Estimate

| Reviews: | 0 | Views: | 2718 |

| Votes: | 0 | Updated: | n/a |

File type Text document

?

Ask a question Remember: Contract-Yurist.Ru - there are a bunch of sample documents here

ACT OF INVENTORY OF SETTLEMENTS WITH BUYERS, SUPPLIERS AND OTHER DEBITORS AND CREDITORS FORM NO. INV-17 ______________________________ (enterprise, organization) Form No. inv-17 Approved by Decree of the USSR State Statistics Committee dated December 28, 1989 No. 241 +————+ OKUD code ¦ 0309016 2 ¦ +————¦ INVENTORY ACT OF SETTLEMENTS +———————————-¦ WITH BUYERS, ¦Number ¦ Date ¦ ¦ ¦ SUPPLIERS ¦document ¦ compilation¦ ¦ ¦ AND OTHER DEBITORS +———+————+——+——¦ AND CREDITORS ¦ ¦ ¦ ¦ ¦ +———————————-+ Based on the order (instruction ) from "___"___________ 20___ No._______ an inventory of settlements with buyers, suppliers and other debtors was carried out as of “___”____________20___. During the inventory, the following was established: 1. For accounts receivable +——————————————————————————+ ¦ ¦ ¦ Balance amount ¦From the total amount- ¦ ¦Name ¦Account+————————————+ specified in ¦ ¦balance sheet items¦ ¦ ¦ including ¦column 3, number- ¦ ¦ ¦ ¦total+————— —————¦ all debt,¦ ¦ ¦ ¦ ¦debt,¦debt, ¦for which expired-¦ ¦ ¦ ¦ ¦confirmed- ¦not confirmed-¦la claim- ¦ ¦ ¦ ¦ ¦ by debtors¦ by debtors ¦ness ¦ +——————+—-+——+—————+—————+——————¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—————————-+—————+—————+——————¦ Total ¦ ¦ ¦ ¦ ——— ———————————————-+ Reverse side of form no. inv-17 2. For accounts payable +——————————————————————————+ ¦ ¦ ¦ Balance sheet amount ¦ From the total amount - ¦ ¦ Name ¦Account+————————————¦we, indicated in ¦ ¦balance sheet items¦ ¦ ¦ including ¦column 3, number- ¦ ¦ ¦ ¦total+———————— ——¦all debt,¦ ¦ ¦ ¦ ¦debt,¦debt, ¦for which expired-¦ ¦ ¦ ¦ ¦confirmation- ¦not confirmed-¦la claim- ¦ ¦ ¦ ¦ ¦ by debtors¦ by debtors ¦ +——————+—-+——+—————+—————+——————¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +————— ————-+—————+—————+——————¦ Total ¦ ¦ ¦ ¦ ——————————————————-+ Chairman of the commission ___________ ___________ _____________________ (position) (signature) (acting, last name) Members of the commission: ___________ ___________ _____________________ (position) (signature) (acting, last name) ___________ ___________ _____________________ (position) (signature) (acting, last name) ___________ ___________ _____________________ (position) (signature) (acting, last name) NOTES: ———- Enterprises can be recommended to carry out an inventory of property and financial obligations, specified in the Basic Provisions for Inventory , considering them as approximate: settlements with debtors and creditors - at least twice a year; The results of the inventory of settlements are formalized by an act of inventory of settlements with buyers, suppliers, other debtors and creditors, which lists the inventoried accounts and indicates the amounts of identified inconsistent receivables and payables for which the statute of limitations has expired. The act is drawn up in one copy by the inventory commission on the basis of the balances of amounts identified from the documents in the relevant accounts, signed and transferred to the accounting department.

Download the document “Form No. inv-17 act of inventory of settlements with buyers, suppliers and other debtors and creditors”

Certificate inv 17 for the inventory report sample

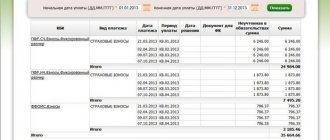

The table provides general data on debts, as well as supporting documents.

The basis for reference is primary accounting, which includes documents on accepted work, invoices, reconciliations, and invoices issued. It happens that several accounts serve as the basis. In this case, all numbers and dates are indicated in columns 8 and 9, although the amount for the counterparty remains total. — several payment orders for one debt Please note that the certificate does not define the final figures, since both debit and credit obligations are placed in the form.

If there are not enough rows in the table, you can increase their number by adding a row to the table. The same applies to the main act.

The certificate is a mandatory addition to the INV-17 act and serves as the basis for drawing up the inventory act itself. The certificate explains the amount of debt for each debtor and creditor, the reason for its occurrence, the date the debt arose, and its amount.

Unlike the inventory report, the certificate is drawn up in one copy and is also stored for five years.

Help and Application

In addition to the act itself, when reconciling settlements with suppliers and counterparties, a certificate is attached, on the basis of which the INV-17 act is subsequently drawn up.

In turn, the basis for drawing up the certificate is the data from the financial statements, which must contain all information about the debt and the amount.

After this, the debt is divided into three groups: confirmed by the debtor, unconfirmed by the debtor and expired debt. After filling out the certificate, the received accounting data is detailed in the INV-17 form.

However, there are no special legal requirements for filling out the INV-17 certificate. Those who are faced with the need to carry out this procedure for the first time will find the instructions for filling out the certificate for the INV-17 act useful.

Column 3 contains information about what the debt was received for. It may indicate a loan, products, services or other reasons for the debt.

Column 4 contains information about the exact date when the debt arose. This column must be filled out especially carefully due to the fact that the statute of limitations is calculated on the basis of this date, and when going to court, it may be impossible to collect the debt from the debtor.

In column 7, you must write down a document that confirms the existence of the debt. As such a document you can use:

- waybill;

- act on the provision of services or performance of work;

- an agreement that specifies the deadline for the counterparty to fulfill its obligations under the agreement;

- the amount of debt for the reporting period.

If situations arise where the statute of limitations had to be interrupted because a reconciliation act was being generated, it is necessary to indicate the reconciliation act as a supporting document and indicate the exact date when it was created.

Column 8 contains information about the date of generation of the document confirming the debt.

Documents for download (free)

- Form No. INV-17

- Completed form No. INV-17

How to fill out the form

Form INV-17 must be prepared by the inventory commission. The composition of this commission is determined by the head of the organization.

This document is generated in two copies. One copy remains with the commission, and the second is transferred to the chief accountant.

During the inventory of receivables and payables, it is necessary to conduct a verification analysis of transactions with funds, customers, suppliers, customers and employees.

Before you start filling out the INV-17 form, you need to create a certificate application. This help contains the following information:

- about creditors and other persons, indicating their contacts;

- reasons for debt;

- documents on which debts arose;

- date of occurrence of the debt;

- amount of debt.

The form and sample for filling out a certificate for form INV-17 can be found in the article.

After completing this certificate, you can begin filling out the act form. A sample act of inventory of receivables and payables is presented below.

The form consists of two pages. The first page displays information about accounts receivable, and the second - about accounts payable.

Filling out the first page involves providing the following information:

- name of the debtor;

- account number of accounting transactions performed with it;

- total balance for this debtor (third column);

- certified amount of debt (fourth column);

- uncertified amount of debt (fifth column);

- the amount of debt for which the statute of limitations has expired (sixth column).

If there is more than one debtor, information for each of them is filled out separately, and at the end the total is calculated.

The second page of the INV-17 settlement inventory act is filled out in the same order, only for accounts payable.

After completion of the registration, all members of the commission must put their signatures on the act.

Statute of limitations

As a general rule, the statute of limitations is three years. However, it can be increased or decreased. The duration of this period is determined in the following order:

- for obligations for which the deadline for fulfillment is clearly established - upon completion of the deadline for fulfilling this obligation;

- for obligations for which the fulfillment period is not established - from the moment the creditor makes a demand to fulfill the obligation.

Similar articles

- Statute of limitations for personal taxes

- Inventory report of receivables and payables (sample)

- Inventory of settlements with debtors and creditors

- Transport tax: statute of limitations

Sample filling

Form INV-17 is used when conducting a mandatory inventory of settlements with suppliers and counterparties in accordance with the Federal Law “On Accounting”. Responsibility for the correct implementation of this procedure lies with the inventory commission, which is selected by the general director.

https://www.youtube.com/watch?v=5EX6IbWzDMI

The difficulty is that many people involved in the process do not know what information should be contained in the INV-17. This document must indicate the following:

- Name of the company of the debtor and/or creditor, as well as contacts of the legal and actual address.

- Information about when and for what the debt was received, that is, how it was formed.

- The exact amount of debt to be written off.

- Documentary proof of availability.

Form INV-17 was approved by the State Statistics Committee of Russia in 1998 by the Resolution “On approval of unified forms of primary accounting documentation for recording cash transactions and recording inventory results.” Officially, since 2013, the use of the form is not a mandatory requirement.

We invite you to read: How to calculate compensation upon dismissal for an employee on maternity leave - Labor assistance

When conducting an inventory, a company can use a form developed independently. But many still continue to use this form when conducting inventory, since it contains all the necessary information.

The act is filled out by members of the inventory commission in two copies. One of them remains with the inventory commission, the other is sent to the company’s accounting department. At the same time, the act indicates not only companies, but also employees if they have incurred debts (salaries, vacation pay, maternity pay, etc.)

In addition to the act itself, when reconciling settlements with suppliers and counterparties, a certificate is attached, on the basis of which the INV-17 act is subsequently drawn up.

In turn, the basis for drawing up the certificate is the data from the financial statements, which must contain all information about the debt and the amount.

After this, the debt is divided into three groups: confirmed by the debtor, unconfirmed by the debtor and expired debt. After filling out the certificate, the received accounting data is detailed in the INV-17 form.

Column 3 contains information about what the debt was received for. It may indicate a loan, products, services or other reasons for the debt.

Column 4 contains information about the exact date when the debt arose. This column must be filled out especially carefully due to the fact that the statute of limitations is calculated on the basis of this date, and when going to court, it may be impossible to collect the debt from the debtor.

In column 7, you must write down a document that confirms the existence of the debt. As such a document you can use:

- waybill;

- act on the provision of services or performance of work;

- an agreement that specifies the deadline for the counterparty to fulfill its obligations under the agreement;

- the amount of debt for the reporting period.

If situations arise where the statute of limitations had to be interrupted because a reconciliation act was being generated, it is necessary to indicate the reconciliation act as a supporting document and indicate the exact date when it was created.

Column 8 contains information about the date of generation of the document confirming the debt.

Example

The INV-17 form consists of two parts, each of which is filled out when conducting an inventory of debts with suppliers and counterparties: the front part of the form and the back.

The first page of the act contains basic information about the enterprise, as well as the date, time and basis for the reconciliation; in addition, it is necessary to indicate the number of the act and the date of its preparation. In order for the form to be considered legal, the title page must indicate the company's activity code.

You can fill out the form by hand or with a pen with blue or black ink. After this, information about accounts receivable is recorded on the front side of the form, and data on relationships with creditors is recorded on the back side.

All members of the commission sign the form of the completed act, after which one copy is necessarily transferred to the accounting department, where the correctness of filling out the data in the INV-17 form will be checked.

After filling out the inventory report form, it must be stored in the archive for at least 5 years. Since INV-17 has not been mandatory for 4 years, filling it out for the first time may be fraught with certain difficulties.

As a rule, an inventory of payments by suppliers and counterparties is carried out so that the organization can have an idea of who owes it and how much, as well as to whom and what amount it owes, and after that it can develop measures aimed at both repaying its own loans and and for collection of accounts receivable.

We suggest you read: How and where you can write a complaint against Beeline: sample complaint

Accounts receivable become uncollectible when a business realizes that there is no likelihood of collection from the debtor. Accounts receivable may arise under the following circumstances:

- the borrower has not repaid the loan issued to him by the organization and does not take any action to repay it;

- a company employee misused funds that were given to him on account for the needs of the enterprise;

- the supplier received an advance, but the products were not shipped;

- the buyer did not pay for the goods that he received, the work performed by the supplier or the services previously provided.

Accounts receivable are subject to write-off under the following circumstances:

- expiration of the debt limitation period;

- impossibility of collecting a debt due to the fact that the statute of limitations has passed or the company has been liquidated.

The act of incurring debt on a loan is confirmed by the loan agreement. The amount of debt is determined by inventory and recorded in the act in the accounts payable section.

Accounts receivable can be written off based on the order. The fundamental documents for this procedure are the act and certificate for INV-17.

Accounts payable may arise in cases where:

- the company did not settle accounts with the counterparty (did not repay wage arrears, did not pay for shipped products, did not repay the loan);

- the company received an advance payment, and subsequently the products were not shipped.

By law, the period of claim for a debt lasts three years. In some situations established by law, the statute of limitations may be increased or, conversely, shortened. In such a situation, the following events may be the basis for calculating the limitation period:

- If the deadline for fulfilling obligations is clearly established, the debt can be written off immediately after the expiration of the claim period.

- If the deadline was not fixed, debts can be reset at the moment the creditor decided to collect the debt from the debtor and formally presented him with a demand for fulfillment of the obligation.

You can learn how to conduct an inventory of fixed assets in 1C from this video instruction.

act of inventory of settlements with suppliers and customers. Form and form INV-17

Sample of filling out the unified form INV-17 in 2021

Help supplement to form INV-17

Sample of filling out the certificate

Download sample forms for inventory at the enterprise: INV-1 Inventory listINV-1a Inventory list of intangible assets INV-3 Entering data into the inventory list INV-4 Inventory of shipped ]INV-5 Inventory of goods and materials accepted for storage[/anchor] INV-6 Inventory of goods and materials on the wayINV-15 Inventory of cash availability INV-18 Comparison sheet of inventory resultsINV-19 Comparison sheet of inventory items INV-22 Order for inventory INV-26 Accounting for inventory resultsHow is an inventory of materials carried out?

How is debt inventory carried out?

Before starting the inventory, employees who are financially responsible must present reconciliation reports to their counterparties. After this, the director of the company issues an order appointing an inventory commission. This body, through documentary checks, must verify the authenticity of the following information:

- accounts receivable and accounts payable;

- settlements with employees;

- settlements with accountable persons;

- settlements with control authorities;

- other payments made by the organization.

How to fill out the attachment to form INV-17

The structure of the document is constructed in such a way as to display the main points that ensure the functionality of the certificate and its ability to act as the basis for the preparation of the INV-17 act. The form includes a title part, a tabular part and a place for the signature of the responsible person.

The upper part of the application form implies the location of information regarding the full name of the business entity within which the need for the work of the inventory commission was initiated in terms of the control check of settlements with counterparties. Next, the structural unit of the enterprise where the implementation of the monitoring mission will take place must be specified. It is possible to leave the field blank and not indicate the structural unit.

The central field of the form contains the name of the document itself. The name is followed by the designation of the details of the act, the affiliation to which is included in the certificate in question (the date of preparation of the corresponding INV-17 act and its registration number are recorded). The purpose of the certificate, the effect of which is addressed to the above monitoring act, is also deciphered here.

Below is the date as of which this document was compiled. As a rule, an inventory is carried out without fail at the end of the year before filling out the annual accounting documentation, and also as necessary during the year.

Inventory report of receivables and payables sample

The State Statistics Committee of the Russian Federation, in Resolution No. 88 dated August 18, 1998, developed not only the form of the act itself used when reconciling obligations, but also approved the annex to it. However, neither the State Statistics Committee of Russia nor the Ministry of Finance of the Russian Federation have developed an official sample for filling out INV-17 in their Methodological Recommendations.

The first page of the document contains general information about the enterprise, its division, and also indicates the start and end of the reconciliation, its basis, the number and date of the act itself. To follow the procedure for filling out INV-17, the code of the type of activity of the enterprise should be reflected on the title page.

Filling out the form is done on a computer or with a black or blue pen.

After reflecting the specified data, information on receivables is entered into the act form.

The reverse side of the document form is intended to reflect information on relationships with creditors.

The data included in the act of inventory of settlements with buyers, sellers, debtors and creditors is certified by members of the commission.

The basis for drawing up the initial form is a certificate, which is an appendix to form No. INV-17, without which the inventory act cannot be considered issued in accordance with Russian legislation.

Information in the specified application is entered in accordance with the data of the synthetic accounting accounts of the enterprise.

We invite you to read: Article 159 of the Civil Code of the Russian Federation ➔ text and comments. Oral transactions.

Electronic requirements for payment of taxes and contributions: new referral rules

Recently, tax authorities updated forms for requests for payment of debts to the budget, incl. on insurance premiums. Now it’s time to adjust the procedure for sending such requirements through the TKS.

It is not necessary to print payslips

Employers are not required to issue paper payslips to employees. The Ministry of Labor does not prohibit sending them to employees by email.

Online cash registers in online stores

Depending on how the online store organizes payment for goods, it either needs to use cash register or not. For example, the seller will not have to issue a check if payment is made through a paying agent. A tax specialist explains the nuances of using cash register systems in online stores.

We send personal income tax to the budget from May vacation pay and benefits

May 31 is the deadline for transferring personal income tax on vacation pay and temporary disability benefits (including benefits for caring for a sick child) paid to employees in May.

The list and quantity of goods at the time of payment are unknown: how to issue a cash receipt

Who fills out the application to INV-17

When filling out the document form, you should pay attention to the reliability of the information recorded in it. Entering data in the appendix to the INV-17 act is assigned to the accountant of the enterprise in which inventory activities are planned for implementation. You can fill out the certificate in one of the following ways:

- handwritten text using strictly blue or black ink;

- using electronic printing means to publish the text of documents.

If the certificate is prepared correctly, the process of subsequent registration of the results of audit activities in the inventory report INV-17 will be completed correctly.

| ★ Best-selling book “Accounting from scratch” for dummies (understand how to do accounting in 72 hours) > 8,000 books purchased |

How is inventory carried out?

The procedure for conducting an inventory of receivables and payables was approved by order of the Ministry of Finance of the Russian Federation dated June 13, 1995 No. 49 (clauses 3.44-3.48). During the event, the inventory commission is obliged to:

- establish the correctness of the organization’s settlements with contractors, hired personnel, the state budget, and founders;

- determine the validity of debt for shortages and thefts listed in the accounting accounts;

- establish the real amount of receivables and payables (including those with an expired statute of limitations).

During the inventory, you need to check the account “Settlements with suppliers and contractors”

Special attention is paid to the analysis of information about goods that have already been paid for, but are still “on the road.” You should also study the status of settlements with suppliers for uninvoiced deliveries

An inventory of debt to employees involves identifying unpaid amounts of wages that are subject to transfer. They also analyze the amounts of overpayments to workers and the reasons for such overpayments.

When checking accountable amounts, members of the commission study the reports of accountable persons on advances issued. The amounts of advances issued for each accountant are checked.

It is imperative to clarify the amount of debt to the tax service and banks.

If, during the inventory, discrepancies were discovered in the amounts of debt between the organization’s data and the data of its counterparties, which had not been eliminated at the date of drawing up the balance sheet, each party shows in the balance sheet those amounts of debt that can be confirmed by accounting data. To resolve disagreements, you should contact the relevant authorities (arbitration court, etc.).

Valuation of accounts payable

First of all, the accounts on balance lines 60, 62 and 76 are compared with the contract data, the credit of which takes into account prepayments and advances received, unfulfilled obligations for purchased materials and goods (services provided and work performed), deposited salaries, VAT deductible, accrued for the amounts of prepayments and advances. Just as when assessing debits, data is verified with counterparties.

Debt analysis

Often the bulk of debts are obligations to credit institutions for loans. Therefore, the next important position is the credit of balance sheet accounts 66 and 67. Registers and documents received from credit institutions (extracts confirming payments, schedules), all contracts are analyzed. In addition to payments, the correctness of interest calculations is checked.

Debts on fees, insurance premiums and taxes are accounted for in accounts 68 and 69. To accurately determine their volume, requests are sent to the Federal Tax Service and the Pension Fund for the issuance of certificates or a reconciliation is carried out.

In the credit of account 70, the presence of salary debts is checked. Pay slips, cash registers, and payment orders are analyzed. Settlements with employees are also reflected in balance sheet lines 71 and 76 - these are unreimbursed advances issued to accountable persons and unpaid compensations. The credit of line 75 is also subject to verification. It reflects debts on dividends and shares.

Uncollectible accounts receivable

Accounts receivable may arise under the following circumstances:

- the borrower did not repay the loan that the organization issued to him;

- the company employee did not report on the amounts he received for reporting;

- the supplier has already received an advance payment, but has shipped the products to the buyer;

- the buyer did not pay for the goods supplied to him, services provided or work performed.

Accounts receivable in accounting must be written off in the following cases:

- after the statute of limitations has expired;

- in other cases when the debt becomes impossible to collect, for example, upon liquidation of the company.

Tags: asset, balance sheet, accountant, loan, tax, order, expense

Sample document:

Appendix to form N INV-17

Approved by Resolution of the State Statistics Committee of Russia dated August 18, 1998 N 88

___________________________________________________________________ organization ___________________________________________________________________ structural unit REFERENCE TO ACT N ______ FROM “__” ________ ____ Y. INVENTORY OF SETTLEMENTS WITH BUYERS, SUPPLIERS AND OTHER DEBITORS AND CREDITORS AS OF “__” __________ ____ Y. ——————————— ——————————— ¦But- ¦Name, address and ¦Numbers-¦Amount for-¦Document confirming¦ ¦measure ¦telephone number debit- ¦due- ¦debt- ¦debt- ¦ ¦po- ¦tor, creditor ¦debt, ¦nost ¦ ¦po- ¦ ¦rub. kop.+——————+ ¦row-¦ +——-+———+name- ¦number¦date¦ ¦ku ¦ ¦for ¦da-¦de- ¦creation¦ ¦ ¦ ¦ What? ¦ ¦ ¦ ¦ ¦ ¦ +—-+———————-+—+—+—-+—-+——-+——+—-+ ¦ 1 ¦ 2 ¦ 3 ¦ 4 ¦ 5 ¦ 6 ¦ 7 ¦ 8 ¦ 9 ¦ +—-+———————-+—+—+—-+—-+——-+——+—-+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—-+——————-+—+—+—-+—-+——-+——+—-+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—-+—— —————-+—+—+—-+—-+——-+——+—-+ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ +—-+———————-+ —+—+—-+—-+——-+——+—-+ ¦ ¦ ¦ ¦and ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦t. ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦d. ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ¦ ——+———————-+—+ —+—-+—-+——-+——+—— Accountant __________________ _________________________________ signature decryption of signature Print with reverse without heading part. Signature printed on the back.

Legislative and regulatory acts

- Federal Law No. 402 “On Accounting”.

- Regulation No. 34n of the Ministry of Finance of the Russian Federation on reporting in the accounting department.

- Resolution of the State Statistics Committee of the Russian Federation No. 88

Dear readers!

Our articles talk about typical ways to resolve legal issues, but each case is unique. If you want to find out how to solve your particular problem -.

It's fast and free!

Or call us by phone (24/7):

If you want to find out how to solve your particular problem, call us by phone. It's fast and free!

+7 Moscow,

Moscow region

+7 Saint Petersburg,

Leningrad region

+7 Regions

(free call for all regions of Russia)