For more than 7 years, there has been a mandatory pre-trial procedure for appealing decisions of tax authorities on desk and field audits. How and within what time frame to draw up objections to an on-site tax audit report will be discussed in this article.

No later than two months from the date of drawing up a certificate of an on-site tax audit, an act is drawn up, and based on the results of an on-site tax audit of a consolidated group of taxpayers - within three months (Clause 8 of Article 89 of the Tax Code of the Russian Federation).

The report is drawn up even if the tax inspectorate did not reveal any violations during the audit. The form of the act was approved by order of the Federal Tax Service of the Russian Federation dated 05/08/2015 No. ММВ-7-2/ [email protected]

TAX DISPUTE RESOLUTION

The act is handed over to the official (or his representative) in respect of whom an on-site tax audit was carried out within five days from the date of its preparation, and when conducting a tax audit of a consolidated group of taxpayers - within 10 days from the date of its preparation (clause 5 of Article 100 of the Tax Code RF). If sent by mail, the date of delivery of the act is considered to be the sixth day counting from the date of sending the registered letter.

The tax audit report must be accompanied by documents confirming violations of the legislation on taxes and fees identified during the audit (clause 3.1 of Article 100 of the Tax Code of the Russian Federation).

Having received the report, the taxpayer may not agree with the results of the on-site tax audit.

Important!

Failure to comply with the pre-trial procedure for appealing acts of visiting tax authorities is grounds for leaving the taxpayer’s application in court without consideration (decision of the Khabarovsk Territory AS dated February 15, 2016 No. A73-17478/2015, determination of the Arbitration Court of the Samara Region dated June 17, 2015 No. A55- 11027/2015).

Thus, before legal battles, the taxpayer must go through a pre-trial appeal procedure.

WHEN CAN A TAX AUDIT COME TO YOU?

Writing order

Disagreement is expressed both with respect to the entire act and with respect to its individual provisions. At the legislative level, the form of an objection to a tax audit report has not been established, but general requirements for the content have been established. The text indicates:

- name and address of the Federal Tax Service;

- details of the document to which the response is written (date and number);

- legal position and basis;

- an appendix indicating the list of documents to be sent;

- FULL NAME. person authorized to sign.

For the document, we use a formal business style of writing. When disclosing your legal position, you should avoid unaccepted abbreviations of words or initially indicate the meaning of the abbreviation. When preparing the text part of the document, practice on this issue is studied. If you come across similar cases with a positive decision, make the appropriate links and mention it. A controversial situation may contain mitigating circumstances for objecting to a tax audit report or precluding prosecution. Emollients include:

- committing an offense due to official dependence or as a result of coercion;

- independently identifying errors and asking for their correction;

- the offense was committed for the first time;

- conscientious payment of taxes for previous periods;

- difficult financial situation of the company.

The official websites of the Federal Tax Service contain an example of an objection to a tax audit report; the use of the form is for informational and advisory purposes only. The list of mitigating circumstances is not exhaustive and is determined based on the totality of all the circumstances of the case. The same action under certain circumstances is qualified differently in different cases.

Objections to the on-site tax audit report: deadlines and procedure

If the taxpayer does not agree with the conclusions set out in the on-site tax audit report, then at the first stage he needs to draw up written objections to the specified act (clause 6 of Article 100 of the Tax Code of the Russian Federation, letter of the Federal Tax Service of the Russian Federation dated August 7, 2015 No. ED-4- 2/13890).

Important!

A tax audit act is not a non-normative act of the tax authority, on the basis of which the taxpayer has an obligation to pay taxes and cannot be an independent basis for applying to the court with a demand for inclusion in the register of debts for the payment of taxes, penalties, fines (determination of the AS of the Altai Republic from 02/19/2016 No. A02-1081/2015).

REASONS FOR APPOINTING ON-SITE TAX INSPECTIONS

How to calculate the expiration date for filing written objections to an act?

According to the rules of Article 6.1 of the Tax Code of the Russian Federation, deadlines calculated in months expire on the corresponding month and day of the last month of the period. The article contains two clauses regarding the expiration date:

1) If there is no corresponding date in the month of expiration (for example, the 31st day, or “the end of February”), in such a month the period calculated in months ends on the last day of the month.

2) If the last day of the period falls on a weekend, non-working day, or holiday, the end of the period is considered to be the first working day following them.

Taking into account the rules of Part 6 of Article 100 of the Tax Code of the Russian Federation, it is possible to file objections to a tax audit report within one month, therefore, the period for objections to a tax audit report expires next month on the calendar date following the date of the month of delivery of the act.

For example:

The desk tax audit report was handed over to the taxpayer on December 28, 2021, taking into account the above rules of Articles 6.1 and 100 of the Tax Code of the Russian Federation, the deadline for objections to the report expires on January 29, 2021.

If the desk tax audit report was delivered to the taxpayer on January 29, 2021, taking into account the above rules of Articles 6.1 and 100 of the Tax Code of the Russian Federation, the deadline for objections to the report expires on March 1, 2021. (The period must expire on February 29, 2021, but this date is not available in 2021, therefore, the month period expires on the first following business day).

EXAMPLE No. 1

The taxpayer received an on-site tax audit report on May 30, 2016. The deadline for filing objections to the received report is no later than June 30, 2021.

The taxpayer has the right to attach to written objections or, within the agreed period, submit to the tax authority documents (their certified copies) confirming the validity of his objections (clause 6 of Article 100 of the Tax Code of the Russian Federation).

Written objections and supporting documents are sent to the tax office that conducted the audit (clause 6 of Article 100 of the Tax Code of the Russian Federation).

Objections can be served in person or sent by mail. Then the period (month) will be counted from the seventh day from the moment of sending the registered letter (clause 5 of Article 100 of the Tax Code of the Russian Federation).

SERVICES IN THE ARBITRATION COURT

Submitting objections

To draw up and submit objections, the taxpayer is given 15 working days from the date of receipt of a copy of the desk audit report (Article 100 of the Tax Code of the Russian Federation). The period for submitting objections is calculated from the day following the day when you received the desk inspection report (Clause 2, Article 6.1 of the Tax Code of the Russian Federation). If the taxpayer does not show up for the report, evades receiving it, etc., then 15 days will be calculated starting from the seventh day after the date the report was sent by mail (paragraph 2, paragraph 5, article 100, paragraph 2, article 6.1 of the Tax Code RF). You can submit objections on any day, including the last. But, of course, it’s better not to delay. Objections are submitted to the tax authority, which carried out the inspection and drew up the corresponding act. Objections are considered within 10 days (clause 1 of article 101, clause 6 of article 6.1 of the Tax Code of the Russian Federation).

Note. If it is not possible to submit the document simultaneously with objections, then you can agree on the deadline for their submission with the Federal Tax Service (Clause 6 of Article 100 of the Tax Code of the Russian Federation). Strictly speaking, approval is not necessary, since the tax authority, when making a decision, is obliged to take into account all the materials it has (clause 1 of Article 101 of the Tax Code of the Russian Federation).

It is more advisable to prepare objections in two copies - one remains with the Federal Tax Service Inspectorate, the other, with a mark from the office of the Federal Tax Service Inspectorate (reception mark, date of reception, signature and full name of the person who accepted) - with the taxpayer. You should not send objections to the desk audit report by mail, since there is a possibility that the Federal Tax Service of Russia will not receive them before a decision is made based on the results of the audit. Unfortunately, the Tax Code of the Russian Federation does not provide for the possibility of extending the deadline for submitting objections. The period during which the head of the inspection (his deputy) must make a decision is counted from the end date of the 15-day period for filing objections (clause 1 of Article 101 of the Tax Code of the Russian Federation). However, objections filed after the deadline, but before a decision is made based on the results of the inspection, must be taken into account when making a decision. That is, in any case, the taxpayer retains the right to give his explanations during the consideration of the materials of the desk audit (clause 4 of Article 101 of the Tax Code of the Russian Federation). That is, you can present your arguments when appealing a decision based on the results of a desk audit to a higher tax authority or court.

Filing an objection to an on-site tax audit report

There is no legally established form for filing objections to a tax audit report, and there are no clear requirements for the content of objections. However, a certain procedure that has developed in practice should be observed.

The written objections contain the general part:

- taxpayer details (TIN, KPP, registration address, etc.);

- date and place of submission of objections;

- start and end dates of the audit;

- period of inspection;

- the name of the taxes in respect of which the tax audit was carried out.

This is followed by the content:

- specific points of the audit report with which the taxpayer does not agree;

- legislative justification for objections (links to the norms of the Tax Code of the Russian Federation, letters from the Ministry of Finance of the Russian Federation posted on the official website of the Federal Tax Service of the Russian Federation);

- established arbitration practice on this issue.

Important!

The last point of the content of the objections is very important, since the tax service, when considering objections to tax audit acts and complaints against decisions, is recommended to take into account the established arbitration practice in the region on this topic (letter of the Federal Tax Service of the Russian Federation dated May 11, 2007 No. ШС-6-14 / [email protected] ).

Registration of objections

Having studied the inspection report and identified the points with which you do not agree, you can begin to directly draw up the objections themselves. There is no approved form for drawing up objections, so complete freedom of thought is provided here. However, there are still some design guidelines.

This is interesting

Objections can be filed not only to the inspection report as a whole, but also to its individual parts.

First of all, it is necessary to indicate to whom these objections are addressed: in the upper right corner it is reflected in whose name the objections are written, indicating the position and surname. It should also be noted to which tax authority the objections were specifically submitted (full name, address). Next, it is indicated from whom the objections are submitted (full and abbreviated name of the organization, tax identification number, checkpoint and address). If objections are submitted by an individual or individual entrepreneur, then initials, surname, TIN and registration address are indicated.

Further, in the center of the sheet, it makes sense to write the following phrase:

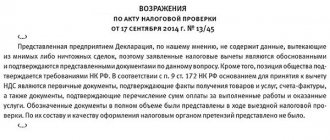

“Objections to the cameral (on-site) inspection report No.... dated...”

Although writing objections is to some extent a creative process, it is advisable to start it by stating some facts. To do this, we recommend using the following wording: “As a result of a desk (on-site) tax audit, an act No. ... dated ... was drawn up in relation to (indicate the name of the taxpayer). Based on the results of this act, the Company (individual entrepreneur) was asked to pay arrears of taxes (fees) in the amount of ..., penalties accrued on it in the amount of ..., as well as fines in the amount of .... These proposals are based on the inspection materials and conclusions reflected in the report. We believe that these conclusions are based on facts that do not reflect the actual circumstances of the case, and also do not correspond to the reality and provisions of the legislation on taxes and fees, for the following reasons.”

Next, the specific point of the audit report with which the taxpayer does not agree is indicated. After this, reasonable and, if possible, documented arguments are given. When presenting your arguments, you should not “overload” the text with quotes from the Tax Code or other laws; it will be enough to make a link to a specific article.

If you need to attach any documents to your objections, you must adhere to the requirements of Article 93 of the Tax Code.

That is, it is necessary to submit duly certified copies of these documents. In this case, all documents are folded into a single pile and stitched. Next, you should put numbers on each page, and on the last sheet of the binder, on the back side, stick a tag with the following text: “Copy is correct.

Numbered and laced on... sheets and date.” The tag is sealed with the seal of the organization (individual entrepreneur), signed by the manager and dated. It must be remembered that tax authorities do not have the right to demand notarized copies of documents unless this is expressly provided for by law.

At the end of presenting reasonable arguments, it makes sense to put forward your demands.

In other words, you need to make an entry with the following content: “Taking into account the above, as well as the documents presented, we ask you to cancel the tax audit report No. ... dated ... (or those points of the act with which you do not agree), as well as the assessment of taxes in the amount of ... and the corresponding amounts penalties and fines."

After drawing up written objections, they should be submitted to the relevant tax authority that conducted the audit. There is no need to rush to do this in the first days of the allotted fifteen. This is because the sooner you submit them, the more time inspectors will have to study them. Therefore, they will be better prepared to challenge the validity of your arguments. And here there is a little trick.

According to paragraph 8 of Article 6.1 of the Tax Code, an action for which a deadline has been established can be performed before 24 hours of the last day of the deadline. That is, you can send objections to the inspectorate until midnight of the last day allotted for submitting objections. In addition, objections can be sent by registered mail with a list of attachments. In this case, the tax authority will receive them only after a few days. Consequently, he will have less time left before making a decision, and he will also need to study your arguments and take them into account, which will be objectively more difficult to do in a time crunch.

But there is also a downside to such actions. Based on the results of consideration of the case materials, the head of the tax authority may decide on additional tax control measures. In this case, the final decision will be delayed for a month.

It is important

If taxpayers' arguments do not have any justification, they are simply not subject to consideration by inspectors.

Time limits for consideration of objections to the on-site tax audit report

Written objections to the tax audit report must be considered by the head (deputy head) of the tax authority that conducted the tax audit, and a decision on them must be made within 10 days from the date of expiration of the deadline for submitting objections (and not from the day the taxpayer actually submits objections to the act checks).

This period may be extended, but not more than by one month (Clause 1, Article 101 of the Tax Code of the Russian Federation).

The tax authority is obliged to notify the taxpayer of the date, place and time of consideration of the audit materials.

Based on the results of consideration of the submitted objections, the head (deputy head) of the tax authority makes a decision:

- on bringing to responsibility for committing a tax offense. When checking a consolidated group of taxpayers, the said decision may contain an instruction to hold one or more members of this group liable;

- on refusal to bring to justice for committing a tax offense (clause 7 of Article 101 of the Tax Code of the Russian Federation).

Moment of receipt of the act

Almost every organization knows that an audit of financial and economic activities is underway, after which a report will be drawn up. Thus, during a desk audit, the report is drawn up within 10 days from the date of completion of the audit, and during an on-site audit, within two months after signing the certificate of the on-site tax audit.

After drawing up the act, it must be signed by the persons who conducted the inspection, as well as by the person in respect of whom it was carried out (or his representative). By and large, no one can force you to sign the act, but if you refuse, then a corresponding note is made in it. Usually it sounds like this: “The person in respect of whom the inspection was carried out (his representative) refused to sign the act.” In this case, particularly meticulous inspectors may involve third parties to attest to this fact. It is worth understanding that, although no liability is provided for failure to sign the act, such behavior may indirectly indicate the taxpayer’s dishonesty. So you can and should sign the act, since such behavior in the future will not cause tax officials to have a biased attitude towards you. According to paragraph 5 of Article 100 of the Tax Code, the act must be delivered to the person being inspected (his representative) within five days from the date specified in the act. Typically, a copy of the act is handed over at the time of its signing, if a representative of the organization came to the inspection in person. However, circumstances may arise when representatives, for various reasons, cannot or do not want to receive it. In such cases, this document must be sent by registered mail with acknowledgment or transmitted in another way that allows you to accurately determine the date of receipt.

Let us note that the confrontation with the tax authorities begins already at the stage of delivering the inspection report. This is where it is necessary to clearly monitor all procedural violations of controllers, since in the end they can be decisive. Thus, if there is a significant violation of the procedure for considering audit materials, as well as the procedure for collecting evidence, the decision of the tax authority may be canceled either in its entirety or in a separate part. At the same time, you should not rush to make claims to the tax authorities on these grounds, since it is always good to have a spare “trump card up your sleeve.” This is explained by the fact that most procedural errors of inspectors can be eliminated during the review of the inspection materials. For this purpose, the head of the inspection (his deputy) may decide to carry out additional tax control measures. But at the stage when the decision on the inspection report has already been made and the inspectors will not be able to correct anything, it is possible to lay out a “wild card”: if the essential conditions of the procedure for considering the act and other materials of tax control measures are violated, this is grounds for canceling the decision by a higher tax authority or court. Such essential conditions include ensuring the opportunity for the person in respect of whom the act was drawn up to participate in the process of reviewing the materials.

In this regard, the date of receipt of the act is of great interest, since this day is the starting point for the beginning of calculating the period for filing objections, the period for considering the case and making a decision on it. That is, all subsequent stages, and in some cases, the outcome of the case, depend on the moment of receipt of the act.

So, if the inspection report is sent by mail, the date of its receipt is considered to be the sixth day from the date of sending. But, given how “properly” the post office works, organizations may receive the certificate a few days later. This is where confusion begins in the timing of the consideration of the case, which can be beneficial to the person being audited. And in order to understand how to benefit from this situation, it is necessary to recall all the deadlines for the stages of reviewing audit materials, and also consider an example.

Thus, from the moment the organization receives the act, it has 15 working days (in the case of drawing up an act on the discovery of facts, the period for filing objections is 10 working days) to familiarize itself with the act and, in case of disagreement, submit written objections. After this 15-day period, within 10 working days, the inspection report must be reviewed by the head (his deputy) of the inspection and a reasoned decision must be made. At the same time, the tax authority must ensure the opportunity for the taxpayer to participate in the consideration of materials. To do this, he is sent a notice indicating the place, date and exact time when the commission will consider the act. Usually the commission is appointed for the first three days out of ten allotted for making a decision. The decision can be made on any of the ten days, and not specifically on the tenth. That is, it can be accepted on the first day after the period allotted for filing objections. In this case, it is not allowed to make a decision before the required 15 days have expired, since this may be regarded as a significant violation of the terms of the review procedure with all the ensuing consequences.

It is important

When signing the act, be sure to check the date, that is, when it was drawn up.

The fact is that controllers often “sin” and indicate in it not the current date, but the past one. Example

An organization was sent a desk tax audit report by mail on February 1, 2012. According to paragraph 5 of Article 100 of the Tax Code, the act will be considered received on the sixth day from the date of sending, that is, February 8, 2012. In fact, the act was received on February 10, 2012. Mistakenly believing that the report was received on February 8, 2012, the inspectors calculated the deadline for filing objections as March 1, 2012. Consequently, on March 2, the taxpayer was invited to review the materials, to which he did not appear. The head of the inspection, having established the fact that the taxpayer was notified of the consideration of the case and his failure to appear, decided to carry out this procedure in the absence of representatives of the company. Based on the results of consideration of the materials on the same day, a decision was made on February 2, 2012 to hold the taxpayer accountable. However, since the act was actually received on February 10, 2012, the last day for filing objections will be March 3. Consequently, consideration of the materials should take place no earlier than March 5 and a decision can be made no earlier than this date. And since it was adopted on March 2, there is a violation of the essential conditions of the procedure for considering the case materials. That is, a higher tax authority or court may conclude that the organization was deprived of the opportunity to fully protect its interests. As a consequence, the decision can be canceled on formal grounds. In support of this conclusion, there is a letter from the Ministry of Finance of Russia dated July 15, 2010 No. 03-02-07/1-331 and resolutions of the Federal Antimonopoly Service of the Moscow District dated January 23, 2009 No. KA-A40/12029-08 and January 23, 2009. No. KA-A41/ 12979-08.

Composition of data in objections

There is no objection form available. The document must indicate information about the recipient, applicant and the subject of disagreement. The use of company letterhead is permitted.

| Intelligence | Composition of information | Location in the text |

| Recipient details | Name of the Federal Tax Service Inspectorate, position, surname, initials of the head to whose name the objections are submitted | Preamble of the document |

| Information about the applicant organization | Name of organization, INN/KPP, OGRN, location address, telephone | Preamble |

| Information about the applicant - individual entrepreneur | Last name, first name, patronymic in full, registration address, telephone number | Preamble |

| Name | “Objections to tax audit report No. __ dated ____” | Centered after the preamble |

| Verification data | Who carried out the inspection, period, number and date of the report | Introductory part |

| Subject of appeal | Arguments, arguments with reference to legal norms | Descriptive part |

| The essence of the appeal | Conclusions and request to review the position of the Federal Tax Service | Final part |

| Proof | List of attached documents | Applications |

When drafting a document, you must follow the rules of business writing.

Appealing the desk inspection report

A desk audit, unlike an on-site audit, is carried out without notifying the organization being audited. In cases where violations of tax legislation are detected, based on the results of the audit, a tax audit report is drawn up, which is transferred to the taxpayer company no later than 10 days after the completion of the desk audit.

There are cases when an organization does not receive an inspection report. In this case, if the company’s management can prove that the reason for not receiving the document is valid, for example, the fiscal authority did not notify that after an inspection of the enterprise an act was drawn up, and the postal item was lost, they have the opportunity to restore the deadline for challenging the act. If the taxpayer was deprived of the opportunity to submit objections to the audit report due to the fault of the tax authority, this may become a basis for canceling the tax authority’s decision on such an audit.

There are often cases when taxpayer organizations avoid receiving the report in every possible way. That is, they know that such an act has been drawn up, but they do not pick it up themselves and avoid receiving the mail. In this case, the date of receipt of the act will be considered the sixth day after sending it by registered mail. As a result, the tax audit report is considered delivered and comes into force within the time limits established by law.

This is important to know: Statute of limitations for theft

But even in this case, the company can challenge the decision that has entered into force by appealing to a higher organization with an appeal within a month from the date of receipt of the decision or with a regular complaint - within a year after the inspection decision is made.