restoration of cash expenses;

- after the end of the financial year, if the source of financial support under the contract was a subsidy for financial support for the fulfillment of a state (municipal) task, they are taken into account in the personal account of a budgetary (autonomous) institution and are reflected in the plan of financial and economic activities of the institution as amounts of receivables from previous years that arose in connection with the violation of obligations related to the execution of the contract, under Article 130 “Income from the provision of paid services (work)” of the KOSGU.

If the customer under the contract is the recipient of budget funds, the amounts of the withheld security are subject to transfer to the budget revenue of the public legal entity to meet the needs of which the state (municipal) contract was concluded. These revenues are reflected according to the income code 000 1 1300 130 “Revenue from compensation of state expenses” using the corresponding codes of subarticles, elements and subtypes of budget income provided for by Instructions No. 65n.

In addition, the Letter dated December 25, 2014 contains the correspondence of invoices regarding the withholding of the amount of the provided security against the unreturned advance. Let's look at how to use it using an example.

A budgetary institution of physical culture and sports (customer), using a subsidy for the implementation of a state task, entered into a contract for the installation of electricity meters in the amount of 110,000 rubles. The contractor transferred funds in the amount of the advance payment (40,000 rubles) to the customer’s account as security for the execution of the contract. The contract was then terminated. Due to the fact that the contractor did not return the amount of the transferred advance, the amount of the received security was withheld against him.

These transactions will be reflected in the accounting of a budgetary institution as follows:

The fact of receipt/issuance of a bank guarantee in the records of the principal and beneficiary

To account for the cost of the bank guarantee, the beneficiary has an off-balance sheet account 008 “Securities for obligations and payments received.” The received collateral is written off off-balance sheet as the debt is repaid. The beneficiary must keep analytical records for each security received.

There are two positions regarding the reflection of a bank guarantee by the principal in accounting:

Position 1: the principal does not reflect the bank guarantee in his accounting.

Supporters of this position explain their point of view by the fact that the principal of the bank guarantee:

- receives not for himself, but for the beneficiary (his creditor);

- does not issue a guarantee (it is issued by the bank).

Consequently, there are no grounds for the principal to use off-balance sheet accounts 008 “Securities for obligations and payments received” and 009 “Securities for obligations and payments issued” to account for the bank guarantee.

Position 2: the principal needs to reflect the bank guarantee on the balance sheet.

This approach allows:

- take into account the fact of a change of creditor if the principal fails to fulfill an obligation (when the guarantor becomes a creditor instead of a beneficiary);

- reflect additional sanctions established by agreement with the guarantor (for example, special penalties for late fulfillment of obligations to the guarantor).

The accuracy of the assessment by external users of the financial statements of the state of the principal's accounts payable depends on how reliable the information about the bank guarantee reflected on the off-balance sheet accounts is. Reflection of a bank guarantee in the accounting of the principal is of particular importance if the transaction is large and subject to disclosure in the financial statements.

You will find the criteria for a major transaction with explanations in the Ready-made solution from ConsultantPlus. Trial access to the legal system is free.

Accounting entries for securing an application for participation in a procurement

————————————————————————- *(1) The choice of a settlement account depends on the timing of the decision to offset the provided collateral against payment of obligations under the contract. If the decision is made earlier than the date of occurrence of obligations under the contract, then the non-cash transaction is reflected using account 4,206,24,000).

Having considered the issue, we came to the following conclusion: In the accounting of a budgetary institution, the costs of acquiring the right to conclude a water use agreement should be reflected using the expense type code 244 “Other purchase of goods, works and services to meet state (municipal) needs” in connection with the subarticle 224 “Rent for the use of property” KOSGU.

Entries in the accounting of the beneficiary and the principal in case of failure to fulfill the obligation

The principal does not always manage to fulfill his obligations to the beneficiary in a timely manner. In this case, the beneficiary may demand in writing from the guarantor payment of the amount not received under the agreement.

After receiving documents from the beneficiary and considering his request for compliance with the terms of the issued guarantee, the guarantor makes a decision to pay the principal’s debt (Articles 374-375 of the Civil Code of the Russian Federation).

After the claim is accepted by the guarantor, the beneficiary makes the following entries in the accounting records:

The bank informs the principal:

- about termination of the warranty;

- the need to reimburse the amount paid by the bank to the beneficiary under the guarantee.

Having received a notification from the bank, the principal reflects the bank's recourse claims in his accounting. We will show you with an example what transactions are used to pay for a bank guarantee.

Greenwich LLC issued a bank guarantee for a period of 1 month, but during this period it failed to pay the seller Corrida LLC the amount of 12,378,533 rubles stipulated in the purchase and sale agreement. The bank, which paid off this obligation for Greenwich LLC, demanded that it reimburse the amount paid.

Two entries will appear in the principal’s accounting:

| Accounting entries | Amount, rub. | Contents of operation | |

| Debit | Credit | ||

| 60 | 76 | 12 378 533 | The bank's recourse claim was recognized |

| 76 | 51 | 12 378 533 | The obligation to the bank has been repaid |

Securing the contract.

What postings need to be made indicating the KPS.

To clarify uncleared receipts, send a clarification notice to the OFK. A new analytical account has been added: 0.205.82.000 “Calculations for uncleared receipts”.

In accounting, we recommend reflecting uncleared receipts with the following entries: Debit 180.0.210.11.180 Credit 180.0.205.82.660 – the amount of income that requires clarification is accrued upon receipt of these amounts. Upon clarification, a reverse entry is made: Debit 180.0.205.82.560 Credit 180.0.210.11.180 This accounting entry is prescribed in the amendments to Instruction No. 162n, adopted in 2015, for government institutions, following the unified accounting methodology, this entry can be applied for budgetary institutions. But since this wiring is not specified in instruction 174n, we recommend that you coordinate it with a higher-level organization.

At the same time, we make an entry for the receipt of funds as a restoration of cash expenses: Debit 000.0.201.11.510 Credit 510.0.210.05.660 – Money to secure the application was returned to the account of the procurement participant Increase in off-balance sheet account 17 (analytics code 510) Justification How to take into account money to secure the application or execution of a contract for procurement under Law No. 44-FZ In the accounting of budgetary institutions: In accounting, make the following entry: No. Contents of the transaction Account debit Account credit 1. Money to secure the application was transferred to the account of the customer or operator of the electronic signature 0.210.05.560 0.201.11.610 Increase in off-balance sheet account 18 (analytics code 610) When the customer or electronic signature operator returns the security funds, reflect them under the KOSGU article

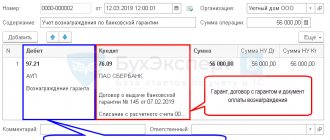

Example of transactions with a beneficiary: receipt and write-off of a guarantee

Let's look at an example that helps the beneficiary navigate the main entries in accounting.

Trading LLC purchased a batch of goods worth RUB 1,693,461. on deferred payment terms. The seller PJSC Delivery requested a bank guarantee as security for the payment obligation.

Postings to the beneficiary (PJSC "Supply") after receipt of the guarantee and delivery of the goods:

| Accounting entries | Amount, rub. | Contents of operation | |

| Debit | Credit | ||

| 008 | — | 1 693 461 | The received bank guarantee is reflected on the balance sheet |

| 62 | 90 | 1 693 461 | The goods were shipped to the buyer LLC Trading |

The buyer did not pay for the goods within the period specified in the contract. PJSC "Supply" sent a written message to the bank about the need to pay the principal's debt under the bank guarantee, attaching the necessary documents.

After reviewing the documents and checking them, the bank transferred the money under the guarantee. The following entries were made in the accounting of PJSC Supply:

| Accounting entries | Amount, rub. | Contents of operation | |

| Debit | Credit | ||

| 51 | 76 | 1 693 461 | Received money from the bank under a guarantee |

| 76 | 62 | 1 693 461 | The debt of Trading LLC has been repaid |

| — | 008 | 1 693 461 | Payment security written off from off-balance sheet accounting |

If the buyer repaid the debt for the goods on time, there would be significantly fewer accounting entries in the beneficiary's accounting. Everything would be limited to reflecting and writing off the received collateral in an off-balance sheet account.

Correct postings of collateral in accounting

In a situation where an organization transferred funds to a municipal or state customer before a decision on the tender was made, this operation cannot be carried out as an expenditure of funds, because the deposit here serves the function of certifying intentions to implement the terms of the contract.

In this case, the following entry should be made: D 76 subaccount “Settlements for the listed deposit” K 51 with a note - deposit in favor of the organizer of electronic trading. Further, regardless of whether the participant lost or won the tender, according to the rules established by Federal Law No. 44, the customer is obliged to return the funds of the financial collateral within the prescribed period. And here, again, we are faced with the fact that this receipt cannot be considered the income of the enterprise, because it is simply a return of the security deposit. Therefore, the posting must be appropriate, the reverse of what was made earlier when making a deposit - D 51 K 76 of the subaccount “Settlements for the transferred deposit” (return of the deposit payment).

At first glance, in addition to the labor resources required to carry out accounting entries, the participating organization does not lose anything - the same funds that were deposited as direct collateral are returned back after some time. But we should not forget that high inflation rates daily eat up finances that are frozen and not working in deposit accounts. From this point of view, losses can be quite obvious, especially if we talk about large government contracts with large sums.

How to solve the problem of provision in the most optimal way for all interested parties?

What affects the accounting treatment of payment of a fee for issuing a guarantee?

Issuing a guarantee is a paid service. The credit institution's fee for issuing a guarantee can be set in different ways:

- in a fixed amount;

- as a percentage of the guarantee amount;

- in a different way.

In addition, the guarantor may establish additional conditions for paying the commission for issuing a bank guarantee. He may require the principal to pay the commission in one lump sum in full or in installments during the validity period of the guarantee.

All this affects not only the accounting procedure for this type of expense, but also requires the principal to additionally elaborate his accounting policy (we will talk about this in subsequent sections).

Find out what to consider when drawing up your accounting policies in 2021 in this publication .

Next, we will talk about the nuances of accounting for the commission for issuing a bank guarantee and the entries used to reflect this type of expense.

Costs of providing electronic trading

In a broad sense, ensuring participation in bidding on electronic platforms is not limited only to the security payment as such. The company bears the necessary costs, without which participation in the auction is impossible. They must be reflected correctly in accounting, also guided by the norms of the Tax Code of the Russian Federation.

Let's look at the most common correspondence accounts. Services of an electronic platform as costs associated with the preparation of tenders can be deducted for VAT for tax purposes if there is an invoice and the provisions of Art. 172 of the Tax Code of the Russian Federation. Based on bank documents, acts and invoices from the electronic operator, accounting entries are made:

For income tax purposes, organizers classify such expenses as other expenses related to production and sales, by type (Article 264 of the Tax Code of the Russian Federation). An entry is made in the BU: Dt 91-2 Kt 60 (76).

A bank guarantee, as one of the types of tender security, is of a paid nature. The commission is reflected by postings:

- Dt 91-2 Kt 76 (60) – fixed bank commission.

- Dt 76 (60) Kt 51 – bank commission paid from the current account.

On a note! Making a security payment is not taken into account for tax purposes, in income and expenses in calculating the base for income tax, VAT until the winner is determined. Then he can receive a VAT deduction if the amount is an advance payment (payment) for participation in the competition and the subject of the auction was the conclusion of an agreement. A similar principle applies when calculating income tax.

The acquisition of digital signature is reflected according to Dt 97, from the credit of accounts payable to suppliers. In this case, the media, disk, if it is highlighted in the documentation, is immediately written off as expenses - Dt 20,26, 44, etc. Kt 60 (76). The electronic key, certificate, and the cost of warranty service are written off evenly over the entire period that the key will be used (usually a year) - Dt 20,26,44, etc. Kt 97.

Main

- Accounting for the opportunity to participate in electronic trading and deposits is carried out on account 76 or on account 55, using subaccounts.

- The use of account 55 is exceptional when it comes to government procurement in accordance with Federal Law No. 44.

- To strengthen control over the movement of funds, use off-balance sheet account 009.

- Other costs that ensure participation in trading are taken into account by standard accounting entries, in accordance with the recommendations for the use of the Chart of Accounts, taking into account the provisions of the Tax Code of the Russian Federation.

- Accounting entries depend on the stage at which the application is located, the results of the auction, and the form of securing participation in it.

Two types of entries to reflect the commission on a bank guarantee when purchasing property

The supplier of expensive equipment or the seller of the building may make it a mandatory condition when concluding an agreement with the buyer that there is a bank guarantee. In the buyer's accounting, the guarantor's remuneration will be recognized as an expense. However, the accounting for this expense will be different depending on the moment at which it was made: before the purchased property is registered or after it. In each case, a different set of accounting entries is applied to reflect the commission for issuing a bank guarantee.

- The guarantor's remuneration was paid before the acquired property was reflected in the accounting accounts.

What entries are used to record a bank guarantee from the principal in such a situation? The amount of remuneration to the guarantor is included in the cost of the acquired asset, since this expense is directly related to its acquisition (clause 6 of PBU 5/01 “Accounting for inventories”, clause 8 of PBU 6/01 “Accounting for fixed assets”).

For such a case, the following set of transactions is used:

The specified accounting scheme reflects the transactions for payment of the bank guarantee and for its reflection in accounts payable until the transfer of money by the principal.

PJSC "Modern Technologies" plans to purchase an office building worth RUB 150,364,199. from Real Estate+ LLC. As security for obligations, the buyer provided the seller with a bank guarantee.

Warranty conditions:

- remuneration to the bank (4% of the transaction amount) - 6,014,568 rubles. (RUB 150,364,199 × 4%);

- Warranty period - 1 month;

- The procedure for paying the commission is the entire amount at a time.

PJSC Modern Technologies paid the commission and purchased the property from the seller. The following entries were made in accounting:

| Accounting entries | Amount, rub. | Contents of operation | |

| Debit | Credit | ||

| 76 | 51 | 6 014 568 | Commission transferred to the guarantor bank |

| 08 | 76 | 6 014 568 | The amount of remuneration to the guarantor is included in the cost of the building |

| 08 | 60 | 150 364 199 | The cost of the building is reflected in non-current assets |

| 01 | 08 | 156 378 767 (150 364 199 + 6 014 568) | The building is included in the principal's fixed assets |

We talk about the nuances of tax accounting for a bank guarantee in this article.

- The guarantee is issued after the value of the asset has been generated.

Here, accounting standards do not allow the amount of the guarantor's remuneration to be taken into account in the initial cost of the asset. Once the accounting value of the property has been formed, it is not allowed to change it.

In such a situation, other expenses are recognized and postings are made:

The situation is dangerous if the remuneration to the guarantor, paid before the initial cost of the asset is formed, is taken into account as part of other expenses. This will cause a distortion in the amount of property tax, which is calculated according to accounting data. Considering that from 2021 the value of movable property is excluded from the tax base, the unlawful write-off of remuneration to the guarantor as part of other expenses will distort the property tax base if the buyer purchased real estate.

Necessary transactions when returning contract security funds.

When the customer returns the collateral, reflect it under article KOSGU 510 “Receipt to budget accounts” and make the following entry: Debit 0.201.11.510 Credit 0.201.05.660 - money to secure the application was returned to the account of the procurement participant; Increase in off-balance sheet account 17 (analytics code 510).

In accordance with Part 2 of Art. 93 of the Federal Law of 04/05/2013 No. 44-FZ (hereinafter referred to as Law No. 44-FZ), a notice of purchase from a single supplier (contractor, performer) is placed in the Unified Information System only if such a purchase is carried out on the basis of paragraphs. 1 – 3, 6 – 8, 11 – 14, 16 – 19 hours.

This procedure is established by paragraphs 72, 98 of Instruction No. 174n, paragraph 235 of the Instruction to the Unified Chart of Accounts No. 157n and confirmed by letter of the Ministry of Finance of Russia dated August 1, 2021 No. 02-06-10/45133. An example of filling out the Report on the implementation by an institution of its financial and economic activity plan (f. 0503737), if the amounts of security for the execution of the contract were transferred as a participant, is given below.

Justification How to take into account money to secure an application or execution of a contract for procurement under Law No. 44-FZ In the recommendation, we will tell you how to reflect the monetary security of an application or contract to an institution: - a procurement participant; - a customer. We will also explain how the customer can take into account the bank guarantee received from the supplier.

How to take into account application security When a customer conducts a tender, auction or request for proposals, he requires application security from procurement participants. To secure the application, the participant transfers a cash deposit to the customer or provides a bank guarantee. According to which CWR and KOSGU should the procurement participant reflect the monetary security of the application? Budgetary and autonomous institutions In budgetary and autonomous institutions, calculations for securing applications are not expenses, but reduce the balance on the personal account.

Features of accounting policies and entries when reflecting remuneration to the guarantor under a loan agreement

The borrower may incur expenses for paying remuneration to the guarantor when issuing a guarantee is one of the conditions for receiving borrowed funds. In such circumstances, it is necessary to take into account the norms of PBU 15/2008 “Accounting for expenses on loans and credits”:

- according to clause 7, borrowing costs are classified as other expenses;

- According to clause 8, it is allowed to recognize additional expenses on loans evenly as part of other expenses during the period of validity of the loan agreement.

How the borrower will write off additional expenses on loans, he must indicate in his accounting policy:

What postings are used in accounting in this case, see the figure below:

Whatever method of recording loan costs in the form of remuneration to the guarantor the borrower chooses, the accounting accounts used will be the same.

Accounting records in a budgetary (autonomous) institution

The transfer by a budgetary (autonomous) institution of funds to secure an application to a special bank account and their blocking can be reflected as follows:

- Debit 0 201 26 510 (increase 17, KOSGU 510) Credit 0 201 11 610 (increase 18, KOSGU 610) - funds were transferred to secure the application to a special bank account;

- Debit 0 210 05 560 Credit 0 201 26 610 (increase 18, KOSGU 610) - the blocking of collateral funds in a special bank account is reflected;

- Debit 0 201 26 510 (increase 17, KOSGU 510) Credit 0 210 05 660 - the removal of the blocking of collateral funds in a special bank account is reflected;

- Debit 0 201 11 510 (increase 17, KOSGU 510) Credit 0 201 26 610 (increase 18, KOSGU 610) - reflects the return of collateral from a special account in the bank.

More on the topic: KOSGU in 2021

Bank guarantee under a government contract: what type of expense and how to take it into account?

If a bank guarantee is required to fulfill obligations under a government contract (or government order), the amount of remuneration to the guarantor can be taken into account as:

- expenses for ordinary activities; or

- other expenses.

Whether the guarantor's remuneration is taken into account at one time or gradually depends on the type of company's obligations secured by the guarantee:

The correspondence of accounts for accounting for remuneration to the guarantor is similar to those described above:

The materials on our website will introduce you to the nuances of concluding and executing government contracts:

- “Concluding a contract without limits on budgetary obligations”;

- “Is it legal to pay UTII when selling goods under state and municipal contracts?”.

ACCOUNTING FOR CASH SECURITIES AND DEPOSITS

When holding competitions and auctions, the customer is obliged to establish requirements for securing applications (Part 1, Article 44 of Law No. 44-FZ). Applications may be secured in cash or by a bank guarantee. The choice of supply method is made by the procurement participant. Security for an application for participation in electronic auctions can be provided by the procurement participant only by depositing funds (Part 2 of Article 44 of Law No. 44-FZ). The procurement participant must have a sufficient and unblocked amount in a personal account opened by the operator of the electronic platform. The specific amount of collateral that is blocked on the account is determined by the auction documentation (Part 16, Article 44 of Law No. 44-FZ). Funds to secure the application must be deposited in a timely manner, since if the participant’s money does not reach the customer’s account before the date of consideration of the applications, such participant is recognized as not having provided security. This rule does not apply when conducting an electronic auction (Part 5, Article 44 of Law No. 44-FZ). At the end of the competition, funds are usually returned to the participant’s account. Refunds are made when conducting a competition and a closed auction within no more than 5 working days, and when conducting an electronic auction, the blocking of such funds ceases within no more than one working day from the date of one of the following cases: 1) signing of review and evaluation protocols applications for participation in the competition, summing up the results of electronic or closed auctions. In this case, the return or termination of blocking is carried out in relation to the funds of all procurement participants, with the exception of the winner of the determination of the supplier (contractor, performer), to whom such funds are returned after the conclusion of the contract; 2) cancellation of the determination of the supplier (contractor, performer); 3) rejection of the procurement participant’s application; 4) withdrawal of the application by the procurement participant before the deadline for submitting applications; 5) receipt of an application for participation in determining the supplier (contractor, performer) after the deadline for submitting applications;

This is interesting: Phone number where you can find out whether there will be an amnesty for citizens of Tajikistan in Russia

Collateral in the contract system

Most often, state (municipal) institutions come across applications for participation in competitions or auctions or contract performance security in accordance with Federal Law No. 44-FZ dated 04/05/2013 on the contract system (hereinafter referred to as Law No. 44-FZ). In this case, institutions can act on both sides - both on the part of the customer receiving the security, and on the side of the tender participant transferring the monetary security, since the mandatory requirements for securing an application for participation in the competition apply equally to all procurement participants. A state (municipal) institution, with the exception of a government institution, which won the competition and became the executor, is subject to the requirements for ensuring the execution of the contract.

Federal Law No. 44-FZ dated 05.04.2013 “On the contract system in the field of procurement of goods, works, services to meet state and municipal needs” (hereinafter referred to as Law No. 44-FZ) established requirements for securing applications during competitions and auctions (Article 44) and to ensure the execution of the contract (Article 96).

Results

When reflecting a bank guarantee, the beneficiary and the principal use accounting entries using balance sheet and off-balance sheet accounts. The fact of receipt and write-off of the guarantee is recorded on the balance sheet. And when reflecting the costs of paying the commission for its issuance, the correspondence of accounts 51 “Current accounts” and 76 “Settlements with various debtors and creditors” is used. The costs of paying remuneration to the bank for issuing a guarantee are reflected in the accounts depending on the type of asset for the acquisition of which it was issued. If the initial cost of the asset has not been formed and the commission is paid, its amount increases the initial cost. In other cases, the commission is taken into account as another expense and is reflected in accounting in account 91.2 “Other expenses”.

Sources: Civil Code of the Russian Federation

You can find more complete information on the topic in ConsultantPlus. Free trial access to the system for 2 days.

Account correspondence:

Civil relations

Relations related to the placement of orders for the supply of goods for state needs are regulated by Federal Law dated July 21, 2005 N 94-FZ “On the placement of orders for the supply of goods, performance of work, provision of services for state and municipal needs.”

According to Part 1 of Art. 3 of Federal Law N 94-FZ, state needs are understood to mean the needs of the Russian Federation, state customers for goods, works, services necessary for the implementation of the functions and powers of the Russian Federation, state customers (including including for the implementation of federal target programs), for the fulfillment of the international obligations of the Russian Federation, including for the implementation of interstate target programs in which the Russian Federation participates, or the needs of the constituent entities of the Russian Federation, government customers for goods, works, services necessary for the implementation of the functions and powers of the constituent entities Russian Federation, government customers, including for the implementation of regional target programs.

State customers are government bodies (including government bodies), management bodies of state extra-budgetary funds, government institutions and other recipients of funds from the federal budget, budgets of constituent entities of the Russian Federation when placing orders for the supply of goods, performance of work, provision of services at the expense of budgetary funds and extra-budgetary sources of financing (Part 1, Article 4 of Federal Law No. 94-FZ).

Methods for placing an order are established in Part 1 of Art. 10 of Federal Law N 94-FZ.

A participant in placing an order can be any legal entity, regardless of the organizational and legal form, form of ownership, location and place of origin of capital, or any individual, including an individual entrepreneur (Part 1, Article 8 of Federal Law No. 94-FZ).

The state customer, the authorized body has the right, and if the contract price is over 50 million rubles. or the contract provides for an advance payment of more than 30%, they are required to establish a requirement to ensure the execution of the contract (clause 15.2, part 4, article 22, clause 9, part 4, article 34, clause 11, part 3, article 41.6 of Federal Law N 94-FZ). In this case, the specified security is provided by the ordering participant before concluding the contract in the form of an irrevocable bank guarantee issued by a bank or other credit institution, or a pledge of funds, including in the form of a deposit. The participant in placing an order independently chooses the method of ensuring the execution of the contract (Part 4, Article 29, Part 4, Article 38, Part 19, Article 41.12 of Federal Law No. 94-FZ, Letter of the Ministry of Economic Development of Russia dated June 21, 2011 No. D28-84).

In this case, security for the performance of the contract is provided in the form of a pledge of funds (by transferring funds to the bank account specified by the customer).

It should be noted that the norms of the Civil Code of the Russian Federation do not contain a direct prohibition on the use of funds as collateral (clause 1 of Article 336, clause 2 of Article 130 of the Civil Code of the Russian Federation). At the same time, according to the position of the Presidium of the Supreme Arbitration Court of the Russian Federation, funds cannot be the subject of pledge. This position is based on the fact that satisfaction of the pledgee’s claim at the expense of the pledged property occurs through the sale of this property (Articles 334, 349, 350 of the Civil Code of the Russian Federation), and non-cash funds, due to their nature, cannot be realized (Information letter of the Presidium of the Supreme Arbitration Court RF dated 01/15/1998 N 26 “Review of the practice of considering disputes related to the application by arbitration courts of the norms of the Civil Code of the Russian Federation on pledge”, Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated 07/02/1996 N 7965/95).

However, since Federal Law N 94-FZ establishes this method of securing the contractor, the organization has the right to choose it and transfer the established amount to the bank account specified by the customer.

Please note that the deadline for the return of funds transferred as collateral is not established by Federal Law No. 94-FZ. In this case, you should be guided by the norms of the Civil Code of the Russian Federation on pledge (Part 1, Article 2 of Federal Law No. 94-FZ). The amount of the deposit is returned to the organization after proper fulfillment of obligations under the contract (clause 3 of Article 352 of the Civil Code of the Russian Federation).

Value added tax (VAT)

Depositing funds as security for the performance of a contract and their return do not entail any tax consequences for VAT. This is due to the fact that these funds are not associated with the sale of goods (work, services).

Corporate income tax

Funds contributed as collateral and subject to return to the organization are not taken into account as expenses for profit tax purposes, regardless of the method used in tax accounting for recognizing income and expenses (clause 1 of article 252, clause 32 of article 270 of the Tax Code of the Russian Federation) . When these funds are returned, there is no economic benefit and, therefore, no income for the organization (Article 41 of the Tax Code of the Russian Federation).

Accounting

The amount of money contributed as security for the execution of the contract is subject to return to the organization upon its execution. Consequently, such an amount is not recognized as an expense for accounting purposes and is reflected in accounts receivable (clauses 2, 16 of the Accounting Regulations “Organization's Expenses” PBU 10/99, approved by Order of the Ministry of Finance of Russia dated May 6, 1999 N 33n). Thus, when transferring funds to the account specified by the state customer in the organization’s accounting records, an entry is made in the debit of account 76 “Settlements with various debtors and creditors” and in the credit of account 51 “Settlement accounts”. At the same time, the specified amount of funds is also reflected in off-balance sheet account 009 “Securities for obligations and payments issued” (Instructions for the application of the Chart of Accounts for accounting financial and economic activities of organizations, approved by Order of the Ministry of Finance of Russia dated October 31, 2000 N 94n).

When the customer returns the funds, the amount of the issued collateral is debited from the specified off-balance sheet account.

The return of funds does not lead to the formation of income for the organization and is reflected in the accounting records as an entry in the debit of account 51 and the credit of account 76 (clause 2 of the Accounting Regulations “Income of the Organization” PBU 9/99, approved by Order of the Ministry of Finance of Russia dated May 6, 1999 N 32n, Instructions for using the Chart of Accounts).

Source: Journal “Institutions of physical culture and sports: accounting and taxation”

In accordance with paragraph 1 of Art. 96 of Law No. 44-FZ in the notice of procurement, procurement documentation, draft contract, invitation to participate in the selection of a supplier (contractor, performer) in a closed way, the customer must establish a requirement to ensure the execution of the contract, with the exception of certain cases. What are the methods of this provision? In what order is security for the performance of a contract provided and how are these transactions reflected in accounting? Can the customer withhold the amount of security previously provided by the contractor against the unreturned advance payment under the contract? You will find answers to these and other questions in the article.

According to clauses 4, 5 of Art. 96 of Law No. 44-FZ, a contract is concluded only after the procurement participant with whom the contract is concluded provides security for the execution of the contract. If a participant fails to provide security within the period specified for concluding the contract, such participant is considered to have evaded concluding the contract.

Accounting for payment of contract security

In this case, the security, at the choice of the procurement participant, can be either the deposit of funds into the customer’s account or the provision of a bank guarantee. In the article we will dwell in detail on the method of ensuring the execution of a contract, when a procurement participant deposits funds into the customer’s account. General provisions According to the general rules, the condition for ensuring the execution of the contract must be established by the customer in the notice of procurement, procurement documentation, project

Accounting for payment of contract security

d.) for improper fulfillment of obligations under the contract. That is, at the moment the organization itself recognizes the sanctions or at the moment the court decision enters into force, if the organization is obliged to make such an offset by a court decision.

However, accountants already have to keep large amounts of information in their heads, therefore, to simplify the task, basic information about securing applications is presented in the form of a diagram (click on the picture to enlarge). Please note: providing security for an application is not an expense, but merely a “freezing” of funds for a certain time.